VAL - Valaris: Weak Quarter But Long-Term Prospects Remain Intact - Buy

2023-11-21 05:02:45 ET

Summary

- Earlier this month, leading offshore driller Valaris reported weaker-than-expected third quarter results due to contract commencement delays and unplanned floater downtime, with these issues expected to carry over into Q4.

- On the conference call, management provided mediocre 2024 guidance and warned of lengthening lead times, resulting in more near-term idle time for its floater fleet.

- However, 2025 should see a very substantial increase in profitability and cash flow generation as a number of floaters will no longer work on legacy contracts at painfully low rates.

- Management remained optimistic on the industry's medium- and long-term outlook and expects dayrates to resume their ascent once the market has digested the influx of previously sidelined capacity.

- While offshore oil and gas service stocks have been volatile as of late, I consider the recent setback an opportunity to start scaling into the shares. Reiterating "Buy" with a price target of $90.

Note:

Valaris Limited ( VAL ) has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

Company Reports Weak Third Quarter Results

Earlier this month, leading offshore driller Valaris Limited or "Valaris" reported weaker-than-expected third quarter results due to contract commencement delays and unplanned downtime on a number of floaters, as outlined by management on the conference call .

Company Press Releases and Regulatory Filings

{kind=link}

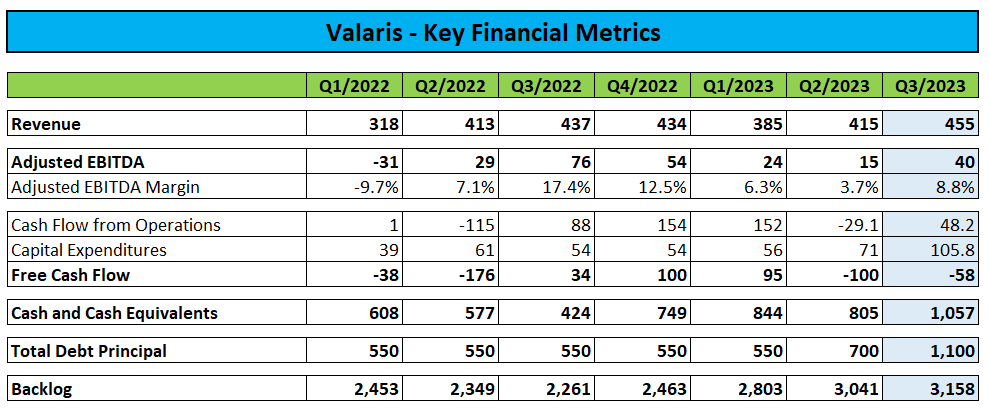

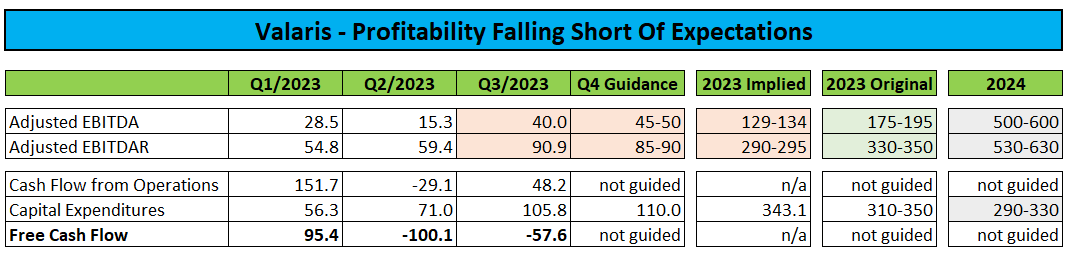

Revenue of $455.1 million was below management's guidance range of $475 million to $485 million. Profitability also fell short of expectations with Adjusted EBITDA of $40 million coming in well below the projected $50 million to $55 million range.

Free cash flow was negative $57.6 million as the company continues to deal with elevated capital expenditures from ongoing drillship reactivations.

Underwhelming Q4 Guidance

On the conference call, management provided underwhelming Q4 guidance. While projected revenues of $485 million to $490 million are just slightly below consensus expectations, profitability will be impacted by the carryover of unplanned floater downtime, further contract startup delays and some special survey and reactivation costs shifting from Q1/2024 into Q4/2023.

Company Press Releases / Conference Call Transcripts / Presentations

{kind=link}

Consequently, fourth quarter Adjusted EBITDA is expected in a range of $45 million to $50 million. Based on these projections, Valaris will miss its stated full-year Adjusted EBITDA target range of $175 million to $195 million by approximately 30%.

With $110 million in capital expenditures expected for Q4, free cash flow is likely to be substantially negative again.

