IQV - Veeva: Downside Risks Driven By Slowing Revenue Uncertain Product Adoption And Increasing Competition

2024-01-08 10:52:52 ET

Summary

- Veeva's revenue growth has slowed over the past two years and is expected to continue to slow in FY24.

- Uncertainties surrounding product adoption, platform migration, and competition pose risks to Veeva's future growth.

- Veeva's valuation is considered optimistic, and the stock could have a downside of approximately 20% over a 5-year investment horizon.

Investment Thesis

Veeva ( VEEV ) climbed close to 20% in 2023, underperforming both the S&P 500 and the Nasdaq 100. The company has experienced a slowdown in its revenue growth and non-GAAP operating margin over the last two fiscal years, and the slowdown is expected to continue in FY24. While the outlook for FY25 is more optimistic across both the top and bottom lines, amidst a growing TAM and a robust product portfolio, I believe that Veeva’s +20% revenue growth days are over. Furthermore, I believe that the stock is overvalued at current levels and could have a downside of approximately 20% over a 5-year investment horizon.

My thesis for Veeva is driven by my quantitative and qualitative analysis, where I believe that there are growing uncertainties around Veeva’s product adoption in an environment where pharmaceutical budgets continue to come under greater scrutiny. Furthermore, there are a lot of unknowns as to the impact on the top line that Veeva’s platform migration projects might cause, especially as Veeva’s revenue is heavily reliant on a few large customers. Finally, there is a growing threat of competition from large players with huge resources at their disposal, such as Salesforce ( CRM ), Microsoft ( MSFT ) and Google ( GOOG ) who have already built their life sciences cloud offerings, which further slowdown Veeva’s market penetration despite a growing TAM.

About Veeva

Veeva is the leading provider of industry cloud solutions for the global life sciences industry. Their vision is to become the strategic technology partner for the life sciences industry and achieve long-term leadership with their solutions that support the research and development (R&D) and commercial functions of life sciences & pharmaceutical companies.

Veeva offers its solutions primarily via 2 major product families:

-

Veeva Development Cloud: Includes application suites for the clinical, regulatory, quality, and safety functions of life sciences companies that enable customers to streamline their end-to-end business processes.

-

Veeva Commercial Cloud: Comprises software and data solutions specifically built for life sciences companies to more efficiently and effectively commercialize their products.

The company uses a combination of subscription-based pricing and professional services to generate revenue.

Peter Gassner is the co-founder and CEO of Veeva and owns around 8.2% of the company. He has a deep industry background in the life sciences and customer relationship management ((CRM)) space, and I believe his deep industry focus has enabled him to lead the company to develop targeted solutions, adapt to regulatory changes, and incorporate relevant enhancements into existing solutions at a rapid pace.

