VIST - Vista Energy: A Success Story In The Making

2023-12-27 23:04:40 ET

Summary

- Vista Energy is an oil & gas producer based in Mexico and Argentina.

- They are currently in the middle of a drilling campaign, which should lead to significant revenue and cash flow improvements.

- The company is presently trading with a low P/E, and multiple PEGY estimates imply it is undervalued compared to its future growth expectations.

- I currently rate VIST as a Buy.

Thesis

Vista Energy, S.A.B. de C.V. ( VIST ) is in the middle of a significant expansion. They are drilling new wells and attaching them to a pipeline network for servicing both local and export markets. While this is producing significant capital expenditure, it should also lead to significant revenue increases.

This is a follow up to my last article on Vista Energy. After looking over their financials and valuation, I presently rate Vista as a Buy.

Company Background

Vista Energy is an oil & gas producer headquartered in Mexico City, Mexico. They were founded in 2017 and operate primarily through Vaca Muerta in the Neuquina basin in Argentina. They have made a pledge to become carbon neutral and are currently expanding their capacity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Long-Term Trends

The global oil and gas market is projected to have a CAGR of 5.4% until 2028. The oil and gas market in Mexico is expected to a CAGR of 3.4% until 2030. The market in Argentina is expected to have a CAGR 3.5% until 2028.

Guidance

Their earnings call transcript can be found here . Normally, I only show highlights from the transcripts and cut most of the extraneous statements out of these articles. However, this transcript is heavy on facts and light on fluff, so I find myself clipping rather large blocks of text. Even though I am summarizing highlights, I encourage investors to read the transcript in its entirety.

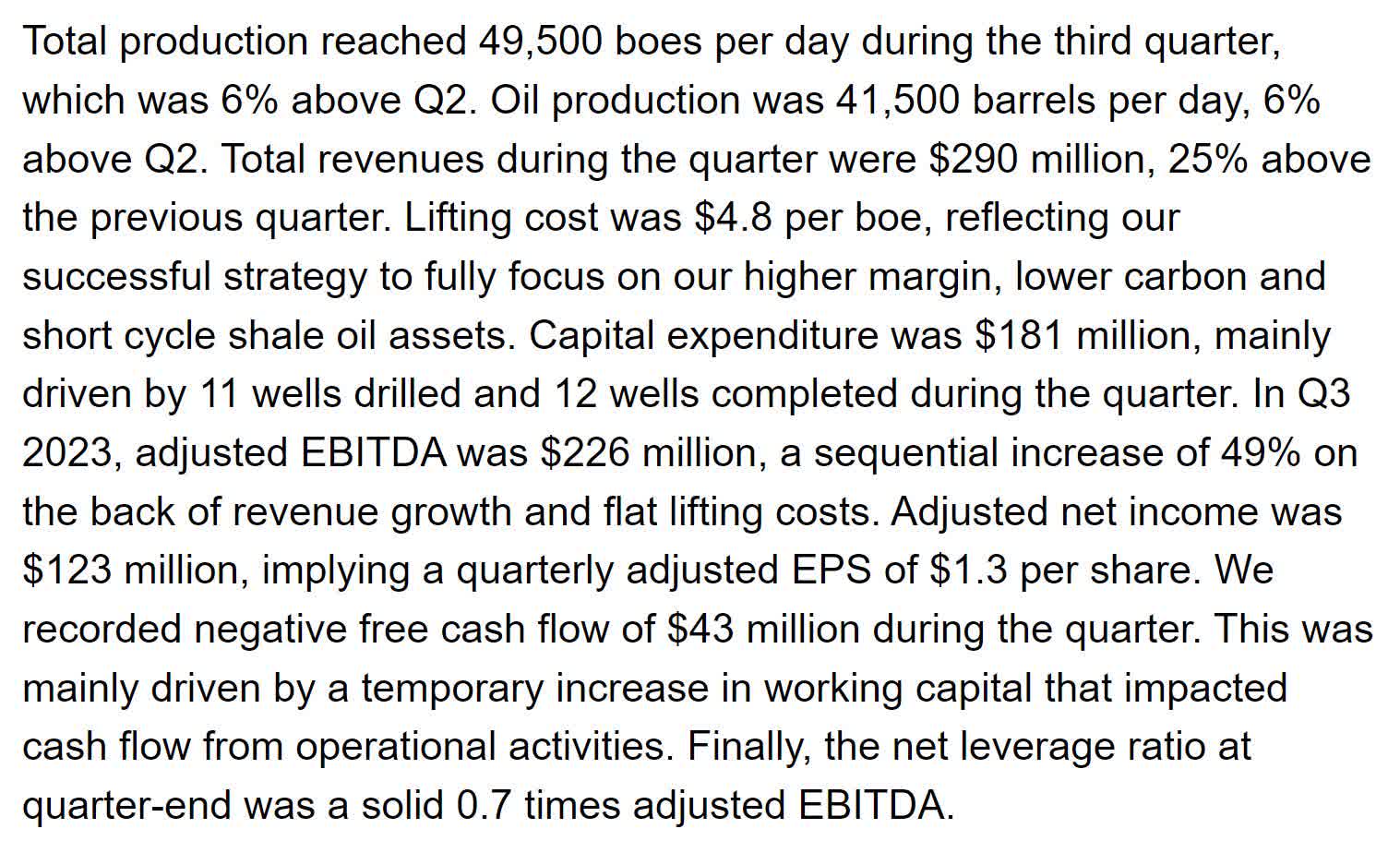

The initial summary statement at the beginning of the earnings call indicated the company is doing well. They have both increased their production and are busy drilling additional wells to drive future revenue growth.

