VCISF - Vinci: No Shortage Of Growth Drivers

2023-10-04 05:07:05 ET

Summary

- Vinci's attractive high-margin Concessions business has come to dominate its bottom line, which should aid earnings stability across the business cycle.

- The Airports business still has some COVID recovery potential left, while the Energy business and Cobra should be a winner from the energy transition.

- A sharp economic downturn represents the main risk to Vinci, particularly the more cyclical Construction business, though I expect the overall business to prove resilient in that scenario.

- With high-single-digit annualized earnings growth potential over the next few years, these shares look attractive.

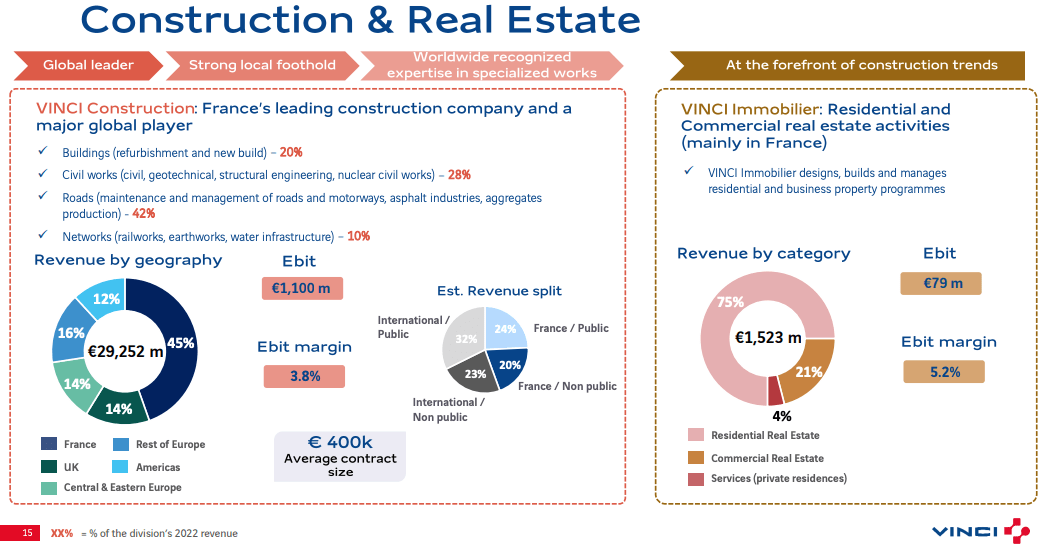

Construction can be a volatile business, but French giant Vinci (VCISY)(VCISF) operates a deceptively resilient businesses. While a little under half of total revenue (€60 billion in FY2022) is generated by its construction contracting arm, Vinci Construction, EBITDA and net income margins in the low single-digit range mean that this is a relatively small contributor to group earnings. Further, around 55% of Construction revenues are tied to public sector clients, while contracts are largely in activities that shouldn't be too sensitive to the business cycle in any case (e.g. road maintenance, water works, railway engineering and so on)(Fig 1).

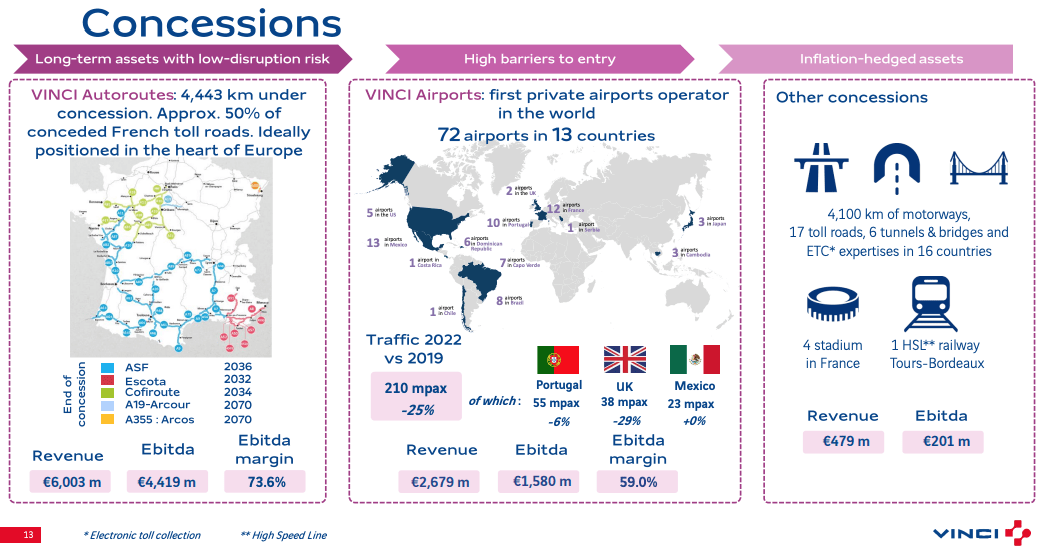

Complimenting the above is the Concessions business, the most attractive part of Vinci's business. Vinci manages around 4,400km of tolled French motorways (Vinci Autoroutes) on long-term contracts that run until anywhere between the early-2030s and 2070 depending on the route. Vinci's network is equivalent to around 40% of France's total motorway network and circa 50% of the tolled motorway network. The company also operates over 70 airports in around a dozen countries.

