DBOEY - VGI Partners Investor Letter - Full Year 2022

Summary

- VGI Partners Global Investments Limited is an Australia-based investment company. The Company’s Investment Strategy is to create a concentrated Portfolio, predominantly comprised of Long and Short Positions in global listed securities, actively managed with a focus on capital preservation.

- The letter provides details on the performance of VG1 for the twelve months ended 12/31/22.

- The letter also provides commentary on current positioning.

- We reflect on a number of the missteps made during 2022, and the important lessons we have taken away from this in order to improve our processes over the years ahead.

“Every recession brings out the sceptics who doubt that we will ever come out of it, and who predict that we will soon fall into a depression, when new cars will sit unsold in the showrooms forever and houses will stand empty, and the country will go bankrupt.”

PETER LYNCH

Dear Fellow Investors,

For the twelve months ended 31 December 2022 (CY22), VGI Partners Global Investments Limited (ASX:VG1) generated a net return of -22.3%. [1]

Global equity markets experienced a challenging year in 2022, the S&P 500 declining -19% over the period, the NASDAQ Composite retreating -33% and the broader MSCI World Index falling -19%. Few asset classes delivered a positive return for the year, as heightened inflationary pressures, rising global interest rates and a horrific conflict on the European continent saw over US$25 trillion in value erased from global equity markets over the course of the calendar year.

CY22 has been incredibly disappointing for VGI Partners. Since the inception of VG1’s portfolio in 2017, we have strived to provide our investors with access to a concentrated portfolio of high-quality businesses, with the ambition to grow our capital at 10-15% per annum. The careful protection of our invested capital base and constant vigilance in avoiding situations that lead to the permanent impairment of capital has been a critical component to this approach. Quite simply, we have not adequately executed on this in 2022.

As a consequence, CY22 comfortably represents the largest annual drawdown the global strategy has experienced in a calendar year since its inception. We are profoundly aware that this has been a disappointing result, and one that we have obviously sought to learn extensively from as we look to restore both our return profile and our investors’ confidence over the period ahead.

Pleasingly, the new year has started well, with the portfolio up +11% through to the 27 th of January. However, we recognise that this is only a first step in recovering the CY22 drawdown for our investors.

In this letter, we provide an update on the current positioning of the VG1 portfolio, a summary of recent changes and an overview of where we see opportunities to generate attractive returns on our capital over the 2023 year ahead. Additionally, we feel it important to reflect on a number of the missteps made during 2022, and the important lessons we have taken away from this in order to improve our processes over the years ahead.

Before discussing the portfolio in more detail, we would also like to provide an update on recent corporate activities of relevance to VG1. As many investors would be aware, VGI Partners and Regal Funds Management merged on 3 June 2022, with the new combined entity renamed ‘Regal Partners’. The VGI Partners investment team continues to manage the VG1 portfolio, but is benefiting from access to Regal Funds Management’s operating infrastructure and investor relations team. Key VGI Partners investment staff continue to own substantial personal investments in VGI’s wholesale funds and VG1. The VG1 Board has also taken a number of steps to assist VG1 and its shareholders. This includes a refinement of the dividend policy in August 2022 – VG1’s new policy is to target a dividend of at least 4.5c each six months. This is in line with VG1’s recent profile, with VG1 paying two dividends during CY22 (4.5c in April 2022 and 4.5c in September 2022). In addition, VG1 has an active on-market share buy-back program, purchasing shares when they are trading at a discount to Net Tangible Assets. This not only provides greater on-market liquidity but can be highly accretive for shareholders. Over 56m shares, or approximately 14% of VG1’s shares, have been bought back since the program began. Post completion of the merger in early June 2022, we have seen VG1’s discount to Net Tangible Assets reduce from over 20% to around 15-16% currently. We look forward to providing more updates through future investor briefings and letters.

Portfolio Thoughts & Positioning

We have always viewed the opportunity to manage our investors’ capital as a privilege, and we thank investors for their patience, support and encouragement over what has undoubtedly been a difficult year. While performance has been challenging, we remain highly confident that the deep fundamental investment approach taken by the VGI team, and our focus on identifying mispriced high-quality businesses, remains an attractive way to generate favourable risk-adjusted returns through the full market cycle. The team retains a high level of conviction in our core portfolio holdings, and pleasingly has taken advantage of share price weakness in a number of existing portfolio positions to progressively add exposure to incredibly high-quality businesses at what we perceive to be very attractive valuations. At writing, in the long portfolio we see, conservatively, about 30% potential upside to our estimate of fair value for the underlying stocks.

As a reminder, VGI Partners seeks to build a concentrated portfolio for VG1 of under-appreciated, highquality businesses that operate within (or we believe will soon operate within) attractive industry verticals. These positions are offset by short positions in companies perceived to be encountering structural headwinds, business model weakness and/or accounting irregularities.

While the concept of investing in ‘quality’ businesses has evolved in recent years to encompass an increasingly broad church, at VGI Partners, our preferred approach is to focus on businesses that we perceive as ‘covertly’ high-quality businesses, namely those which are initially ignored, under-appreciated, or disdained by the broader market consensus, and therefore tend to provide far more attractive opportunities from a valuation perspective versus more traditional (or ‘overtly’) higher-quality names. Of course, the drawback from owning covert high-quality businesses, at least initially, is that such holdings can make you stand out from the crowd, at times can make you look foolish, and can sporadically inject higher levels of volatility into a portfolio as the underlying value of these businesses is progressively appreciated by the broader market.

In uncovering these covertly high-quality businesses, we look for companies that enjoy strong moats that protect the underlying business, and ideally moats that are expanding (or, at a minimum, remaining stable). We like businesses with the ability to allocate capital at attractive rates of return (that is, rates well in excess of the businesses’ own cost of capital), those with a resilient business model or underlying customer base and those that enjoy growth optionality. Additionally, we spend significant time seeking to understand the underlying industry structures in which our companies operate, given our preference for investing in businesses with the ability to generate sustained economic profits, and not just accounting profits [2] .

While covertly high-quality businesses are our preference, we are equally happy to deploy capital into more overtly, or already well-appreciated, businesses during times when either depressed sentiment across the broader market provides us with an attractive opportunity to do so, or when one of these businesses experiences shorter-term setbacks in their business model or growth profile, leading to their share prices over-correcting to the downside, at least over the short term.

