DNNGY - Vestas: Future Potential Current Struggle

2023-10-30 12:40:05 ET

Summary

- The wind energy market has promising future potential but is suffering from many challenges lately.

- Vestas is the worldwide market leader in wind turbines but is also going through volatile times, like many other wind energy companies.

- Their peer Siemens Energy even engaged in talks with the German government for a rescue plan of €15B, after quality issues with their products this summer.

- Vestas' margins have been negatively affected by supply chain issues, interest rates, competition and more.

Vestas Wind Systems A/S ( VWDRY ) is the world market leader in wind turbine production. Just like many renewable energy companies, it is going through some dynamic times. In this article, I will briefly outline the challenges for the wind energy business, but also look at its future potential. After this, I will go over Vestas' business segments and how these segments combine into the total picture of a dynamic company. I hope that after reading this article, you have a better understanding of risks, opportunities and the current state of Vestas.

Brief introduction

Renewable energy stocks have gone through quite some struggle lately, which has been somewhat different per sector. In the case of solar energy, this has been impacted by the quick rise of interest rates, leading to hampering demand by consumers. In wind energy sales happen in a different way, so interest rates have impacted it in different ways. Problems for wind already started long before rising interest rates, probably just after the COVID crisis in 2020. After this crisis, the sourcing of supply chains became a huge problem, exacerbated by events such as the Suez blockage. Also, as demand for metals used in wind turbines such as steel, aluminum and copper exploded, so did their prices, which more than doubled between 2020 and 2022. This led to financial trouble for wind projects, which are often sold using tenders with fixed prices. Like most industries, the wind energy sector will also likely suffer because of the higher interest rates and inflation.

For example, in a much-discussed attempt to lower their losses, wind project developer Ørsted A/S ( DNNGY ) recently tried to persuade New York to use higher rates on wind projects in the state to correct for some of the effects of inflation from which the company is suffering. This attempt did not succeed , which caused no relief in the sector.

Especially offshore wind, where much of the future growth of the wind industry is expected to be, needs to cope with many problems. While the industry is dealing with headwinds caused by inflation and rising interest rates, the endeavor of starting up a whole new business in the US is proving to be quite an undertaking .

Vestas

Vestas Wind Systems, being the largest wind turbine company in the world, is of course not immune to these problems. This is reflected in the financial results of the company, recording negative annual EBITDA for the first time since more than 10 years.

As you can see in the graph above, the most recent quarterly EBITDA looks a bit less dramatic, but we cannot draw any real conclusions from this yet. Vestas' quarterly results have always been fluctuating heavily in the past, since the wind energy business can be quite lumpy with regard to earnings.

In June this year, Vestas' peer Siemens Gamesa (which has become a part of Siemens Energy AG ( SMNEY )) announced quality issues in some of their wind turbines, which knocked off more than half a billion from their 2023 Q1 operating profits. This announcement made their shares drop quickly. Until now, at Vestas no comparable issues have been discovered, but the news from Siemens Gamesa made it clear that quality issues can have a large impact on the bottom line of wind energy companies.

Just recently, the problems at Siemens Energy seem to have become much worse after the company is seeking guarantees from the German government. These developments did not lead to a shock among the peers of Siemens Energy, in fact shares of Vestas sharply rose on the same day after Siemens Energy's announcement. Still, this situation is illustrative of how fragile business models in the wind industry can be if something goes wrong. Vestas itself already went bankrupt in 1986, and went through an ugly major restructuring in 2012 after its shares had already dropped by more than 90% in 2 years' time.

So the wind technology sector is anything but a boring industry. For investors, that's not always good news. Unlike many other sectors, it has to deal with on the one hand political and economic forces influencing it, and on the other hand quickly changing technological development, as wind turbines are getting larger and more advanced, because size can be beneficial for efficiency. Did you know the hub of the Vestas V162 is actually as high as the Washington Monument?

{kind=link}

The V162 had its first commercial sale lately for a new project in northern Germany, so wind turbines have come a long way since the picturesque windmills which were used for milling, sawing or pumping in medieval European villages. Also, offshore wind turbines are a whole new area of technology, where one needs to take account of sea currents, more difficult servicing and more extreme weather.

It is not my intention to take a deep dive into the velocity at which innovation of wind turbines is leaping forward, I only wanted to give a brief impression about the R&D efforts which are continuously demanded in this industry.

Continuous struggles

Because of the continuous innovation occurring on the technological side, there's always a risk of falling behind for wind turbine manufacturers. Even for the largest manufacturers like Vestas, this makes it imperative to not rest on its laurels but continue to invest in R&D as to not lose its market leadership.

