VLO - Valero Energy: A Solid Q3 With A Powerful Buyback In Place

2023-10-27 03:28:29 ET

Summary

- Valero's Q3 earnings beat expectations, with net income falling but EPS rising due to aggressive stock buybacks.

- The company's refining business remains its main source of earnings, with margins expected to normalize but remaining wider than pre-COVID given supply constraints.

- Valero's low multiple and limited refining capacity make it an attractive investment opportunity with potential for upside.

Shares of Valero ( VLO ) have essentially tread water over the past year, lagging the broader market gain. After reporting Q3 results on Thursday, shares fell about 1%, in what has been a down day for the overall market. With just a 5x earnings multiple though, this is a stock that is deserving of a deeper examination. While I do expect earnings to decline, Valero stands out as an attractive opportunity.

{kind=link}

In the company’s third quarter , Valero earned $7.49, which beat estimates by $0.17. The first thing to highlight is that net income fell from $2.8 to $2.6 billion but EPS rose by $0.30 from $7.19. That is the power of the company’s capital return policy. With earnings particularly high, VLO has been aggressively buying back stock. It returned $2.2 billion to shareholders last quarter with a $360 million quarterly dividend and the balance in share repurchases. As such, its share count is down 10.5% from last year.

Over time, VLO targets a capital return policy of 40-50% of operating cash flow. Last quarter though, it returned 60% of operating cash flow to investors. This is not because cash flow has fallen to a troubling degree, rather cash margins have been so strong that VLO has been generating excess cash well beyond its investment needs, which it then is returning. That 40-50% is intended to be a cycle average. However, the dramatic share count reduction will mean EPS will outperform net income as we saw last quarter. Since 2012, VLO has bought back nearly 40% of the company.

Valero

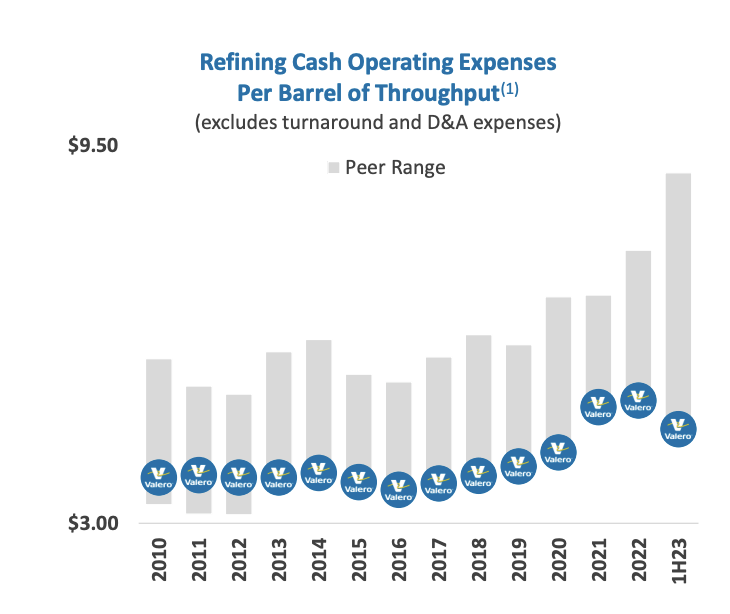

Looking at Q3 results, refining operating income was down $400 million to $3.4 billion. Its refineries ran at a solid 95% utilization, even with some maintenance work. With that work complete, management is expecting to run at a 96.5% utilization rate in Q4 as product demand has stayed strong with diesel inventories being relatively tight still. With investments to modernize refineries over the past ten years, VLO has been able to increase utilization and lower operating costs, leaving it with a cost advantaged system and boosting margins.

{kind=link}

Valero earned a margin per barrel of oil of $19.47 from $21.43 last year. On a percentage basis, refining margins actually expanded to 9.4% from 9% as crude oil prices were lower, but that decline in dollar margin per barrel is what caused earnings from this unit to fall from last year. We will discuss refinery margins further in a moment.

