TGL:CC - VAALCO Energy: The Merger News Wiped Out $50 Million

- VAALCO Energy announced a stock-for-stock merger with TransGlobe Energy.

- The target and acquirer were cheaply priced relative to their fundamentals, but the synergies from the deal appear elusive.

- The market didn't appreciate the announcement either and wiped out overnight $50 million, or 8%, of the companies' combined market cap.

- I don't think the deal itself destroys value, but investors may worry it is a precursor to more future growth capex and lower shareholder returns.

- Management should enunciate and quantify the synergies; a clear long-term framework for capital returns would also help.

VAALCO Energy, Inc. ( EGY ) made a splash when it announced on July 14 it would merge with TransGlobe Energy Corporation ( TGA ). VAALCO would acquire the shares of TransGlobe in a stock-for-stock deal; each TGA share would exchange for 0.6727 VAALCO shares, representing a 24.9% premium per TGA share. After the deal, VAALCO stockholders would own 54.5% and TransGlobe shareholders 45.5% of the combined company.

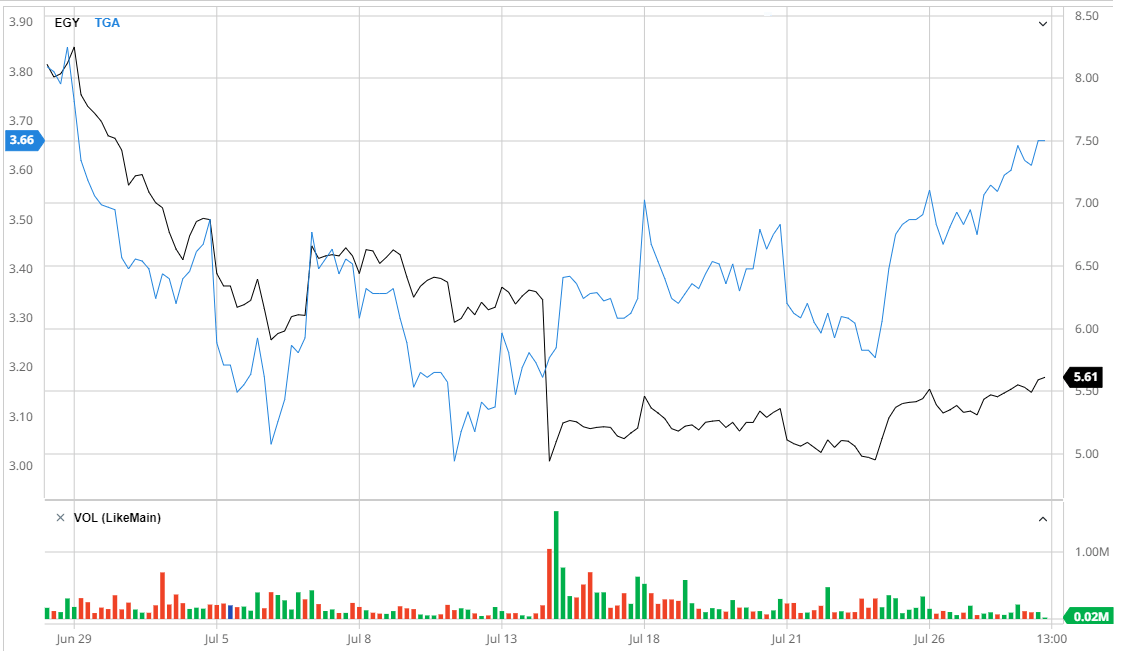

The market didn't like the news:

{kind=link}

EGY shares plunged 16% after the announcement while TGA only gained 5%. At the July 14 close, the combined market cap was $50 million lower compared to the day prior; this represents an 8% loss. It isn't unusual for the acquirer's shares to fall, but the drop in the combined valuation suggests the market may even see negative synergies.

While I agree the synergies haven't been articulated well, I think at worst they would be zero, but not negative. Rather, I suspect the market may be perceiving the scaling up as a sign the combined company could embark on a more ambitious growth agenda. Translation: more capex, less shareholder returns in the near term. The market reaction would then fit with other recent examples where oil companies chasing growth were penalized following an acquisitive event.

I remain bullish EGY, but only because we are coming out of a major correction in the energy sector; not because of the TGA deal.

