VLDR - Velodyne: Slower Ramp Compared To Peers Keeps Me Underweight

Summary

- Velodyne’s internal management issues have derailed the development and pipeline development for the company.

- Velodyne’s broad portfolio has a differentiated position relative to competitors but is lagging behind peers in relation to automotive applications.

- There could be further share dilution in the future as the company may look to raise capital to secure the development pipeline while navigating the economic downturn.

- I keep a sell rating on the company’s share, with a preference for other companies in the space, such as LAZR and INVZ.

Thesis

I keep a sell rating on Velodyne ( VLDR ) as I believe there are better LiDAR players vying for market share in the space and VLDR would likely underperform in comparison to peers. I expect Velodyne's revenue ramp to be materially more modest than those of peer companies with greater relevance in the automotive LiDAR market, even though the company should benefit from greater visibility and stability in relation to revenues from broader industrial applications. With the company slated to turn profitable and generate cash flow only late in the decade, Velodyne will likely need to raise capital before then, diluting existing shareholders, or combining with another player.

Internal governance issues have derailed the development and pipeline development for the company

As a matter of background, the corporate governance issues as well as the conflicts between the previous management team and the Board has resulted in the significant derailment of the development process as well as the pipeline build opportunity with customers.

Recent changes driven by the challenges faced by the company include:

1) Founder David Hall being ousted, including mitigating his control over the development and technology pipeline.

2) Anand Gopalan resigning as CEO in mid-2021 after taking the company public through a SPAC.

3) Drew Hamer, CFO, transitioning away from the company in June 2022.

Pipeline update is suspended, but healthy non-automotive pipeline as of the last disclosure

Velodyne used to disclose its project pipeline, with a very high level of detail, like number of signed and awarded contracts and their order book contribution, and number and estimated order book contribution from contracts, that are in various stages of negotiation.

The second element of this disclosure, the contracts in negotiation phase, was very volatile, both in terms of potential order book contribution and the number of contracts, which confused investors regarding the company's future. Recently, the company stopped providing these disclosures and is looking to provide some other metrics to give investors a hint of what the future holds for the company without giving too many details that might be competitively sensitive.

However, as of the last update, Velodyne outlined a broad opportunity base in nonautomotive markets. As per the last disclosure on the Q3-2021 earnings call, Velodyne had signed 35 multi-year agreements and had increased the project pipeline to 220 projects, with 1/3 of the projects in the Industrial and Robotics market.

Automotive highway applications lagging behind peers

Velodyne's broad portfolio has a differentiated position relative to competitors but is lagging peers in relation to automotive applications, particularly as relates to highway autonomy.

Velodyne leverages a 905 nm laser, which, while cost-efficient, appears to lag behind the 1550 bn laser in relation to long-range detection and performs better in different weather conditions. The 905 nm laser and 905 nm-based LiDARs lead the industry in terms of cost, but the industry standard relative to performance for front-facing applications on vehicles travelling at higher speeds is being set by the capabilities of the 1550 nm laser. While I don't rule out wins for surround view applications in automotive, I think the high-margin front-facing applications in the automotive are less likely for Velodyne.

Amazon contract major pivotal win for new phase for the company

Velodyne is still trying to find its footing in the larger opportunity of the Auto market; however, in the meantime, its leadership in the broader industrial market applications is further accentuated by the contract signed with Amazon to enable delivery applications. While the contract itself does not assure any revenue unless Velodyne meets performance applications, and the use cases themselves have returns for Amazon as a customer, the decision by Amazon to choose Velodyne as the LiDAR supplier lends further credence to the performance superiority for broader industrial applications.

Financial outlook

Margin ramp through better cost structure

I am not optimistic about the revenue ramp for the company compared with peers, but the actions being pursued by the new management team make me optimistic due to a cost structure that is more right-sized for the modest revenue opportunity than it was before.

I see potential for margin expansion led by volume leverage and outsourcing manufacturing. I expect margins to increase beginning in due to 1) an expected increase in shipping volume during the next fiscal year, 2) moving all contract manufacturing from San Jose, California to Thailand, cutting labor and manufacturing costs in the process, and 3) transitioning all products onto MLA (micro LiDAR array) and ASIC (application-specific integrated circuit) technology.