Briefly though, VLO has two smaller units. Its renewable diesel unit generated operating income of $123 million from $212 million last year. While sales were up a third as expansion projects came online, diesel margins compressed from last year. While still healthy, diesel markets were extremely tight last year as Europe scrambled for fuel after turning away from Russian oil. This unit is operating at more of a normal level now.

On the other side, ethanal operating income rose to $197 million from $1 million last year, with production up over 20%. Corn prices are lower than a year ago, outpacing the decline in crude oil, which has helped to widen margins. While these renewable energy businesses provide some earnings, 90-95% of Valero’s results come from its core refining business. Refining margins, more so than renewable diesel or ethanol, are what will drive the stock.

It has been a bull market for refining since shortly after COVID. 3:2:1 spreads, which measure how much refiners get for their refined products (gasoline, diesel) relative to the crude oil input soared. This is why Valero’s profits surged and it has been able to buy back so much stock. Now, these margins have been to normalize. A reason VLO trades at such a low multiple is markets are viewing some of its ~$20/barrel margin as a one-time windfall rather than a recurring source of income. The one-time windfall is definitely good for shareholders, but VLO will never get a 15x multiple on peak earnings.

{kind=link}

A question then is where do margins go over time; in other words, what is Valero’s true run-rate earnings power. At the current share count and with its ~23% tax rate, if we cut Valero’s refining margins in half, it would have run-rate earnings of $3.75/share or about $14-15/year. That would leave the stock with just an ~8.5x multiple. Right now, per the analyst consensus, earnings are forecast to decline to $15.51 next year. Given the share count will continue to fall next year, the consensus is essentially in-line with a halving of refining margins.

