XLV - Vera: Disappointing Data From Phase 2 ORIGIN Trial Initiating Coverage With A Sell Rating

Summary

- Vera’s phase 2b ORIGIN data was underwhelming with lower than expected proteinuria reduction ~31% even at 9 months.

- We believe Atacicept’s commercial opportunity in IgAN is questionable due to the high degree of competition from KDNY, Otsuka, and Remegen.

- VERA plans to start a pivotal ph3 IgAN study by 2023; we do not believe things will change with a larger phase 3 trial.

- Lupus Nephritis may be an opportunity, but the clinical catalyst is expected at least 1-2 years later making VERA uninventable at this point in time.

- VERA's current valuation is around US 250M and holds 114M cash. we think the cash runway should not be a problem.

Background

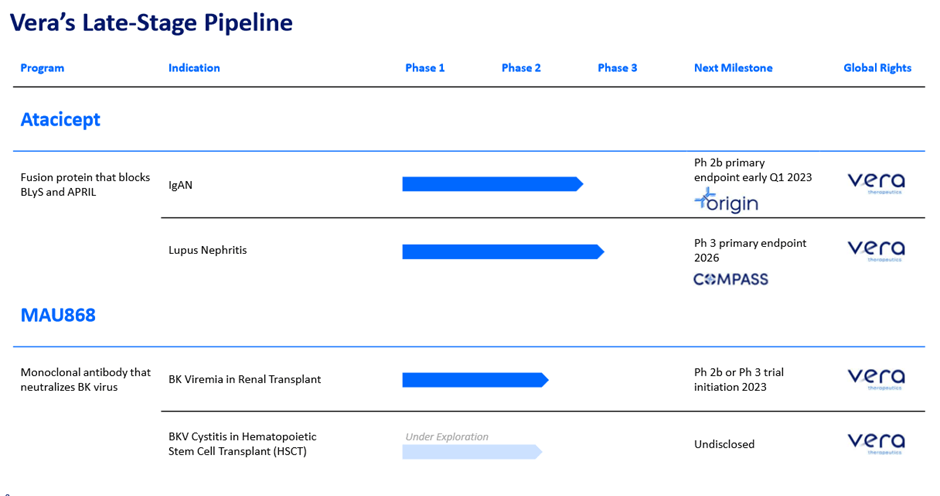

Vera therapeutics is a US small-cap biotechnology company developing an antibody for several kidney-related disorders. According to the company's IR deck , The lead candidate is atacicept, which is a fusion protein that blocks BlyS and APRIL pathways currently being studied in IgAN and Lupus nephritis.

VERA pipeline (Company source) VERA pipeline (Company)

{kind=link}

According to the company's description, Atacicept is a full human fusion protein, TACI receptor fused to a slightly modified Fc portion of human IgG1. According to the literature , the mechanism of action and thesis around Atacicept revolves around the hypothesis that blocking both APRIL and BLyS leads to a greater degree of efficacy because dual blocking could reduce long-lived plasma cells (BLyS), in addition to blocking B cells (APRIL). This leads to a greater degree of reduction in autoantibody production. BlyS (BAFF) and APRIL are produced by a variety of cells including monocytes, dendritic cells, and T cells, and they help to regulate B cell maturation, function, and survival.

By blocking APRIL and BlyS, you can theoretically reduce the following downstream effects:

- TACI receptor: involved in T-cell independent antibody responses and B cell regulation, class switch recombination

- BCMA: involved in plasma cell survival

- BlyS-R: immature B cell survival and maturation

Recent literature suggests that memory B cells provide a quick antibody response, and plasma cells produce antibodies and maintain the autoimmunity and inflammatory process. Short-lived plasma cells produce antibodies and long-lived plasma cells arise from B-cell differentiation in a secondary immune response, live in bone marrow or inflamed tissues, and produce antibodies independently of antigen stimulation by helper T cells and memory B cells, leading to chronic autoimmunity. This may be the reason why these long-lived plasma cells are resistant to steroids, immunosuppressive therapies, and B cell depletion therapies (i.e., rituximab) as they are independent of helper T cells and memory B cells. These long-lived autoreactive plasma cells maintain autoimmunity and lead to aggravation and reactivation of autoimmune diseases. As such, blocking them provides a solid mechanism of action for treating IgA nephropathy or Lupus Nephritis. However, we are unsure whether the dual blockade would increase the speed of action or if it would just help with the long-term durable response. There is a wealth of evidence that blocking BLyS alone works in SLE and LN, but the reason why the company is combining BLyS with APRIL is that they hypothesized that mono-blocking of BLyS alone may not be potent enough for IgAN.