The Good: Veeva’s growing TAM and impressive product roadmap

Veeva’s growing TAM gives it opportunities to expand

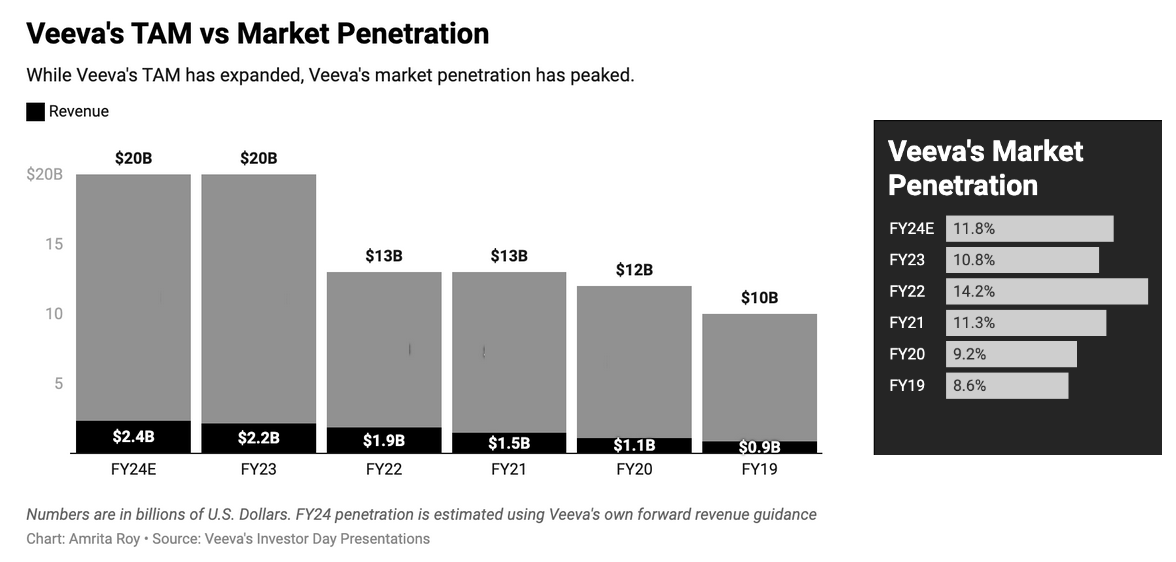

With the benefits of having an established cohort of management executives, Veeva constantly keeps revising their north star metrics and diligently keeps investors updated on changes that include forward-looking projections. I state this because Veeva keeps refreshing their TAM regularly as they align the future vision of their product roadmap with their target markets. After perusing through their investor day presentations going back to 2019, I was able to estimate their market penetration, as seen below.

Veeva Investor Day Presentations

{kind=link}

Between 2019 and 2021, Veeva’s estimated TAM expanded by 30% to $13B . By 2023, Veeva’s TAM had expanded 1.5 times to $20B . One of the main reasons for the augmentation in TAM was seen in the expansion of Veeva into newer segments of the target markets. Over the last 2 years, Veeva has built an impressive product roadmap that not only allows them to branch off from their product’s dependence on Salesforce’s platform but also uses their newfound independence to expand into emerging segments in MedTech, such as clinical data. So far, from the chart above, it appears that Veeva’s platform relationship with Salesforce confined Veeva into a corner of the target market, but the hope is that a stronger product roadmap can potentially lead Veeva into expanding its market share into an expanding TAM.

Veeva has built an impressive product roadmap

Veeva announced in December 2022 that they would not be renewing their platform agreement with Salesforce after 2025. The legacy Veeva CRM solutions were built on Salesforce’s Salesforce1 platform. With this, the doors to aligning its product strategy with emerging MedTech segments have opened. Veeva has been busy in the years after the world emerged from the pandemic lockdowns preparing for a product roadmap without Salesforce’s platform while building and executing on their product strategy.

