VMD - Viemed Healthcare: Superb Growth Expectations Reiterate Buy

2023-05-18 02:18:45 ET

Summary

- Viemed Healthcare collected another quarter of sequential and YoY sales growth.

- Investors have revised expectations for the company and added $273mm in market cap off March 2022 lows.

- Diverting capital back into growth investments to drive earnings growth.

Investment Summary

The revised investment thesis posed for Viemed Healthcare, Inc. ( VMD ) in November 2022 has been partially vindicated with a 49% return to the time of writing. As a reminder, I suggested clients to buy VMD in November at $6.80-$7.00 with a suggested price target range of $10.65-$12.65. This was built on:

- Multiple growth initiatives to be realized downstream despite their impacts on profitability (at the time in Q3 FY'22).

- Employee base to 722 underscored by a large growth in sales rep headcount, another 52 reps in September. Last quarter, it was. 770 employees, and it expects to add another 180 this year.

- Durable medical equipment ("DME") sales growth of 63% YoY, equipment and supply sales of 51% - both are attractive percentages.

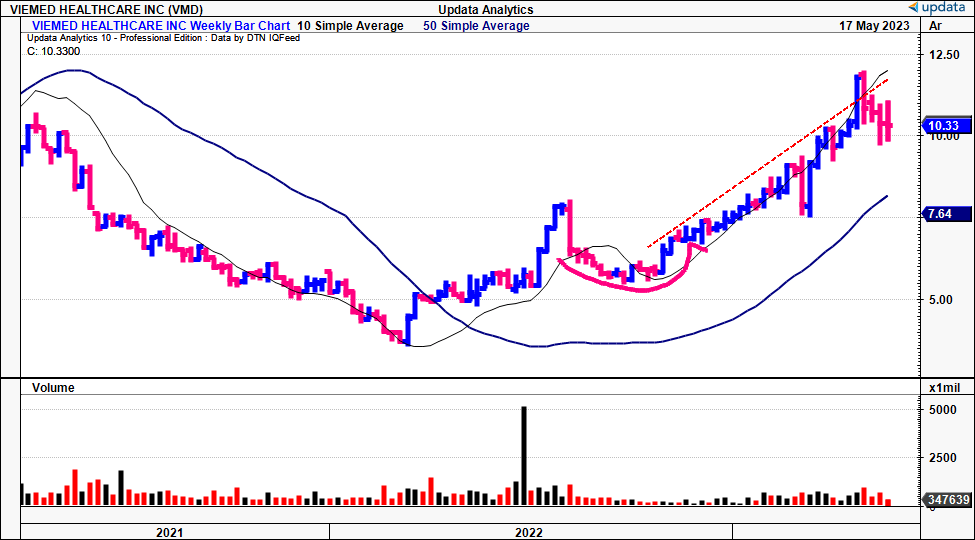

VMD has taken out the $10 level amid a tremendous rally off FY'22 lows, breaking out from the cup and handle pivot point shown and forming the ascending channel. The climax top, where the equity line broke the upper trend line around 5-6 weeks ago, could present us with a period of consolidation in the near-term.

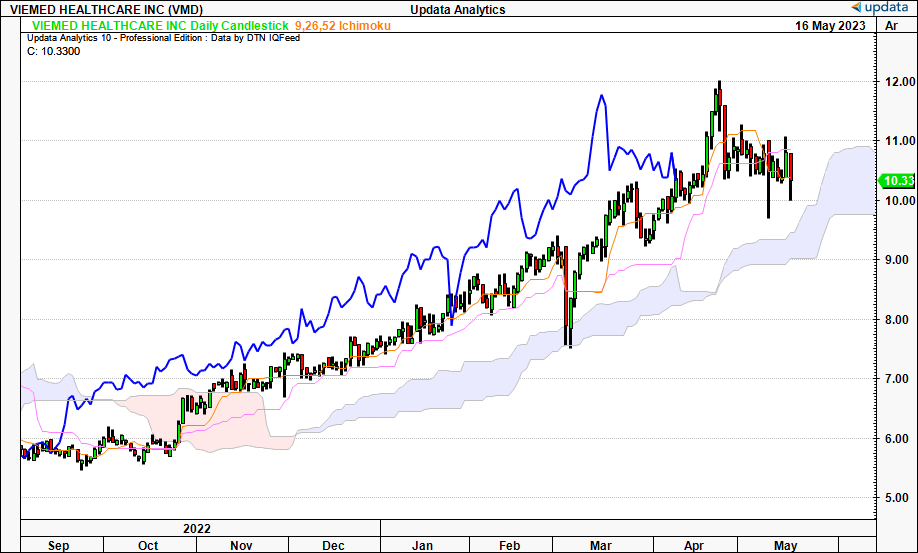

Thankfully, long-term investment potential is backed by robust fundamental data in VMD's case, and the market certainly has high expectations for the company. Its Q1 earnings are telling of the same, with bold capital allocation projected by management ahead. Further, it is still within long-term trend with room to consolidate, seen in Figure 1a.