{kind=link}

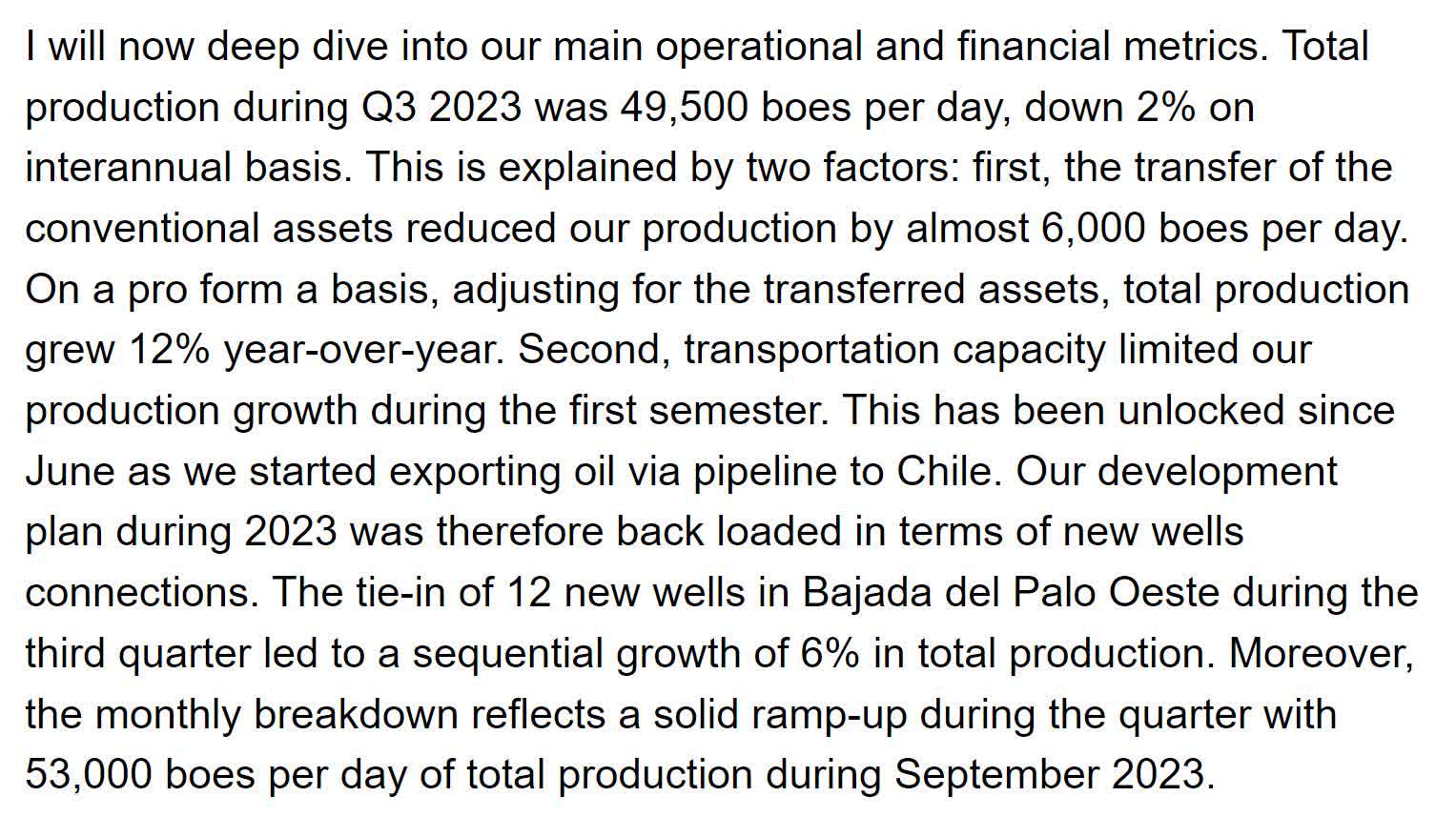

Production is 2% lower due to a transfer of assets. When adjusting for this, their total production grew 12% YoY. In June they began exporting oil through Chile. They managed to connect an additional 12 wells to the pipeline network this quarter.