The table below provides a snapshot of the top 10 holdings in VG1’s portfolio as at 31 December 2022 and represents a collection of what we believe to be high-quality, attractively-priced, global businesses with significant potential to meaningfully grow their earnings over many years ahead. Consistent with our concentrated approach, the top 10 long positions account for 68% of our total invested capital.

| Top 10 Long Investments as at 31 December 2022 |

| % of Portfolio |

| CME Group Inc. ( CME ) |

| 12% |

| Amazon.com Inc. ( AMZN ) |

| 12% |

| Deutsche Börse AG ( DBOEF ) |

| 7% |

| Cie Financière Richemont SA |

| 7% |

| SAP SE ( SAP ) |

| 7% |

| Pinterest Inc. ( PINS ) |

| 5% |

| Française des Jeux ( LFDJF ) |

| 5% |

| Mastercard Inc. ( MA ) |

| 5% |

| The Walt Disney Co. ( DIS ) |

| 4% |

| Rheinmetall AG ( RNMBF ) |

| 4% |

| Source: VGI Partners analysis. |

Regular readers of our monthly reports will recognise a number of our existing longer-term positions in the above, in addition to more recent changes to the overall portfolio composition. US-listed derivatives and futures exchange operator CME Group was our largest investment position, closely followed by US technology and e-commerce conglomerate Amazon (an investment we first initiated in VGI’s global strategy in 2014). Both positions are discussed in more detail later in this letter. As a consequence of updated information and adjustments to our assessment of risk-reward, previously larger positions in multinational payments business Mastercard and Swiss-headquartered luxury watch and jewellery retailer Cie Financière Richemont have been reduced, while the portfolio has exited its position in Japanese-listed optical and precision technology manufacturer Olympus Corp. ( OCPNF )

More recent additions to the portfolio include German automotive and defence supplier Rheinmetall, US listed oil services business Schlumberger ( SLB ), and diversified global entertainment group The Walt Disney Company. In the case of Disney, we saw an opportunity to invest in a more overtly high-quality business that has encountered a series of short-term setbacks. We feel this has provided us with a highly attractive entry price for a business that is a global leader in theme parks, hotels and cruise lines, operating with a well-established and growing competitive moat, and that has consistently delivered high returns on invested capital. Amazon arguably feels like it is also rapidly falling into this category, as the broader market’s disdain for the company’s core cloud infrastructure and e-commerce businesses grows, despite strong underlying fundamentals. We will discuss the investment thesis and upside potential from both these positions in greater detail later in this letter.

By some margin, the greatest detractor to VG1’s portfolio returns was the rotation away from high-growth and tech-oriented businesses. The portfolio had high exposure to this thematic via holdings such as Amazon, Pinterest, Qualtrics ( XM ) and IAC , as well as the gradual re-purchase in the first half of 2022 of holdings in Spotify ( SPOT ) and Palantir ( PLTR ). These left the portfolio vulnerable as valuations compressed and investors rotated aggressively into more defensive and/or profitable businesses. In hindsight, the portfolio was over-exposed to these higher-growth and still maturing companies. However, as we have discussed before, we think many of these businesses will start to generate substantial profitability and free cashflows over the next few years (in fact, many of them already are) and still strongly believe in the underlying businesses mentioned above.

In terms of FX, the portfolio remains fully hedged to Australia Dollars ((aud)). As we take an active view on the currency, we may move back to an unhedged or partially hedged position, but only when we believe there is a clear mispricing based on our fundamental analysis. Currently, we remain positive on the AUD because of the favourable position Australia finds itself in: endowed with plenty of commodities at a time when demand for these is growing rapidly given the global undersupply and underinvestment in commodity production experienced in recent years.

Short Selling

Our short portfolio was a positive contributor to returns in CY22, adding ~10% to portfolio returns. After an exceptionally challenging few years for short selling strategies, the abrupt conclusion of the cheap money era has rapidly refocused market participants toward company fundamentals and valuations and, in doing so, significantly widened the opportunity set for short sellers. The portfolio currently retains a higher short exposure than historically as a result, reflecting the increasingly attractive environment (particularly in more cyclical industries where we anticipate significant risks to earnings and margins over the period ahead).

The largest short contributor in CY22 was a custom basket of higher-multiple, loss-making technology stocks – a position that we discussed in our semi-annual letter in July 2022. This basket consisted of businesses that carried, in our view, significantly challenged business models and lofty valuations, many of which subsequently experienced share price declines of 50-80% over the course of the year. While a successful outcome, we regret not leaning into this position in greater size. A secondary contributor to the short book was a basket of stocks focused on companies in the semiconductor sector, which we initiated in anticipation of the market eventually recognising that the sector is ultimately a cyclical industry and recent increases in capacity would lead to negative consequences for the industry. Again, this position was discussed in more detail in our letter of July 2022.

Pleasingly, the portfolio also benefited this year from a number of single-stock shorts, including a position in Tesla ( TSLA ), the well-known electric vehicle manufacturer that was experiencing a slowing in business momentum throughout the year as a result of pressures on consumer discretionary purchases, supply chain disruptions and increasing competition. We have expected for some time that the electric vehicle category would become more competitive, and more recently have begun to witness aggressive price cuts by manufacturers in an attempt to clear inventory, which is a negative trend for an industry that is only likely to see more competition over the coming years. The portfolio also benefited from a short position in a US-listed discount grocery store business, where investors were being pitched a large-scale store rollout story by senior management, albeit using forecasts that were extrapolating the temporarily favourable conditions into the long term and at a time when insider selling was rapidly accelerating. Both these short positions have now been profitably closed.

Finally, our proprietary screens, which focus on identifying accounting red flags, have also displayed greater efficacy over the year, identifying a number of situations where weak cash conversion or evidence of inventory building have subsequently led to earnings downgrades and share price declines. This has been particularly prominent in the retail sector, where growing inventory problems have led to discounting and, in turn, margin compression. Additional focus has also been placed on the small pockets of the global economy that are still normalising post COVID-19, and where supply chain disruptions and/or volatility of input prices continue to create unsustainably high pricing increases, which, in some cases, are being assumed by the broader market as the ‘new normal’.

Opportunities

While technology has obviously been a key detractor from returns in CY22, we continue to believe the sector provides a number of compelling opportunities to buy excellent businesses with the ability to generate meaningful returns on capital over the years ahead. Enterprise software, for example, continues to remain a key focus for the team, given these businesses often display highly attractive economics, including predictable and recurring revenue streams, high levels of customer ‘stickiness’ (often due to the mission-critical nature of their use case) and long runways for growth in markets with low overall penetration.

The broader malaise across the listed technology sector through 2022 drove a significant de-rating of valuations across the enterprise software sector, which has subsequently ignited a wave of merger and acquisitions (M&A) announcements through the second half of the year. The rapid emergence of M&A activity from large tech-orientated private equity firms in the listed sector (which typically seek to purchase businesses in the private markets prior to their underlying value being realised by public market investors) would likely suggest that private market valuations for quality, growing enterprise software businesses are, in many cases, now 75% to 100% above public market valuations, a sign that the capitulation in public markets has reached peak levels.

On the completely opposite end of the spectrum from enterprise software, the defence sector is another area we have recently found equally appealing. We see structural growth after years of under-investment and the Ukraine conflict has acted as a massive catalyst for defence budget acceleration, particularly in Europe. Meanwhile, the Taiwan/China stand-off is accelerating the spend in the Asian region. Western armies are short on ammunition and other ordnances; for instance, Germany requires 10 years of ammunition purchases to simply meet minimum NATO requirements. This is one of the many reasons we have started building a position in Rheinmetall, a leading German defence business, which we discuss later in the letter. The shift to digital capabilities by military departments also bodes well for one of our other holdings, Palantir, whose core business revolves around supplying software solutions to Western government agencies and the military globally.

