VLO - Valero Energy: Holding At Current Levels

2023-12-11 13:18:09 ET

Summary

- Valero Energy Corporation has underperformed in the refining sector over the past year, ranking near the bottom in terms of total return.

- The refining sector faces challenges such as fluctuating crack spreads and increased global competition.

- Valero's prospects include its position as the largest independent refiner globally and its expansion projects, with a near-term catalyst being the Port Arthur SAAS project.

- We think the company rates a hold at current prices, but a slight dip might draw our interest.

Introduction

The refining sector has seen some recent weakness, leading us to drop in for any bargains that might be accumulating in the discount bins. What we found was a mixed bag, with one major refiner in particular underperforming the rest of the cohort. In this case, we are discussing Valero Energy Corporation (VLO) a leading provider of refined petroleum products and an emerging leader in bioenergy.

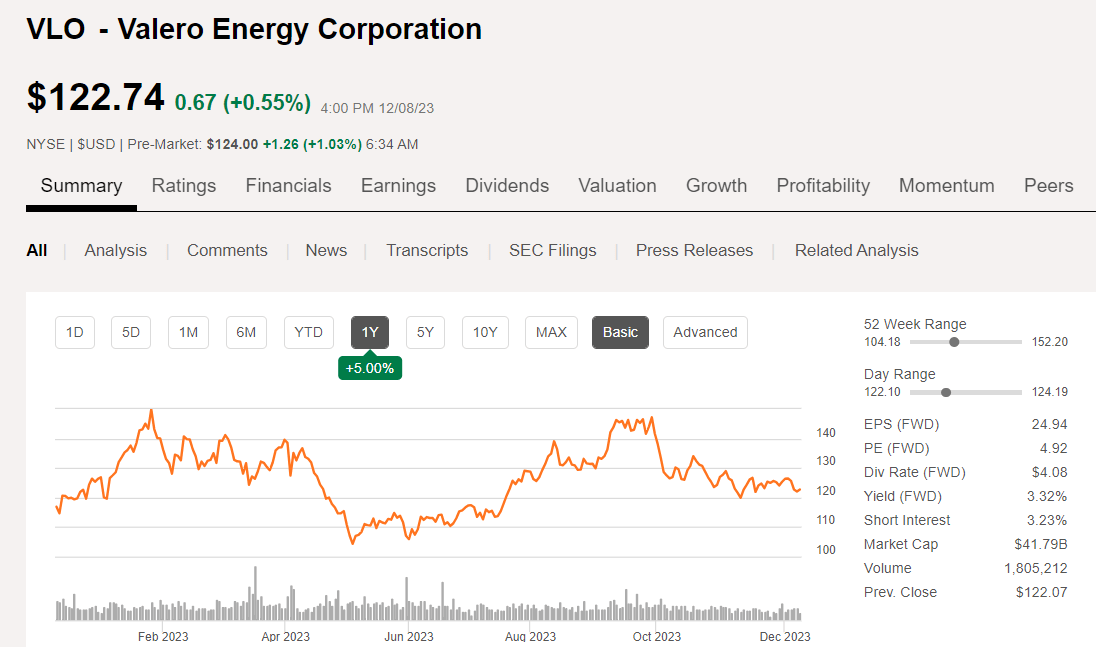

We have covered VLO previously, and the last report on this company is linked for your reference. The analyst community ranks it as overweight , with price targets ranging from $130-$171, and a median of $150. The company has receded from recent peaks near $150 and is heading into a traditional turnaround from producing gasoline to making more heating oil for the Northeast.