Net-net, I reiterate VMD as a hold, looking for $13-$17, a revision up from the last publication.

Fig. 1

{kind=link}

Fig. 1a

Note: Trading above cloud = bullish. Daily time frame is looking weeks ahead. Hence, bullish on medium-term. (Data: Updata)

{kind=link}

Before proceeding, it is essential to grasp these key downside risks to the investment thesis:

- Market machinations that produce downside volatility. A large correction in the S&P 500 will likely cause a larger selloff in VMD.

- Not meeting growth targets outlined by the market. Investors will reprice the company if that's the case.

- Ongoing macro-level risks that are a threat to corporate earnings.

These risks must be heavily considered by investors before considering any investment decision.

Q1 earnings dissection + growth outlook

At this stage in its lifecycle, the valuation of VMD's equity is measured by its steady-state value, plus the contribution from future growth. Here, growth is benchmarked against revenue, earnings and returns on capital.

Looking to the first quarter, evidence is found in the financial results. Revenues of c.$40mm were up 31% YoY and 600bps sequentially. It pulled this down to 61% gross on $8.3mm core EBITDA for the quarter. VMD is at a $160mm FY'23 run-rate on $24mm annual pre-tax earnings if it keeps this pace. They key economic findings for VMD's investment case, as it relates to Q1, are outlined below.

1. HMP transaction (completed at 1.1x FY'22 sales)

Leading points for the discussion for its Q1 is the HMP transaction, key facts of which are to follow. I'd start by saying there are major strategic benefits to this acquisition in my opinion. One major upside to VMD following the transaction, expected to close at $31mm (1.1x sales), will be the extensive payer/physician relationships HMP brings.

This broader database is a strategic lever for the firm, because it will spread the distribution of its patient and payer network across a wider geography. For example, HMP's business is ~45% sleep and 13% ventilation, two markets VMD excels in. This offers plenty of revenue synergies because HMP is already growing its sleep franchise to share the execution risk there, whilst VMD get to focusing on growing HMP''s ventilation segment.

These points are worth noting as well:

- Additional market share . As a reminder, HMP is a major provider across 3 states (Tennessee, Alabama, Mississippi), this serves >44,000 activations at the time of writing. In my opinion, HMP's market position in these regions positions the VMD well to capture additional market share one the deal is fully integrated. In FY'22, HMP reported revenues of ~$28mm, which would immediately fold into VMD's top-line on closing.

- Accretive potential, plus synergies. By estimation, the true deal value for VMD is to amalgamate HMP's extensive respiratory team with the company's own complex respiratory model. This is the keystone moment for VMD in my informed opinion. Despite substantial capital investment into scalability and clinical programs, to date, the major hurdle VMD has had to overcome has always been on the labour side. It has the artillery, just not the troops. The HMP remedies this barrier as the firm "identified 180 incredibly talented individuals that will have access to our well-developed resources and capabilities" as part of the transaction.

Net-net, the move will strengthen VMD's respiratory supply chain in my opinion, and is an appropriate use of capital to achieve strategic growth initiatives.

2. Capital allocation, returns on incremental investment

Analysis of core business revenue, margins, capital investments and allocations is telling of VMD's near-term growth opportunities. For one, the c.$40mm in turnover clipped another 31% YoY expansion, as mentioned. The sequential gain of 6% is notable as well - there's seasonality in VMD's revenue in H1 vs. H2 thanks to insurance changes and so on. In that vein, pushing through this with a 6 point gain is good evidence the firm captured additional market share.

There's far more to the story here, however. VMD is recycling its retained capital into additional profit growth, and, evidently, additional market valuation.

There is ample evidence in my findings.