{kind=link}

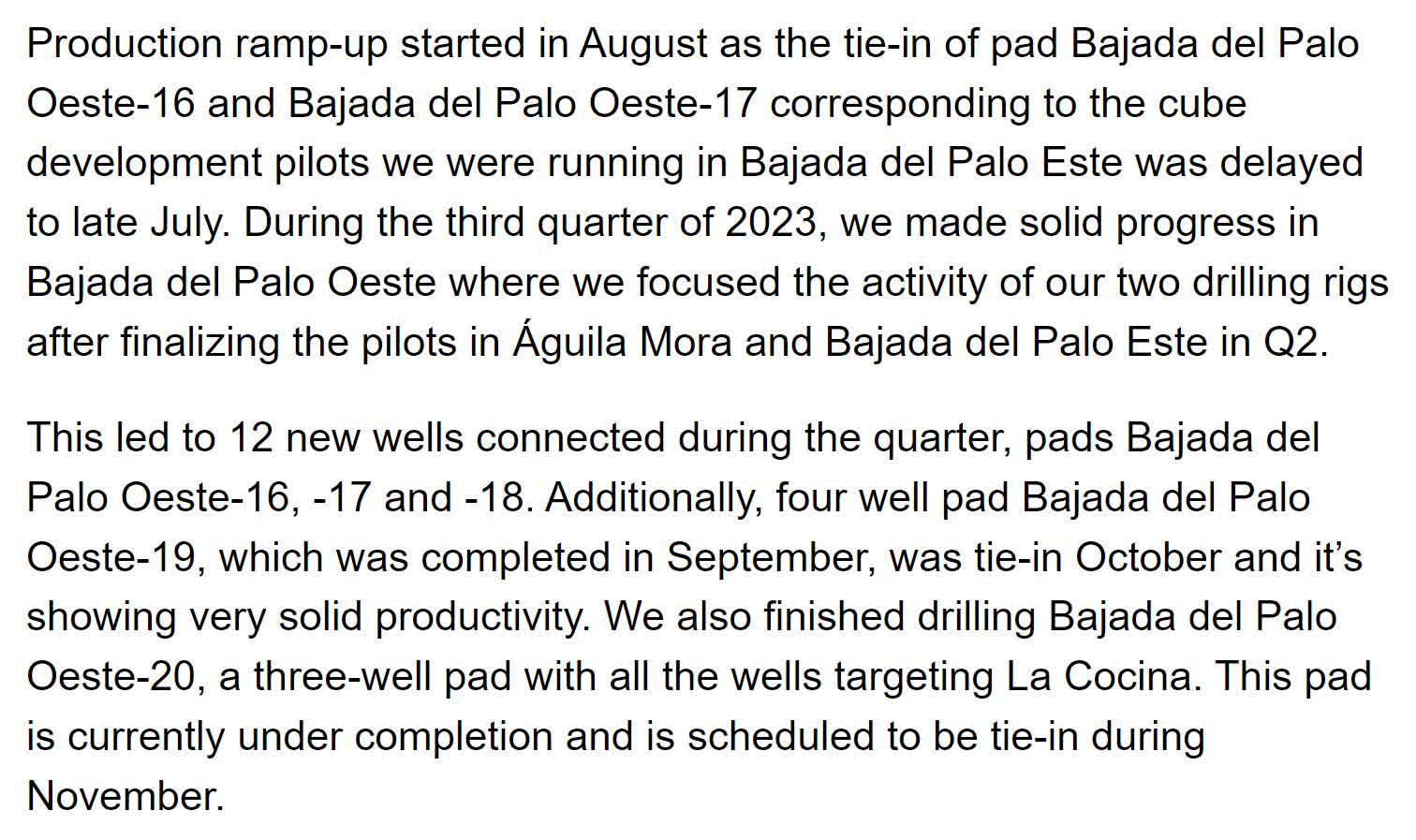

They began ramping up production in August and continued to tie wells to the pipeline network through October and September. They also have an additional 3 wells (the Palo Oeste-20 pad) they planned to attach in November.