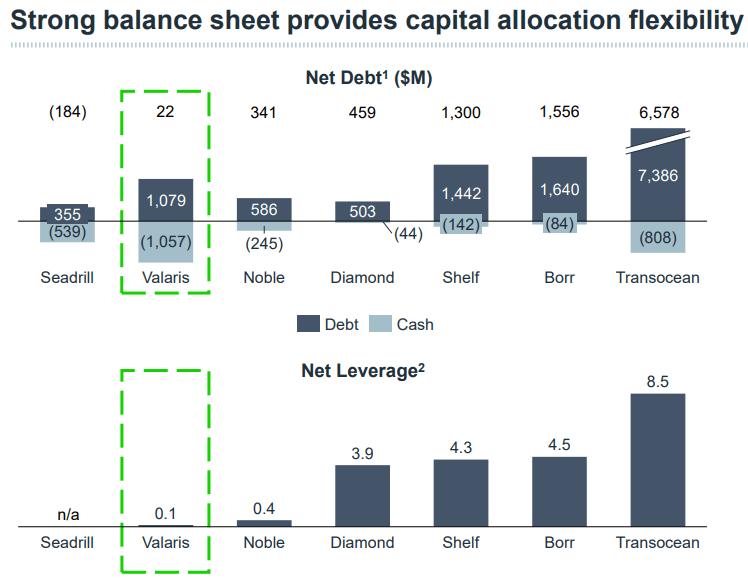

Strong Balance Sheet

However, the balance sheet remains in great shape with negligible net debt and more than $1 billion in cash and cash equivalents at the end of Q3:

{kind=link}

Share Buybacks Continue

During the quarter, the company repurchased 1.2 million shares at an aggregate cost of $85.0 million at an average price of $73.30 with only $29 million left to achieve the company's stated target for an aggregate $200 million in share buybacks this year.

With regards to capital returns next year, Valaris will provide more detailed guidance on the company's Q4 conference call in February. However, management hinted to the initiation of a dividend at some point going forward:

Our philosophy around return-of-capital is simple. And when this business is generating meaningful and sustained free cash flow, we're going to return it all to shareholders, unless we've got a more value-creative or better use for it.

As we look forward, that's going to include a dividend. We'll flex with share repurchases, and we'll even look at special dividends if we got a significant liquidity event, because as we said, this team is dedicated to capital return to shareholders.

Mediocre 2024 Guidance

Management also provided preliminary 2024 guidance with profitability well below my overly optimistic expectations (emphasis added by author):

We currently forecast revenues to be between $2.25 billion and $2.35 billion and adjusted EBITDA to range from $500 million to $600 million , including approximately $30 million of reactivation expense. 2024 revenue and EBITDA are expected to benefit from a full year contribution from VALARIS DS-17 and they are anticipated to increase meaningfully in the second half of the year versus the first half, driven by contract startups for the DS-8 and DS-7 in the first half, as well as drill ships rolling to higher day rate contracts during the year.

Newbuildings Will Cause Cash Position To Take A Hit

Please note that the company's capital expenditure guidance for Q4/2023 and 2024 does not account for the anticipated near-term exercise of purchase options for the newbuild drillships Valaris DS-13 and Valaris DS-14:

Exercising the options on both rigs would increase fourth quarter CapEx by approximately $370 million. The incremental CapEx covers the purchase price of the rigs and costs to prepare the rigs to be moved from South Korea to Las Palmas, where they would be stacked alongside VALARIS DS-11 until they are contracted.

Mobilization of the rigs to Las Palmas would require an additional $30 million in capital expenditures next year.

Considering the company's guidance for Adjusted EBITDA and capital expenditures, 2024 free cash flow generation is likely to be limited.

In combination with projected cash outflows for the above-discussed newbuilds and $50 million in assumed share repurchases, I would expect Valaris' cash balance at the end of 2024 to be between $700 million and $750 million.