{kind=link}

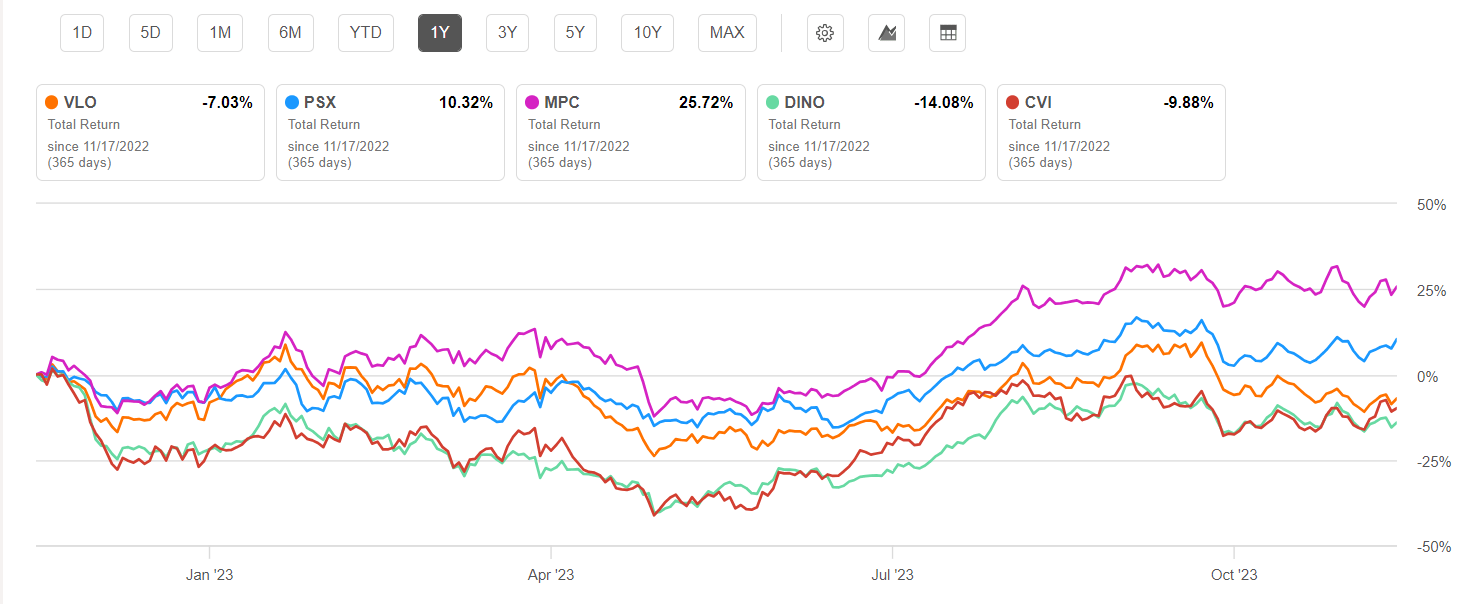

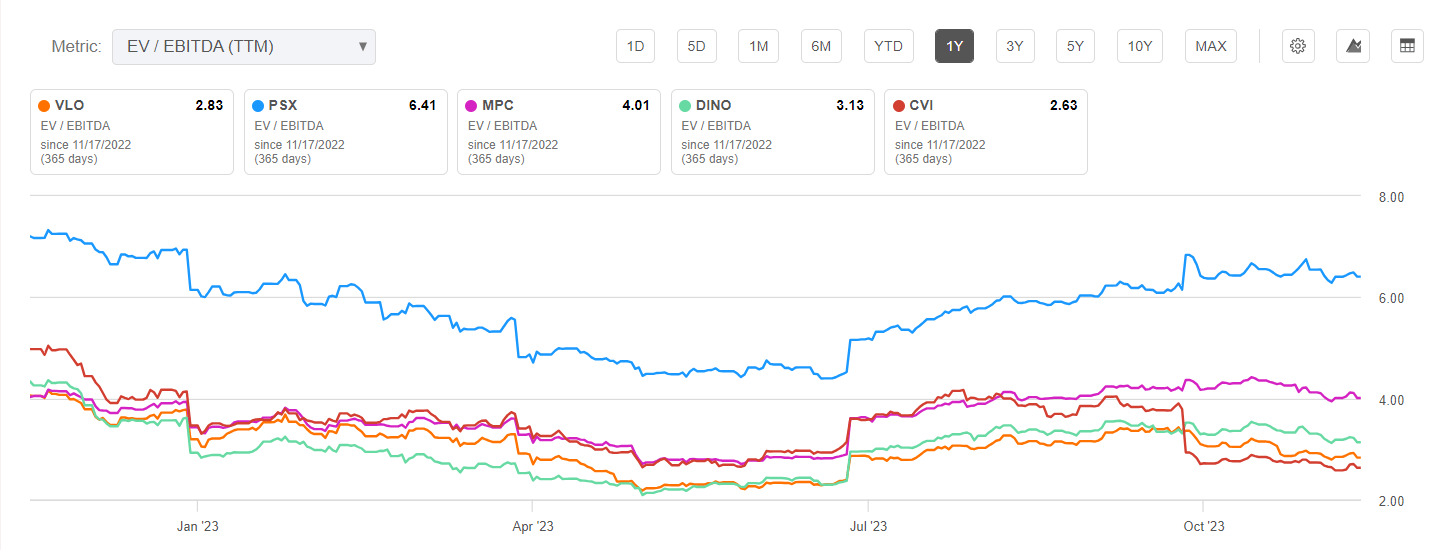

In terms of total return over the past year, VLO ranks near the bottom of the refining cohort, coming in at just above HF Sinclair ( DINO ). Given that, investors who've been long the past year have a right to be testy, particularly when compared with the spectacular returns of Phillips 66 ( PSX ) and standout performer Marathon Petroleum ( MPC ).

{kind=link}

Let's review the prospects for the refining sector and VLO in particular. They've underperformed over the last year, but that's looking back. What lies ahead, will VLO retake recent heights or wallow in the abyss?

A quick look at the "mechanics" of the refining sector

I will start out by reminding you of a couple of things that provide tailwinds or headwinds to refiners. The 3-2-1 Crack Spread - the difference in what the two barrels of gasoline and one barrel of diesel will sell for vs. the three barrels of crude that it takes to make them. The ramp higher in WTI in Q3 put a hurt on the input side of this