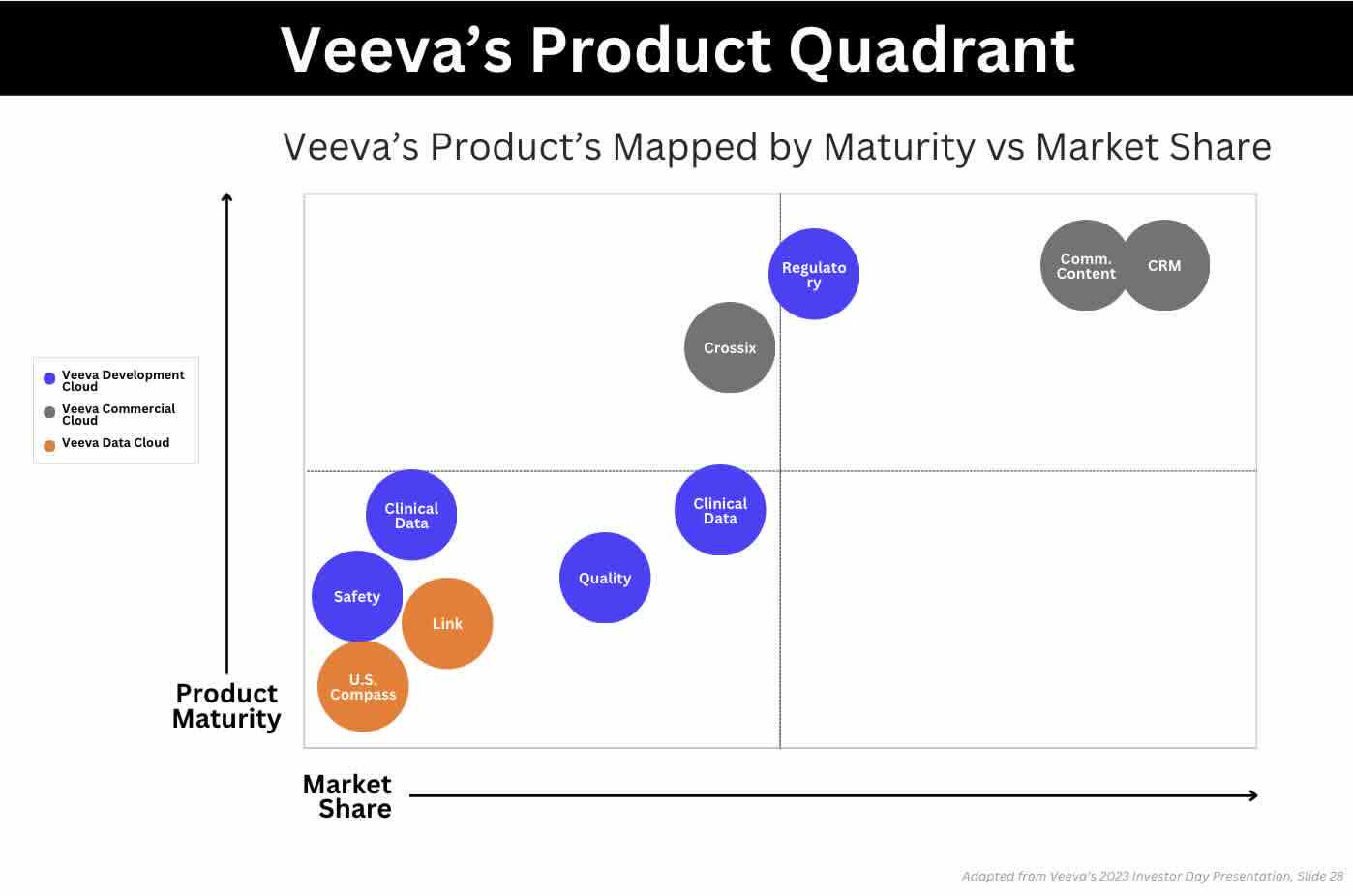

I have attached a slide from Veeva’s most recent investor day slide deck that maps the growth stage of all their products vs. implied market share. I have also slightly altered the slide from the original investor slide to show the different products by different product verticals.

{kind=link}

The left quadrant of the chart above tells me that Veeva has a robust set of products that have been recently released to their customers. Given some of the success that their CRM & Regulatory products saw, management sees adoption trends continuing into their new products as well, especially in their Veeva Data Cloud suite of products. I believe that their data products are mostly geared towards customers that depend on looking at analytics and real-time data, putting them directly in collision with an established incumbent in this space, IQVIA ( IQV ).

The bad: Uncertain product adoption, increasing competition, slowing revenue growth & unfavorable valuation

Fundamental Headwinds: Product adoption, migration & competition

While Veeva has a great management and product roadmap and has the advantage of being highly verticalized with their product offerings in the life sciences space, I believe there is severe uncertainty as customers evaluate Veeva’s new products, which is even more critical for Veeva as they migrate to Veeva’s new platform. Veeva CRM is the most critical product for Veeva in terms of adoption, revenue generation, and maturity. This product was built on a legacy platform that harnessed the technology of its platform partner, Salesforce. With the relationship having ended and Veeva having elected to build the platform using internal resources from the ground up, I believe there is a huge unknown as to the issues that customers may face during the migration phase until 2025. This is especially concerning because Veeva has a very small customer base and leans heavily on a few customers, such as pharmaceutical giant Merck ( MRK ), which leaves Veeva very little room for error.