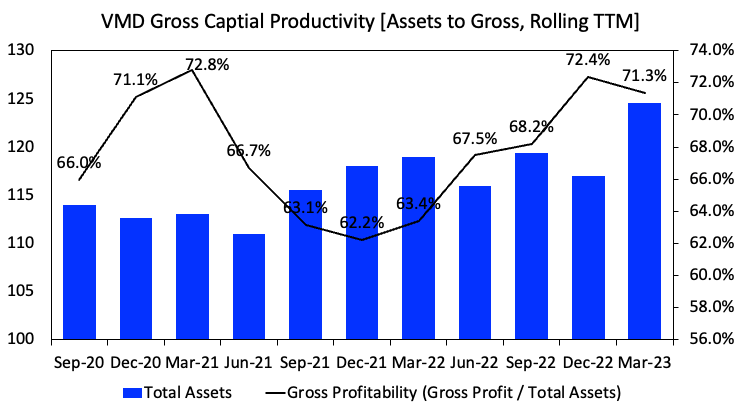

- One, gross capital productivity is superb and gaining momentum, after firm generated $0.71 on the dollar in gross profit from its asset base in Q1. This is observed in Figure 2. Here, gross capital productivity is shown via gross profitability, the TTM gross profit divided by total assets each quarter. It shows the seasonality in VMD's business as well, and the upsides in Q1 on this. Looking forward, I am looking to another 70-73% gross profitability in FY'23, which could generate $92-$110mm in gross this year on my estimates.

Fig. 2

{kind=link}

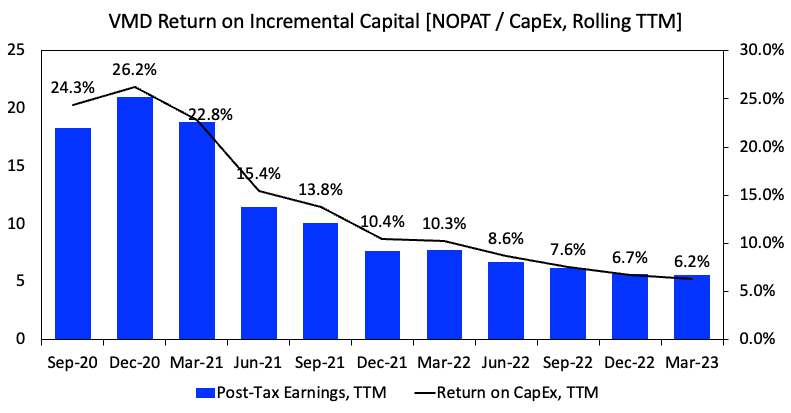

- Two, CapEx of $24-$25mm per quarter is a healthy pace and is being ploughed back into the firm's major product lines in vents and oxygen. The gross benefits of this are discussed in the point above, and the net benefits are observed in Figure 3. Here, tax-adjusted operating income is plotted against the return on CapEx in rolling TTM periods. This represents the total profit generated by each turn in capital investments. NWC is not included in this calculus. The absolute level of VMD's post-tax earnings have been hampered by tax payable from 2021 onwards, yet still produce 6-7% trailing returns. I believe this is one major factor, along with revenue growth, that has spurred investors to reward VMD with a higher market valuation. Whilst the near-term profits have shrunk, the market expects tremendous upside from this, discussed below.

