VAL - Valaris Limited: Fleet Expansion And Market Dynamics Bolster Investment Thesis

2023-11-21 08:05:18 ET

Summary

- Valaris reported improved day rates and added to its contract backlog, despite revenue stabilizing over the past six quarters.

- Valaris is poised to add two drillships to its fleet before the end of 2023, enhancing its revenue-generating capacity in 2024 and beyond.

- Valaris remains inexpensive in an offshore drilling market marked by increasing demand and constrained supply of rig capacity.

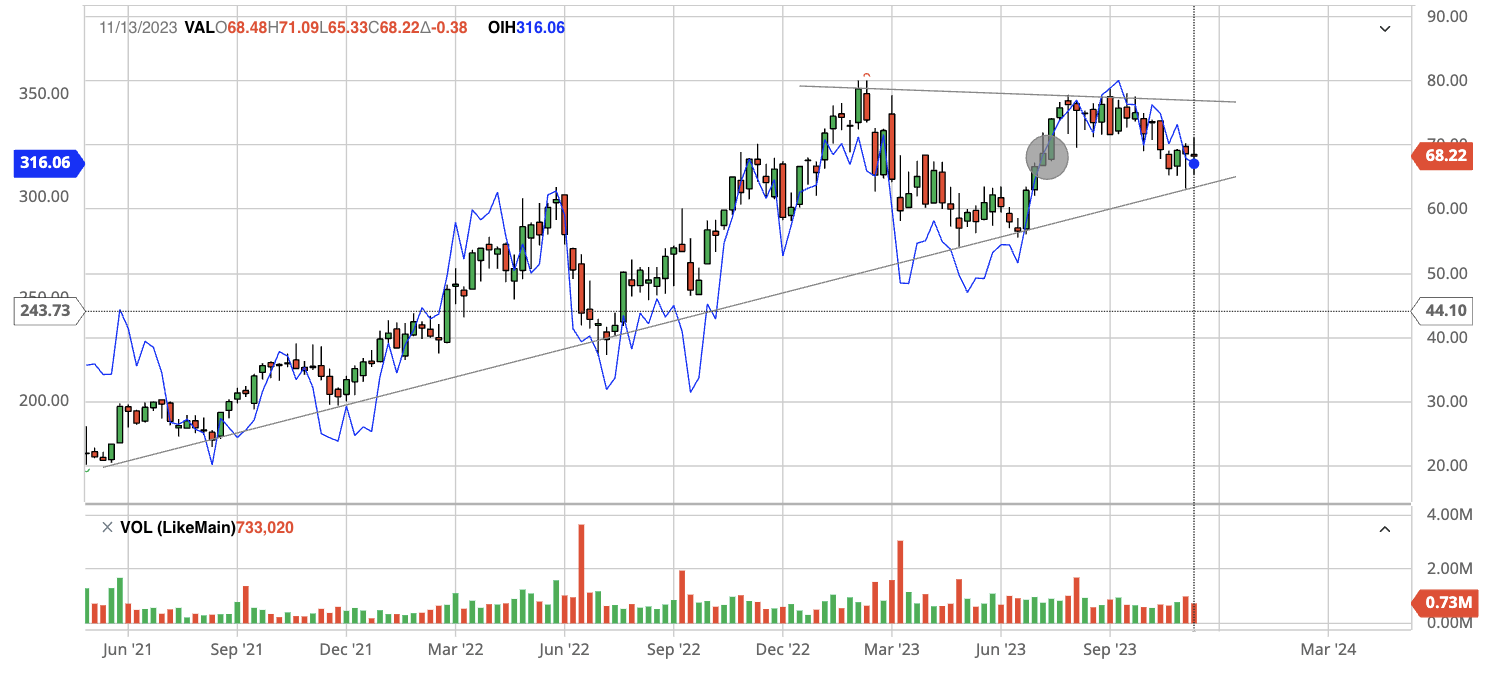

Since the publication of my previous article on Valaris Limited ( VAL ), the stock has remained relatively flat, as illustrated in Figure 1, despite significant developments in operations.

Fig. 1. Stock chart of Valaris, as compared with VanEck Oil Services ETF (OIH) (Modified from Barchart and Seeking Alpha)

{kind=link}

Valaris released earnings reports for the second and third quarters of 2023. The company also secured $400 million through the issuance of 8.375% senior secured second lien notes due in 2030 to finance the drillships Valaris DS-13 and Valaris DS-14. Additionally, it continued to secure new contracts and contract extensions .

As such, it is a good time to review the investment thesis to determine its current validity.

