VLO - Valero Energy: Buy Rating Fueled By 3% Dividend Yield And Undervaluation

2023-11-29 15:58:19 ET

Summary

- Valero Energy is rated buy today, agreeing with the Wall Street consensus.

- Positive drivers of bullishness include 3.2% dividend yield, dividend growth, share price dip below the moving average, and lowered debt risk.

- Some negatives to consider are YoY revenue and earnings declines despite product demand.

Company Snapshot

Today's research note covers Valero Energy ( VLO ) , in the energy sector.

Some relevant facts about this company include: it's based in San Antonio Texas, trades on the NYSE, and calls itself the world's largest petroleum refiner and world's largest producer of low-carbon transportation fuels. It is also a Fortune 500 company with 15 refineries across the US, Canada, and UK.

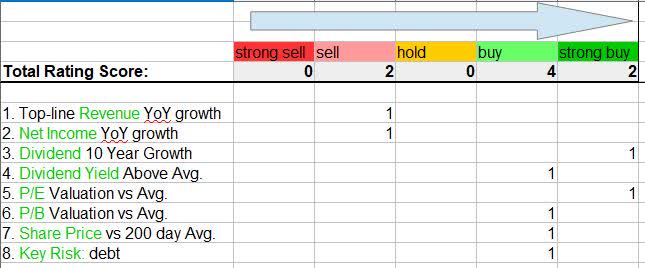

Total Rating Score

Here is my score matrix I created for this stock, with a point given towards the buy side for any strong or positive metrics in that category, and towards the sell side because of weak or negative metrics:

{kind=link}

Based on the score total in today's note, I am rating this stock a buy.

Compared to the rating consensus today, my sentiment is mostly aligned with that of Wall Street:

Valero - rating consensus (Seeking Alpha)

Rating Methodology

Starting in December 2023, I adopted a simplified and straightforward 8-point approach focusing on just a few core areas such as whether the company is growing both revenue and earnings, whether it presents a strong dividend income opportunity, whether an undervaluation opportunity exists, a share price presenting a value-buying potential, and identifying a key risk of the company as well as its potential impact to an investor.

Top-Line Revenue YoY Growth

I am looking for any positive revenue growth on a YoY basis, and here is what I found:

From the most recent income statement data, in the quarter ending Sept 2023 it had $36.9B in revenue vs $43.2B in Sept 2022, a 14.5% YoY decline .

From the company's Q3 earnings release on October 26th, we can see that a positive driver of revenue was their renewable diesel segment:

Segment sales volumes averaged 3.0 million gallons per day in the third quarter of 2023, which was 761 thousand gallons per day higher than the third quarter of 2022. The higher sales volumes were due to the impact of additional volumes from the DGD Port Arthur plant, which started up in the fourth quarter of 2022.

However, from that same release it appears the weak spots were the declines from the refining segment, however according to the CEO the "product demand remained strong in our US wholesale system."

Personally, I anticipate this "demand" will continue to drive top-line sales for this company going forward, despite the YoY decline.

Net Income YoY Growth

I am looking for any positive net income growth on a YoY basis, and here is what I found:

Also using the same income statement, in that quarter it had $2.62B in net income vs $2.81B in Sept 2022, a 6.7% YoY decline.

In terms of their income statement shown in the Q3 earnings release , operating expenses and total cost of sales actually declined on a YoY basis, however interest expenses on debt actually spiked a little, which I will discuss further in the key risks section.

I think therefore what will help drive bottom-line earnings to improvement will be a significant top-line revenue growth in the next few quarters, combined with eventual lower interest costs when and if rates come down again. What will drive this will be demand for its product which is such a major part of the economy.

Consider that this is also supported by an October article by Reuters :

Valero beat analysts' estimates for third-quarter profit on Thursday, powered by sustained fuel and refined products demand against the backdrop of tight supplies.

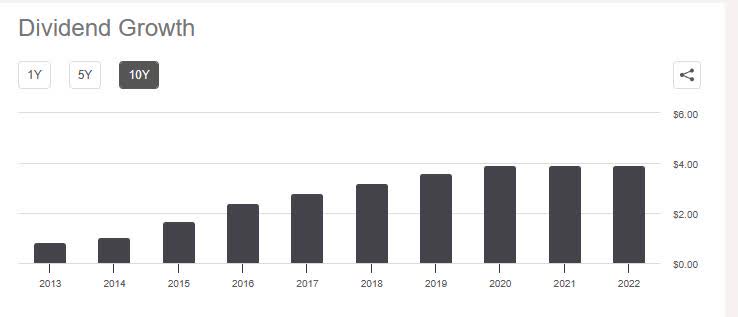

Dividend 10 Year Growth

I am looking for dividend 10 year growth trends, and here is what I found:

{kind=link}

When looking at the chart above, I can see that there is a positive dividend growth trend. Comparing the 2022 annual dividend of $2.92 and the 2013 annual dividend of $0.83, we see an over 250% growth in 10 years.