Autoroutes and Vinci Airports contribute around 15% to the top line collectively (9% and 6%, respectively in 1H2023), but sport EBITDA margins of ~73% (Autoroutes) and ~60% (Airports)(Fig 2). With a small contribution from its collection of other Concessions assets, this means that the high-margin Concessions segment accounts for the lion's share of group operating income (~70% in 1H2023).

Fig 1 (Source: Vinci SA 2023 Investor Presentation) Fig 2 (Source: Vinci SA 2023 Investor Presentation)

{kind=link}

{kind=link}

Airports & Energy Businesses Can Drive Growth

Missing from the above is Vinci Energies (~18% of 1H2023 EBIT) and Cobra IS (~7%). Cobra is an industrial engineering contractor that has a large business line in energy infrastructure (maintenance and turnkey construction projects like solar farms etc.). It is mainly active in the Iberian Peninsula and Latin America (combined ~75% of Cobra revenue). Vinci Energies is more diverse than its name suggests and is a holding segment for a myriad of different companies. Energy infrastructure is obviously a big part of it, but this segment also captures things like niche industrial applications (e.g. specialized equipment, digital solutions and so on).

Many governments have committed themselves to the so-called energy transition away from fossil fuels. This is going to require vast amounts of new infrastructure, and would be a natural tailwind to a chunk of Vinci's business. Indeed, it already is. Vinci Energies revenue in 1H2023 (€9.1 billion) was already 44% higher compared to 1H2019, while margins have been expanding too (Fig 3).

I am similarly bullish about the airports business in the Concessions segment. Vinci has some excellent long-term growth drivers here; for instance, last year it acquired a 30% stake in Mexican operator OMA (NASDAQ: OMAB ), which is enjoying a boom due to supply chain nearshoring . Q3 numbers aren't out yet, but looking at airport data directly shows we can expect good growth. OMA, for example, reported 17% YoY traffic growth in July and 22% YoY growth in August (Fig 4). Better still, airport traffic hasn't fully recovered from the impact of the COVID pandemic yet, so there is still a fair amount of latent growth potential there. Because margins are so high in this segment, Airports revenue growth has an outsized impact on Vinci's bottom line.

Ditto for Autoroutes. Revenue growth potential is modest there, ultimately boiling down to low-single-digit annualized contributions from traffic levels and tariff hikes, but operating leverage means a bigger impact on Vinci's bottom line. All told, the company has no shortage of drivers to grow profits.

Fig 3 (Data Source: Vinci SA Interim Results Reports) Fig 4 (Data Source: OMA)

Sharp Economic Downturn The Main Risk

At this point in the cycle a sharp economic downturn represents the main risk to Vinci. The Construction segment has a cyclical bias to it and low EBIT margins could leave it susceptible to a sharp drop in earnings should revenues weaken. Due to the macro-resilient nature of its Concessions business (particularly Autoroutes), I do expect this would result in relatively flat group medium-term earnings growth rather than the 7-9% annualized growth I expect (see "Anticipating Earnings Stability" section below). While an exogenous shock that simultaneously hits Concessions EBIT can't be ruled out (COVID was only three years ago after all), it appears unlikely.

Anticipating Earnings Stability

Vinci shares trade for €101.42 each in Paris trading at time of writing ($26.38 for the ADRs, ticker "VCISY"). That works out to around 13.5x FY2022 EPS, and represents a circa 4% yield on the FY2022 dividend per share. Vinci's valuation looks fairly cheap to me, notwithstanding the chance of an economic downturn, though even in that scenario I expect the underlying business to hold up reasonably well.

I say that for a few reasons. Firstly, while it is true that EBIT fell substantially between 2019 and 2020 (from €5.74 billion to €2.86 billion), this was mostly due to COVID-specific factors, chiefly the unprecedented collapse in airport and road travel due to lockdowns. Vinci Airports EBIT fell from a €1 billion profit (2019) to a €0.36 billion loss (2020), while the usually reliable Autoroutes division saw EBIT fall 33% YoY. A contraction of that magnitude is very unlikely to happen this time. A recession might knock business air travel in particular (20% of Vinci Airports passenger traffic), for example, but it's not going to be anything like what happened in 2020. For a more 'normal' benchmark of performance in a downturn, here's what Vinci's EBIT looked like during the global financial crisis: €3.12 billion (2007), €3.38 billion (2008), €3.10 billion (2009) and €3.43 billion (2010). Much more resilient.