Similar to enterprise software, we have seen acquisitions in the defence sector at significant premiums to public market valuations – one such example was Maxar Technologies ( MAXR ), which received a private equity takeover proposal in December 2022 at a 129% premium to the last traded price. Again, this highlights the dislocation between public market prices and those that an informed, private buyer is prepared to pay given a 5-year view. We find this encouraging.

In addition to defence, we have focused our efforts on other new sectors where we see structural growth, including energy and medical technology. The long-term outlook for energy looks highly attractive given many years of under-investment and more recently amplified by ESG constraints and corporate discipline. Although we reviewed commodity owners (where we leveraged the expertise of the Regal resources team), we focused our efforts on the second derivative – the oil service companies. These are the picks-and shovels of the industry and arguably the highest-quality way to gain exposure. As a result, we invested in Schlumberger earlier this year and grew this to a circa 8% weight during the year (now circa 3%).

Similarly, medical technology has been an area of ongoing focus. Olympus was sold during the year after generating an attractive return (briefly discussed later in the letter). In turn, this has led us to other opportunities in the sector. We are in the process of building two holdings in medical technology – companies that operate in highly consolidated industry structures, are mission-critical to customers and are exposed to attractive long-term structural growth drivers. We will be discussing these in more detail in future communications.

Hidden Risks & Signposts

A large contributor to the significant drawdown in technology and growth stocks has been the growth in ‘cross-over’ funds over the last decade, particularly in the US. These funds (many of them household names in the growth hedge fund complex) have substantially grown their assets and, in turn, their allocations to completely illiquid Venture Capital ((VC)) investments. The rising interest rate environment and subsequent reassessment of growth asset valuations forced the ‘cross-over’ funds to cover redemptions by selling their listed investments. We believe that a number of the names in the VG1 portfolio have been caught up in this downdraft over the last 12 months. We are mindful that a further leg down in growth valuations could be led by a re-pricing of the illiquid VC investments within these portfolios. Whilst this has been a well-publicised dynamic, private equity funds may prove to be a hidden risk in the system.

In fact, warning signs are developing in what is a completely unregulated segment of the financial markets with substantial amounts of hidden leverage and opaqueness. Private equity firms have been slow to take downward re-valuations. We see potential that 2023 reveals an avalanche of redemptions as negative returns are revealed to investors in private market or cross-over funds (which hold public equities and unlisted assets) over the next 3-6 months, triggering gates reminiscent of the Global Financial Crisis. Asset-liability mismatches are starting to become apparent and the canary in the coal mine looks like the Blackstone ( BX ) B-REIT situation (where Blackstone began to limit redemptions from its real estate trust after withdrawal requests spiked). Property-skewed funds and cross-over funds seem to be the most vulnerable. At writing, additional warning signs have come to our attention and we believe the amber lights are flashing and potentially are about to turn red.

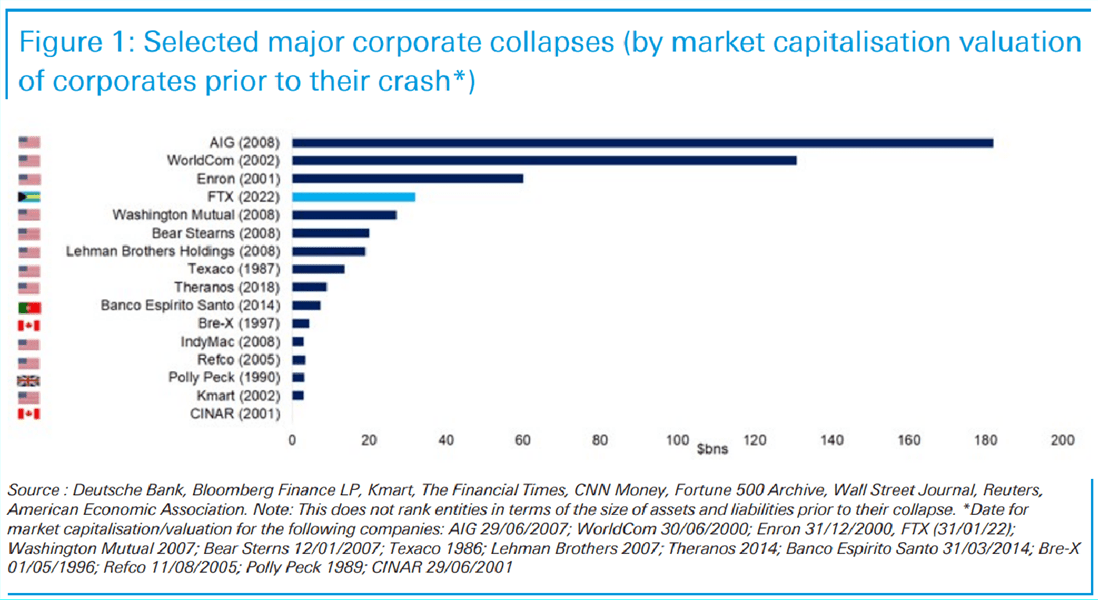

In meetings with investors over the last six months, we have said that the signposts that we are closer to an equity market bottom would include the reveal of a large fraud as well as a sell-off in Tesla, the retail investor poster-boy. We have seen the collapse of FTX, a large crypto company, and evidence that it is an outright fraud, along with a severe unwind in the Tesla share price (where we fortunately had a short position during CY22; since closed). Interestingly, FTX ranks as the fourth largest corporate failure in history by market cap. We are yet to see signs of outright capitulation and fear amongst investors, which will likely be the final stage, nor have we seen central banks globally meaningfully withdraw liquidity from the system.

{kind=link}

Pressures are also building for consumers globally. Looking at the US as an example, the household consumption picture prima facie remains healthy, but digging below the surface there are worrying signs. Inflationary pressures are squeezing consumer budgets and consumers have been forced to lean into excess savings or, even worse, take on credit card debt to fund consumption (US credit card debt is growing at the fastest pace in a decade, while the savings rate for US households is near all-time lows). Households are also facing pressure from the higher cost of debt, which is feeding through into collapsing demand for large-ticket items, such as new homes and new auto purchases. These are the largest assets for the average household, and both home and used car prices have been under severe pressure. Consumers are being hit from all sides but job losses have yet to become widespread. We are therefore keeping a close eye on the general consumer environment with all the pressures that are building.

Mistakes

We constantly assess and review our past investments, aiming to improve our decision-making going forward. For every investment, we like to conduct a pre-mortem review (to identify risks and how an investment can go wrong when we first make the investment) and then a post-mortem review to understand the extent to which our investment thesis did or did not play out after the fact, with an emphasis on identifying mistakes and learning from these. We think this is a critical process so that we can improve and avoid repeating errors going forward.