Pre-clinical rationale is summarized below:

- BLyS Overexpression Leads to Kidney IgA Deposits and Nephritis in Animal Model: BLyS transgenic nephritic mice show mesangial IgA deposition, high circulating levels of aberrantly glycosylated polymeric IgA1 and nephropathy with age.

- BLyS Levels are Elevated in IgAN Patients and are Associated with Disease Severity: i) BLyS serum and renal levels are elevated in IgAN patients, and ii) BLyS plasma levels are increased with increasing glomerular pathological score and are correlated with proteinuria. Source: Company IR deck

{kind=link}

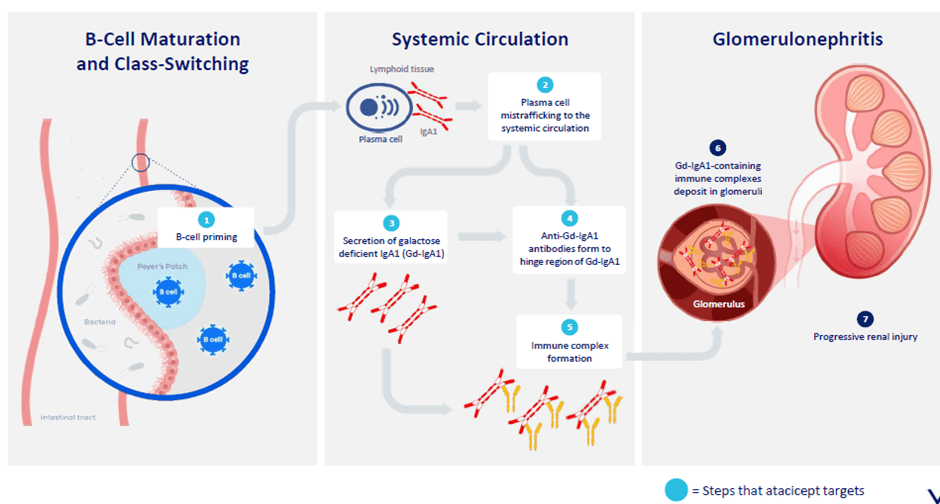

IgA Nephropathy pathophysiology, anti-APRIL/BlyS pathway turns off the “core cause” of the disease

IgAN disease starts with a high degree of B-cell production in the payer’s patch area leading to an increase in IgA1 production mistrafficked into the systemic circulation. This further leads to an increase in galactose deficient IgA (Gd-IgA1) and Anti-Gd-IgA1 antibody production formed to the hinge region of Gd-IgA1. Once Gd-IgA1 are deposited in the glomeruli, Gd IgA1 containing immune complexes stimulate local production of cytokines such as IL-6 and TGF-Beta; these cytokines promote inflammatory response through recruiting leukocytes and lead to glomerular and tubulointerstitial fibrosis. Furthermore, this glomerular inflammation is further enhanced by the complement system.

Once the kidney’s function declines to a certain point , the liver fails to perform its tasks properly leading to end-stage renal disease that needs life-long dialysis (for life). As such, the importance of slowing down the progression becomes extremely important in IgA nephropathy.