{kind=link}

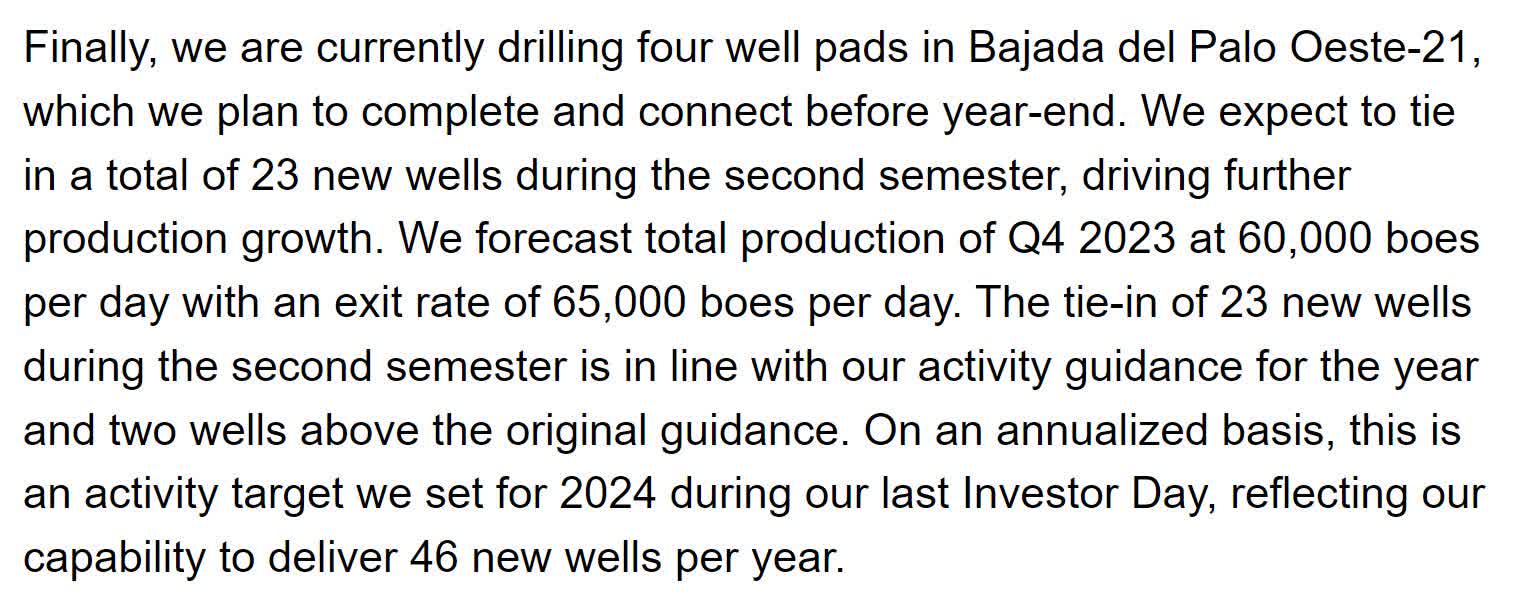

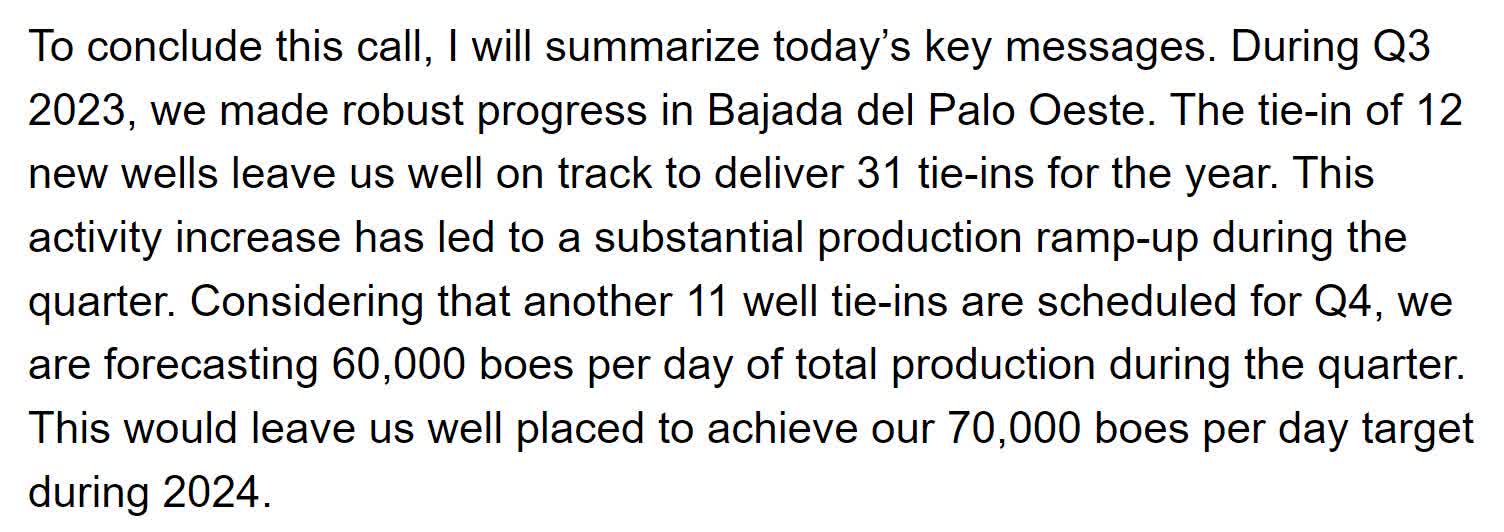

As of the October 25th call, they planned on drilling and connecting an additional four well pads before the end of the year. They expect to be able to complete and connect 23 new wells during the second semester. This is two wells above their previous guidance.

{kind=link}

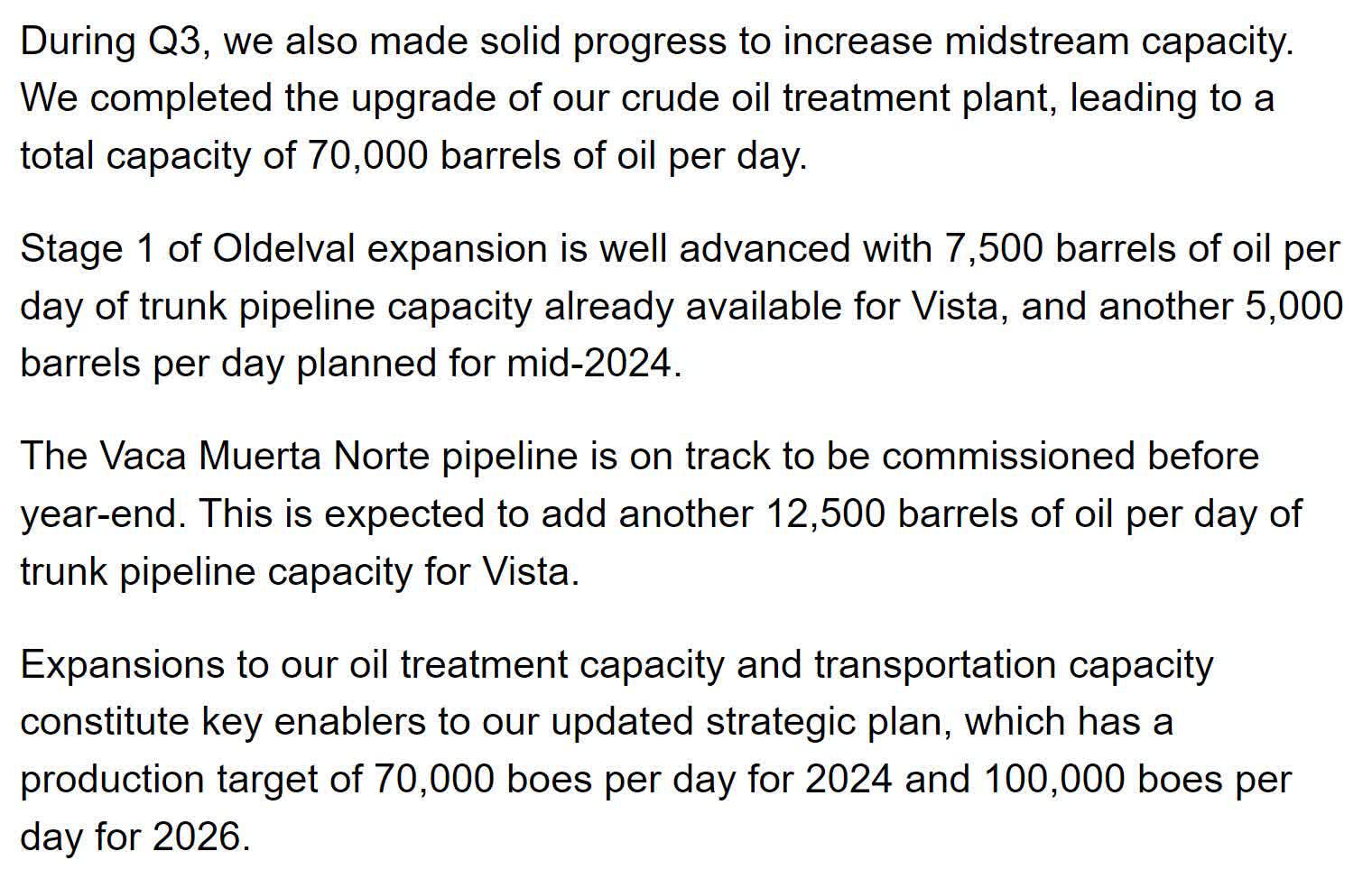

During the quarter, they completed the construction of a crude oil treatment plant. They also plan on brining an additional pipeline online before the end of the year. They expect for these developments to help contribute to their target of 70K barrels per day for 2024 and 100K per day for 2026.