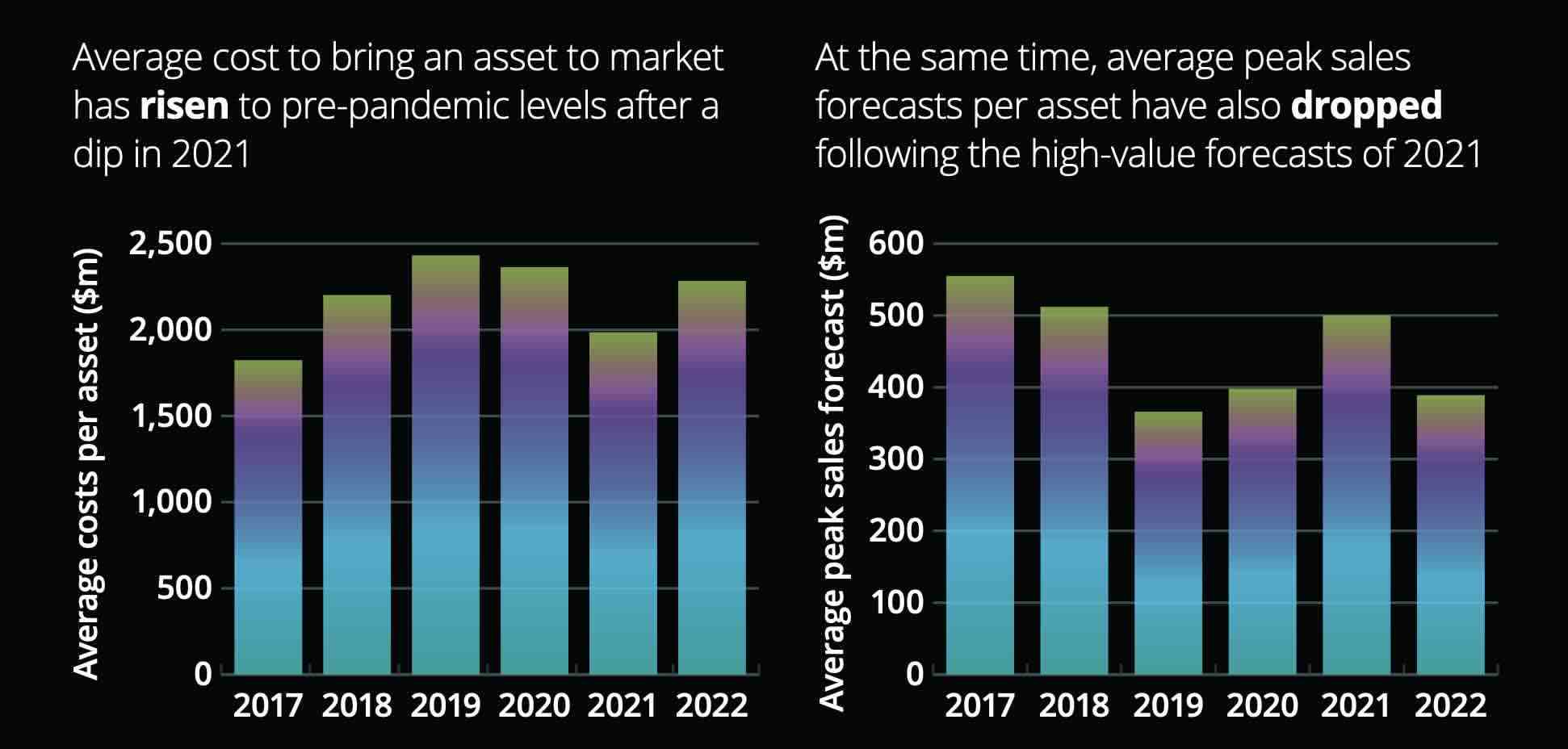

Moreover, this migration of Veeva’s core product coincides with another development in the world of pharmaceuticals, where it has become more cost-intensive for pharma companies to develop their pharma assets and launch them into the market. As per a study conducted by Deloitte on the R&D spend of the Top 20 pharma companies in the world, the average cost to develop an asset from discovery to launch increased 13.5% to $2.2B in 2022, while the average forecast peak sales per pipeline asset for the combined cohort decreased from $500M in 2021 to $389M in 2022.

Deloitte Study, 2023 - Measuring the return from pharmaceutical innovation

{kind=link}

I believe these trends may persist in light of continued uncertainty in the economy and higher rates pushing large pharma companies to scrutinize their budgets even more, thus adding downward pressure on Veeva’s revenue prospects. In their Q3 FY24 earnings call , when specifically asked about shrinking pharma R&D budgets, Veeva’s CFO mentioned that his base case assumption was that the “macro conditions would continue to play out.”

Finally, with Veeva wrapping up their platform agreement with Salesforce, it is also unknown how Salesforce and other large cloud companies with huge resources at their disposal may dent Veeva’s market share expansion ambitions. Salesforce wasted no time in launching their own life sciences cloud now that their relationship was terminated with Veeva. Other hyperscalers, like Microsoft and Google, already have their own life sciences cloud offerings. IQVIA, a clinical data and healthcare analytics company, has gotten so aggressive in defending its market share that Veeva’s CEO called them out on the most recent earnings call:

The anticompetitive behavior of IQVIA also creates significant barriers there because let's say the customer is using the IQVIA data for one data product, and we're selling one data product. And our services are necessary to mix those 2 data products together to provide a solution for the customer as well. IQVIA is not going to allow us to do that. They're not going to grant, let's call it a third-party agreement. So that's what slows things down.