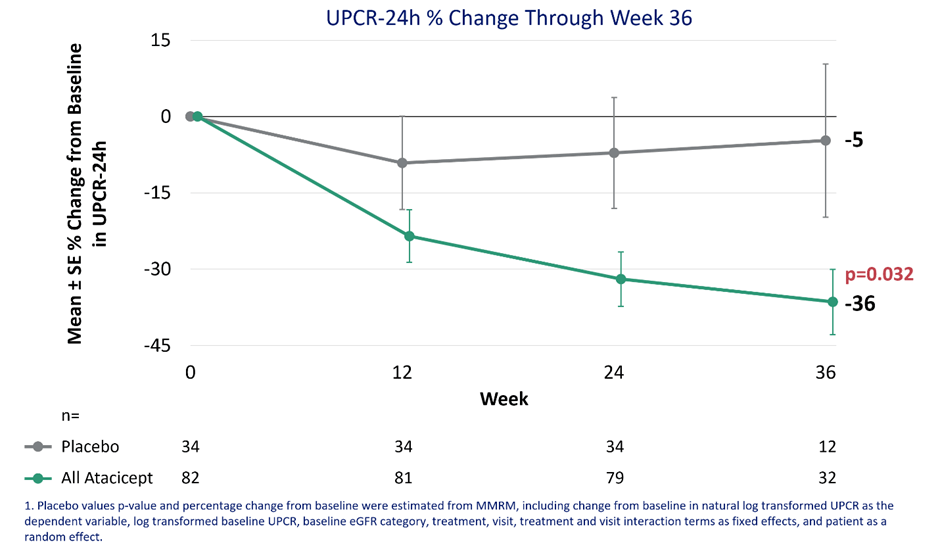

Phase 2b ORIGIN data was underwhelming even at a 9-month timeframe

The company released disappointing phase 2b ORIGIN 9-month data on Jan 3 rd, 2023, which makes VERA uninvestable at this current moment. Our thesis is explained in detail below.

UPCR proteinuria change over 36 weeks (Company)

{kind=link}

We believe the key bar for success for ORIGIN was to cross proteinuria reduction >40% (placebo adjusted) to stand out amongst other B-cell modulating therapies which showed 30-50% placebo-adjusted proteinuria reduction. However, VERA’s Atacicept only showed around -31% which is underwhelming further making atacicept’s positioning in IgAN questionable. Furthermore, it is important to note that Atacicept’s onset of action seems fairly slow; with additional 12 weeks of treatment (even with a high dose 150mg arm), additional proteinuria achieved at week 36 was only -6% additional UPCR reduction, this can be a significant disadvantage of atacicept moving forward.

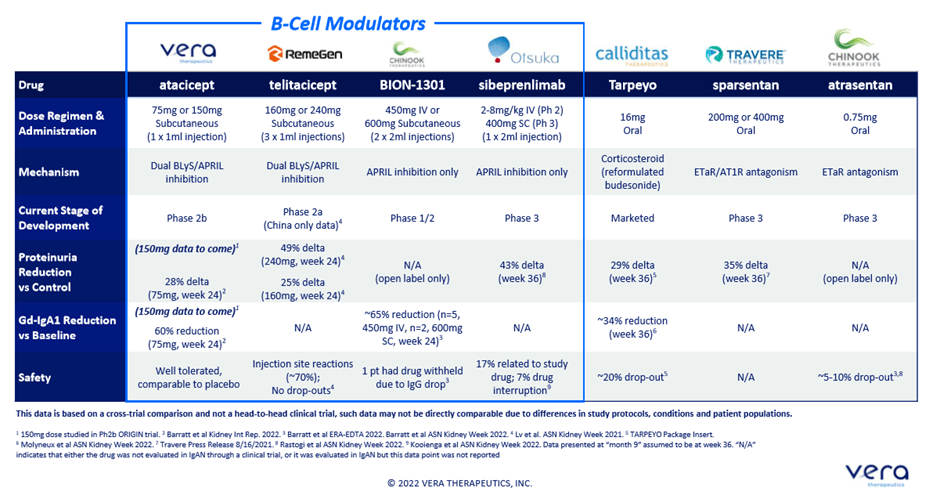

Competitive landscape (Company)

{kind=link}

Considering the fact that Atacicept is a dual BLyS/APRIL inhibitor, we believe it should provide significantly better efficacy (proteinuria above anti-APRIL) and a comparable or slightly worse safety profile for its commercial success. Otherwise, prescribers may choose to just go with an anti-APRIL as not blocking BLys pathway comes with lower i) CVD and ii) infection risk, as we have seen with Sibeprenlimab’s clinical trial. The study design of the ORIGIN study is adequately powered, 80% powered to detect a 28% difference in UPCR, which can be used as a basis for accelerated approval.