Day rates and equipment utilization

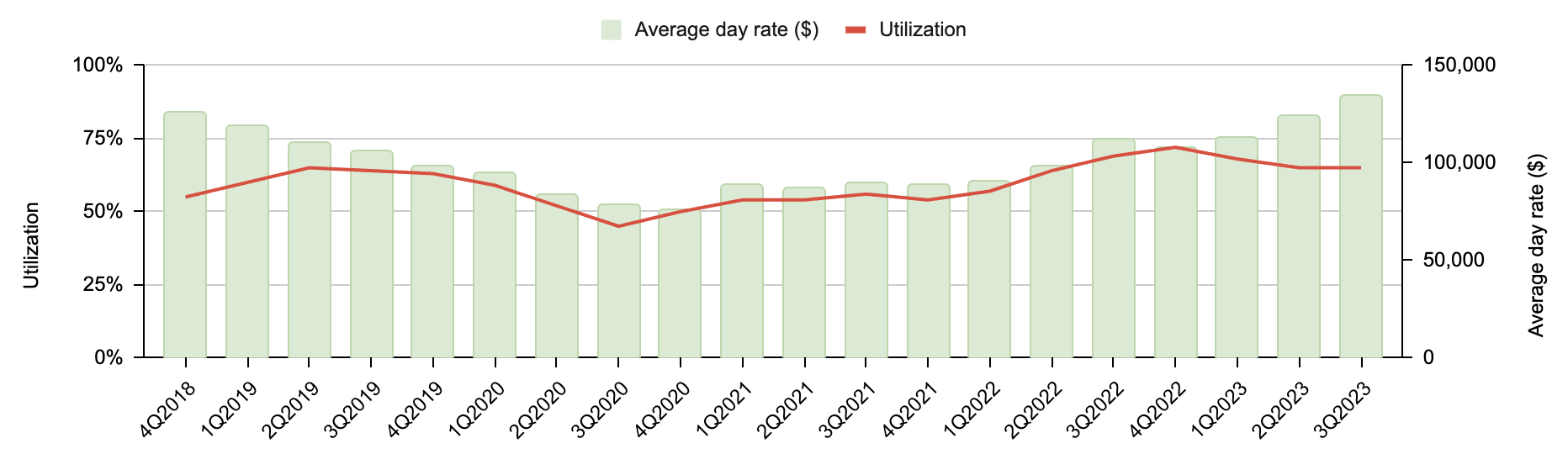

Continuing the trend established in the July 2023 article, the average day rate further improved, benefiting from the absence of a newbuild cycle. As shown in Figure 2, the average day rate reached $124,000 in the second quarter and $134,000 in the third quarter of 2023, up from $113,000 in the first quarter of 2023.