equation but was overcome by refined product margins for most of the quarter. In Q4, it cratered to $17, but has rebounded a bit since to the $23 level, and might account for the recent rally in VLO.

VLO management is a bit dour about the upcoming quarters. COO Gary Simmons addresses crack spread expectations in response to an analyst query-

In terms of the outlook going forward, we'd expect gasoline to kind of follow typical seasonal patterns, weaker cracks , kind of the fourth quarter and first quarter. So as long as that's the case, our view would be that when you get to driving season next year, demand picks back up, you'll see cracks respond.

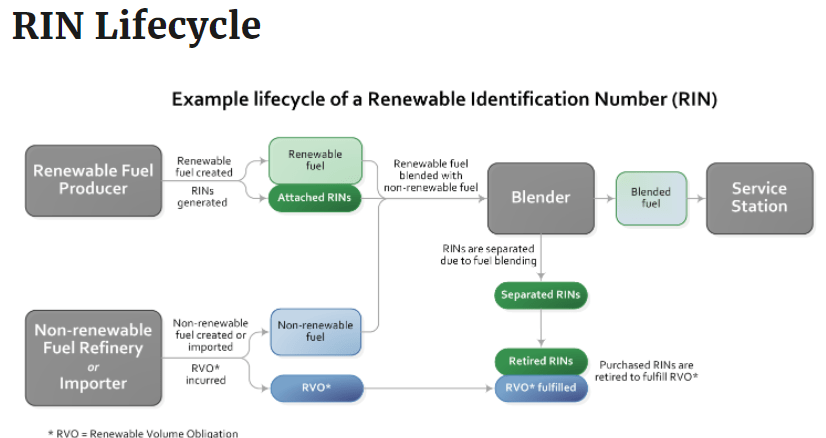

The next big thing for refiners is RINS (Renewable Identification Number). These are created by the distillation of ethanol for blending into gasoline. If this seems hideously complex and hard to track for you, we are in agreement. As a survivor of the crude price controls of the '70s, I strongly suspect there is a way to game this system. But it's the system we have.

