VTC - VCLT: Long Term Corporates Now Yield Less Than Cash

2024-01-11 01:18:52 ET

Summary

- The Vanguard Long-Term Corporate Bond ETF has seen its yield to maturity fall below cash for the first time on record.

- The recent rally in the VCLT has been driven by a drop in long-term bond yields and narrowing credit spreads.

- The risks outweigh the rewards for the VCLT at present, but still-high real yields suggest it should still outperform US stocks absent a sustained rise in inflation.

I have been bullish on the Vanguard Long-Term Corporate Bond Index Fund ETF ( VCLT ) for over a year on the basis of high nominal and real yields. The ETF has performed reasonably well, rising 7% since my last update in May, but after the recent rally the yield to maturity on the index has fallen below cash for the first time on record. The deeply inverted Treasury curve and depressed credit spreads make long-term corporate bonds and the VCLT unattractive at present, and it would take a renewed rise in yields to warrant a bullish stance.

The VCLT ETF

VCLT holds a broad portfolio of long-term investment-grade corporate bonds and tracks the Bloomberg US Long-Term Bond Index. The current weighted average yield to maturity is 5.4%, having fallen from as high as 6.6% at the October peak. With a weighted average maturity of 22.7 years and a duration of 12.7 years, the fund is highly sensitive to interest rate changes, and the recent rally in the ETF has been mainly due to expectations of aggressive easing by the Fed. In terms of credit risk, over half of the fund's holdings in A-rated credits or higher. When compared with other bond ETFs the VCLT's long duration means it has much higher sensitivity to interest rate expectations relative to the Vanguard Total Corporate Bond ETF ( VTC ) which results in higher volatility. The fund charges a negligible expense fee of just 0.04% and has seen rapid inflows over the past few years resulting in a market capitalization of $6.8bn.

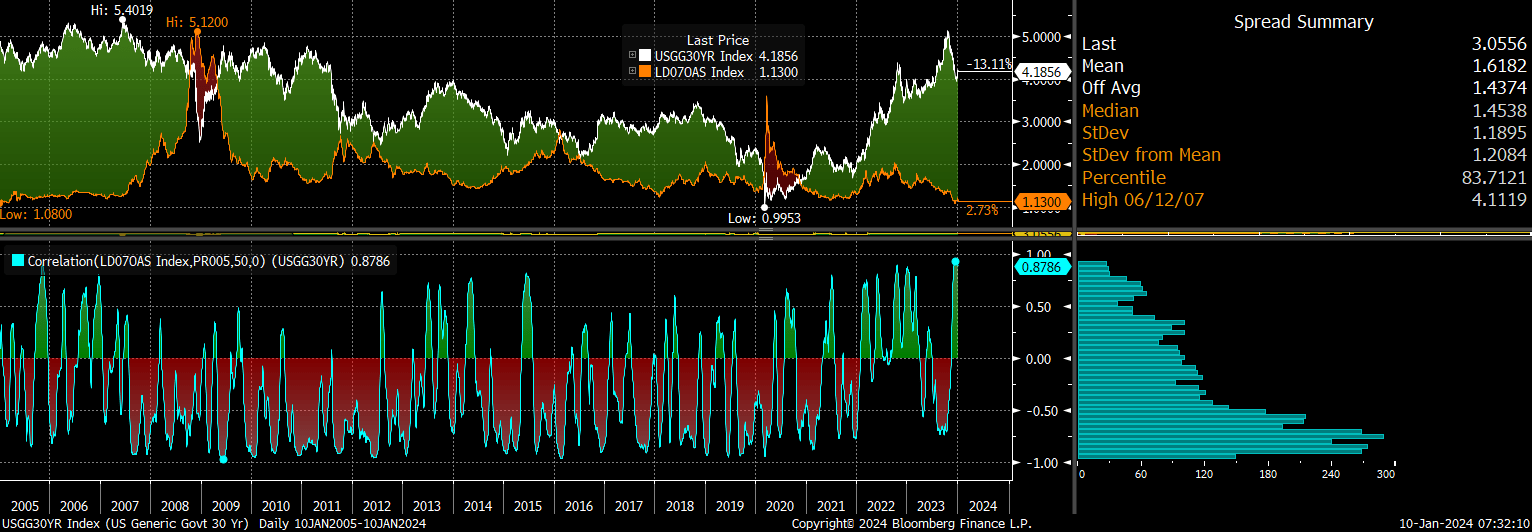

Treasury Yields And Credit Spreads Have Moved Together Amid Soft Landing Optimism

The strong rally seen in the VCLT over the past three months has been primarily due to the sharp drop in long-term bond yields, which have fallen by around 100bps. In contrast to previous sharp declines in UST yields, this period has also seen credit spreads narrow as investors have embraced the idea of normalisation of inflation and a soft landing scenario. The chart below shows the 50-day rolling correlation between 30-year UST yields and long-term credit spreads is at its highest level in almost two decades.

