VEOEY - Veolia: A Stock You Should Definitely Consider But Close To 'Hold'

2023-07-25 10:50:48 ET

Summary

- The article discusses the potential of investing in water and environmental companies, using French firm Veolia as an example.

- I believe that investing in this undervalued stock could yield market-outperforming returns.

- Veolia is highlighted as a profitable operator of crucial infrastructure and contracts, making it an attractive investment opportunity, and I view it as a "buy".

Dear readers/followers,

In this article, I'll once again show you and remind you of the French company Veolia ( VEOEY ). Investing in water and environmental - not ESG, environment - companies is something I believe everyone should be considering at this time. The amount of value in these sorts of stocks that could be unlocked if invested in at undervaluation is immense. It is, in fact, market-outperforming.

As "proof of concept", I give you my original Veolia investment, which despite not being done at the "trough" of the company, nonetheless has seen rates of return that more than double the S&P 500 if we include the dividend payouts we've seen since.

Seeking Alpha Veolia RoR (Seeking Alpha)

So, yes. Veolia is a great business. It's a profitable operator of infrastructure and contracts that is not only important but crucial to a society. Exactly the sort of investments I typically look at.

So, let's see what we have going for us here and update my Veolia thesis for you.

Veolia Environment - Further Upside in French Water/Environment

It's a pretty simple company - at least if you look at the basics. 170 years of history and former part of Vivendi, and it focuses on managing what has traditionally been part of governmental responsibilities , but since has become privatized. With over €20B in market cap, despite its sheer size in Europe, it's really only a small-time player in what is a global demand for water, waste, and ancillary services. These are global markets that are herculean in their size.

Furthermore, the company is the only global player in Hazardous waste. It's not a "clean" thing to be in, but it's a very profitable thing to be in.

Veolia IR (Veolia IR)