As previously highlighted, our high exposure to technology, high-growth oriented businesses drove the bulk of our underperformance in CY22. One key mistake we made was with Qualtrics ( XM ), which was the second largest detractor in the year. With the benefit of hindsight, we over-estimated the company’s growth profile and overpaid for the business. We assumed the category would be more resilient even in an environment where customers are scrutinising IT budgets and we failed to change our mind when growth began to disappoint. Our valuation approach was also overly reliant on long-term free cashflows – because we like to think about businesses with a long-term mindset – but we did not pay enough attention to near-term valuations and expectations. Lastly, we were insufficiently critical when XM announced a large acquisition at the peak of the software bubble in mid-2021, as this was a potential sign that the outlook for XM’s core business had deteriorated.

The big lesson that we draw from our XM investment is one of sizing – given the wide range of outcomes, this should have been reflected through a smaller-sized investment. We continue to own XM today as the valuation and expectations have been reset, and XM remains the undisputed leader in an emerging, mission-critical software category with a long growth runway. This view has been substantiated by our conversations with customers at the XM Innovation Sydney event in November 2022 and recent CIO surveys affirming XM’s pole position amongst emerging software vendors. In recent days, SAP have announced a strategic review of its XM stake, removing a key overhang for the stock and increasing the probability that XM will trade more in line with peers or be acquired.

IAC was another key detractor during the year, as we made the mistake of holding onto our investment for too long. A key part of our original IAC thesis was underpinned by a near-term catalyst in the form of an upcoming spin-off (Vimeo) providing a chance to crystallise value and for the business to narrow the discount to its sum-of-the-parts. While this thesis played out, we then held onto our IAC investment, thinking the business continued to trade at a meaningful discount to the value of the assets it owned. We failed to appreciate that IAC was entering a ‘re-build’ stage and, given the lack of upcoming spin-offs, would continue to trade at a deep discount to the value of its net assets.

In addition, IAC undertook a meaningful acquisition (Meredith), which is a business complementary to one of its existing assets (Dotdash). This increased IAC’s exposure to the advertising market (Dotdash & Meredith generate all revenues through advertising) at a time when the ad market was starting to slow. We made the mistake of not realising quickly enough that the integration of the two businesses was taking longer and facing some hiccups, which, in turn, caused management to delay its financial targets. One of IAC’s other businesses, Angi, similarly faced issues with its strategic direction, leading to management changes and the IAC CEO having to step in to turn around the business. Overall, a key mistake we made was failing to appreciate that investments relying on sum-of-the-parts valuations tend to perform poorly in weaker market conditions when investors demand a larger discount versus the net asset value – unless there is a clear path to unlock value (e.g. through a spin-off). We continue to own IAC as we believe that the management team are now addressing the recent issues appropriately and that their actions can assist with closing the large discount to net assets over time.

As we mentioned at the start, we have gone through an extensive process of scrutinising all of our key positions and re-underwriting assumptions. We feel excited about our current portfolio but acknowledge the need to remain mentally flexible to avoid mistakes and to change our mind quickly when we think our investment thesis is drifting.

Portfolio Update

Below we provide an update on some of our key holdings.

CME (~12% weighting)

CME is a business likely familiar to you, being one we have owned in our global strategy since 2008 and which was our largest VG1 position at the end of 2022.

CME operates futures and derivatives exchanges, including the Chicago Mercantile Exchange, the New York Mercantile Exchange, the Chicago Board of Trade, and the Dow Jones Index Services. On top of this, CME also owns other key assets related to foreign exchange trading & infrastructure and a strategic shareholding in Standard & Poor’s (S&P) Index business.

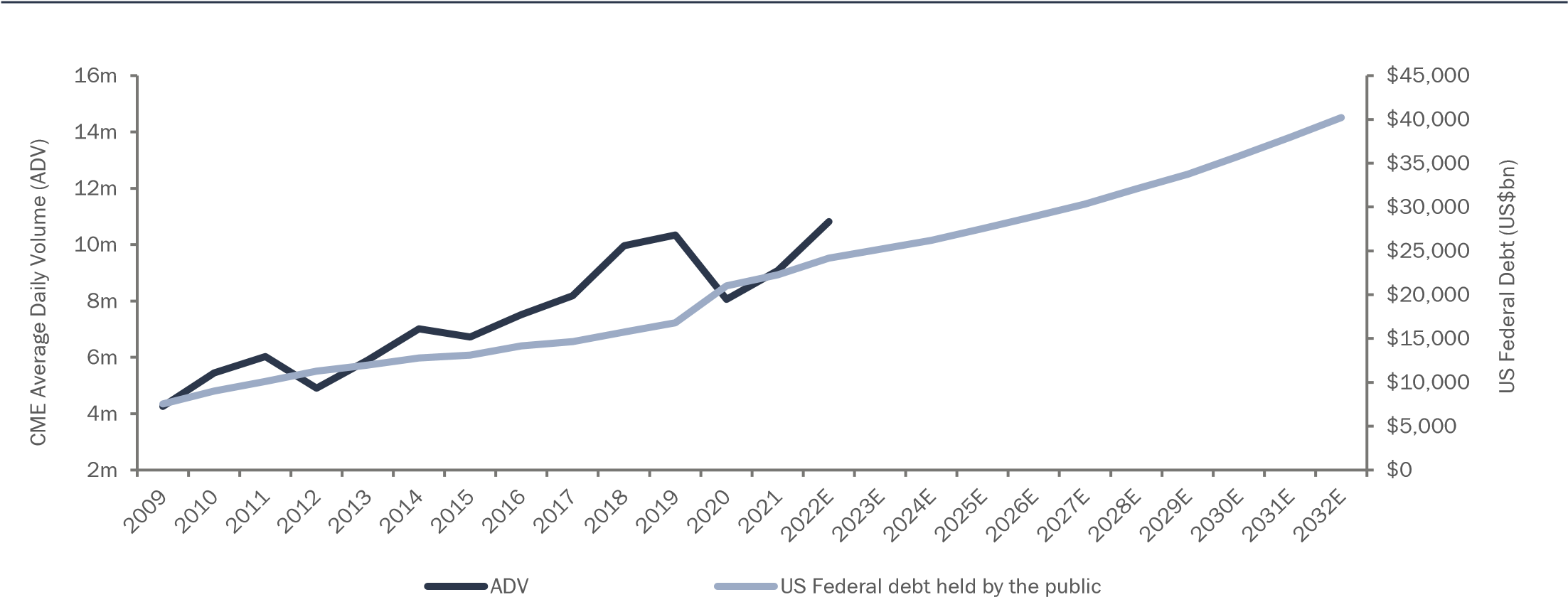

The key driver of trading activity for CME is in its interest rate derivatives products, where it has an effective monopoly in the exchange trading of interest rate derivatives in the United States, with benchmark products across the entirety of the interest rate curve. Demand for interest rate derivatives is driven by volatility in interest rate markets, whose effect is compounded by the number of bonds held by those looking to manage interest rate risk and, by extension, market liquidity. The below chart of average daily volumes of interest rate derivatives and US Federal debt held by the public illustrates the extremely strong relationship the size of the US Treasury market and volumes growth, although there are deviations around this primarily around Fed intervention (for example, at the start of the pandemic, volumes were suppressed by an enormous amount of Quantitative Easing (QE) and effectively zero interest rates which reduced the demand for hedging products). We expect the growth in the size of the US Treasury market, particularly in relation to privately held US treasuries as the Fed undergoes a balance sheet unwind, to remain a powerful underpinning of CME’s interest rate derivatives business.

