VGR - Vector Group Is A Steady 'Buy' In Tobacco

2023-11-19 03:52:42 ET

Summary

- Vector Group Ltd. is a diversified holding company in the tobacco sector, with its brands, including the fourth largest cigarette brand in the US, Montego.

- The company's operating income increased by 7.6% in 2022, driven by the sales of its Montego brand.

- Regulatory challenges, such as the FDA's potential ban on menthol cigarettes, could impact VGR's products, but the stock is undervalued and offers a robust dividend yield.

Vector Group Ltd. ( VGR ) is a diversified holding company focusing mainly on the tobacco sector with its subsidiaries, Liggett Group and Vector Tobacco. VGR’s brands stand out, especially in the deep-discount cigarette segment. Montego is marketed as an American-made cigarette with a discount; it is the fourth largest in the U.S., behind Marlboro, Newport, and Camel. Liggett outperformed the industry with an operating income increase of approximately 7.6% compared to 2022, principally thanks to the sales of its Montego brand. However, the company has to face possible regulatory hurdles with the FDA’s finalizing of a ban on menthol cigarettes that could impact VGR’s products. Still, from a valuation perspective, my model indicates the stock is significantly undervalued. In my opinion, this undervaluation, coupled with its robust dividend yield, makes it a solid “buy” in the tobacco sector, particularly for dividend investors.

Business Overview

Vector Group Ltd. is a diversified holding company that owns and operates brand names in the tobacco and real estate industries. VGR had headquarters in Miami, Florida, with offices in Manhattan, New York. The company is part of the S&P SmallCap 600 and Russell 2000 Index. These indexes follow the performance of small-cap American stocks with a total market capitalization of $850 million to $5.2 billion.

Its subsidiaries, Liggett Group and Vector Tobacco, run the tobacco segment. Their brands include Pyramid, Grand Prix, Liggett Select, Eve, Montego, and USA. The Montego brand is the fourth largest in the U.S., behind Marlboro, Newport, and Camel; it is marketed as an American-made cigarette at a discount. The current cost advantage per pack is $0.92 compared to the largest U.S. tobacco companies. In the third quarter of 2023, the discount tobacco market grew 10.5% while industry volumes declined.

Source: Investor Presentation November 2023

The discount segment is competitive because consumers prioritize price over brand loyalty. Liggett’s competitors are large manufacturers like Philip Morris USA, RJ Reynolds Tobacco Company, ITG Brands LLC, and other smaller tobacco manufacturers and importers. VGR's advantage is that around 35% of current volumes in this segment are exempt from payment due to the perpetual Master Settlement Agreement ((MSA)) signed by tobacco companies and US states in 1998. This exemption ranges from $160 million to $170 million for Liggett and Vector Tobacco from 2013 to 2022. Under the MSA, Liggett has no payment obligations unless its market share exceeds an exemption of approximately 1.65% of total cigarettes sold in the United States, and Vector Tobacco has no payment obligations unless its market share exceeds an exemption of roughly 0.28% of total cigarettes sold in the United States.

{kind=link}

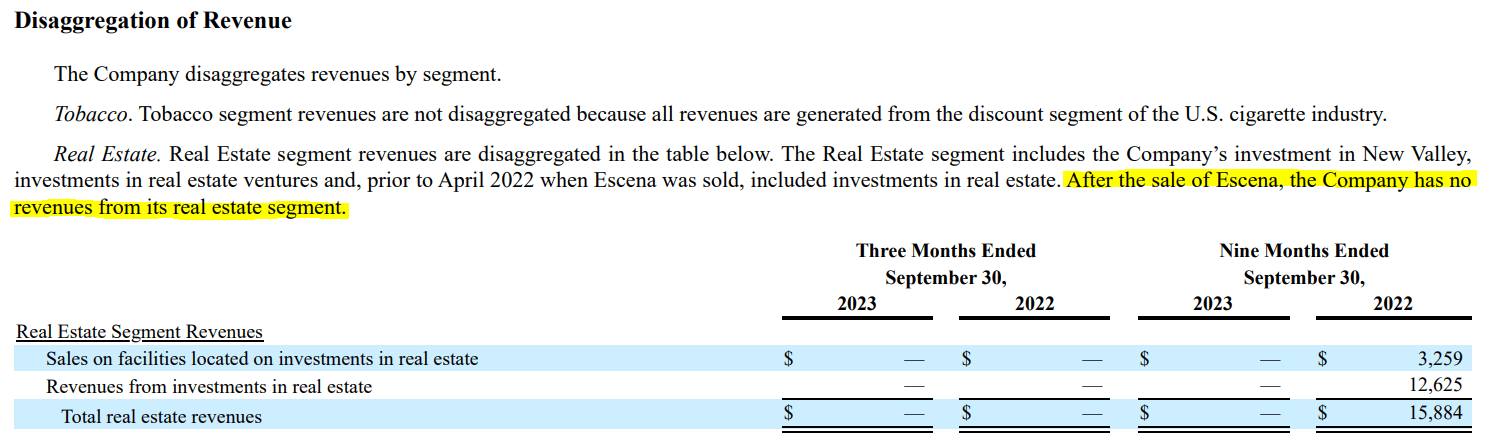

Additionally, VGR has a real estate angle as well. VGR owns New Valley LLC, which has minority investments in real estate projects like cooperatives, condominiums, and apartments across the US. Nevertheless, for the nine months that ended on September 30, 2023, the revenues for this segment dropped to $0 from $15,884 in 2022, even though VGR’s New Valley still maintains approximately $122 million invested in real estate and ownership percentages. Still, this revenue drop can be misleading because these real estate assets' income shows up in VGR’s other income, earnings, and losses from real estate ventures. For the last quarter, this figure was $3.74 million.