RINs are traded and adjusted in price according to scarcity. If production of Ethanol falls off, the refining requirements (known as the RVO) continue, unless federal dispensation is received. This happens rarely. Currently, the federal government is mandating E-15 for the summer at a time when it normally goes to E-10. This great for the farmers, but potentially not so great for refiners, unless you produce them yourself.

{kind=link}

There is a lot of commentary percolating through the grapevine about blending costs to meet Tier 3 gasoline requirements, vs. crack spread margin capture. Tier 3 involves reducing S content to 10 ppm or less, and there is a performance cost associated with it that the government couldn't care less about. You do though as too low an octane number and your engine will knock like a door-to-door vacuum cleaner salesman. Just be aware that those back-end costs can haunt refiners.

Managing octane is done in a variety of ways in the early stages of refining, or through input blending. Costs like these-RINs, octane enhancers used to raise the RON to meet engine performance specs.

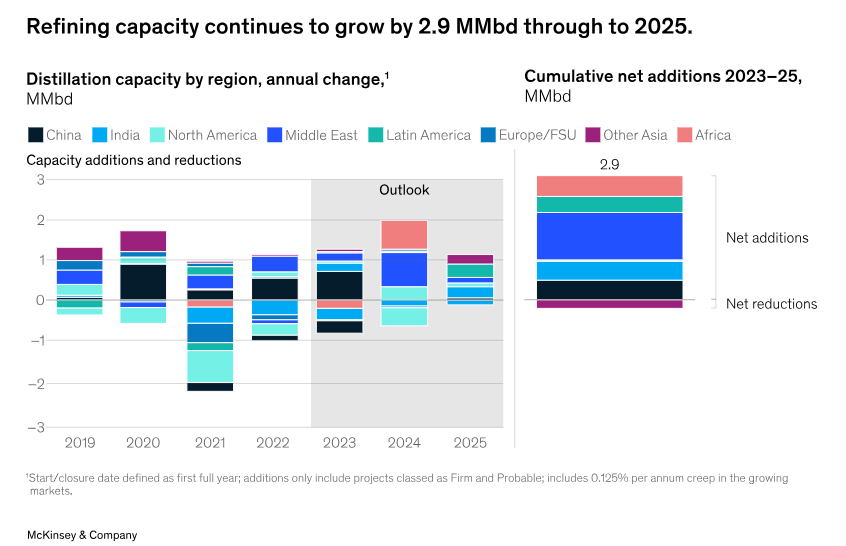

The macro environment for refiners is changing a bit. There is new capacity coming domestically and globally. Reuters notes that U.S. capacity will increase by several hundred thousand BOPD this year. Globally, McKinsey expects about 2.9 mm BOPD of new capacity coming online by 2025, with the biggest part of that increase coming here in North America.