At the same time, wind turbine manufacturers need to be able to compete with each other on the cost side, since new projects are most often sourced using tenders. I wrote about the tender structure of wind projects before and how it is beneficial for keeping costs under control for governments but it creates risks for companies like Vestas. Margins can sometimes end up being razor-thin if competition is strong.

The supply chain has proved to be another potential source for struggle lately. In March 2021, the Suez Canal blockage already led to sourcing problems for Vestas, and later these problems were continued by rising demand for raw materials and rising costs.

Meanwhile, wind turbine manufacturers mostly depend on (local) governments for their sales: new wind projects need to be planned, paid for and commissioned by public agents. These can depend on potentially volatile political situations and economic environments. Policy usually has a shelf life of one or maybe a couple of election cycles, which increases uncertainty for companies like Vestas.

So, with large continuing R&D expenses, strong competition on the cost side, supply chain problems and dependency on political and economic environments, it's no wonder that Vestas' margin often seems to be under pressure. Still, there's one part of the company which seems less affected by many of these factors: the service segment. But more about this later, let us first look at the reason why you would even bother to consider investing in a company like Vestas: the future.

Future potential

The previous paragraph which lists the struggles might suggest that investing in the wind industry is very hazardous. Well, as we have seen last week with Siemens Energy, it can be dangerous. But it could also be very worthwhile, simply because of its growth potential.

The growth of demand for renewable energy is not likely to stop any time soon. While effects of climate change are getting more and more clear around the world, energy independence has become a more central aim of many legislations lately. The war in Ukraine underscored the importance of this, and renewable energy will often play a large role in independence.

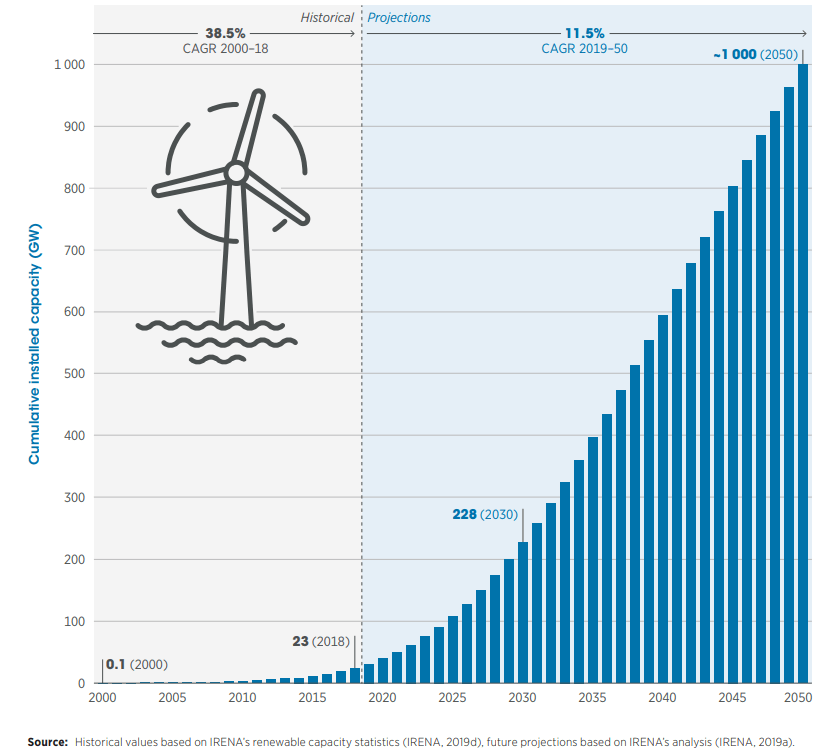

The main part of growth of wind energy is likely to come from offshore installations. A graph below from the International Renewable Energy Agency (IRENA) shows the possible growth of offshore wind installed capacity. This graph was made in 2019, so it is already quite dated, but it still serves as a nice confirmation of future potential. Figures in their 2022 report about renewable energy capacity statistics show a growth in offshore wind from 35 to 56 MW installed capacity between 2020 and 2021. This even surpasses projections in the graph below.

Future of Offshore Wind Installed Capacity (IRENA)

{kind=link}

Offshore wind energy production is still dwarfed by onshore at this moment, the production of which was 769MW in 2021 worldwide. Onshore wind energy also still shows some very healthy growth, and its future potential for the bottom line of Vestas should not be underestimated. But offshore has some benefits which onshore does not have: stronger winds, turbines can be built higher, and the sea still has much more available space. And as a bonus, there's much less NIMBY there.

New technologies, like floating offshore wind can prove to be strong contributors in the growth of this sector, as the following graph illustrates, taken from a report by Ørsted on how to scale floating offshore wind:

Potential future growth of floating offshore wind (Ørsted report)

Please note that floating offshore wind is not only a potential future technology, but it is already being developed. After some delays, Vestas secured an order for a floating wind farm in France already last year, which is expected to be commissioned in mid-2024.

