VLO - Valero Energy: Adjusting Estimates But It Is A Buy

2024-01-12 07:26:03 ET

Summary

- Post Ukraine/Russia world, US refineries have become a preferred diesel supplier for Europe.

- Despite lowering our crack spread estimates in 2024, VLO is the lowest-cost producer with the DGD earning recovery story to play.

- Valero's disciplined capital management and favorable valuation make it an attractive investment with a target of $152 per share.

Following our update on Phillips 66 (Rating Downgrade) with a crack-level normalization expected in 2024, today, we are moving on with Valero Energy analysis ( VLO ). The company proved to be one of Mare Evidence Lab's most successful investments, with a return of +100% (including dividend payments). It was supported by our Darling Ingredients Diamond Green Diesel JV Valued At Zero . Before taking advantage of our 2024 crack-level estimates, it is essential to report that 2023 has been a challenging and resilient year for the company. However, in terms of share price returns, in 2023, the company has been among the worst-performing refiners, and this was due to its exposure to heavy and medium sour differentials as OPEC+ has decided to lower oil production. That said, the company is a best-in-class operator in terms of margin and ROIC with significant optionality in its refining system. For the above reason, we continue to broadly favor refiners with export capabilities as supply chains continue to adjust to a post-Ukraine/Russia world.

{kind=link}

On a MACRO basis, diesel demand remains solid, and compared to October, there is a better level of inventories. Moreover, as already mentioned:

After the Russian invasion, the routes have become longer, and more ships are needed to transport an equal quantity of products. This CAPEX constraint favors US refineries. Moreover, sanctions imposed on Russia have deprived Europeans of their largest diesel supplier. To replace the Russians, Europe turned to the countries of the Middle and Far East. With the Israel-Gaza retaliation, diesel supply that usually passed through the Red Sea and crossed the Suez Canal is now almost interrupted .

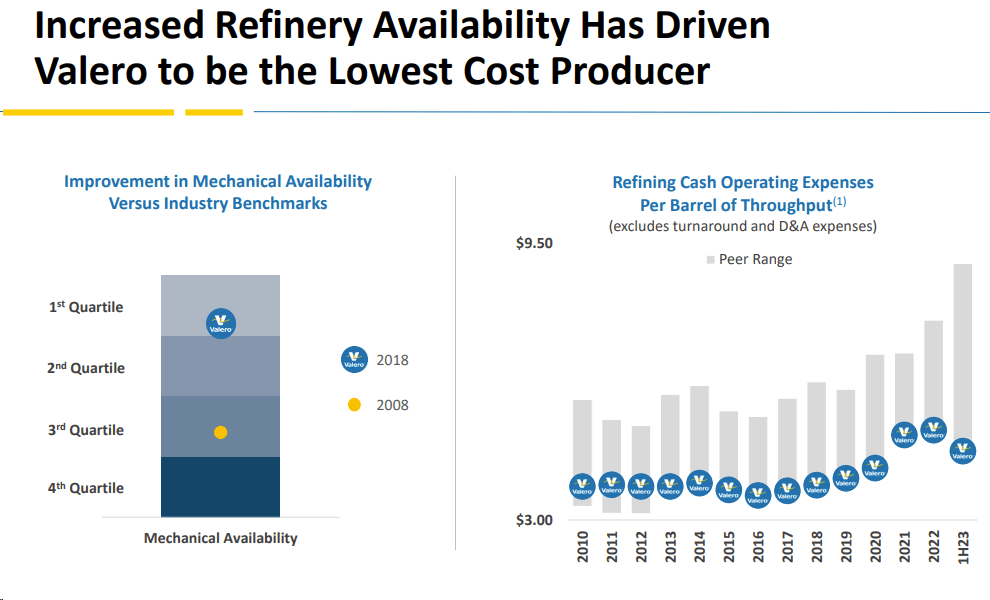

Therefore, we are confident that United States refineries like Valero will benefit from this ongoing conflict. In addition, in mid-cycle earnings, as we forecast for 2024, the company usually manages the crude differential headwinds better than comps (Fig 1). This is an advantage that cannot go unnoticed. In 2024, our team believes crack levels should remain above mid-cycle because supply and demand are almost balanced.