At this time, I forecast limited software revenues for the company in the automotive market but could see potential upside to my gross margin forecasts were the company to be successful in driving customer adoption of software solutions.

{kind=link}

Earnings outlook: Profitability late in the decade

Forecast EPS profitability in 2027

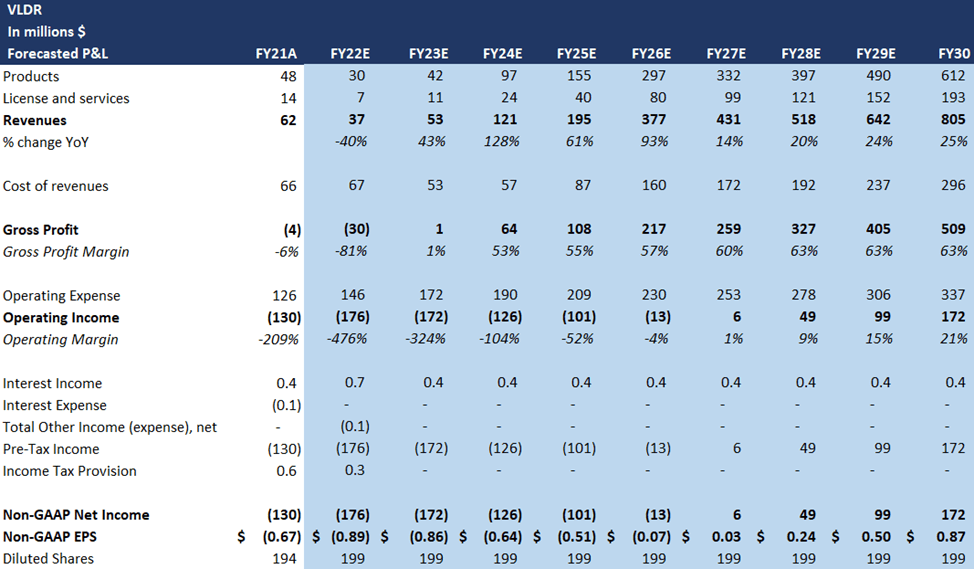

Velodyne is on track to record another year of losses on a per-share basis in 2022, much like most other LiDAR companies. However, with the modest revenue ramp towards 2030, I don't expect the company to reach profitability in relation to earnings per share until 2027, despite significant gross margin expansion as well as good cost control.

Earnings power of less than a dollar per share, with potential for further dilution

As shown in the image above, I forecast Velodyne to have earnings power of closer to $0.87 in 2030. However, I could see further dilution with the company ending the Sep-Q with $220 million of cash and cash equivalents on the balance sheet, as the company may look to raise capital to secure the development pipeline while navigating the economic downturn.

Risks

Acceleration of ADAS and AV adoption

While not the primary market for Velodyne at this time, Velodyne still derives a significant portion of revenues from automotive applications of LiDAR. I expect significant growth for LiDARs in ADAS and AV applications, but for limited share for Velodyne. Stronger-than-expected adoption from automotive OEMs and Teir-1s could drive upside to the industry and subsequently Velodyne.

Product portfolio has applications across broad industries and could be a relative outperformer if auto opportunities get pushed out

I expect a greater mix of Velodyne's revenues to come from non-automotive applications that range across a broad range of industries. The broad range of applications could allow for a quicker revenue ramp and a more stable pipeline of opportunities, and VLDR shares could end up being a relative outperformer if the opportunity in the auto industry gets pushed out in terms of timing.

Final thoughts

Velodyne is well positioned in the broader industrial markets with its technology, which should enable a steady ramp in revenue, but the challenges in meeting performance specifications of the automotive market will limit the Service Addressable market for the company and likely drive a more moderate growth ramp relative to peers through the end-of-the-decade. I expect Velodyne to be differentiated in relation to drivers of growth with a balance of revenue between Auto and non-Auto markets, at the behest of its leadership in market share in the broader industrial applications and a modest 1%-2% share of the automotive LiDAR market. Therefore, I keep a sell rating on the company's share with a preference for other companies in the space such as Luminar Technologies, Inc. ( LAZR ) and Innoviz Technologies Ltd. ( INVZ ).

For further details see:

Velodyne: Slower Ramp Compared To Peers Keeps Me Underweight