{kind=link}

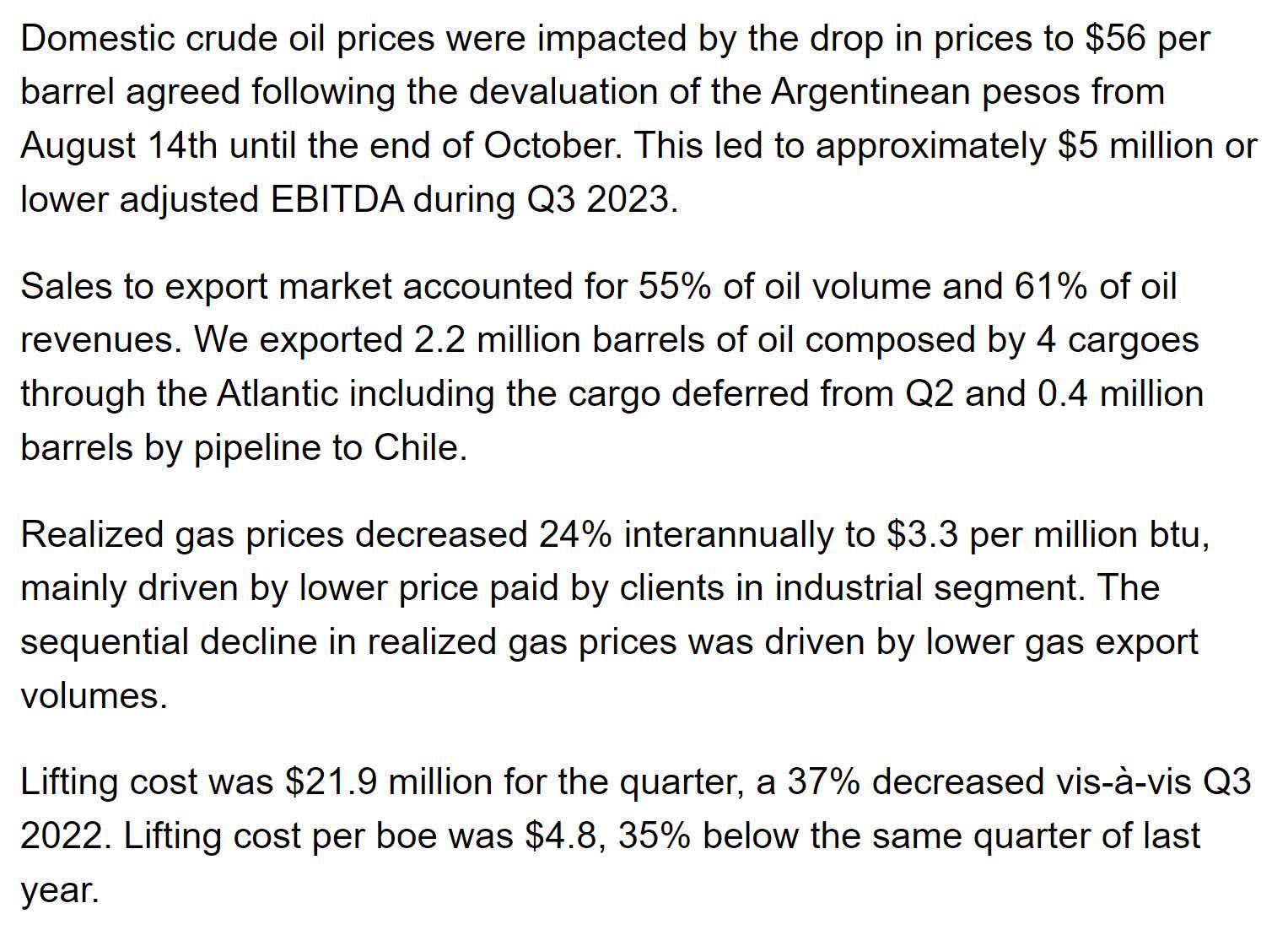

Their income was affected by the drop in price of crude oil to $56 per barrel, leading to a shortfall of expected Adjusted EBITDA of roughly $5M. The price of gas fell internationally by 24%. They managed to lower lifting costs per barrel by 35% compared to this same quarter last year.

{kind=link}

They expect their lifting costs to stay low and for the average cost for the full year to be $5.2 per barrel, which is roughly 5% lower than previous guidance.

{kind=link}

They are forecasting 60K barrels per day for Q4 and 70K per day for 2024.

{kind=link}

Quarterly Financials

Their quarterly financials are showing significant revenue growth up until September of 2022. Their revenue is heavily affected by changes in the price of oil.