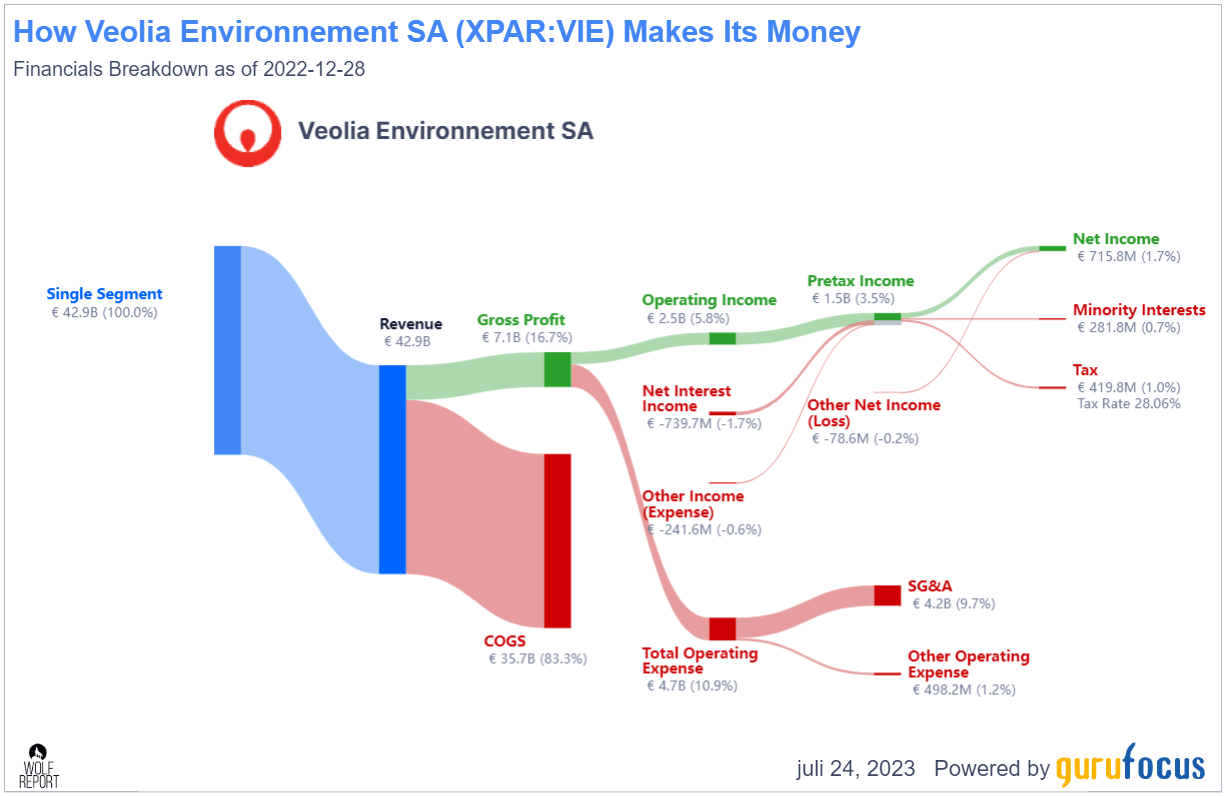

Profitable to the tune of around 16.66% gross margin, and around 5-8% operating margin. it's not the most profitable company out there, but it has been improving its margins over time - and what we want to look at here is scale, which Veolia certainly has. The company, in terms of profitability, has a "COGS problem". By that, I mean that over 83% of the company's revenues from its single operating segment (it doesn't split it as such - many French businesses do not actually disclose single-segment specifics) are going to COGS. This is the primary risk and issue that I would say this company has.

{kind=link}

This slim profit margin after all means that if the company has debt - which it does - and if there is an inflationary component or cyclicality to any of its work - which again, there is - then the potential for Veolia to go net-profit negative is not an unrealistic prospect. Not if things turn sour.

On the other hand, the company has scale and power in a segment that not many other players venture into. And insofar as its profit goes, all we need to do to make sure we're doing it "right", is not to enter the company at too high a price. We want a discount, in layman's terms. And since 2022, we've been able to get that discount pretty easily, which is why I've been investing in the business.

However, there's no doubt that you want to be somewhat careful with a company with this low degree of profitability and a very small amount of stockholder equity - because of what frankly is available on the market otherwise.

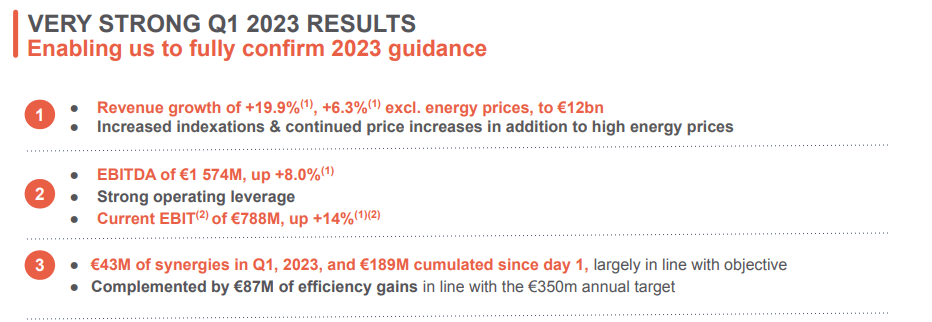

The company's start to 2023 has been a strong one - and I don't expect the next quarter to be any sort of massive downturn either. Veolia saw organic EBITDA growth of 8%, a solid merger with Suez that has delivered on strong, near-€200M in synergies already, with another €280M targeted for the remainder of 2023.

The company has had little issue coping with both inflation and cost increases, reporting extreme resilience to macro with strong operating leverage - which I believe because I've worked in public procurement and I know the nature and specifics of contracts signed and how these companies tend to work.

The company fully confirmed 2023E guidance - another positive.

{kind=link}

This also includes a solid reduction in net debt, due to high control despite volatility and seasonality in the company's working capital. These increases came from across the business, including growth in Water, Waste, and Energy, up almost 10% and down to 6% respectively. 1Q23 current EBIT is up 14%.