As a dividend-oriented investor and analyst, this commitment to returning capital back to shareholders tells me a company has the financial capacity to do so, but also presents a nice cashflow opportunity if considering holding the shares longer-term.

In fact, the Q3 earnings release spoke to their capital strength:

Valero returned $2.2 billion to stockholders in the third quarter of 2023, of which $360 million was paid as dividends and $1.8 billion was for the purchase of approximately 13 million shares of common stock.

Dividend Yield Above Average

I am looking for a dividend yield above its sector average, and here is what I found:

{kind=link}

In comparing the dividend yield of Valero which is 3.26% , to two of its major energy-sector peers Marathon Petroleum ( MPC ) and Phillips 66 ( PSX ), it is somewhere in the middle of the pack and also you can see it grew it yield by over 12% lately.

I think this presents an opportunity for a dividend-oriented investor to buy while the yield is over 3% like it is. You can also correlate this increase in dividend yield with the recent decline in the share price. However, as I will mention later, I think there is upside potential that will drive the share price up and therefore this yield will decline again.

P/E Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-earnings , and here is what I found:

When considering the forward P/E is 5.03 and the sector average is 10.75, I consider this a great undervaluation with a price that is just around 5x earnings.

Tying this to the financials and share price, it appears to me what is driving this undervaluation is the decline in share price and not an earnings spike, so with the earnings being in YoY decline I think the current share price appears reasonable.

P/B Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-book value , and here is what I found:

With a forward P/B that is 1.64, vs the sector average of 1.63, it is practically in line with the average and I think paying 1.6x book value is a reasonable valuation.

To help me understand what is driving this valuation, I turned again to the balance sheet which shows total equity (book value) went up to $28.05B vs $23.7B in the prior September, so this increase in book value combined with the decline in share price lately presents a nice valuation for this stock in my opinion.

Share Price vs 200-day Average

My portfolio strategy prefers dip-buying opportunities when the share price falls below the 200-day simple moving average , so here is what I found:

This stock's share price (as of the writing of this article) of $125.24 is less than a 1% difference vs the 200-day simple moving average I am tracking.

I consider it a value-buy opportunity as it is considerably off its September highs with the current dip below the average, while I can snag the above-3% dividend yield on this profitable and market-leading company in its sector as a major energy player.

Further, the upside potential I think will come from earnings beats and a return to YoY earnings and revenue growth. The company already beat earnings estimates in all of the last 4 quarters. So, I would be looking to get in at the current price and ride it up to at least $150.

Key Risk

As an investor and analyst I find it relevant to analyze risk as well, and here is one key risk of this company I identified: company long-term debt.

In looking at the balance sheet , we can see that the long-term debt was a whopping $10.57B in Sept 2022, dropping to just $7.8B in the most recent quarter, a 26% YoY decline in debt.

Correlating that same period with interest expense which affects the income statement , interestingly the interest expense rose in this period but not by a huge amount. It went from $138MM in Sept 2022 to $149MM in Sept 2023, which is just a 7% YoY increase.

We also should consider the rate environment and how it has impacted the cost of debt in the last year. The good news, from CME FedWatch data , is that there is practically a 0% probability expected of another Fed rate hike after its December 13th meeting coming up.

So, with the decline in debt, I will go ahead and consider this an acceptable risk, considering that this is a very capital-intensive industry with high overhead and need for financing. Its peer Marathon Petroleum , for example, actually saw their company debt go up to $25.9B from $25.08B a year prior, so I think Valero is in an improved debt situation vs this peer.

Analysis Wrap-up

To summarize, my sentiment is bullish on this one today as it appears to me as an undervalued dividend income play, with upside potential due to product demand, a lower debt risk profile, and the potential to return to YoY earnings growth again. It is also within what I call critical infrastructure stocks, such as utilities and energy, supermarkets/food, and telecom, for example, and having a major market penetration in its segment.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Valero Energy: Buy Rating Fueled By 3% Dividend Yield And Undervaluation