{kind=link}

Fig 1

Q4 Update and 2024 Forecast

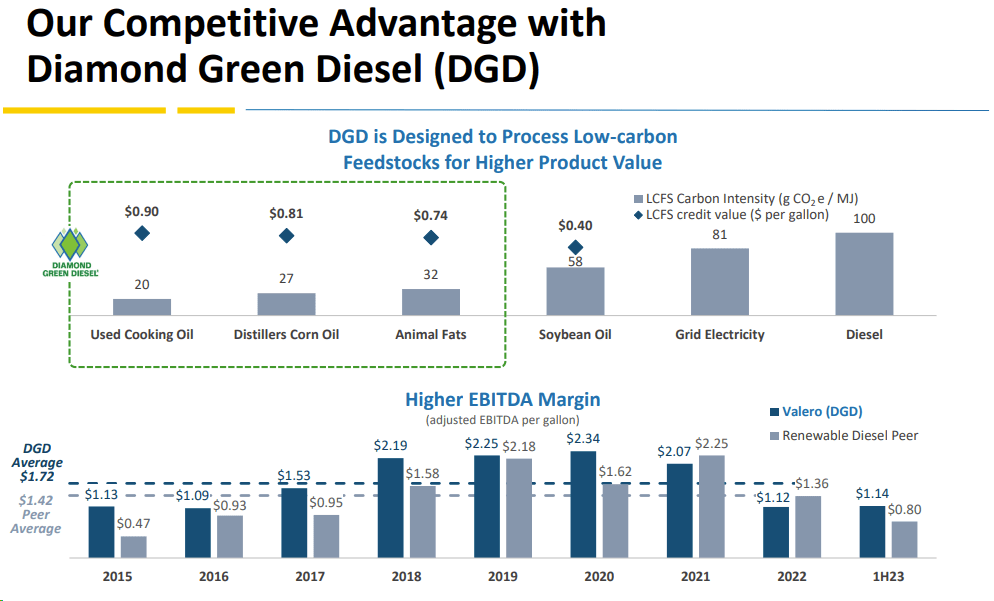

On a negative basis, we are modeling lower Q4 2023 estimates mainly due to a lower-than-expected refining margin and a downside revision from DGD JV earning contribution. Starting with the refining segment, with a utilization rate at 94% level (guidance midpoint), we anticipate a gross margin of $12 per barrel (compared to a gross margin of $19.47 per barrel achieved in Q3). Therefore, we expect Valero's core operating profit to be $1.5 billion compared to a $3.45 billion result in Q3. Looking at the renewable diesel JV in our model, we anticipate a core operating profit of $50 million compared to a $123 million performance achieved in Q3 2023. We estimate 3,587 thousand gallons per day versus 2,992 thousand gallons per day (planned plus unplanned downtime) in Q3 2023. In our estimates, the gross margin per gallon decreased from $0.95 to $0.65 on a quarterly basis. This pessimistic scenario is based on feedstock price lag. That said, we forecast a reverse environment in Q1 2024 and a much stronger DGD earning contribution in the year ahead. In the ethanol division, we see Valero EBIT at $150 million with lower volume and a gross margin per gallon at $0.68.

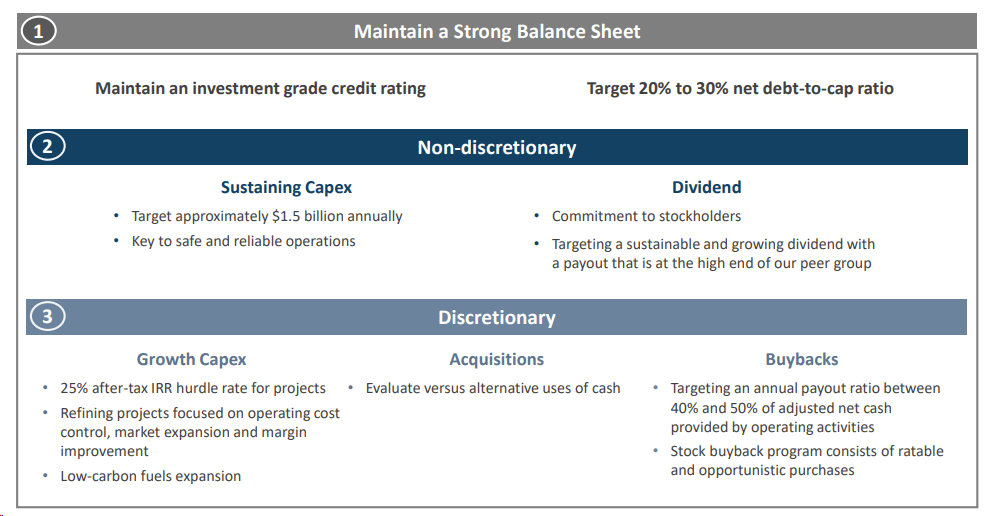

On a yearly basis, we arrived at sales of $149.45 billion with an EBITDA expected at $14.4 billion. We are modeling a $900 million share repurchase in the last quarter with a working capital constraint at $150 million on lower oil crude prices. Our team saw $1.75 billion in cash flow, including working capital negative one-off and modeling capex at $600 million; our FCF reached $1 billion. We see $345 million in dividend payments and $500 million in buybacks, with a Q4 total return of capital at approximately 51% on the company's FCF. This aligns Valero with its long-term target payout, which is between 40% and 50%. In 2024, we see EC gasoline, EC diesel, and EC 321 spread at $16.5, $33, and $22.5, and we have a mid-point DGD EBITDA estimates (Fig 2); we are projecting a company 2024 EBITDA of $9.5 billion. CAPEX is $1.4 billion, and FCF is $5 billion. With the above management payout ratio (Fig 3), we anticipated a $1 billion deleverage, $1.4 billion in dividends, and up to $2.6 billion in potential buyback.

{kind=link}

Fig 2

{kind=link}

Fig 3

Conclusion and Valuation

Valero's disciplined capital management is supportive in a mid-cycle environment. The company is well positioned as it relates to debt on the balance sheet with the expectation of cash build-up while increasing shareholders' remuneration (with a dividend hike). Phillips 66 trades at a 2024 EV/EBITDA of 7x, while Valero is at 4.5x. As a reminder, in Mare Evidence Lab's long-term assumption, the 321 crack spread is forecasted at $11.5 per barrel. Applying an 8% FCF/EV yield target and a multiple of at least 6x in the EV/EBITDA, similar to large-cap refining peers, we derived a share price of $152 per share, confirming a buy rating on the company. Primary Valero risks include narrowing Gulf Coast crude spreads, lower-than-expected product export demand, a change in the disciplined capital allocation, and weaker fundamentals in biodiesel and ethanol markets.

For further details see:

Valero Energy: Adjusting Estimates, But It Is A Buy