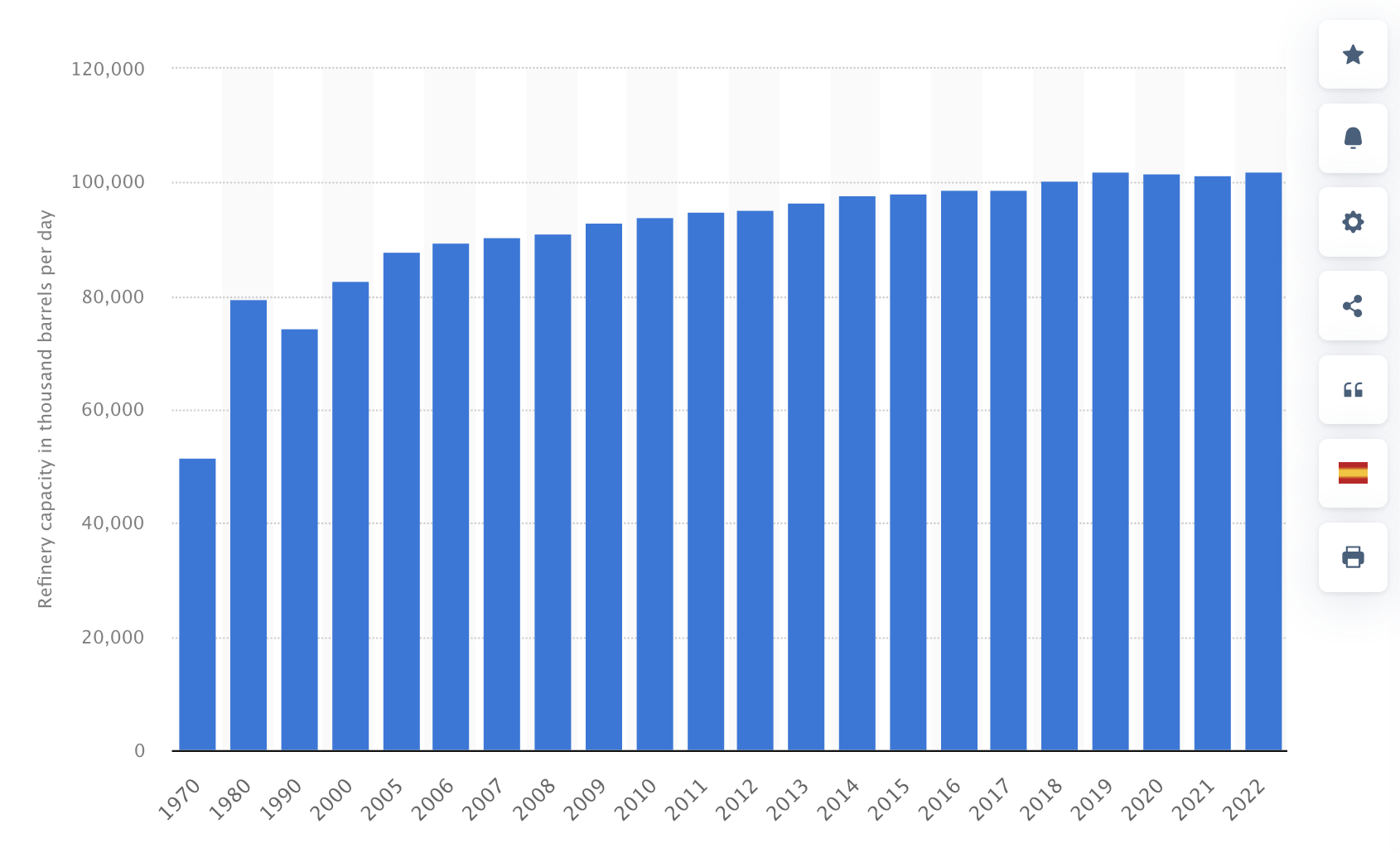

In 2019 , VLO was earning $9.65 a barrel, and in 2018, it earned $10.32 a barrel. So this halving would be in-line with the pre-COVID norm, which was a good but not record setting environment for refiners. I see the risks skewed to the future being a bit brighter than this on average, for the simple reason that the world does not have much refining capacity. As you can see below, after rising steadily in the 2000s, refining capacity growth has really slowed down. There has essentially been no new refining capacity over the past four years. Oil demand is still rising though given ongoing economic growth and development in emerging markets. This increasingly means refining, even more so than production, is the bottleneck in the supply chain. That should mean wider margins on average.