Veeva’s revenue growth is slowing at a rapid pace

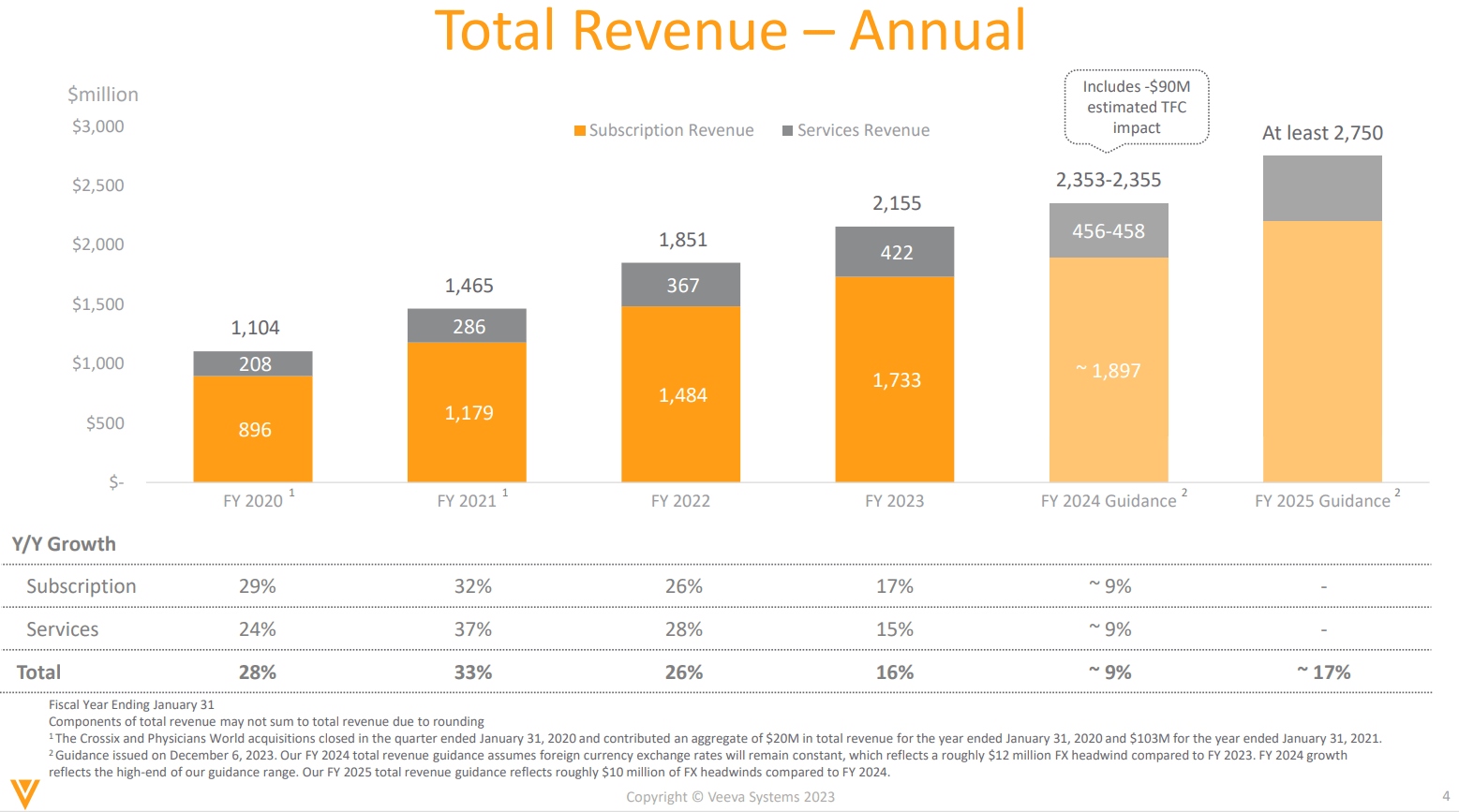

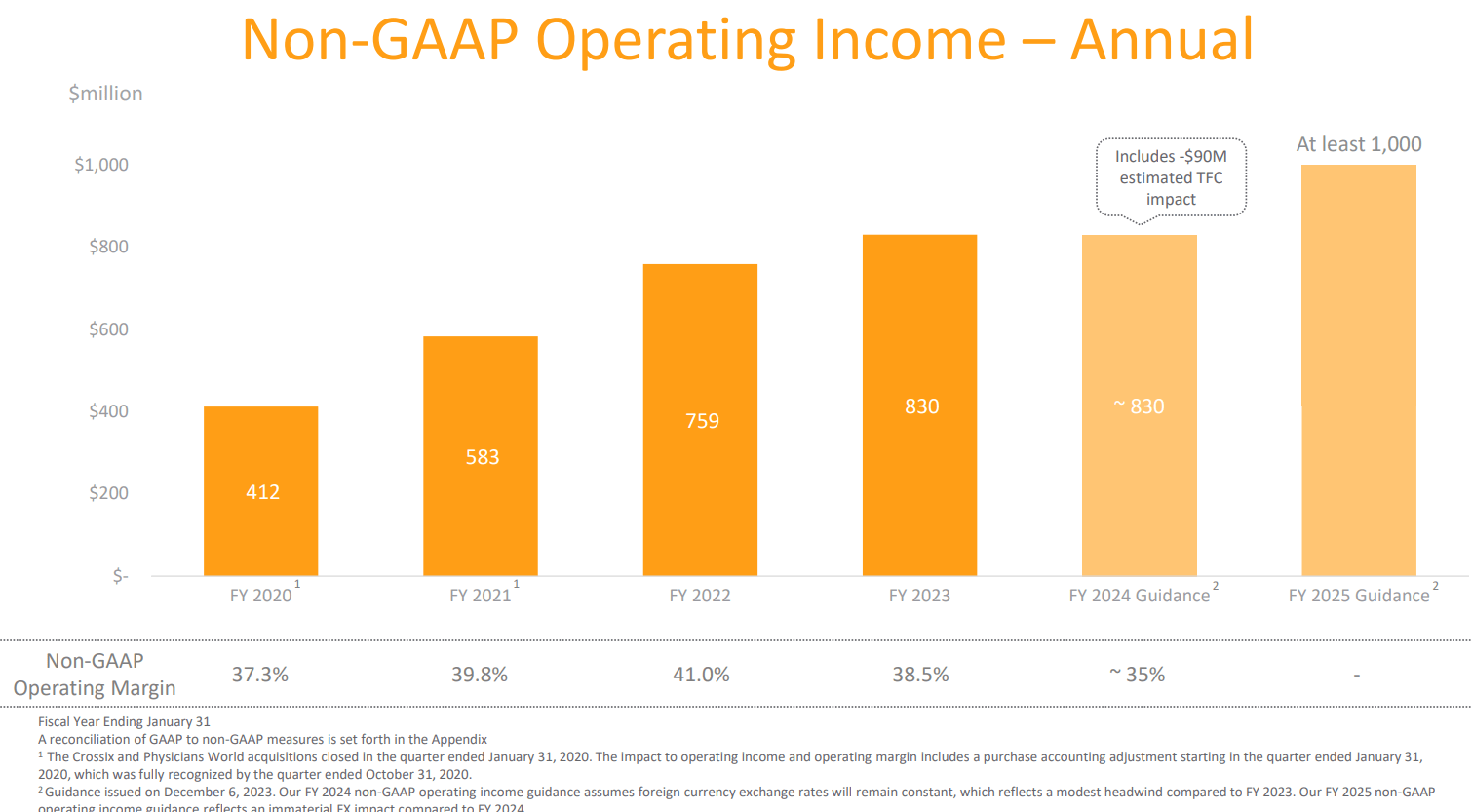

Veeva produced revenue and earnings growth in Q3 FY24 that came in at expectations. Revenue grew 12% YoY to $616.5M. Subscription revenue contributed 80%, while revenue from Professional Services made up the remaining 20%. Meanwhile, non-GAAP income grew slower than revenue at 7%, with the non-GAAP operating income margin dropping to 38% from 39.7% a year ago. While Sales and Marketing spend as a percentage of revenue remained steady on a YoY basis, the decline in non-GAAP operating margin was driven by a faster increase in R&D spend, which accounted for 26% of revenue in Q3 FY24 vs. 23% of revenue in Q3 FY23.

