IQV - Veeva Systems Q3 Preview: Navigating Challenges And Opportunities For F2025

2023-11-29 13:05:34 ET

Summary

- Veeva Systems Inc. stock is well-positioned with lower expectations as it prepares to report its fiscal Q3 2024 results.

- Assessing the potential benefits for investors as Veeva transitions from its fiscal year 2024 to fiscal 2025.

- Why paying 26x forward free cash flows is now a better entry point for Veeva Systems.

Investment Thesis

Veeva Systems Inc. (VEEV) stock is well-placed with lower expectations, as it heads to report its fiscal Q3 2024 results, expected post-market on Wednesday 6 December 2023.

I now believe that this is a good entry point for investors to start averaging into their holding of Veeva.

For a long time, as you'll soon see, I've been neutral on Veeva. But given that its suboptimal fiscal 2024 year is now almost coming to a close, investors have better prospects ahead as they look forward to fiscal 2025 (starting February 2024)

In summary, I argue that paying 26x forward free cash flows for Veeva is a fair price to pay for this business. The best risk-reward this stock has offered for a long while.

Rapid Recap

In my previous analysis at the start of September, I said,

While I don't consider the stock to be particularly cheap, I have to say, that Veeva continues to grow into its valuation. This means that if Veeva can be counted on to grow at around 20% CAGR in fiscal 2025 and for a few more years beyond that, this valuation is a fair at this point.

[...] I find Veeva's fiscal 2025 now attractive enough that I'm now able to revise my hold rating to a tepid buy rating.

Author's work on VEEV

As you can see above, for a long while I was neutral on Veeva, as I argued that this year would not see a lot of appreciation as the stock was too richly priced for what it offered.

I then became tepidly bullish, as fiscal 2024 (its transition year) was nearing a close.

And now, since my previous analysis, the stock has become more attractively priced. The stock isn't a clean blemish-free story, but I believe that the combination of its reasonable growth with very strong profitability should support this stock's valuation.

Veeva's Near-Term Prospects

In Veeva's upcoming fiscal Q3 2024 earnings call, Veeva undoubtedly will seek to paint a bullish picture, even as it acknowledges that it's having to navigate a challenging macro environment, such as continued project scrutiny and a challenging funding landscape for smaller companies.

Given these ongoing industry shifts, Veeva will have to double down on its work effort as it also has to migrate existing customers to Vault CRM by 2025, which means that there's considerable risk in this period, which will demand tremendous effort across sales, product, and services teams.

The success of this transition will be critical for Veeva's sustained leadership in the commercial solutions space.

Furthermore, the competitive landscape, particularly in the data domain with Veeva's products Compass challenging established players like IQVIA Holdings Inc. (IQV), signifies that there's plenty of execution risk for Veeva.