VAALCO

I have covered EGY before and will refer to my prior article for more background. Here it suffices to say that VAALCO is a small oil player focusing on offshore Gabon with an undeveloped interest in neighboring Equatorial Guinea. Back in December, EGY was trading around $3 and was preparing for a capex-heavy 2022 to ensure maintenance of its production levels for the next decade.

While EGY is up a lot since then, I have remained bullish on the stock because the fundamentals have been getting better, too:

- My prior analysis assumed $65-$75 Brent price while Brent is now at $100.

- VAALCO has been reporting positive news from its drilling efforts and the results may even surpass expectations.

- If 2023 Brent averages $95, EGY can probably generate more than $200 million in free cash flow, assuming capex will fall after the 2021/2022 drilling campaign and ongoing FSO conversion are over.

- Even at EGY's peak price in early June, the implied EV/FCF multiple was only about 2.5 times.

TransGlobe Energy

TGA wasn't on my radar before the merger announcement, but it operates on a similar scale as EGY:

{kind=link}

Unlike EGY though, TGA focuses primarily on onshore interests in Egypt and derives a smaller portion of its production from Canada. TGA's last corporate presentation from June estimated $70 million in annual cash flow at $95 Brent, implying a 4x EV/ EBITDA multiple. It is less favorable than EGY, but one could still conclude both companies were considerably undervalued.

My take on the merger

Besides the proverbial "synergies", the other factors motivating the merge were "diversification" and "capital access." From the joint press release:

The Combined Company will have a larger, and more diversified reserves and production base, enhancing risk management, increasing portfolio optionality to high-grade and sequence investment projects towards the highest-return projects, as well as increasing access to a broader set of capital sources relative to each company on a standalone basis.

So we have "synergies", "diversification" and "capital access" as driving forces. I am somewhat skeptical of all three.

Synergies

I double checked Google Maps before writing the article, but Egypt is about 5,000 miles away from Gabon, not to mention Canada. The assets just don't seem naturally very synergistic:

{kind=link}

Sure, terminating the Toronto listing will save some costs; there could be some administrative and support function synergies, too. However, part of the savings will be offset by the one-time transaction costs. Operationally, it isn't so clear yet what will drive the synergy.

Diversification

Being focused only on offshore Gabon with the undeveloped interest in neighboring Equatorial Guinea, VAALCO is clearly subject to specific country risks. A combined company that derives half of its production from Egypt and a little bit from Canada will be less risky indeed.

But the question is less risky for whom? For management or for the shareholders? I personally don't have 100% of my portfolio allocated to VAALCO and it is reasonable to assume most shareholders are already diversified. Without real synergies, we are probably looking more to a GE-style diversification where autonomous businesses operate under the umbrella of a conglomerate. These structures add diversification for management, but aren't really incremental to the marginal investor who is already diversified.

Capital access

Being bigger and having more favorable access to the capital markets is usually a good thing. But why would the combined company need more capital? Logically, it must be to pursue growth opportunities, and this is why I think the market maybe reacted negatively.

Management naturally looks at the business long-term and expansion makes sense; that is how oil companies have always operated. Unfortunately, we live in strange times when the long-term future of oil is less certain, despite the current energy policy debacle in Europe as well as the U.S.

So the market doesn't really want oil companies to grow, but rather to enter some type of "tobacco mode" and start gradually liquidating themselves through cash distributions. We have seen other examples this year of companies that got penalized for perceived "empire building"; conversely, buybacks and special dividends have been rewarded handsomely.