Vestas' cash cow: service

I already mentioned this before, but Vestas does not only produce wind turbines, it also services them. The servicing segment is a part of the company which has some very different characteristics and could act as an 'anchor' in bad times, reducing the risk of investing in the company. Wind turbines simply need periodic service, since otherwise they risk being switched off for longer time periods due to defects. And missing days, weeks or even months of electricity production can be very pricey for operators. For Vestas, servicing is a very dependable and profitable income stream. Let me explain this by showing you some data:

In their latest financial report of Q2 2023 , Vestas reported a stellar growth of their service segment of 29.1% year-on-year. As can also be seen in the graph from Vestas Q2 2023 financial report, margins in this service segment are also relatively healthy (especially considering margins in Vestas' power solutions segments have been negative).

Vestas service revenue and EBIT margin (Vestas Q2 2023 financial report) Vestas power solutions revenue and EBIT margin (Vestas Q2 2023 financial report)

Vestas' revenue stream from service amounted to 26% of their quarterly revenue in Q2 2023, which is already a quite sizeable share.

Their expected contractual service revenue backlog amounts to $31.6B, a year-on-year increase of $2.6B. Vestas' service backlog is higher than their wind turbine backlog ($20.0B), but it is likely to be very dependent on the wind turbine business.

As Vestas grows its service activities, which have a stable and positive margin, this will improve the financial stability of the company and reduce the risk of the more volatile and fluctuating financial results of the power solutions segment.

Scale advantages

Being the market leader in wind turbines, Vestas does have some benefits compared with their competitors, including:

- The company has more possibilities for increasing the robustness of its supply chain.

- Production can be streamlined more easily when you're producing more wind turbines of a specific type.

- Thanks to its size, Vestas will have easier access to debt and is less likely to experience large-scale financing problems even in this high-rate environment.

- Vestas' service segment is already contributing in a major way to the bottom line of the company. The scale of the company has positive effects for the service segment, since finished projects of the power solutions department of the company are likely to be new projects for the service department. This reduces the risk of the more volatile power solutions segment of Vestas.

Upcoming earnings

In their Q3 financial results, which will be released on the 8th of November , we might be able to see a glance of whether we can expect recovery or more hard times for Vestas. I believe it is unlikely their earnings will look good, but I am especially interested in the margins of their different segments: has their service margin stayed on track and has their power solutions margin not deteriorated further? Also, the guidance of Vestas would give some more clarity about whether we can expect a bad 2024 or some recovery.

I have been an investor in Vestas since years, but it is hard to pinpoint a fair value for the shares at this moment. I am aware I gave the stock a buy rating at much higher prices 2 years ago, but currently I am rating the company as a hold. Given the current environment and the struggles in the renewable energy segment it seems fair that Vestas' share trades for a strong discount compared with a couple of years ago. And frankly their latest earnings do not give enough confidence to expect much higher share prices on a short-term basis in my view.

In the long term, however, I believe in the potential of Vestas to profit from the long-term growth of wind energy. Growth cannot compensate for everything, but most of the struggles the company is facing can be overcome in the longer term. Interest rates and supply chains will eventually likely calm down, continuous R&D becomes more and more baked into their DNA but will be less volatile, and geopolitical developments are pointing into a direction of more energy independence. But it will take time.

As Vestas itself stated in their outlook for 2023 :

Our industry needs structural change to increase profitability, especially within the wind turbine segment. The structural changes primarily entail strengthening the commercial discipline in customer dialogues, lowering the frequency of new technology introductions as well as maturing the assessment of risk.

Conclusion

Ever since the first decade of the 2000s I have been following the wind industry quite closely. As long as I remember, there seems to have been a strange mix of large future potential coupled with current-day problems. Most people agree that wind energy (especially offshore) has a bright future. But even during the years in which Vestas' financial performance looked good, the company always seemed to have large future potential which could be attained as long as some short-term problems could be fixed. It might be that this is usual in nascent technologies such as the wind sector, but it feels as if the wind technology sector has been stuck in this phase for a long time. For Vestas to be attractive to long-term investors, two questions are of utmost importance:

- Will the margins for Vestas be large enough, given all the potential struggles? The company is targeting a 10% EBIT margin in 2025, I believe achieving this would be a good start.

- Will Vestas be able to combine new technology development with earnings growth?

As I tried to outline in this article, I believe the answer to both of these questions will eventually be a yes, but for the coming years, the same mantra remains: Future potential, current struggle.

For further details see:

Vestas: Future Potential, Current Struggle