Size of the US Federal Debt Held by the Public vs Average Daily Volume of CME Interest Rate Contracts

{kind=link}

As such, we are high conviction that the reversal of QE and the normalisation of bond market conditions will provide a significant tailwind for CME’s trading activity in the near term, while its net interest margin should benefit from greater investment income on margin collateral. Other derivatives complexes, including equity and energy, are likely to also benefit from a normalisation of market conditions and we note that incremental futures contracts generate an extremely high drop-through rate to cash earnings due to CME’s strong operating leverage as a primarily digital platform. As a result, we believe current conditions are highly favourable for CME’s interest rate derivatives business, other derivatives complexes and net interest margin and we see substantial upside risk to consensus earnings and free cashflow estimates.

At writing, CME is trading at a CY23 PE of 20x, free cashflow yield of 6% and dividend yield of 5%.

Amazon (~12% weighting)

Amazon is a dominant player in e-commerce (#1 globally), cloud computing (#1 globally), and digital advertising (#3 globally), all massive and structurally growing end markets. Amazon’s share price declined nearly 50% in calendar 2022 due to a myriad of macro and company-specific headwinds, including slowing economic growth, rising inflation, tighter monetary policy, and substantial overinvestment. Free cashflow turned deeply negative. We are disappointed, to say the least. Nevertheless, the investment case for Amazon today is remarkably compelling. Market expectations have been reset, the valuation is extremely attractive, and management is intent on improving profitability and reducing capital intensity. Amazon remains a high conviction holding and we are incredibly excited by its prospects.

For the past year, the market has been concerned about the growth and profit outlook for its e-commerce business, which is presently loss-making due to overinvestment and cost inflation. Management has responded by laying off more than 18,000 employees — the biggest reduction in Amazon’s history. Beyond the reduction in force, Amazon has frozen hiring in its e-commerce and corporate divisions, cancelled or delayed warehouse openings, raised prices on a variety of products (including Prime memberships), eliminated several unprofitable lines of business and seeded new ones (e.g. Buy with Prime) to fill excess capacity. (Amazon doubled the size of its e-commerce footprint over 2020-2021.) Buy with Prime has been shown to increase shopper conversion by 25% on average and is now widely available to US-based merchants.

Looking past the short-term headwinds, we are highly optimistic about the trajectory of the e-commerce business. Whilst logistics investments have led to short-term losses, they have strengthened the competitive moat of the e-commerce business and its ability to meet customer demand for years to come. E-commerce is a highly valuable business which has spawned the 3rd largest advertising business in the world (the best search results in the world for advertisers are those of Amazon customers) and a subscription business (Amazon Prime) which acts as a powerful flywheel to e-commerce and other business lines such as devices, streaming video/music and soon satellite broadband (via Amazon’s Kuiper business). We think the market is overly pessimistic about the prospects for e-commerce (inclusive of advertising) and underwrite scenarios where we estimate the e-commerce business alone is worth more than US$60 per share.

As we wrote last year, we reiterate our view that Amazon’s current share price is more than underpinned by its Amazon Web Services (AWS) business alone. Cloud computing remains in the early stages of growth, with customers across the industry only around 30% through the migration of their workloads from onpremise infrastructure to the cloud, based on commentary from industry experts, key corporates and Chief Technology Officers. Until recently, cloud spending has been largely resilient amidst macro headwinds. This changed last result when all three hyper-scalers warned of a slowdown in growth as enterprises scrutinise technology budgets. Indeed, Amazon is proactively working with its customers to cost-optimise, which will have a negative impact on short-term sales growth but is the prudent long-term business decision. As a result, we forecast AWS growth to slow further in 2023 before re-accelerating in 2024. The long-term revenue growth profile of AWS remains robust, and sustainable operating margins have the potential to exceed 40% given a concentrated industry structure, AWS scale advantages, and a mix shift toward value-added software.

As we look to the future, Amazon’s focus on improving operating efficiencies, reducing working capital, and lowering capital expenditures should result in an exponential increase in free cashflow and shareholder value. We forecast a return to positive free cashflow in 2023. By 2025, we expect free cashflow to exceed US$70 billion, representing a growing 8% free cashflow yield, which we consider incredibly attractive for an asset of this quality.

Deutsche Börse (~7% weighting)

On the back of recent purchases and relative share price performance, Deutsche Börse (DB1) has grown to the portfolio’s third largest position. DB1 is a well-diversified exchange group whose activities touch most aspects of European capital markets, offering a blend of transactional and non-transactional revenue exposure. It provides trading, clearing, pre/post-trading and data & analytic services in four key operating segments: Trading & Clearing, Fund Services, Security Services and Data & Analytics.

The transactional side of the business, like CME, has strong structural tailwinds as artificial depression of policy rates by central banks coupled with QE in the Eurozone begin to reverse and DB1’s Trading & Clearing businesses (including Europe’s largest derivatives exchange Eurex) benefit from a larger hedging market and continued macro volatility. Current uncertainty also benefits its EEX business (the dominant venue for power trading in Europe), which is poised to grow as tension in European energy markets, and the ongoing structural shift in electricity generation to renewables, continues to support trading activity. As per CME, DB1 operates a digital platform which enables an extremely high drop through to cash earnings from each incremental dollar of trading revenue.

On the other side, Clearstream is the keystone to DB1’s non-transactional revenue stream, with over US$13.5trn of securities in custody (including around 40% of Eurobonds in issue and 100% of all issued securities in Germany). Because of the size and stickiness of Eurobond custody assets, much of Clearstream’s revenue base is highly stable and the rising rate backdrop acts as a strong tailwind for net interest margin earnings (as greater collateral margin requirements, coupled with increased yields, produces powerful earnings potential for the group); this had previously been a source of downgrades during 2019-21. Moreover, we expect the acquisition of ISS within the Data & Analytics segment to drive long-term non-transactional revenues by expanding the scope and quality of DB1's ESG offering as demand for ESG products continues to accelerate.

Despite these strong tailwinds and solid execution over the last year, DB1 trades at a discount relative to peers and below our fair valuation. We view this as unjustified given the quality of earnings and organic growth potential. At writing, DB1 is trading on a CY23 free cashflow yield of 6%, PE of 16x and a dividend yield of 3%.