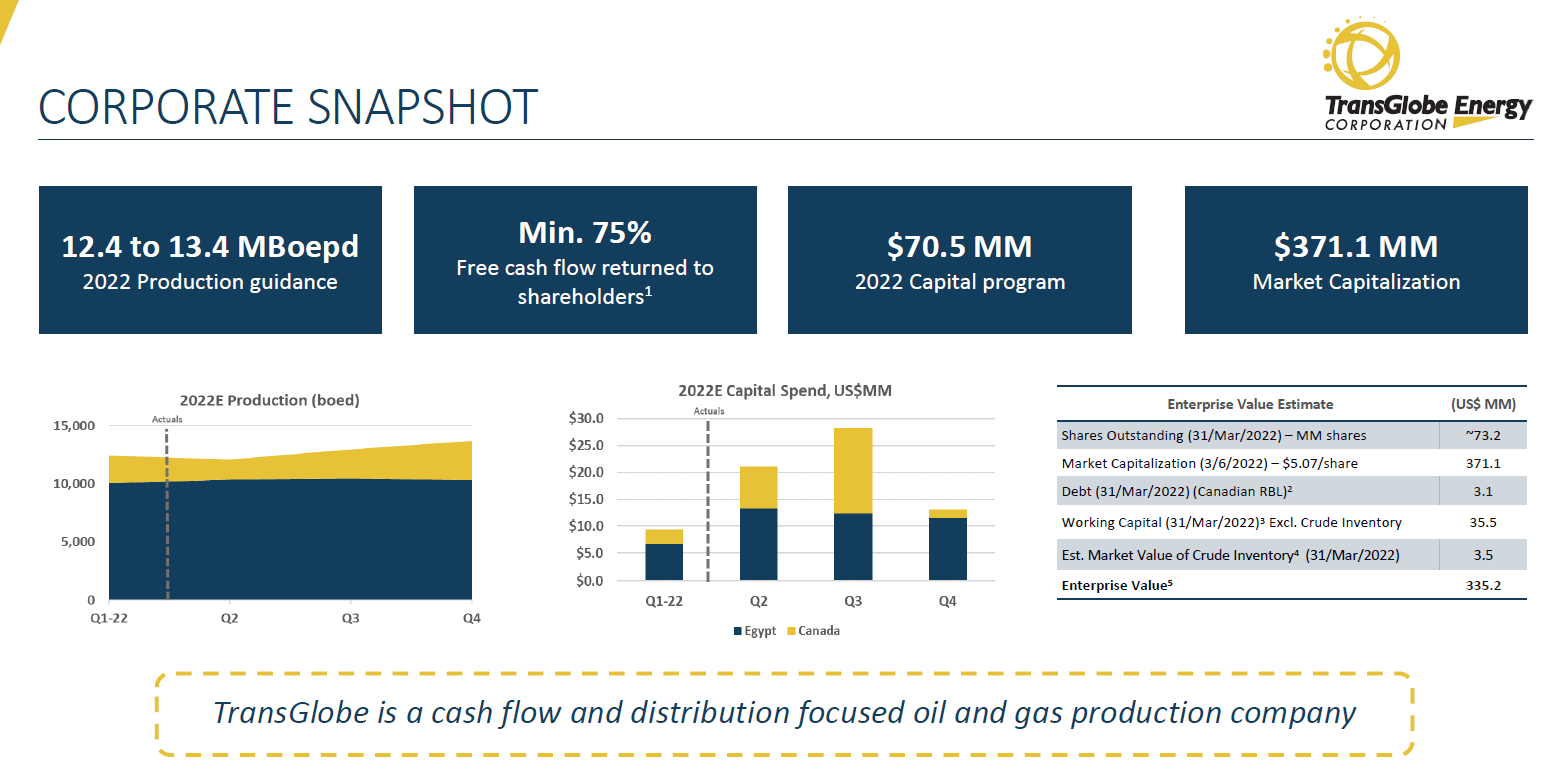

The pro forma combination deck boasts a $28 million dividend which is about 4% yield only. The market will likely need some longer-term guidance on the cash return strategy; one can get a 4% yield from Exxon Mobil ( XOM ) with much better diversification.

Were VAALCO shareholders short-changed?

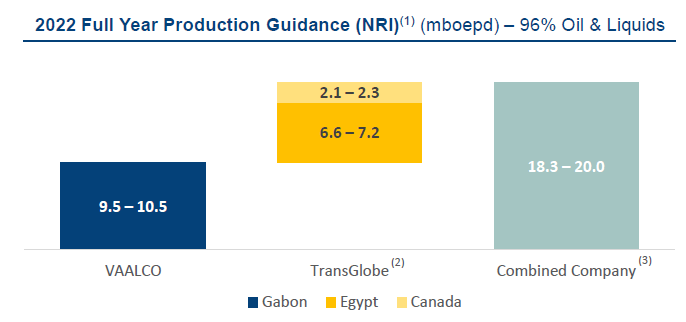

Probably not, at least not by too much. EGY does better on some metrics, but TGA looks better on others. Current production is roughly equal:

{kind=link}

TransGlobe is adding more reserves:

VAALCO & TransGlobe Energy Presentation

TGA's management projected $70 million in annual free cash flow ("FCF") at $95 Brent; I think VAALCO's normalized FCF would be at least $200 million with the same pricing assumption. I would also add that TGA's PSC in Egypt looks less favorable nominally, with up to 80% government take from profit oil (when Brent exceeds $100 and production is greater than 25,000 bbl/d). In VAALCO's case, Gabon would only take up to 60%, but EGY's PSC also includes a royalty. It is hard to compare fiscal regimes, though, when the cost structure is different anyway.

So, overall, it's a tough call to make. TGA's shareholders get more certainty through the 25% premium because it isn't clear if TGA's stock would have ever outperformed EGY relatively by more. But then TGA also gives up the upside if that had happened. Plus, if the market continues disliking the deal and discounting EGY's stock price, TGA's shareholders could even end up worse off in absolute terms. Relatively, though, I would argue EGY shareholders are getting the worse end of this.

What the market thinks

Now that we have two weeks of trading data after the announcement, we can get a better sense of how the market evaluates the deal too.

Between July 13 and 14, the combined market cap fell by $50 million or 8%. Not a good sign, and I already discussed my hypothesis.

The deal also established a theoretical price for TGA derived from EGY's price and the exchange ratio. Since July 14, TGA has traded at a volume-weighted average discount of about 4%. As a "merger arbitrage spread," this isn't an impressive number. Based on a research study I looked up, the average merger arbitrage spread in the broad sample studied was 6% with a standard deviation of 11%. I am led to conclude that the market thinks the deal will go through. There is also about a $9 million termination payment for each side which is not immaterial.

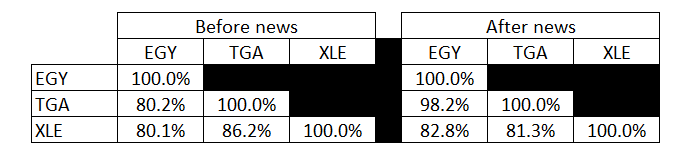

How about the stock price behavior relative to the broader energy sector? I computed the daily returns correlation matrix for the 30-day period prior to the news release and the two weeks since the announcement:

{kind=link}

I used the Energy Select Sector SPDR Fund ( XLE ) as benchmark.

EGY's correlation to the XLE hasn't really changed. TGA is now close to 100% correlated to EGY, which of course makes sense. Accordingly, TGA's correlation to XLE has also changed and now matches EGY's.

In other words, changes in how the market perceives the energy sector affected EGY similarly before and after the merger news. The price drop on July 14 was a one-time (negative) adjustment to reflect the news.

Since July 14, the combined market cap has almost come back to the pre-news level, with 7.4% gain through July 27. But the XLE moved up 10.7%, so the negative impact of the merger news persists.

The takeaway

EGY and TGA shareholders probably each have reasons to debate who got the worse end of this deal, but at this point it is pretty much water under the bridge. We have two weeks of data, which shows a modest merger arbitrage spread, as TGA's stock now tracks EGY very closely based on the exchange ratio.

Looking ahead, EGY and TGA shareholders have the same choice to make, namely, do they want to hold the EGY (combined company) stock long-term or not. For me, as a VAALCO shareholder, I see it as follows:

- I tend to agree with market's penalty of $50 million on the combined market cap. Pooling disparate assets together doesn't destroy value, but it does maybe signal more aggressive growth ambitions at the expense of shareholder returns.

- However, the news came on top of a 30% correction of the broader energy sector that had nothing to do with the merger news. That is, EGY fell from $8.60 to $6.23 on the industry downtrend alone, and the merger knocked it down further from $6.23 to $5.20. Given we now seem to be coming out of this huge correction, I think a "buy" rating is still appropriate.

In summary, just as the market, I am not happy with the merger, but I think given the macro picture it makes sense to stay long EGY or TGA for the time being, depending on what you own.

Longer term, I personally would want to hear more detail on the "synergies" and how the company plans to return cash to the shareholders. As much as I am bullish on oil, I feel 2022 may be a bit late for investing into "growth" oil companies.

For further details see:

VAALCO Energy: The Merger News Wiped Out $50 Million