{kind=link}

The thesis for VLO

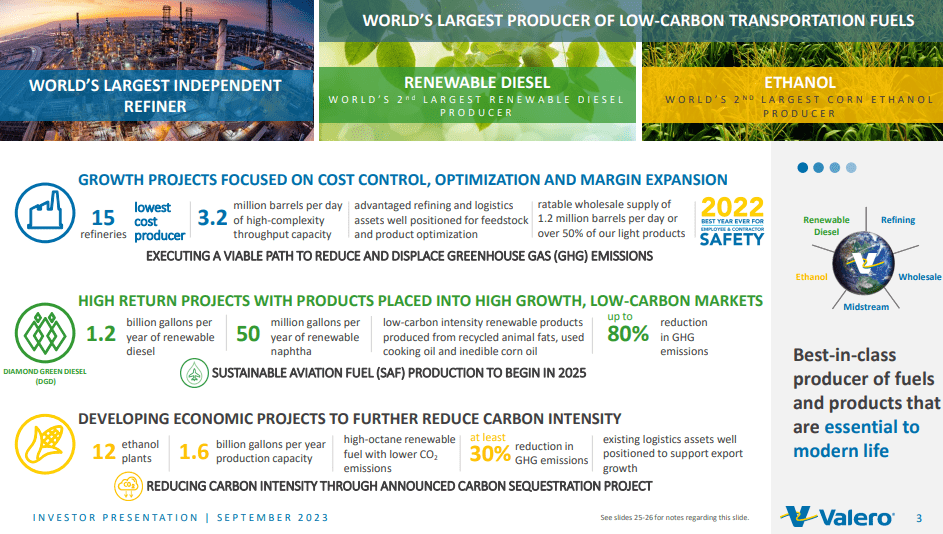

The company is the largest independent refiner globally, and its 3.2 mm BOPD of output constitutes ~12% of U.S. daily supply. Its petroleum refining footprint is advantageously positioned across U.S. markets. VLO controls some aspects of its RIN requirements through internal ethanol production and is a major producer of renewable fuels. The company has a number of expansion projects underway that will be accretive to future earnings.

VLO product mix (VLO)

{kind=link}

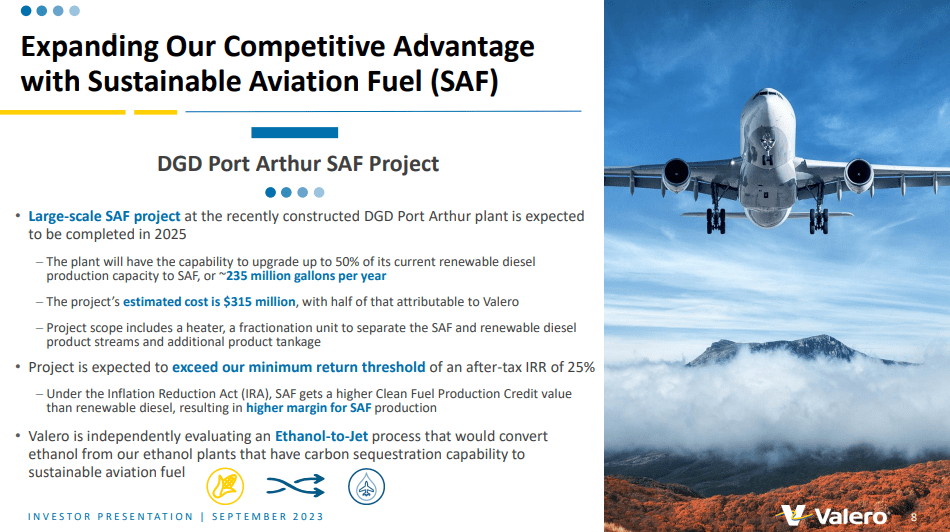

A near-term catalyst for VLO

The Port Arthur SAAS project under which it will be producing it Diamond Green Diesel and JetA fuels is scheduled to come online in 2025. These fuels will be advantaged by government incentives and end user commitments to use cleaner fuels and should be accretive to margins.

VLO SAS graphic (VLO)

{kind=link}

Risks

I see three key risks for VLO.

The first is electric vehicle ("EV") adoption. To the extent EVs capture market, VLO loses a customer. Current trends bring EV adoption projections into question, and the company discloses no concerns along these lines. Bloomberg discusses some of the challenges for EVs.

Near term, as the company discusses, crack spreads could be adverse through Q1 of next year. In this scenario, the current rally in shares might fade.

Global competition could be a challenge. Nobody drives the giant cars we do here in the States. Imports of refined products could chip away at margins.

Q3 2023 review and guidance

For the third quarter of 2023, net income was $2.6 billion or $7.49 per share, compared to $2.8 billion or $7.19 per share for the third quarter of 2022. Adjusted net income was $2.8 billion or $7.14 per share for the third quarter of 2022.