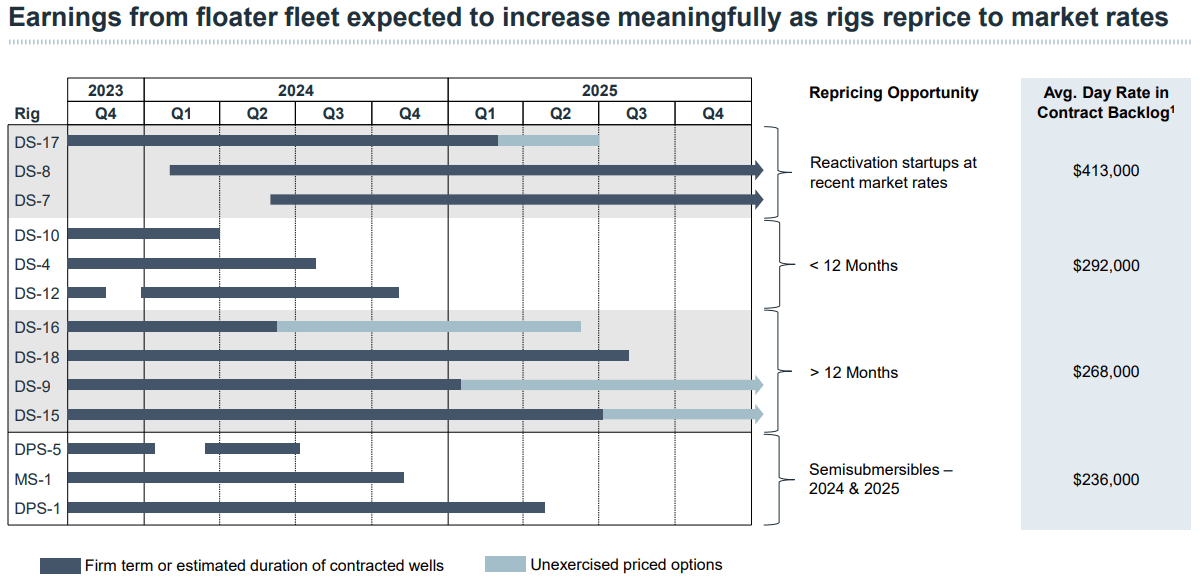

Substantial Profitability Increase in 2025

With the vast majority of available days for 2024 already contracted, potential upside will be limited next year. However, 2025 should be an entirely different story with a large number of floaters no longer working on legacy contracts at painfully low rates:

{kind=link}

As a result, average drillship dayrates in backlog are likely to eclipse the $400,000 mark in 2025:

Company Presentation

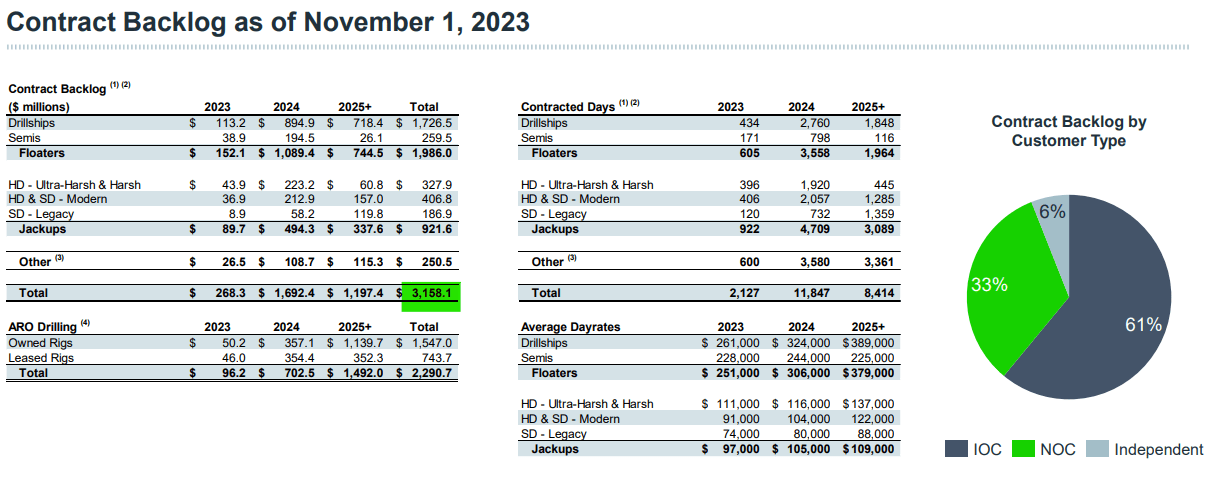

Backlog Continues To Increase

As of November 1, total backlog amounted to $3.16 billion, up 4% sequentially mostly due to customers extending contracts or exercising priced options for drillships working offshore Brazil and a multi-year plug and abandonment jackup contract award in the North Sea.