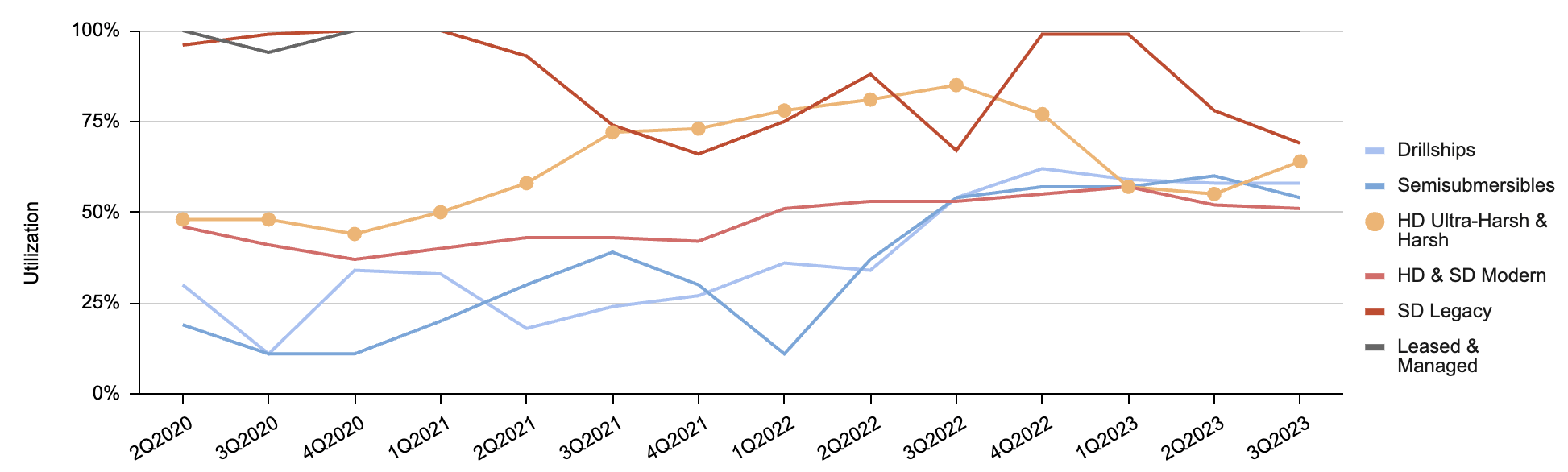

Meanwhile, rig utilization declined slightly from 72% in the fourth quarter of 2022 to 65% in the second and third quarters of 2023, stabilizing since mid-2023. This trend is mostly driven by the weakening utilization of jack-up rigs, as demonstrated in Figure 3.

Fig. 2. Average day rate and utilization by quarter for Valaris (Compiled by Laurentian Research for The Natural Resources Hub based on Valaris' financial releases) Fig. 3. Valaris' utilization by rig type (Compiled by Laurentian Research for The Natural Resources Hub based on Valaris' financial releases)

{kind=link}

{kind=link}

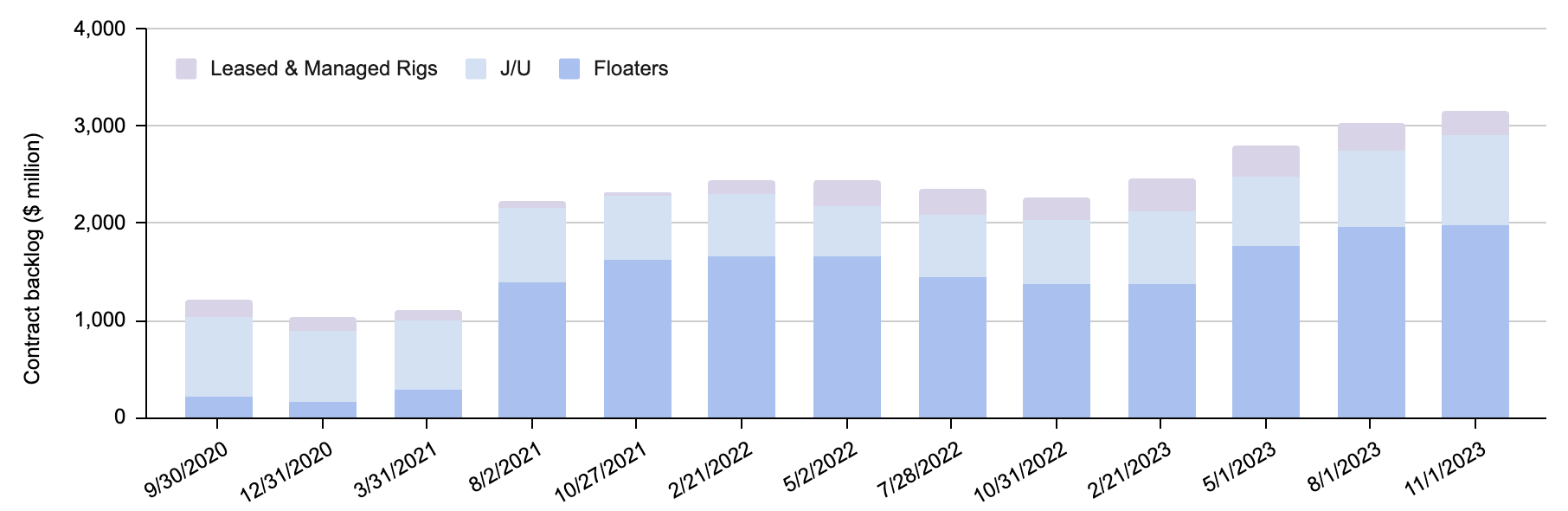

The contract backlog confirms that the offshore drilling market has continued to improve, as shown in Figure 4. As of November 1, 2023, Valaris had accumulated a contract backlog of $3.2 billion, capable of supporting 1.7 years of operation on a 3Q2023 run-rate basis.