{kind=link}

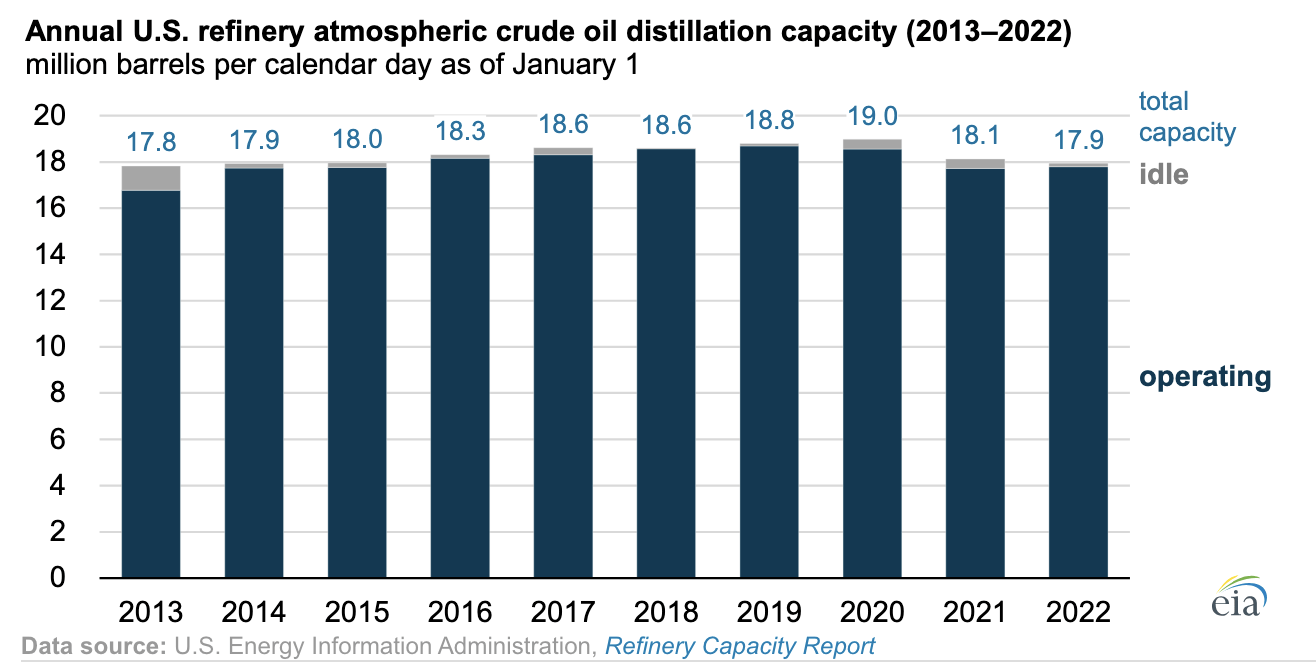

This is particularly true in the US. As some smaller refineries have shuttered, our refining capacity is down about 6% from pre-COVID levels. While these markets are global to a large extent, there is shipping cost, so local market dynamics do matter. The relative underperformance of US refining capacity to global capacity is likely to further insulate US refining margins, all else equal.

{kind=link}

Now, as economics 101 student can tell you, the reason bottlenecked, or supply-constrained, markets have wider margins is to encourage investment and the development of new supply to meet the demand. The last significant refinery in the US was built in the 1970s , though. Given the regulatory environment and the fact a brand-new refinery could cost well in excess of $8 billion, it simply is not feasible to build one. Indeed, the cost could be even greater with Mexico’s plans to build a refinery potentially spiraling to $20 billion . Western governments are also focused on investing in renewable energy not supporting increased supply of crude oil refining capacity. There is no investment/supply-side reaction function to wide refining spreads given this backdrop.

This has left existing refinery owners in a strong position to enjoy wider margins. Indeed, we can see the lack of interest in investing in Valero’s financials. Last quarter, it spent $303 million of sustaining cap-ex and just $91 million on growth spending, mostly in its smaller renewables businesses. Barring something truly unforeseen, the US has as many refineries today as it ever will. The same is likely true of Europe. As such, it will be difficult for global refining capacity to match, let alone exceed, underlying product demand. That means margins will be structurally wider, maybe not as wide as today, but wider than 2018/2019 on average.

I would write that Valero has 14 refineries and will never grow beyond that. However, while that is true in terms of its not organically building more, there is the possibility of M&A. Finally, the Citgo sales process is starting and expected to last until next summer, though there is likely to be further legal arguments over it, which could end the auctions altogether. I could see Valero bidding for some of Citgo’s assets which are quality refineries able to process cheap, heavy crude. Whether Citgo will be sold and to what parties is impossible to know, but if Valero does win, that would likely cause a temporary slowing in its buybacks to fund the purchases. If Citgo is sold, I expect different firms would buy different assets, limiting VLO’s potential purchase to a manageable $5-8 billion.

Overall, I view $15-17 as a reasonable estimate for VLO’s earnings power the next year given a likely 5% share count reduction and where refining spreads are. However at 8.5x earnings, markets seem to be discounting that even this lessened margin is unsustainably high. Given the reasons discussed, that is where I disagree. I see run-rate earnings holding at least at the $15 level. It is a low margin, capital intensive business but I believe 10x run-rate earnings is reasonable, pointing to a fair price of $150. That is 20% of upside.

I believe investors should begin accumulating VLO stock. In the meantime as it trades below its fair value, that just means the buyback reduces the share count even more quickly, further increasing run-rate earnings power and long-term value for shareholders. Refining is a supply constrained business, and it is likely to remain so. That is good news for Valero and its shareholders.

For further details see:

Valero Energy: A Solid Q3 With A Powerful Buyback In Place