Richemont (~7% weighting)

Richemont is a position we have written extensively about since 2019. It remains a Top 10 holding and the business continued to perform strongly during 2022.

Demand for high-end luxury has proved sustainable thus far, as the top 1% of households by net worth continue to spend more on luxury items such as jewellery, watches and handbags. Richemont’s super luxury jewellery brands, Cartier and Van Cleef & Arpels, are the crown jewels of the group’s portfolio of brands; these account for the majority of Richemont’s profitability and, consistent with our investment thesis, have posted accelerating revenue growth in recent periods.

Geographically, the highlight has been Europe, where growth was led by strong local demand and the resumption of inbound tourism from the US and Middle East. Asia Pacific was weaker during 2022 because of the store closures in mainland China and Macau due to the enforcement of the zero-COVID policy in China. However, given China’s recent reopening under less stringent COVID policies, we expect Chinese demand to rebound and turn into a tailwind this year (note that this has already started to be reflected in expectations with a 17% re-rate over the last few weeks).

One of the reasons we have long admired and invested in super-luxury businesses is their pricing power. Higher prices add to the allure of luxury products while simultaneously creating exclusivity. Encouragingly, during 2022, Richemont raised prices on key brands such as Cartier and Van Cleef and across multiple geographies, a trend which we expect to continue going forward. Financially, price increases are highly attractive as the revenue delta drops straight through to the bottom line. This, alongside operating leverage, has allowed Richemont to expand margins.

During 2022, Richemont reached an agreement to sell its online operations, YNAP, to Farfetch, the leading luxury e-commerce retailer. The disposal of YNAP has been a key part of our CFR investment thesis, as we believed this was a distraction for management and masked underlying profitability. This has simplified the story for investors: the deal will allow Richemont to retain upside on the equity of both YNAP and Farfetch and allow management to focus wholly on running Richemont’s core business.

We have recently started to reduce our portfolio weighting in Richemont. The recent share price increase is reducing the risk-reward profile and we think this is the best of times for luxury goods companies.

SAP (~7% weighting)

SAP is in the midst of a multi-year transition of its business to the cloud which continues to gain momentum. We attribute much of its success – which has not been without challenges and setbacks – to the strategy initiated by Christian Klein after he became sole CEO in mid-2020, in particular “RISE with SAP.” Launched in January 2021, RISE is a commercial construct to migrate customers onto SAP cloud products such as S/4HANA Cloud (Cloud ERP) and SAP’s Business Technology Platform (BTP).

Late last year, we travelled to Germany and met with SAP management to learn more about BTP specifically. The platform offers data and application services which customers and partners can use to integrate SAP and non-SAP applications, in effect a “digital core” with powerful flywheel effects. It is foundational to SAP’s RISE offering with 80% of customers adopting the platform. The BTP business has a sales run rate exceeding €1.5 billion with high margins and we expect it to grow substantially over the next few years.

SAP’s cloud transition has resulted in some one-time and duplicative costs (infrastructure, R&D and sales), resulting in a circa €200 million lower operating profit in 2022 versus 2019, despite circa €3 billion higher sales. Having studied these transitions, we believe the shift is camouflaging the underlying earnings power of what will be higher quality earnings (>80% recurring revenue). We expect the one-time and duplicative costs will dissipate from 2023 onwards, resulting in positive operating leverage and sustainable double-digit operating profit growth.

Recent results from SAP have been mostly supportive of our thesis with leading indicators, specifically Current Cloud Backlog, accelerating despite macroeconomic uncertainties. The BTP flywheel has improved integration between SAP’s cloud modules (SuccessFactors, Concur, etc.) and S/4HANA, leading to improved cross-sell/upsell rates. Recent results from back-office software peers Oracle and Workday have also been resilient.

SAP’s moat is stable-to-growing and the business is well-positioned in many of the world’s largest corporations as an essential component of their IT operating platform. Our field trip to Germany gave us incremental confidence that the strategy is gaining traction following a painful period of transition. We also view the appointment of a new CFO, Dominik Asam, who joins in March from Airbus and has a solid reputation, as one of the many positive catalysts building in the business.

Given the cloud transition and some execution missteps, SAP trades at a meaningful discount to fair value. Earnings are poised to accelerate as they execute on the cloud transition. In our view, a more meaningful reflection of the company’s earnings power requires looking out to at least 2025, with SAP trading at a 6% free cashflow yield and a 15.5x PER on our forecasts.

New LONG Position: Walt Disney Co. (~4% weighting)

The Walt Disney Company is a diversified media conglomerate operating media networks, theme parks, film and TV studios and direct-to-consumer streaming services. It is the global leader in theme parks with hotels and cruise lines aimed at families. Key assets within Disney are the instantly recognisable entertainment franchises that have multiple avenues of monetisation such as Mickey Mouse, Star Wars, ABC and Marvel’s Avengers.

Disney’s share price declined due to a number of factors in 2022, presenting us the chance to purchase a long-admired business and its unique collection of valuable intellectual property assets at what we consider to be a very attractive valuation. Summarily, the EPS of Disney has declined from US$7 in 2018 to ~US$2.60 in 2022 but we believe that the earnings power of the assets has not diminished to anywhere near this extent.