{kind=link}

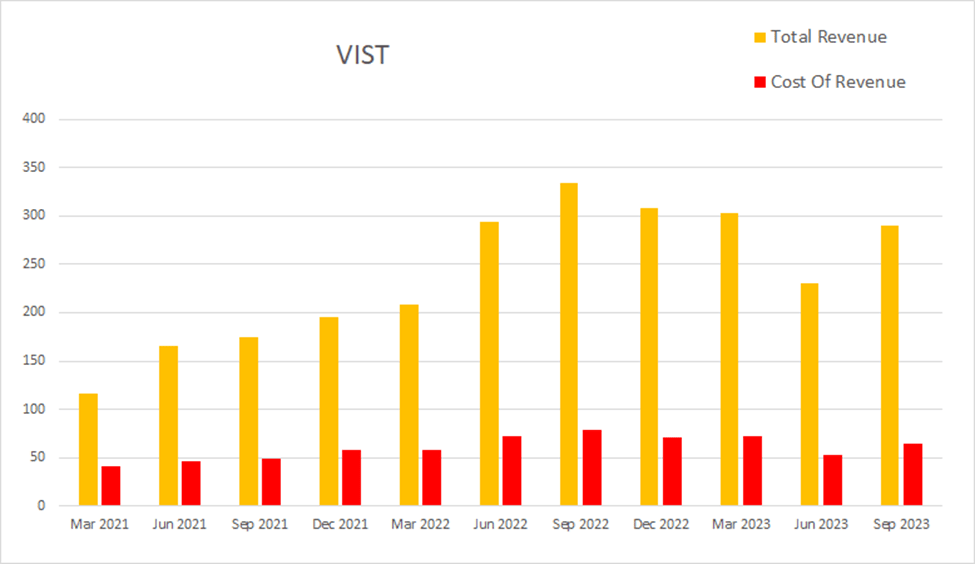

Eight quarters ago Vista had a quarterly revenue of $175M. Four quarters ago that had grown to $333.5M. By this most recent quarter that had declined to $289.7M. This represents a total two-year increase of 65.54% at an average quarterly rate of 8.19%.

{kind=link}

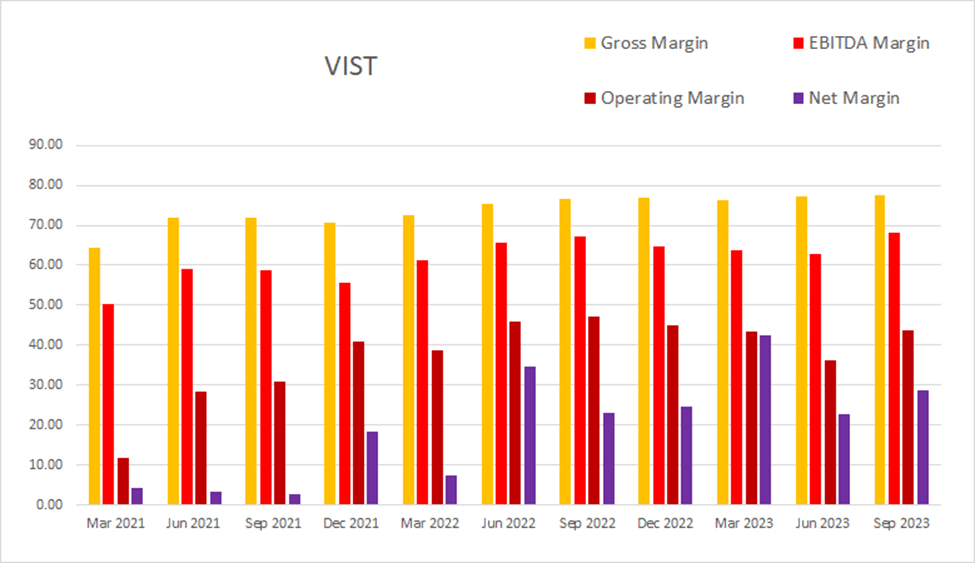

Their gross margins expanded up until September of 2022, but have remained fairly stable since then. As of the most recent quarter gross margins were 77.53%, EBITDA margins were 68.04%, operating margins were 43.80%, and net margins were at 28.68%.

{kind=link}

They have been both diluting and buying back shares. The sum of their last eight quarters of dilution comes to 7.64%; the sum of their dilution over the last four quarters comes to 9.76%.

{kind=link}

{kind=link}

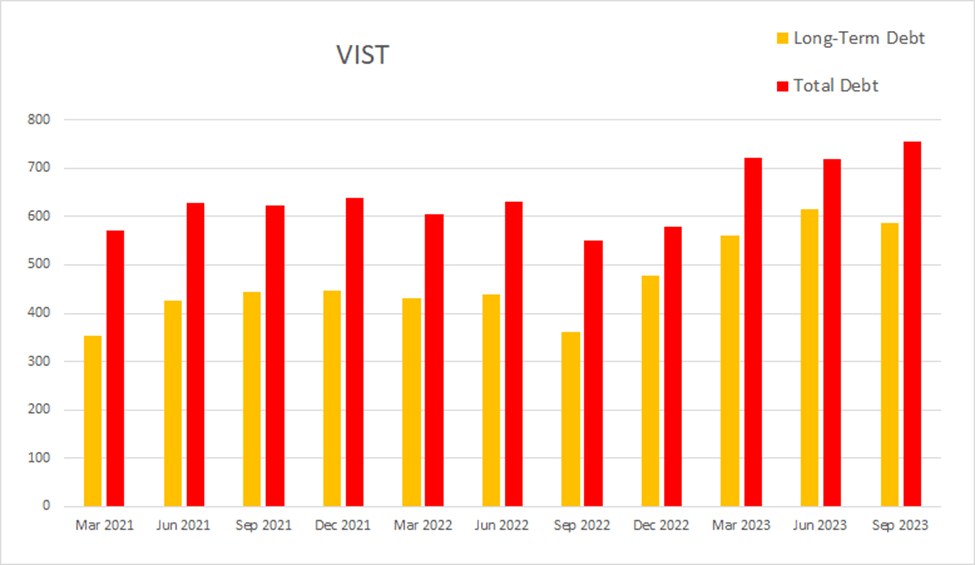

The most recent quarter, Vista had -$5.2M in net interest expense, total debt was at $754.50M, and long-term debt was at $587.6M.