Shifting gears to FY24 guidance, Veeva’s management is guiding for a revenue of $2.355B, which represents a 9.2% growth on a YoY basis. Even if I take into account the projected negative impact of $90M on the top line as a result of the customer contracting change that standardized terminations for convenience ((TFC)) rights in 2023, revenue growth would have still slowed to 13% in FY24 from 16% in FY23.

From here on, the management expects revenue to grow 17% to $2.75B in FY25. This would mark the third consecutive year of sub-20’s revenue growth, despite a growing product portfolio that I had previously reviewed in this post. Furthermore, given uncertainty around migration and its impact on the top line, coupled with increasing competition in the space, I would not expect Veeva to go back to its mid- to higher 20’s level of revenue growth rate and instead see its revenue growth normalize to mid-teen levels over the next 5 years with the current product roadmap in place.

{kind=link}

Meanwhile, the management also expects non-GAAP operating income of $830M in FY24, which would translate to a non-GAAP operating margin of 35%. As for FY25, management expects non-GAAP operating income of $1B, which represents a growth rate of 20% on a YoY basis, in line with FY25 revenue growth projections. At the same time, the non-GAAP operating margin will improve to 36.3%. While this is an improvement from FY24 levels, the overall non-GAAP operating margin is worsening incrementally when compared to FY20, FY21, and FY22.

{kind=link}

Moving forward, I expect the revenue growth rate to normalize at 15% over the next 5 years. Given historical performance and management’s focus on profitability, I would also expect non-GAAP operating income to grow in line with revenue growth during this period of time. Should that be the case, my expectation is that Veeva should produce close to $4.8B in revenue and $1.7B in non-GAAP operating income with a 35.3% margin by 2029.

Veeva’s valuation is still too optimistic

Veeva is currently trading at a forward price-to-earnings ratio of 33.5 based on its earnings expectation for FY25. As per management’s guidance, Veeva is expected to grow its revenue and non-GAAP operating income by 16% and 20%, respectively, in FY25.

Taking S&P 500 as a proxy, where S&P 500 companies are expected to grow their earnings by 10% as per FactSet , Veeva should be trading at 1.6 times the forward price-to-earnings multiple of S&P 500. The current forward price-to-earnings ratio for the S&P 500 is 20. Given that, Veeva should not be trading at a forward multiple of over 32. Currently, Veeva is trading 3% over that. In other words, if Veeva fails to surprise its earnings estimates and forward guidance by less than 3%, it will most likely see short-term volatility in 2024. In the coming quarters, I believe the management will continue to sound cautiously optimistic around their migration project and the evolving competitive landscape, where I don’t expect them to revise their FY24 and FY25 projections higher for both the top and bottom line. As a result, I expect the stock to remain range-bound with possible bouts of negative short-term volatility given its current pricing.

However, when I assess the company on a 5-year investment horizon, it becomes clear to me that the stock is likely overvalued at current levels. Assuming that the company is able to produce $4.8B of revenue and $1.7B in non-GAAP operating income in 2029, as I had stated earlier per my assumptions, it would equate to a present value of non-GAAP operating income of $1.1B, or an adjusted earnings per share of $7.0, if discounted at 8.3%. Once again, taking S&P 500 as a proxy, where it has grown its earnings by 8% on average over the last 10 years, as per FactSet, with a price-to-earnings multiple of 15–18, I believe that Veeva should be trading at a price-to-earnings multiple that is 1.5 times that of S&P 500 in 2029. As a result, I believe that over a 5-year investment horizon, the price-to-earnings ratio of Veeva should be no greater than 27 in 2029. This would mean that the fair value of Veeva’s stock is around $150, which translates to a 20% downside from current levels.

Authors' 5-year investment valuation model

Conclusions

Veeva is experiencing a slowdown in its revenue growth and non-GAAP operating margin. Although the company operates in a growing TAM with an impressive product portfolio and management that has historically remained focused on profitability, dark clouds are starting to form in areas of product adoption, competition, and concerns related to the migration project.

Given my above concerns, I believe that Veeva’s 20+ revenue growth days are over, and I expect revenue to normalize in the mid-teens moving forward over the next 5 years, with non-GAAP operating margin growing in line with revenue. This would mean that Veeva’s stock is overvalued today, and the stock could have a downside of around 20% over a 5-year investment horizon.

For further details see:

Veeva: Downside Risks Driven By Slowing Revenue, Uncertain Product Adoption And Increasing Competition