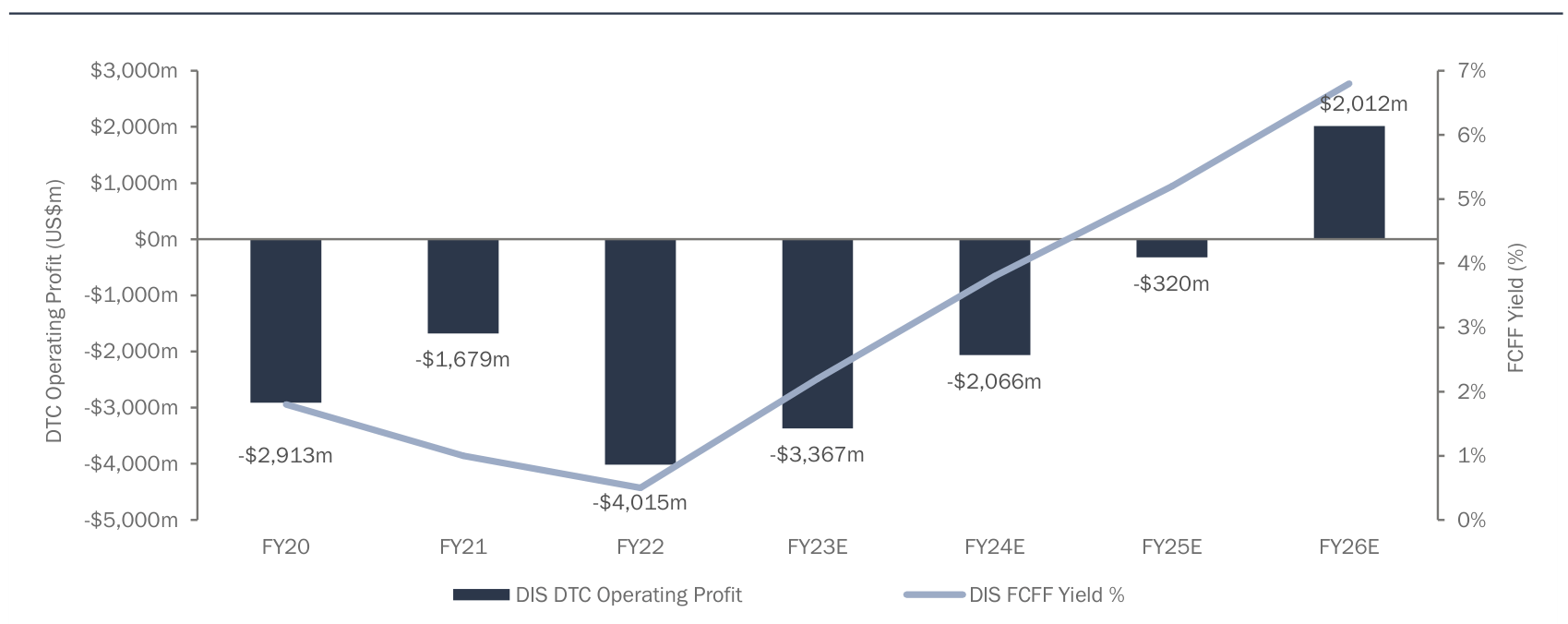

Disney is currently undergoing a business transition within the Media and Entertainment Distribution division (DMED) from traditional media property distribution via third parties (i.e. cinemas and broadcast networks) to a Direct-To-Consumer ( DTC ) model via the Disney+ streaming service. A key element of our thesis is that the earnings power of the company is currently being masked by the marketing and content investments within Disney+ and that this will normalise over the next several years. To put this in perspective, Disney+ (DTC sub-segment) currently generates operating losses of over US$3.3bn (a negative 14% operating margin) compared to operating margins at its nearest streaming competitor, Netflix, of +15.5%.

A secondary concern around Disney has been the CEO leadership transition from Bob Iger to Bob Chapek that occurred in February 2020. As well documented in the media, the changes that Bob Chapek made to the organisational structure of the business affecting the creative output at Disney did not resonate with senior executives nor investors and he was ultimately removed by the board. Hollywood loves a sequel – Bob Iger was sensationally reinstated to the CEO role in November of 2022. During his original tenure as CEO, Mr Iger was a well-respected leader, overseeing successful acquisitions of Pixar, Marvel Entertainment and Lucasfilm. We view the board actions as supportive of long-term shareholder value creation as Mr Iger seeks to unify the executive team and navigate the company through the current challenges.

The resilient cashflows of the Disney components have allowed it to invest heavily in the DTC content space and give the management team the necessary flexibility to prove out the earnings power of the business. In this context, it would be remiss of us to not discuss the Parks, Experiences and Products division ( PEP ) of Disney, which makes up 35% of revenue and 49% of operating profits (ex DTC losses) but has been overlooked recently given the intense focus on the media business. PEP is a solid business, with the opportunity to invest alongside the core franchises in a ‘flywheel’ of value creation (i.e. Star Wars and Avengers attractions at Parks). After suffering as a result of COVID, the business has bounced back remarkably well, with operating profit now 8% above the FY19 level. Further upside will come from the full re-opening of International Parks – prior to COVID these represented 10% of operating profit of the division. Contrary to conventional wisdom, Return on Invested Capital ( ROIC ) in this business is estimated at 18% and there is further opportunity to invest material amounts of capital at high rates of return.

When we built our stake, Disney was trading at more than a 35% discount to fair value, and we could underwrite the valuation if the streaming business simply broke even. On our FY26 estimates, Disney is trading on a 7% FCFF (free cashflow) yield, despite profitability still being depressed and continuing to reinvest aggressively as highlighted. Using conservative profitability assumptions, we expect the stock to re-rate back to a 4-5% free cashflow yield in FY26.

Walt Disney ( DIS ) DTC Operating Profit and FCFF Yield

{kind=link}

New LONG Position: Rheinmetall AG (~4% weighting)

Increased geopolitical tensions in 2022 have created a renewed willingness by nations to invest in defence capabilities and energy security. Whilst not traditionally an area of focus for VGI, team members have been conscious of this theme and on the lookout for any investment opportunities that may arise as a result. The return of travel in a post-COVID world enabled several members of the team to get back on the road and do one thing we love as part of the investing process – meet in-person with management teams and extensively tour company facilities. After several preliminary calls, we were able to meet with Rheinmetall management in person in late 2022 and came away impressed with the management team and their shareholder alignment, with incentive compensation linked to Return on Capital Employed (ROCE) and operating cashflow, unique in the European market.

Rheinmetall is an international systems provider for defence products, with regional leadership positions in weapons and ammunition, vehicle systems and electronic solutions. There are a number of elements to the moat of the business: a) the currently approved production facilities in a highly sensitive areas (air defence systems, weapons and vehicle systems) where barriers to entry are high, b) technological capabilities and c) relationships with key customers.

The conflict in Ukraine has provided the catalyst for a significant renewal of defence capabilities across the European region, with NATO signatories having committed to significantly increase their spending after a long period of material under-investment; Rheinmetall will grow with these commitments. The current war is seeing supplies rapidly diminish through direct/indirect transfers and it is estimated that 10 years could be required to replenish German stocks to NATO commitment levels in Rheinmetall’s ‘home’ market. In light of this, the German government has increased its defence spending commitment to 2% of GDP and established a 100bn euro special fund. New members have joined NATO and other countries have also committed larger percentages of budget spending to defence (Spain and Italy: 1.4% to 2%; UK: 2.2% to 3%). These commitments provide a strong multi-year tailwind to the Rheinmetall business.

Over the last several years, Rheinmetall has been undergoing a portfolio transformation process as it seeks to become a pure play defence technology business. Traditionally, the business has had a large exposure to Auto Original Equipment Manufacturer (OEM) customers (and Internal Combustion Engine ( ICE ) vehicles in particular) with ~50% of the revenue and operating profits in the business coming from the auto division in 2018. Whilst the company has made investments to capture component revenue from EVs, their exposure to the ICE supply chain has been a drag on the trading multiple and sentiment. Recent portfolio management activities have created a ‘cleaner’ business with higher expected ROIC. Disposal of the pistons unit removes automotive revenue exposure and we project that, following a shrewd recent acquisition in the ammunition space (Expal), by FY25 ~70% of sales and over 80% of profits will come from the defence division.

Rheinmetall Sales and EBIT

Source: Company filings, VGI Partners analysis.