{kind=link}

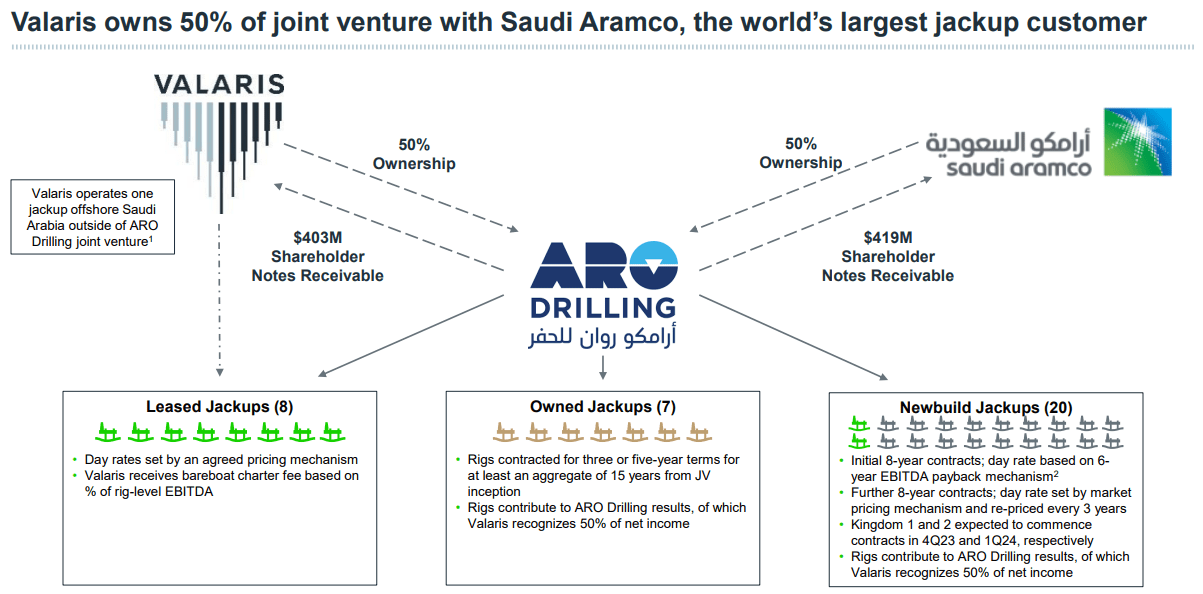

Please note that reported backlog does not include ARO Drilling, its non-consolidated joint venture with Saudi Aramco ( ARMCO ).

{kind=link}

Floater Market - Some Near-Term Headwinds But Outlook Remains Strong

On the conference call, management remained optimistic on the long-term outlook for its floater segment but warned of lengthening contract lead times causing " gaps in schedules across the industry during 2024".

In addition, key customers continue to take a measured approach towards increasing offshore investments as they are " weighing capital spending in a rising cost environment against the desire to return capital to shareholders ".

Moreover, dayrates are likely to take a breather in the near term as the market is digesting capacity additions from reactivated and newbuild assets.

We may see a wide range of rates in the near term depending on the specific circumstances of each opportunity. However, we continue to expect that we will see an upward trajectory in the medium term as stacked and new-build capacity continues to diminish and the total supply and demand balance continues to tighten.

We believe that two to three year programs are likely to be awarded at or close to leading-edge rates, while we may see lower rates for some of the five year plus opportunities, as some may be willing to accept a lower rate to secure long-term duration and backlog. Similarly, we may see lower rates on some of the shorter-term gap-filled jobs as contractors are willing to bid more aggressively to avoid rigs going idle for a period.

While management was constructive on near- to medium-term floater opportunities offshore Brazil and West Africa as well as in the Mediterranean, " visible demand " in the U.S. Gulf of Mexico is lower at this point.

However, the company still expects the market to require basically all of the currently sidelined high-specification floater capacity (stacked rigs and stranded newbuilds) in the years to come.

Jackup Market - Improving Trends But Norway Remains A Weak Spot

Commentary around the jackup side of the business was generally positive with average day rates continuing to trend upwards driven by ongoing strength in the Middle East and increasing demand in Southeast Asia.

Company Presentation

On the flip side, the harsh environment jackup market offshore Norway is not expected to pick up before 2025.

Valuation

Valuation-wise, Valaris currently trades at an estimated 2025 EV/EBITDA ratio of approximately 4.5x:

Conference Call Transcript / Author's Estimates

Assigning an EV/Adjusted EBITDA multiple of 6x would yield a $90 price target for the shares thus providing for more than 30% upside from current levels:

Author's Estimates

Key Risk Factor - Oil Price Correlation

Please note that offshore drilling stocks remain heavily correlated to oil prices so any sustained down move in the commodity would almost certainly result in industry shares taking a hit.

Bottom Line

Valaris reported third quarter results below management's projections and lowered full-year profitability expectations quite meaningfully due to a combination of unplanned floater downtime, contract startup delays and some special survey and reactivation costs shifting from Q1/2024 into Q4/2023.

Similar to a number of competitors, the company warned of lengthening contract lead times resulting in more near-term idle time for its floater fleet.

However, management remained optimistic on the industry's medium- and long-term outlook and expects dayrates to resume their ascent once the market has digested the influx of previously sidelined capacity.

While offshore oil and gas service stocks have been volatile as of late, I consider the recent setback an opportunity to start scaling into the shares.

For further details see:

Valaris: Weak Quarter, But Long-Term Prospects Remain Intact - Buy