Fig. 3

{kind=link}

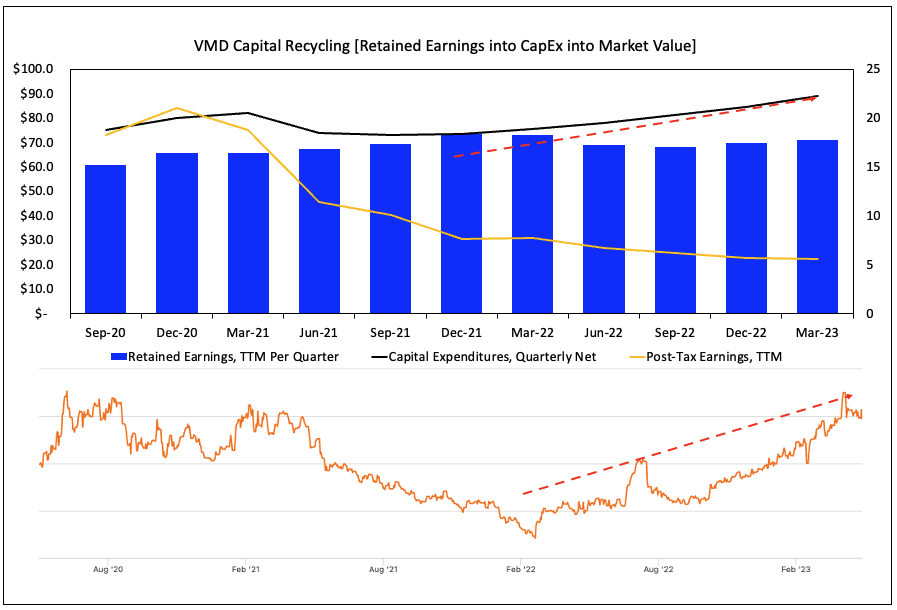

- Three, VMD's capital allocation has switched to earnings growth this year after prioritizing buybacks and debt retirement in 2022. Management are now saddled up to drive capital commitments to M&A and additional growth funding to create value. The correspondence between the capital VMD has retained from shareholders (retained earnings), CapEx and market valuation are seen in Figure 4. Retained capital has been put to work since Q1 FY'21, shown via the uplift in quarterly CapEx. Since embarking on this plan from December 2021, the market has rewarded VMD with an 171% increase in market valuation off its March lows. This tells me VMD is rotating capital investments back into market valuation. To illustrate, from the March 2022 period to date, VMD invested an additional $408mm in fixed assets, seeing investors value it $273mm higher in market cap, a 67% market return on investment. By proxy, this evidences the company's high returns on capital above the hurdle rate.

Fig. 4

Note: Market Cap Data shown to 17/05/2023 (Data: Author, VMD 10-Q'; market cap image drawn from Seeking Alpha. )

{kind=link}

3. Valuation

Investors are paying ~19x forward earnings for VMD on last check, still a 30% discount to the sector. You might frown at the 4x premium to book value, but I'd remind you, you've enjoyed a 36% 2-year gain in book value/share in VMD, ahead of the S&P 500 index's return over that time. This, as the stock trades above moving average's across all time frames (32% above the 200DMA alone). I believe similar trends are possible moving forward, so the 4x multiple may be warranted at this stage, and more indicative of the value management have created above the company's book value of equity.

It is important to understand what expectations the market has baked into VMD's stock price. I'd use a 12% discount rate to price VMD given this represents a long-term opportunity cost of key benchmark rates (UST 10-year + S&P 500). Recall that investors have added another c.$250mm in VMD's market value since it began reinvesting ~$405mm of capital back into the business. In that vein, the market obviously expects this investment to pull through to earnings growth:

- At the 12% hurdle and $273mm value add, analysis reveals that investors expect another c.$32.5mm in post-tax earnings from this $408mm investment ($32.5/0.12 = $270mm).

- Furthermore, it expects $50mm in forward earnings from VMD at the current market value ($50/0.12 = $416mm).

- These are tremendous growth percentages that call for 85% earnings CAGR over the next 3-years, from the TTM EBIT of $7.9mm ((7.9x1.85^3)/0.12 = $416mm).

Circling back to the value equation brought up earlier of steady-state plus growth, you can see the market is placing high odds on VMD's growth contribution, when factoring its FY'22 numbers. It values just $68mm for the steady state ($8.2/0.12 = $68.3mm) and therefore, I estimate that 83% of VMD's current market valuation is formed by the forward growth expectations outlined here. In that regard, hitting its guidance numbers are therefore paramount in ensuring valuation upside over time.

My numbers reveal differences to the market's expectations. I have VMD to be at $77mm in annual EBIT by FY'25, $60mm adjusted for tax, well above the $5.5mm at present. Should it keep the pace of CapEx up, at $400mm over the next year, this incremental return on investment would create future value for shareholders with 1-2% in economic earnings vs. the hurdle (($60-$5.5 = $54.5) / $400 = 13.625%). Discounting this at the 12% hurdle rate is an NPV range of $500-$641mm in market valuation for VMD, or $13-$17/share (($77, $60)/0.12 = $500-$641mm). This represents 30-70% upside potential.

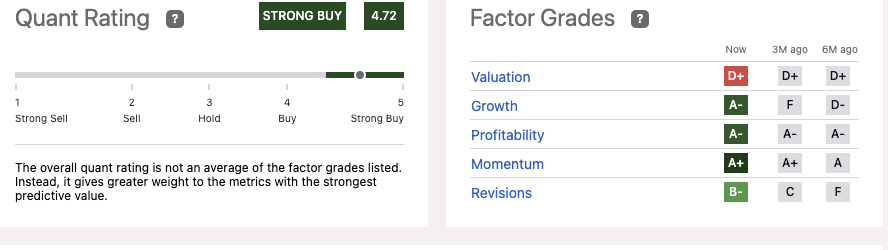

These findings are well supported with objective data in the quant rating system, that advocates VMD as a strong buy. This added conviction adds substantial weight to the buy thesis.

Fig. 5

{kind=link}

In short

There are multiple inflection points currently driving up the equity line of VMD. Notable among these, are the strong revenue upsides and heavy reinvestment back into future growth. The market expects a large uptick in earnings from these efforts, evidenced in the firm's 50% rally since November. I believe there is scope for the stock to rate another 30-70% higher to $13-$17 per share with my forward earnings estimates into FY'25. Net-net, reiterate VMD as a buy.

For further details see:

Viemed Healthcare: Superb Growth Expectations, Reiterate Buy