From a valuation perspective, we believe that there are a number of areas supporting valuation. Rheinmetall has a strong history of dividend payments, with dividends increasing at an 18% CAGR from FY17-22. At the FY22 Investor Day, Rheinmetall committed to increasing the dividend payout ratio from 35% to 40% – at expected FY25 dividend of 7.5 per share and assuming the business trades in line with historical dividend yields, we believe the shares are trading at a more than 20% discount to fair value. Historically Rheinmetall has traded in a range of 5x-7x EV/EBITDA – with a chance to re-rate to 6x-8x EV/EBITDA on a significantly higher earnings base.

European defence names generally trade at a significant discount to their US peers, but with such strong budgetary commitments, we see optionality here for a re-rate. The US defence landscape re-rated post a budgetary change from 2011-2020. The French defence budget markedly increased post the annexation of Crimea by Russia in 2014, providing a tailwind to Thales.

Potential risks here stem from the lumpiness of defence sector contracts – indeed we have already seen during our ownership period a delay in several contract awards, but we view these as short-term setbacks vs the longer arc of renewed defence spending in Europe. Further risks are in the relationship with key customers, such as the German government, highlighted by a recent issue with PUMA tanks malfunctioning in live fire exercises. Any export controls would also be a cause of concern given the business has 35% ex Europe revenue exposure and cause us to review the investment thesis.

Exited Position: Olympus (~8% weighting)

We flagged in our last investor letter that we had started reducing our holding in Olympus, the global leader in the manufacturing of gastrointestinal endoscopes. Since then, we have completely exited the position after generating an attractive return on our investment (the stock compounded at ~18% p.a. during our holding period). We took the view that Olympus had reached a close-to-fair valuation and we saw less scope for further margin improvement in the near term following the restructuring programs already instituted by management. The stock has fallen by 20% since our sale and we are continuing to follow it closely in case we see an opportunity to re-initiate a position. Given the appeal of the healthcare industry, where there are a number of high-quality businesses with durable moats and attractive growth opportunities, we have already found better uses of capital and started building stakes in two other healthcare businesses.

In Closing

Recent returns have been truly disappointing and, in our opinion, not representative of our team’s collective efforts nor the underlying quality of the portfolio we hold, which we strongly believe is materially under-valued.

Since VGI Partners’ establishment in 2008, we have been entirely focused on managing our portfolio. Our commitment is to preserve and grow our collective capital over the long term, regardless of the market environment, by owning a portfolio of high-quality businesses which have been purchased with a margin of safety coupled with a series of businesses that have utterly under-appreciated or subject to camouflaged quality characteristics ignored by the crowd.

When we have made errors in the past, we have learnt from them and kept moving forward. Our performance in 2022 has generated much self-reflection and self-assessment. We can do better and we will do better.

To be clear, we cannot eliminate short-term volatility from our returns; however, we are more confident than ever that our process and investment philosophy position our portfolio to produce attractive returns over the long term and through the cycle.

We are very grateful that we have long-term oriented investors who entrust us with their capital. Thank you for your ongoing support and investment with VGI Partners Global Investments Limited.

Yours faithfully,

VGI Partners

| [1] Past performance is not a reliable indicator of future performance. [2] Economic profits are the profits a business generates in excess of its cost of capital, versus accounting profits that can be easily (and often) manipulated by accounting shenanigans. In our experience, long-term, sustained economic profits are typically generated by businesses that operate within favourable or concentrated industry structures, or those with unique business attributes, such as elevated network effects, patents, density economics or special licences. |

DisclaimerThis newsletter is provided by Regal Partners Marketing Services Pty Ltd (ACN 637 448 072) (Regal Partners Marketing), a corporate authorised representative of Attunga Capital Pty Ltd (ABN 96 117 683 093) (AFSL 297385) (Attunga). Regal Partners Marketing and Attunga are businesses of Regal Partners Limited (ABN 33 129 188 450) (together, referred to as Regal Partners). The Regal Partners Marketing Financial Services Guide can be found on the Regal Partners Limited website or is available on request. VGI Partners, is a business of Regal Partners Limited, which is the investment manager of VGI Partners Global Investments Limited (VG1). The information in this document (Information) has been prepared for general information purposes only and without taking into account any recipient’s investment objectives, financial situation or particular circumstances (including financial and taxation position). The Information does not (and does not intend to) contain a recommendation or statement of opinion intended to be investment advice or to influence a decision to deal with any financial product nor does it constitute an offer, solicitation or commitment by VG1 or Regal Partners. It is the sole responsibility of the recipient to consider the risks connected with any investment strategy contained in the Information. None of VG1, Regal Partners, their related bodies corporate nor any of their respective directors, employees, officers or agents accept any liability for any loss or damage arising directly or indirectly from the use of all or any part of the Information. Neither VG1 nor Regal Partners represents or warrants that the Information in this document is accurate, complete or up to date and accepts no liability if it is not. Past performance The historical financial information and performance figures given in this document are given for illustrative purposes only and should not be relied upon as (and are not) an indication of VG1 or Regal Partners’ views on the future performance of VG1 or other Funds or strategies managed by Regal Partners or its related bodies corporate. You should note that past performance of VG1 or Funds or strategies managed by Regal Partners or its related bodies corporate cannot be relied upon as an indicator of (and provide no guidance as to) future performance. Forward-looking statements This document contains certain "forward-looking statements" that are based on management’s beliefs, assumptions and expectations and on information currently available to management. Forward-looking statements can generally be identified by the use of forward-looking words such as, “expect”, “anticipate”, “likely”, “intend”, “should”, “could”, “may”, “predict”, “plan”, “propose”, “will”, “believe”, “forecast”, “estimate”, “target” “outlook”, “guidance” and other similar expressions. Indications of, and guidance or outlook on, future earnings or financial performance are also forward-looking statements. You are cautioned not to place undue reliance on forward-looking statements. Any such statements, opinions and estimates in this document speak only as of the date of this document and are based on assumptions and contingencies and are subject to change without notice, as are statements about market and industry trends, projections, guidance and estimates. Forward-looking statements are provided as a general guide only. The forward-looking statements contained in this document are not indications, guarantees or predictions of future performance and involve known and unknown risks and uncertainties and other factors, many of which are beyond the control of VG1 or Regal Partners, and may involve significant elements of subjective judgement and assumptions as to future events which may or may not be correct. There can be no assurance that actual outcomes will not differ materially from these forward-looking statements. No representation, warranty or assurance (express or implied) is given or made in relation to any forward-looking statement by any person (including VG1, Regal Partners, their related bodies corporate or any of their respective directors, officers, employees, agents or advisers). In particular, no representation, warranty or assurance (express or implied) is given that the occurrence of the events expressed or implied in any forward-looking statements in this document will actually occur. Except as required by law or regulation, VG1 and Regal Partners disclaim any obligation or undertaking to update forward-looking statements in this document to reflect any changes in expectations in relation to any forward-looking statement or change in events, circumstances or conditions on which any statement is based. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

VGI Partners Investor Letter - Full Year 2022