{kind=link}

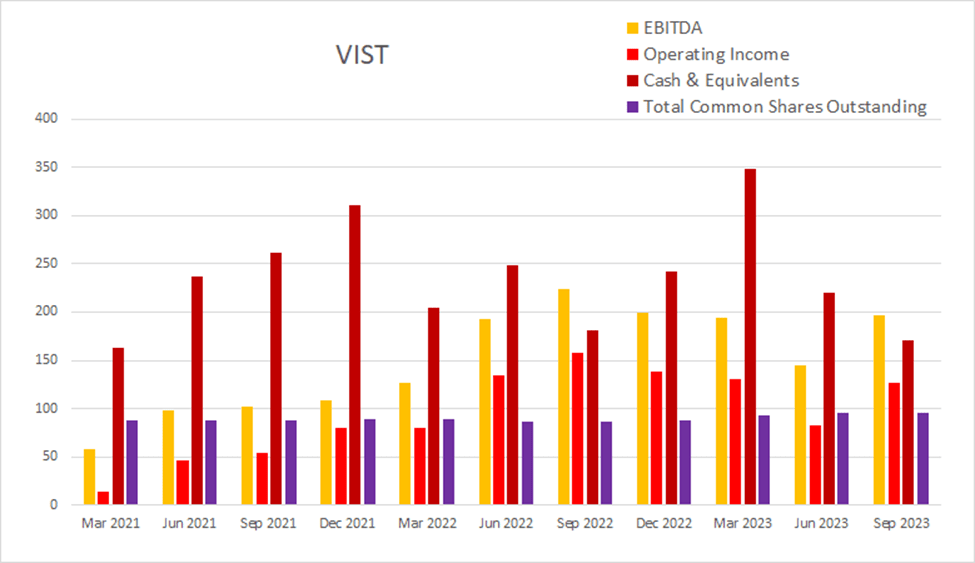

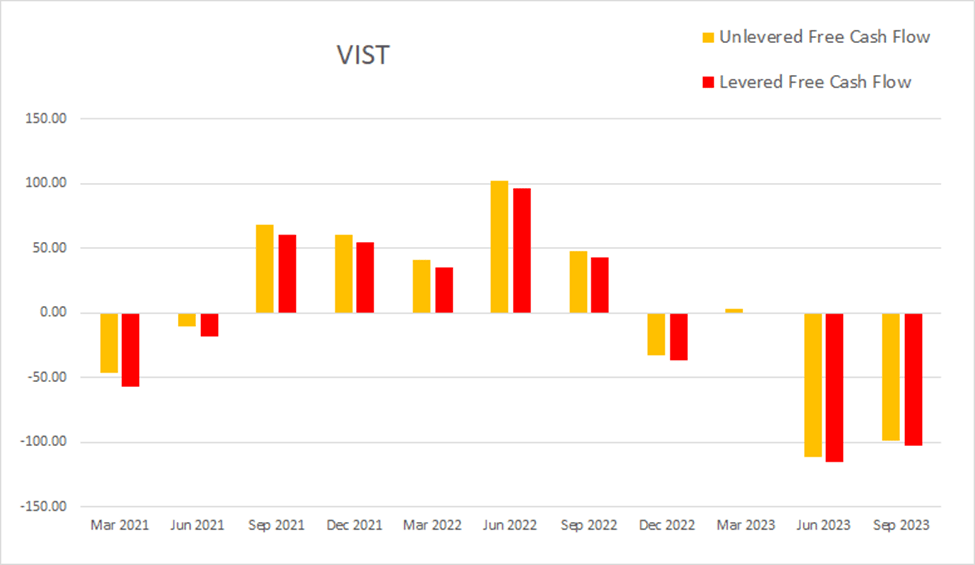

As of the most recent earnings report, cash and equivalents were $171M, quarterly operating income was $127M, EBITDA was $197.1M, net income was $83.1M, unlevered free cash flow was -$99.30M, and levered free cash flow was -$102.7M. As mentioned in their earnings call, they had significant capital expenditure. This most recent quarter they had $162.8M in CapEx. This is why they posted positive net income and negative cash flow.

{kind=link}

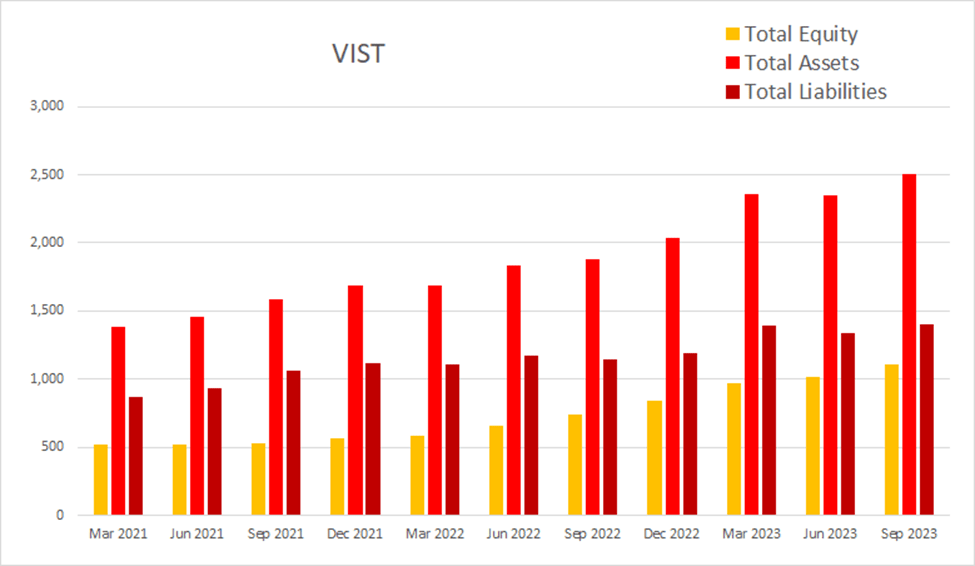

Total equity has been rising.