The second reason I am bullish on Vinci's medium-term earnings stability is due to inflation. A good portion the firm's revenue and EBIT is linked to inflation metrics, even if it doesn't capture the full change in the index (e.g. Autoroutes tariffs typically price at 0.7x CPI). However, this will still support nominal earnings growth. The third reason is the Airports situation mentioned above: there is still some COVID-linked recovery potential in the tank there.

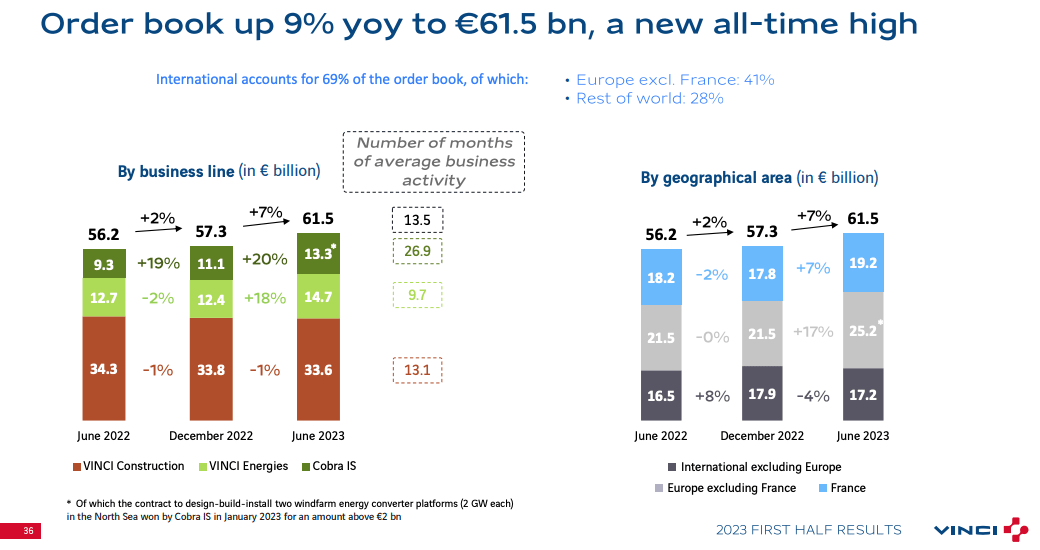

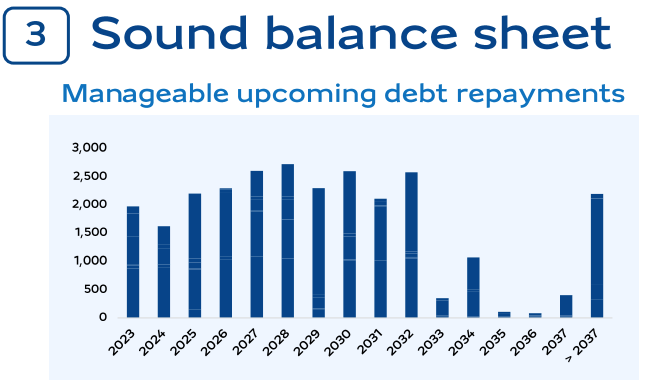

The final reason is the size of Vinci's order book. It is at a record €61.5 billion, equivalent to 13 months activity (Fig 5). This should prevent the company from having to take on unprofitable contracts in the event activity dries up. Vinci does have around €1.5-€2.0 billion in annual debt maturities over the next few years (Fig 6), but between cash on the balance sheet (~€10.7 billion as of 1H2023) and retained earnings generation (~€2.2 billion) I expect this to be easily manageable.

Fig 5 (Source: Source: Vinci SA 2023 Interim Results Presentation) Fig 6 (Source: Vinci SA 2023 Investor Presentation) Fig 7 (Source: Vinci SA 2023 Investor Presentation)

{kind=link}

{kind=link}

With that, I see Vinci growing net income by around 7-8% per annum over the next few years. That is driven in roughly equal parts by revenue and profit margin expansion as Concessions growth has an outsized impact on earnings growth. With Vinci typically paying out 50% of net income as a dividend (Fig 7), I expect the current 4% payout to grow broadly in line with earnings. Implied shareholder returns of 11-12% on a flat 13.5x P/E look attractive. Buy.

For further details see:

Vinci: No Shortage Of Growth Drivers