Veeva's Transitional Year, Fiscal 2024

{kind=link}

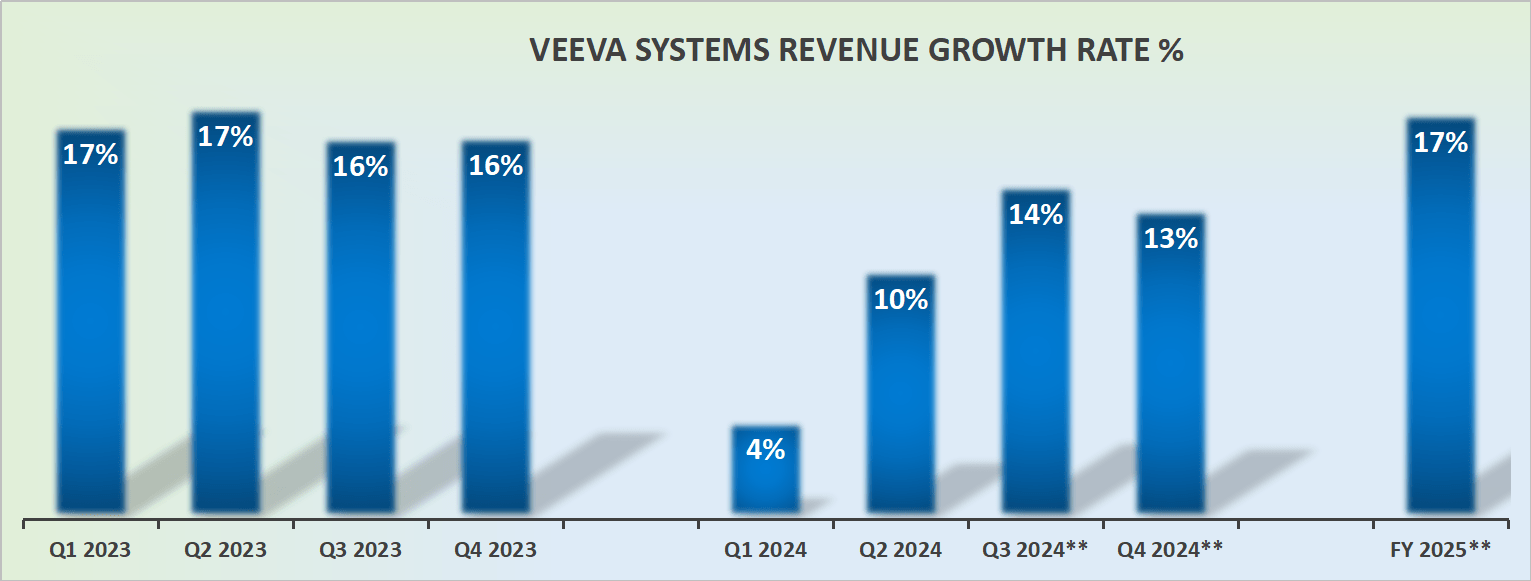

Veeva has long made clear that fiscal 2024 would be delivering suboptimal growth rates as the company embraces its TFC standardization (the contract adjustment), but that starting in less than 90 days' time, in fiscal 2025 (starting February 2024), the business should be able to deliver a more attractive rate of return.

Given this context, I believe the following table is helpful.

SA Premium

What we see here is that Veeva only barely beats analysts' estimates by around 1%-2% each time. To put this more concretely, this means that when Veeva is guiding for fiscal 2025 to grow at about 16% to 17%, it will be very unlikely that Veeva will be able to higher than 20% CAGR in fiscal 2025.

And on top of that, investors should remain mindful, that this approximate 17% y/y growth rate comes on the back of rather a lackluster year, which means that the comparables have been made easier.

Therefore, investors should not be expecting that on a normalized pace for Veeva to grow much faster than around 12% to 14% CAGR.

VEEV Stock Valuation -- 26x Forward Free Cash Flow

As discussed already, Veeva Systems doesn't have a habit of under-promising and overdelivering to any great extent. Consequently, when Veeva guides for at least $1 billion of non-GAAP operating income, I believe that this is generally the right ballpark to think about.

Even if Veeva ends up delivering around $1.1 billion of non-GAAP operating income, it wouldn't be a lot higher than this figure. Therefore, it is priced at approximately 26x forward free cash flow.

It's hard to justify that paying 26x forward free cash flow for a business that is most likely growing in the mid-teens normalized growth rates is a bargain valuation.

On the other hand, given that Veeva has limited competition, aside from IQVIA, I believe it's reasonable to contend that Veeva has a substantial market share and will continue to control a large proportion of the pharmaceutical and biotechnology sector. Therefore, given its dominance over the sector, this provides Veeva with a moat around its business, so that paying what appears on the surface to be a stretched multiple, is actually a very fair multiple.

The Bottom Line

In conclusion, my perspective on Veeva Systems has undergone a notable evolution over the past few months. Initially adopting a neutral stance due to concerns about its valuation, I gradually shifted to a tepid bullish outlook as the fiscal year 2024, characterized as a transition year, neared its close.

Now, with the impending release of fiscal Q3 2024 results, I find the stock more attractive.

Despite acknowledging the headwinds that Veeva faces in navigating a challenging macro environment, including project scrutiny and a tough funding landscape for smaller companies, the company's strategic moves, such as the migration of existing customers to Vault CRM by 2025, present both opportunities and risks.

Moreover, in evaluating the stock's valuation at approximately 26x forward free cash flow, I recognize the seemingly stretched multiple. However, Veeva's dominant market position and substantial control in the pharmaceutical and biotechnology sector, justify this valuation as a fair reflection of its industry dominance.

For further details see:

Veeva Systems Q3 Preview: Navigating Challenges And Opportunities For F2025