The refining segment reported $3.4 billion of operating income for the third quarter of 2023 compared to $3.8 billion for the third quarter of 2022. Refining throughput volumes in the third quarter of 2023 averaged 3 million barrels per day, implying a throughput capacity utilization of 95%. Refining cash operating expenses were $4.91 per barrel in the third quarter of 2023, higher than guidance of $4.70 per barrel primarily attributed to higher-than-expected energy prices.

Renewable Diesel segment operating income was $123 million for the third quarter of 2023 compared to $212 million for the third quarter of 2022. Renewable diesel sales volumes averaged 3 million gallons per day in the third quarter of 2023, which was 761,000 gallons per day higher than the third quarter of 2022. The higher sales volumes in the third quarter of 2023 were due to the impact of additional volumes from the DGD Port Arthur plant, which started up in the fourth quarter of 2022. Operating income was lower than in the third quarter of 2022, primarily due to a lower renewable diesel margin in the third quarter of 2023.

The ethanol segment reported $197 million of operating income for the third quarter of 2023 compared to $1 million for the third quarter of 2022. Ethanol production volumes averaged 4.3 million gallons per day in the third quarter of 2023, which was 831,000 gallons per day higher than the third quarter of 2022. Operating income was higher than in the third quarter of 2022, primarily as a result of higher production volumes and lower corn prices in the third quarter of 2023.

For the third quarter of 2023, G&A expenses were $250 million and net interest expense was $149 million. Depreciation and amortization expense was $682 million and income tax expense was $813 million for the third quarter of 2023. The effective tax rate was 23%. Net cash provided by operating activities was $3.3 billion in the third quarter of 2023. Included in this amount was a $33 million favorable change in working capital and $82 million of adjusted net cash provided by operating activities associated with the other joint venture member share of DGD. Excluding these items, adjusted net cash provided by operating activities was $3.2 billion in the third quarter of 2023.

Valero returned $2.2 billion to stockholders in the third quarter of 2023 of which $360 million was paid as dividends and $1.8 billion was for the purchase of approximately 13 million shares of common stock resulting in a payout ratio of 68% adjusted net cash provided by operating activities. VLO ended the quarter with $9.2 billion of total debt, $2.3 billion of finance lease obligations and $5.8 billion of cash and cash equivalents. Debt to capitalization ratio, net of cash and cash equivalents, was 17% as of September 30, 2023, and they ended the quarter well capitalized with $5.4 billion of available liquidity, excluding cash.

Guidance for Q4. Capex for Valero for the full year 2023 is expected to be approximately $2 billion, which includes expenditures for turnarounds, catalysts and joint venture investments. About $1.5 billion of that is allocated to sustaining the business and the balance to growth. For Q4, operations, VLO expects refining throughput volumes to fall within the following ranges: Gulf Coast at 1.77 million to 1.82 million barrels per day; Mid-Continent at 445,000 to 465,000 barrels per day; West Coast at 245,000 to 265,000 barrels per day; and North Atlantic at 470,000 to 490,000 barrels per day.

Source .

Your takeaway

VLO is trading at an attractive multiple in comparison to most of the refiner cohort-2.91X. We have just missed the Q3 dividend (Ex-div, 11-14), so there is no real pressure to jump in though, absent some catalyst that isn't readily apparent at this time. VLO is currently at its 200-day SMA, in what looks like a descending channel pattern to me. I think the best plan is to put VLO on a watch list for an entry point below the support level of $113. It made a double bottom in the $105 range this summer, so that might be a pretty good target.

{kind=link}

At the right price, I think we want to own VLO stock. Valero Energy Corporation's liquids fuels business is thriving and I believe it is positioned to do well in the coming years. Let's keep an eye on it, and be ready to jump if that $105ish level rolls around.

For further details see:

Valero Energy: Holding At Current Levels