Fig. 4. Contract backlog of Valaris, for floaters, jackups and leased and managed rigs (Compiled by Laurentian Research for The Natural Resources Hub based on Valaris' financial releases)

{kind=link}

Financials

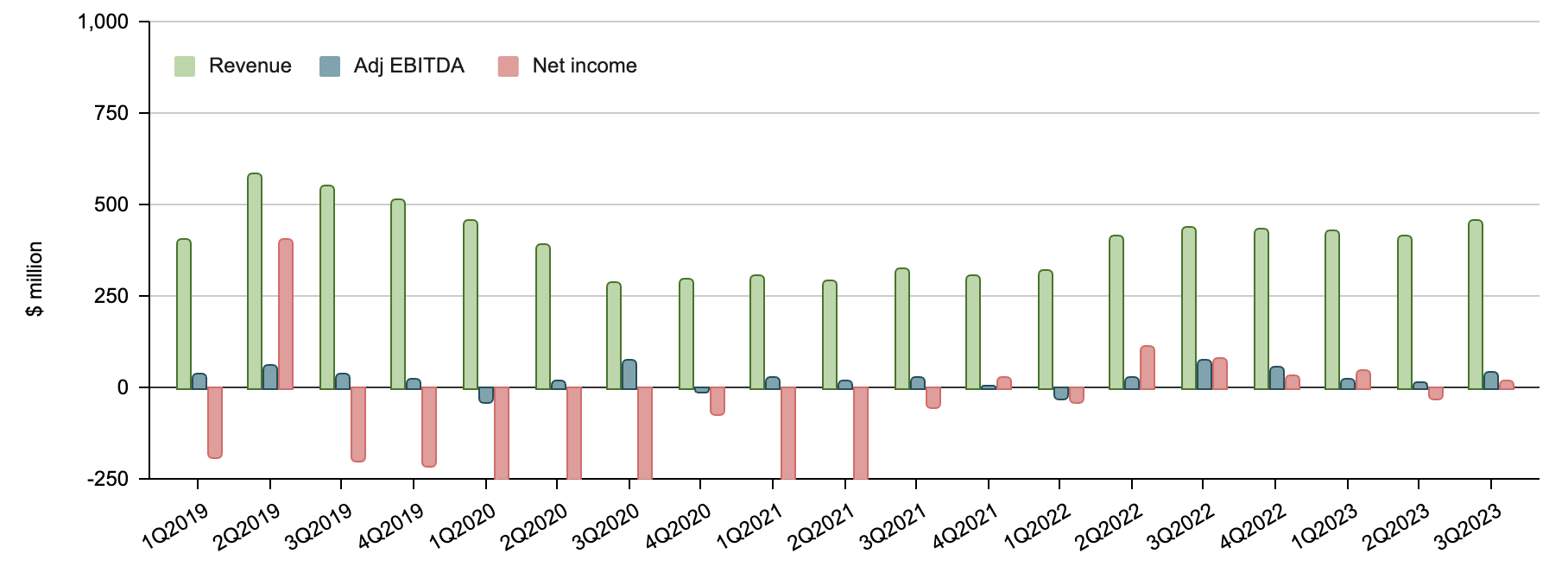

The combination of strengthening day rates and softening rig utilization has resulted in a revenue holding pattern over the past six quarters, as illustrated in Figure 5.

During this period, the EBITDA margin hovered around 4-17%, while the net margin ranged from -7 to 27%. Both figures were much lower than the respective high watermarks of 41-68% and 27-48% reached in the latter part of the last cycle from 2005 to 2013, indicating that the offshore drilling cycle is still in its early stages.

Fig. 5. Quarterly revenue, adj EBITDA and net income of Valaris (Compiled by Laurentian Research for The Natural Resources Hub based on Valaris' financial releases)

{kind=link}

Looking ahead, Valaris CEO Anton Dibowitz said :

"The outlook for Valaris is positive, with increasing demand and constrained supply tightening the market. We are confident in the strength and duration of this upcycle, and we expect to deliver meaningfully improved earnings in both 2024 and 2025 due to the impact of recent and ongoing drillship reactivations at attractive day rates, as well as the repricing of rigs from legacy day rate contracts to higher markets rates."