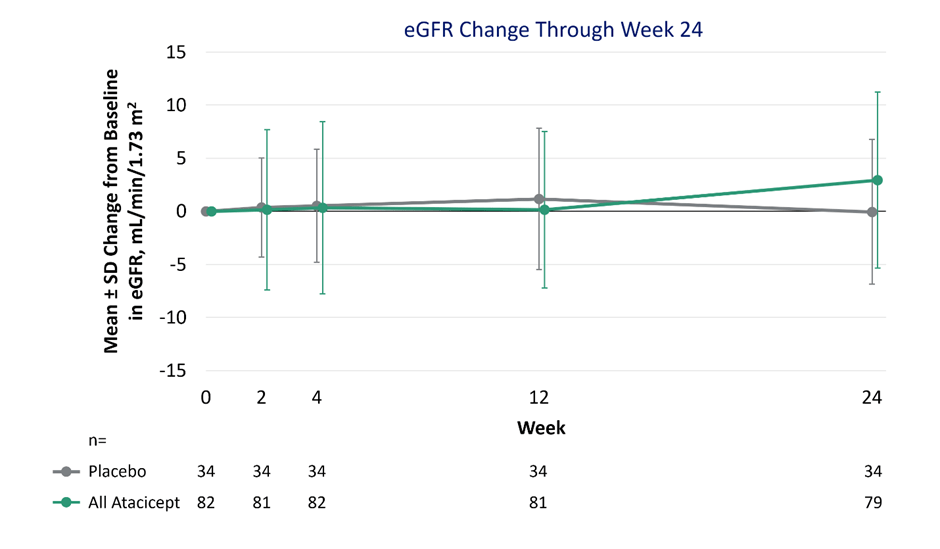

Robust eGFR stabilization shown

eGFR is the gold standard endpoint that FDA would need to confirm before approving through an accelerated pathway. As expected with the B-cell modulation mechanism of action, robust eGFR stabilization (and a slight increase) was observed; however, we believe 9 months is too short of showing enough separation. The eGFR remained stable in the placebo arm and clear separation (to the under 0 portion) was not observed. Furthermore, we note the company has not provided a dose breakdown and its impact on eGFR which will be key to understanding the dose response. We note that questionable dose response was shown during the phase 2a JANUS trial where 75mg arm’s proteinuria increased after around 20 weeks of therapy, driven by few outliers, but a clear dose-response was demonstrated during the eGFR portion so ORIGIN's eGFR data seems surprising.

eGFR Change over time (Company)

{kind=link}

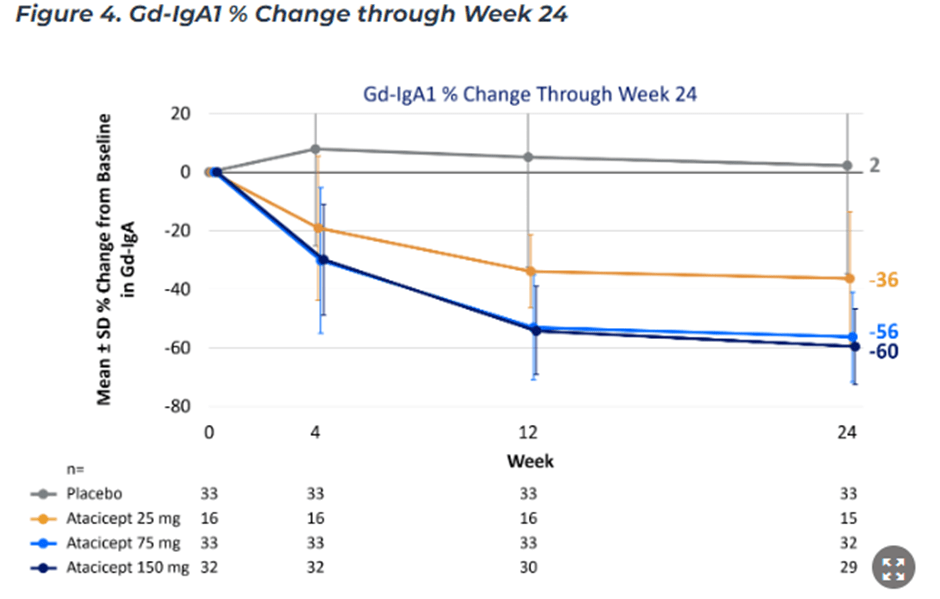

No clear dose response in Gd-IgA1; this may mean that there is a ceiling effect in the anti-April/BlyS class

As shown below, no clear separation between the 75mg and 150mg arms was shown in terms of reduction in Gd-IgA1. This is concerning as Gd-IgA1 has a good pre-clinical rationale as a biomarker to estimate the progression of IgAN’s disease (proteinuria and time to end-stage renal disease). No meaningful difference between the 75mg and 150mg arm may indicate that there is a ceiling effect or point of saturation and additional clinical benefit may not be possible by giving patients higher doses.