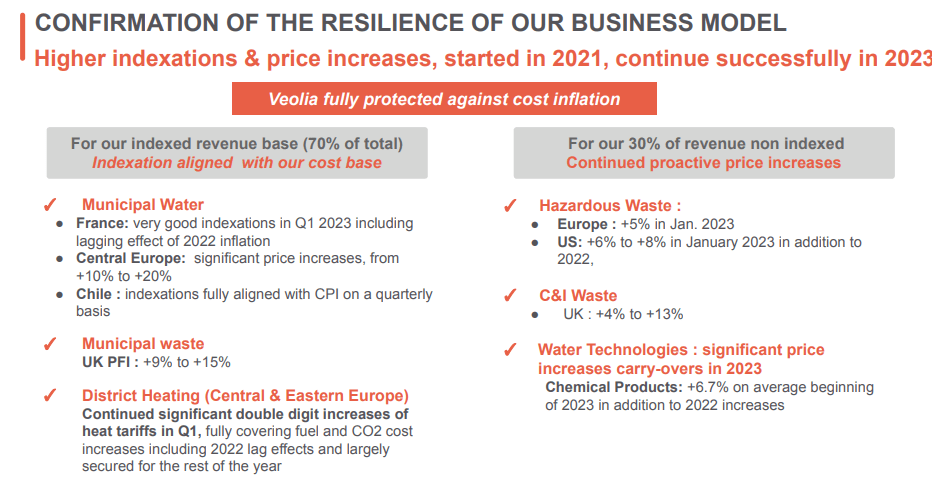

70% of the company's revenue base is completely indexed, including the overall lagging effects of the 2022 inflation. Overall, wherever the company is active, we can see solid increases in pricing which mean that overall, the company's sensitivity and exposure to these negative inflation and cost trends are extremely low.

{kind=link}

And the company also continues to "win" contracts here. Veolia is slated to operate the largest Energy from-waste facility in Europe, located in Turkey, turning 1.1M tons of waste to treatment per year, another 1.5M tons of CO2 emissions are reduced, notable through the production of 560,000 MWh of electricity per year, which is the equivalent of 1.4M inhabitants in the nearby metropolis. Biogas capture as well as other projects in Biomass are also gaining traction. Depollution assets and projects are won - Veolia recently won a new integrated waste management contract in Australia, as well as a 10-year contract with a €700M backlog in Lille Water.

Given the company's lack of data when it comes to specific incomes and cost trends, we can only get a limited view of where the company is saving money, and where it is costing more. What can be said is that most of the savings we've seen have come from operational efficiency, as expected - and about half of them are within Europe.

I would also state without a doubt, that Veolia continues to be in an attractive position for growth here, and in a good place to deliver very strong earnings growth irrespective of the macro development from here on out.

1Q23 confirmed this for me - and I expect 2Q23 to be no different given how insulated the company's revenues are from inflation and cost increases. While the company will probably stay at those low net margin numbers, which don't allow for much dividend growth either, it's still a very resilient, "basic" business in what sort of needs it addresses.

It has a strong balance sheet with below a 3.5x leverage, with its self-financing model providing ample headroom against issues. There is significant growth potential, and this is including the 85% macro immunity here.

The company fully expects continue strong earnings as well as some dividend growth here on a forward basis - and that this will continue regardless of this aforementioned macro.

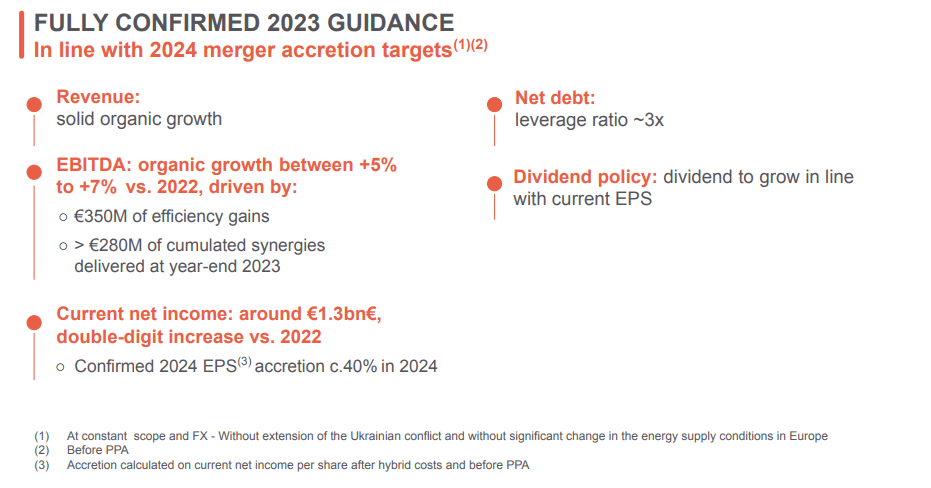

Aside from its 2023, the company also has the 2024 merger accretion targets, and for the time being, these are actually being realized.

{kind=link}

Overall, my level of worry for Veolia is about zero. The company trades on Paris under the native ticker VIE and currently has an in-context modest yield of 3.77%. This was pretty good when I started writing about the company, but in this context, this environment has grown lackluster.

What hasn't grown lackluster is the relative upside that the stock has based on continued growth. I also hasten to remind you that Veolia is BBB rated, and is expected to grow no less than 15%+ per year until 2023.

So let's look at what we have here.