Correlation Between 30-Year UST Yield And Long Term Corporate Credit Spreads (Bloomberg)

{kind=link}

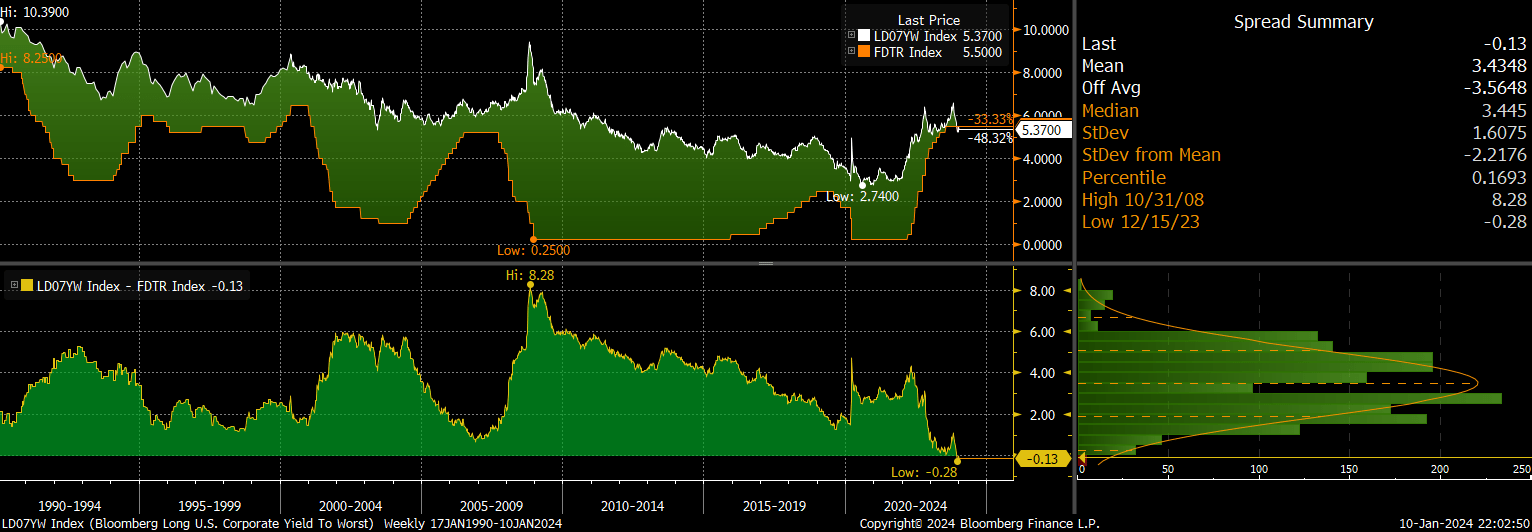

As a result of this drop in UST yields and credit spreads the VCLT now yields less than the Fed funds rate for the first time on record going back to 1990. Over this period the average spread of long term corporate yields over the Fed funds rate has been 3.4%, reaching as high as 8.3% during the global financial crisis.

Long Term Corporate Yield Vs Fed Funds Rate (Bloomberg)

{kind=link}

In order for the VCLT to outperform cash over the coming years we would need to see the Fed lower rates without a significant rise in default rates and credit spreads, which is something that has not occurred since the early-1990s. This would likely require a continued decline in inflation readings and the avoidance of a recession, and while this is certainly possible, the 5.4% yield on the VCLT is not high enough to compensate for the risk of unforeseen shocks. Perhaps the biggest short term risk comes from a recovery in oil prices which would put renewed upside pressure on inflation and cause investors to pare back their rate cut expectations.

Still A Better Bet Than Stocks

Although the risks outweigh the reward for the VCLT at present, it is still highly likely to outperform US stocks over the coming years unless we see a sustained rise in inflation. The 5.4% yield compares with a dividend yield of just 1.5% on the S&P500, which means that dividends would have to grow by 3.9% annually for the VCLT to underperform, assuming no change in valuations.

Long Term Corporate Yield Vs SPX Dividend Yield (Bloomberg)

{kind=link}

With long-term breakeven inflation expectations sitting at just 2.2%, this would require a 1.7% real annual rise in dividend payments, which in turn would likely require a 1.7% rise in real earnings, sales, and US GDP. Based on the slowing growth in working age population and productivity growth, real GDP is likely to average below 1%, meaning that it would require a sharp rise in inflation for the S&P500 to outperform. Even if this were to occur, the scope for capital losses is significantly higher in stocks relative to the VCLT.

For further details see:

VCLT: Long Term Corporates Now Yield Less Than Cash