Dose response not shown (Company)

{kind=link}

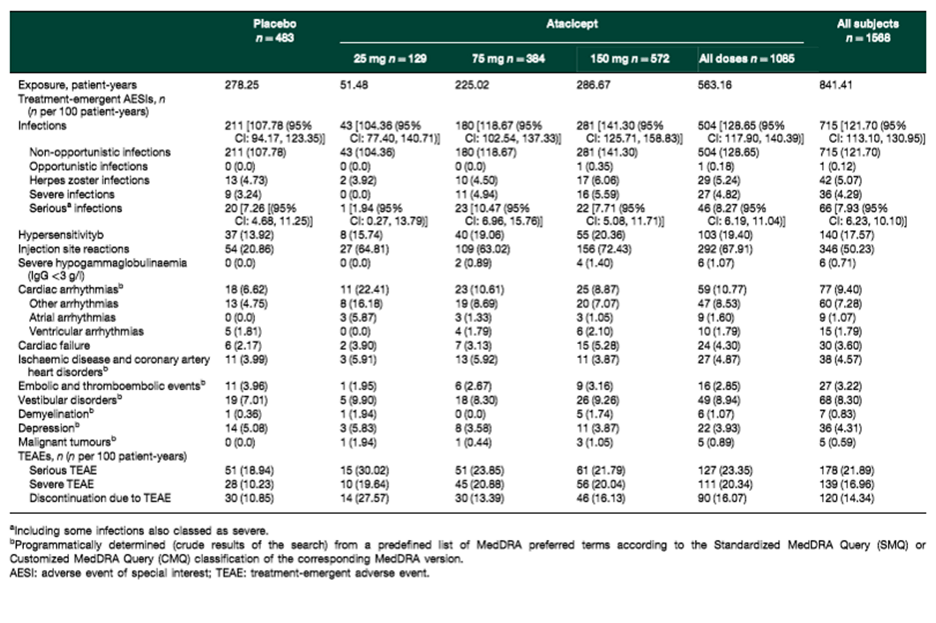

Safety seems robust, but the safety overhang remains

The data showed that the safety was robust aligning with the previously observed clinical profile. There were lower serious adverse events in the atacicept arm compared to the placebo arm, 2% vs. 9% (PBO arm). The biggest concern amongst investors was potential infection risk, which wasn’t shown during the trial likely due to exclusion criteria filtering out patient subgroups with high infection risk. However, the safety overhang around cardiovascular side-effect, infection, and malignancy (less likely based on meta-analysis) remains.

Meta Analysis of Atacicept (doi:10.1093/rap/rkz021)

{kind=link}

Approval is still a probability, but the commercial potential seems unattractive

The key question is whether the drug can be approved based on this data and what would be the commercial potential of Atacicept in IgAn. We believe approval is a possibility as atacicept has fulfilled i) robust proteinuria benefit within 9 months of treatment (barely passing >30% reduction which we think is the bar for the FDA), ii) eGFR stabilization confirmed the proteinuria reduction, and iii) a fairly robust safety profile was shown. However, we believe the market for B-cell modulation therapy is getting crowded with two other Anti-APRIL/BlyS competitors (Telitacicept, ALPN-303 (ALPN)) and Anti-APRIL monotherapies such as Chinook’s ( KDNY ) BION-1301 and sibeprenlimab showing superior proteinuria reduction over atacicept. Net net, we expect that the peak sale could be significantly lower than what the market and the management hoped previously.

Risks

Clinical risk and commercial risk remain as Vera is still pre-commercial biotech without an approved drug candidate. Even with approval, self-commercialization comes with a great degree of commercial risk as first-time launchers historically underdeliver vs. big pharma companies with robust commercial infrastructures. Financing risk as Vera is still not cashflow positive; they will have to rely on external financing. We find risk-reward not attractive enough to enter even after the market sell-off that we have seen during the last few days.

In conclusion

We remain on the sideline based on disappointing IgAN data which may have killed Vera’s IgAN franchise (but we expect minimal readthrough on its Lupus pipeline). We find IgAN a very interesting therapeutic area to follow during 2023 due to many clinical catalysts from Travere ( TVTX ), Otsuka (Sibeprenliamb additional phase 2 data), Narsoplimab ( OMER ) phase 3 9-month data, and Chinook’s ( KDNY ) phase 3 6-month data on its ERA Atrasentan. We look forward to reading the full data publication of the phase 2b ORIGIN as baseline characteristics of the population may have influenced VERA’s underwhelming proteinuria data; until more clarity is provided by the company, we remain on the sidelines.

For further details see:

Vera: Disappointing Data From Phase 2 ORIGIN Trial, Initiating Coverage With A Sell Rating