Tobacco Economics, Inflation, and Regulatory Challenges

Moreover, inflation significantly impacts manufacturing costs, especially in processing leaf tobacco and raw materials. Despite decreased sales, the tobacco gross profit has increased due to an 8% increase in pricing. Operating income for the Q3 2023 increased by 7.6% to $94.8 million. For the first nine months of 2023, revenues slightly increased tobacco-adjusted EBITDA by 5.6%?.

In the last 10-Q , VGR reported its financial situation as of September 30, 2023. The company presented a consistent cash flow with approximately $437 million in cash and cash equivalents, with investment securities and long-term investments for $174 million. Net income and adjusted EBITDA increased from $52.7 million to $94.9 million in 2023. The retail shipments of the Liggett Group outperformed the industry with an operating income increase of approximately 7.6% compared to 2022, principally thanks to the sales of its deep-discount Montego brand.

Investor Presentation November 2023

However, VGR faces a potential challenge because the FDA announced that they will finalize a ban on menthol cigarettes in the coming months. The VGR's star of tobacco products, the Montego brand, offers menthol cigarettes. Therefore, it is unsurprising that VGR opposes the ban, arguing that it could lead to an unregulated market. Menthol masks the harshness of tobacco flavor, making it easier to consume it. The menthol in tobacco is considered an incentive to acquire the smoking habit. Evidence indicates that a ban has health benefits that outweigh potential losses in tax revenue. If the FDA ruling is legally challenged, a court is likely to confirm a menthol ban for the protection of public health.

Valuation Analysis: A Deep Discount

From a valuation perspective, the analysis is rather simple. VGR doesn’t have explosive growth, making its revenues somewhat stable. It doesn’t have a complicated corporate structure, either. However, I think the best approach at this point is to use the latest quarterly figures and annualize them, given the ongoing changes in the company. I believe that is a more representative assessment of its revenue capabilities and profitability margins.

In that sense, the company reported $364.11 million in revenues for the latest quarter, which I annualized in my model. I also used the latest quarter's EBIT margins of 24.8% in my assumptions. Lastly, I think it’s best to simply bypass most of the tax variables by using a flat corporate tax of 21% assumption. Other than that, I used the same approach for the D&A and CAPEX figures but annualized the YTD figures because of their slightly different nature. Then, I discounted the implied FCFFs at the company’s WACC of 7.5%, using its credit rating of Ba3 from Moody’s . These bonds currently yield about 7.2% , which is my cost of debt input.

Author's elaboration.

The result of my valuation model suggests that VGR is significantly undervalued. My model indicates a fair value of roughly $4.75 billion, implying an upside potential of 186.5% from current levels. However, I think a certain “tobacco discount” is appropriate, and indeed, I think that offsets my valuation to some extent. Nevertheless, the disparity is large enough to consider VGR still undervalued.

Moreover, it’s also a stock with an undeniably attractive dividend yield of 7.58%, further solidifying my “buy” rating for VGR. The payout ratio of 67.8% is indeed high, casting doubts on the dividend's safety. Yet, when looking at the free cash flow figures of approximately $350.0 to $400.0 million per year, it’s not so unsustainable. For context, the next year, it’s expected to pay $0.80 in dividends per share, which would be about $123.2 million in cash dividends paid. Yet, this would only be approximately 35.2% to 30.8% of the company’s free cash flow. Thus, I think the dividend is likely sustainable, and its yield is exceedingly attractive, coupled with a clearly undervalued market cap.

VGR has been a choppy stock over the last five years but now appears to trade near the bottom of its historical trading range. (TradingView.)

Risks to the Investment Thesis

Generally, the company’s main risk is declining tobacco consumption over time. There’s a stigma associated with smoking nowadays, and this will undeniably be a headwind for the foreseeable future. Moreover, advertising VGR’s products is often challenging due to regulatory requirements and limitations, so I doubt VGR’s revenues will increase significantly over the long run (other than with inflation). Also, the company’s debt is notable as it’s 56.1% of its total enterprise value. Yet, I think it’s a manageable debt , and coupled with its free cash flow of at least $350 million per year, it seems like a sustainable capital structure.

Another current major risk for VGR is the near FDA ban on menthol cigarettes that could affect the mentholated versions of VGR’s products, including the Montego brand. This can disrupt a revenue stream for the company and would hit my valuation estimate by extension. Nevertheless, as a whole, the current discount is so steep that I think these risks are wholly offset by it.

Conclusion

Overall, I think VGR is a nice and simple tobacco company, especially after the divestitures and spinoffs it has made in recent years. The result is that now VGR is truly a tobacco pure play and generates a steady stream of free cash flows that broadly cover the dividend for shareholders. Moreover, I estimate that VGR is significantly undervalued by up to 186.5% before considering any tobacco discount in my assessment. Yet, after all is said and done, I think the stock is a good investment at these levels, especially for dividend investors looking for simple and reliable companies with attractive dividend yields.

For further details see:

Vector Group Is A Steady 'Buy' In Tobacco