Veolia Valuation - Plenty to like, despite 30%+ RoR.

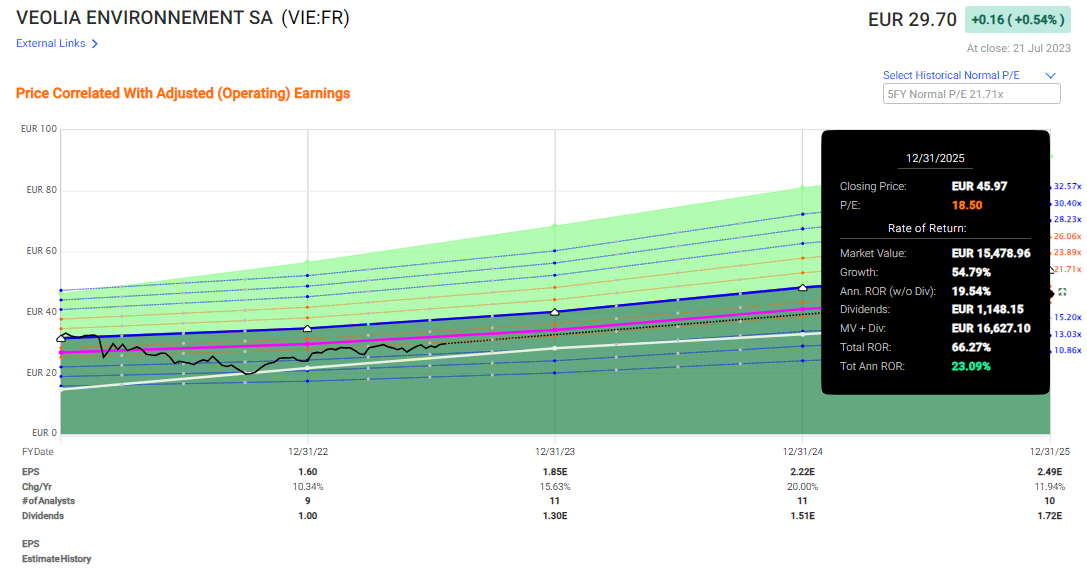

Veolia is no longer what I would consider "cheap". It was cheap when I started writing about it - so if you bought it below €20/share, you have my congratulations here. Still, there is an upside to be had for Veolia investors even here at this stage. The company is currently being traded at a blended P/E of 17x. This is high, but given the growth prospects of nearly 16% per year, this is not outsized in any way.

The upside even just to a straight 18.5x, which if those growth prospects would materialize would be the least I would expect with that yield, is over 20% per year here.

{kind=link}

There is some uncertainty as to the exact size of this RoR, given an analyst miss ratio of about 50% on a 1-year basis with a MoE of about 10%. So you should definitely be more cautious here. The upside for Veolia at around €30/share is far less than it was at €20 or €25/share. However, my previous PT for the company was €35/share - and as of this article, I'm neither bumping this nor reducing it. My price targets take into consideration a pretty far-reaching set of potentials, and I don't see anything that would change my estimates here.

Price targets other than mine for the company are as follows. 13 analysts following the business give Veolia a somewhat lower target than mine, at an average PT of €33.6. That's an upside of about 13% at today's price, and that's from a range of €25 to €43.4/share. I view €42+ as somewhat exuberant, even with this growth rate, and €25 as far too cheap, given everything we know of the company. Out of those 13 analysts, 10 are at either a " buy " or an "outperform" rating, which gives credence to my own positive rating on the business here.

I continue to see Veolia as a very solid investment here at this juncture - with an upside potential that is definitely enough to justify both interest and investment here.

I continue to be " long " the company here, and I may add shares going forward.

Thesis

- Veolia is a great business in several great fields. They have some excellent moats, a solid history, and good future prospects. The SUEZ M&A only strengthened the company's next few years.

- There are downsides and risks, of course. But these, at this valuation, are relatively small. A company such as this, with these sorts of operations, at this sort of price, is exactly the sort of investment you may want to make.

- This upside can even go up to 25-30% if we allow for a premium valuation or even higher, historically-accurate EPS growth. The message I want to send to you when you look at Veolia is that this is an undervalued water/waste/energy company.

- My official PT is €35/share, and I'm at a " buy ".

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I just can't call Veolia "Cheap" any longer - aside from this, it fulfills every single upside I look for, and because of this, I see it as an extremely solid play here.

For further details see:

Veolia: A Stock You Should Definitely Consider, But Close To 'Hold'