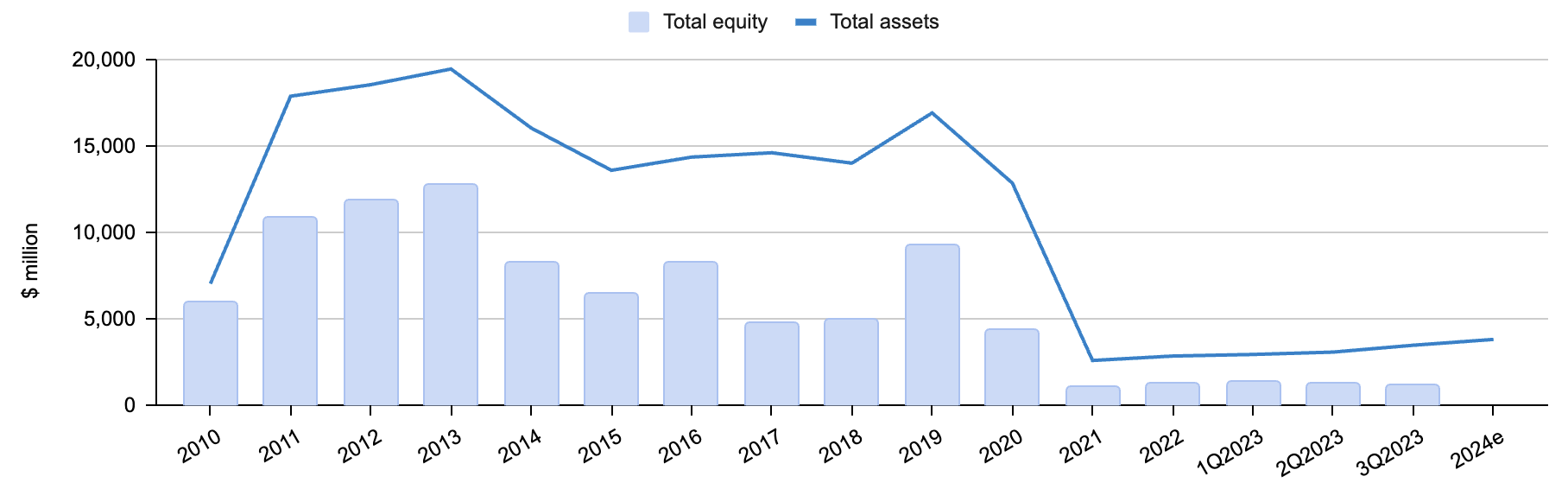

Newbuild drillships Valaris DS-13 and Valaris DS-14, for which Valaris intends to exercise its right to take delivery on or before December 31, 2023, are expected to add significantly to assets (Figure 6) and contribute to revenue-generating capacity in 2024 and beyond. Assuming the rig utilization and day rate remain the same as in 3Q2023, the addition of these two newbuild drillships to the fleet alone is expected to result in approximately a 7% increase in 2024 revenue, adjusted EBITDA, and net profit.

Fig. 6. Total equity and total assets of Valaris (Compiled by Laurentian Research for The Natural Resources Hub based on Valaris' financial releases)

{kind=link}

Valuation and risks

As of November 17, 2023, Valaris had a forward P/E multiple of 132X and a forward P/B ratio of 4.0X. These metrics appear to indicate significant overvaluation. However, as I pointed out in the July 2023 piece:

"the price/earnings ratio of a cyclical business can significantly mislead an investor... as [Peter] Lynch indicated, such high multiples may actually be good news because they are a precursor indicator of business improvement and share price appreciation."

As the offshore drilling upcycle continues, Valaris' asset value is expected to be reassessed, considering the reactivation of stacked rigs and revaluation of property and equipment. Currently, Valaris has a book value of $1,184 million, but it is estimated to possess a gross asset value exceeding $9 billion. This results in a forward P/B ratio of 0.54X, which is no longer considered expensive. Recognizing the undervaluation of its stock, Valaris has actively repurchased shares, buying back $85 million during the third quarter and $171 million year to date. The company remains on track to achieve its 2023 share repurchase target of $200 million.

The primary risks associated with the offshore drilling industry, Valaris included, involve a potential newbuild cycle and tepid exploration and production spending by oil companies. At present, both scenarios appear unlikely. Despite issuing $400 million in debt, Valaris' net debt stood at only $55.3 million as of September 30, 2023, significantly lower than its peers, including Noble Corp. ( NE ), Transocean ( RIG ), Borr Drilling ( BORR ), Diamond Offshore Drilling ( DO ), and Shelf Drilling ( SHLLF ).

Investor takeaways

A comprehensive analysis of Valaris' operational and financial performance over the past couple of quarters reinforces the validity of the investment thesis. Average day rates continued their upward trajectory, and the contract backlog showed further improvement. The forthcoming addition of drillships Valaris DS-13 and Valaris DS-14 to the floater fleet is poised to enhance its revenue-generating capacity in 2024 and beyond.

In the current offshore drilling market, marked by increasing demand and constrained supply of rig capacity, Valaris presents an exciting business outlook. Consequently, I maintain a buy rating for Valaris, for investors with a time horizon exceeding three years.

For further details see:

Valaris Limited: Fleet Expansion And Market Dynamics Bolster Investment Thesis