{kind=link}

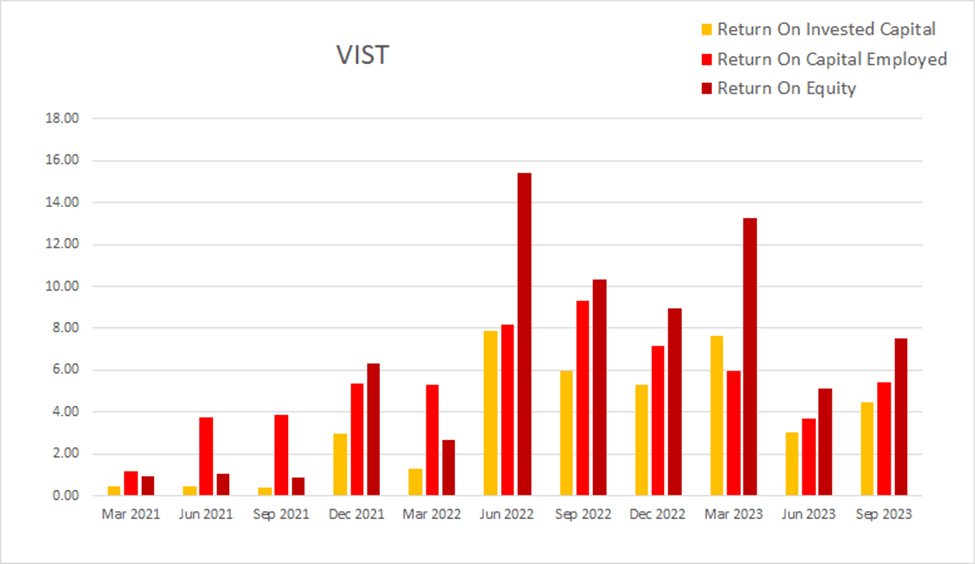

Their quarterly returns vary significantly with the price of crude oil, but are still quite attractive. As of the most recent earnings report ROIC was 4.47%, ROCE was 5.43%, and ROE was 7.51%.

{kind=link}

Valuation

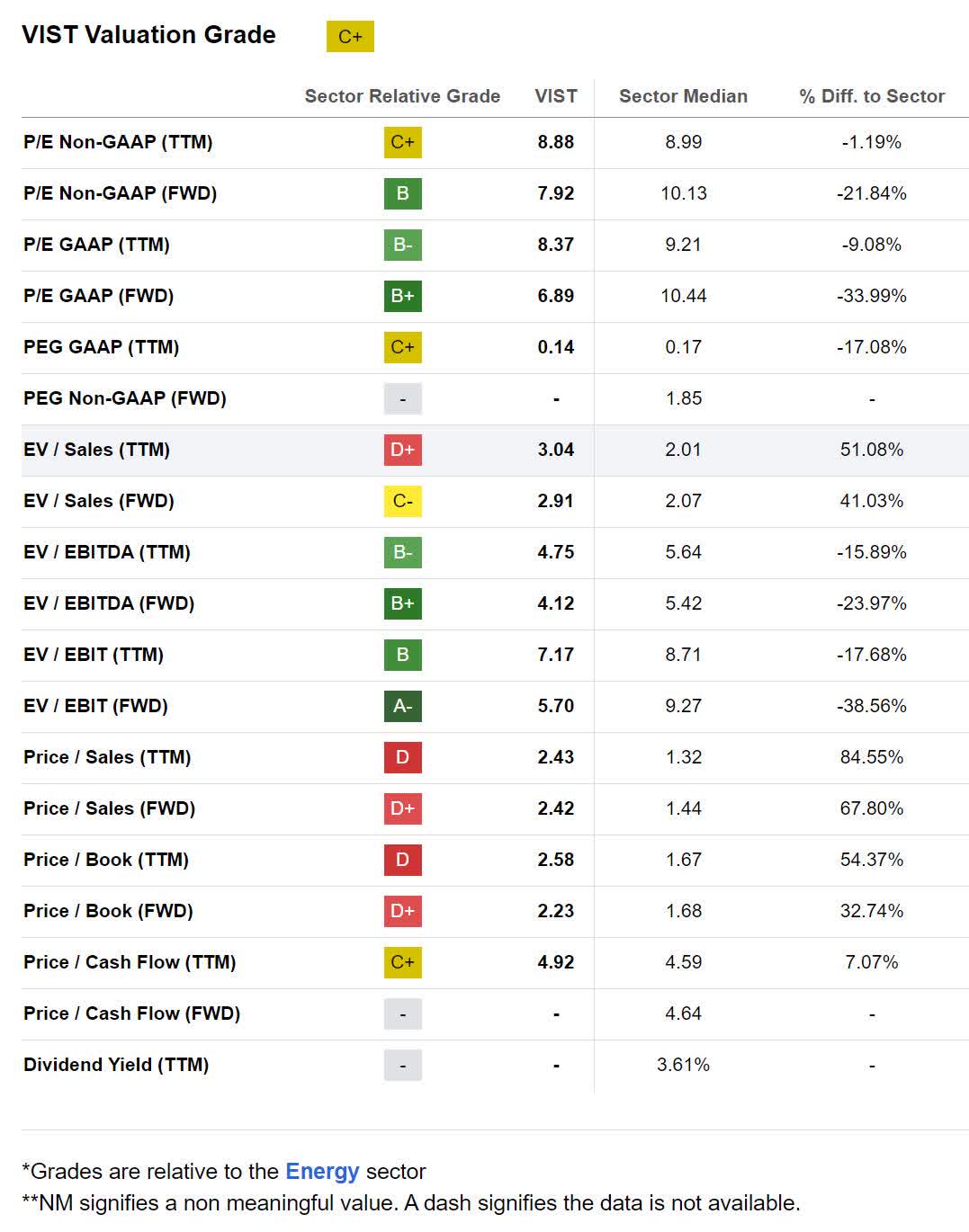

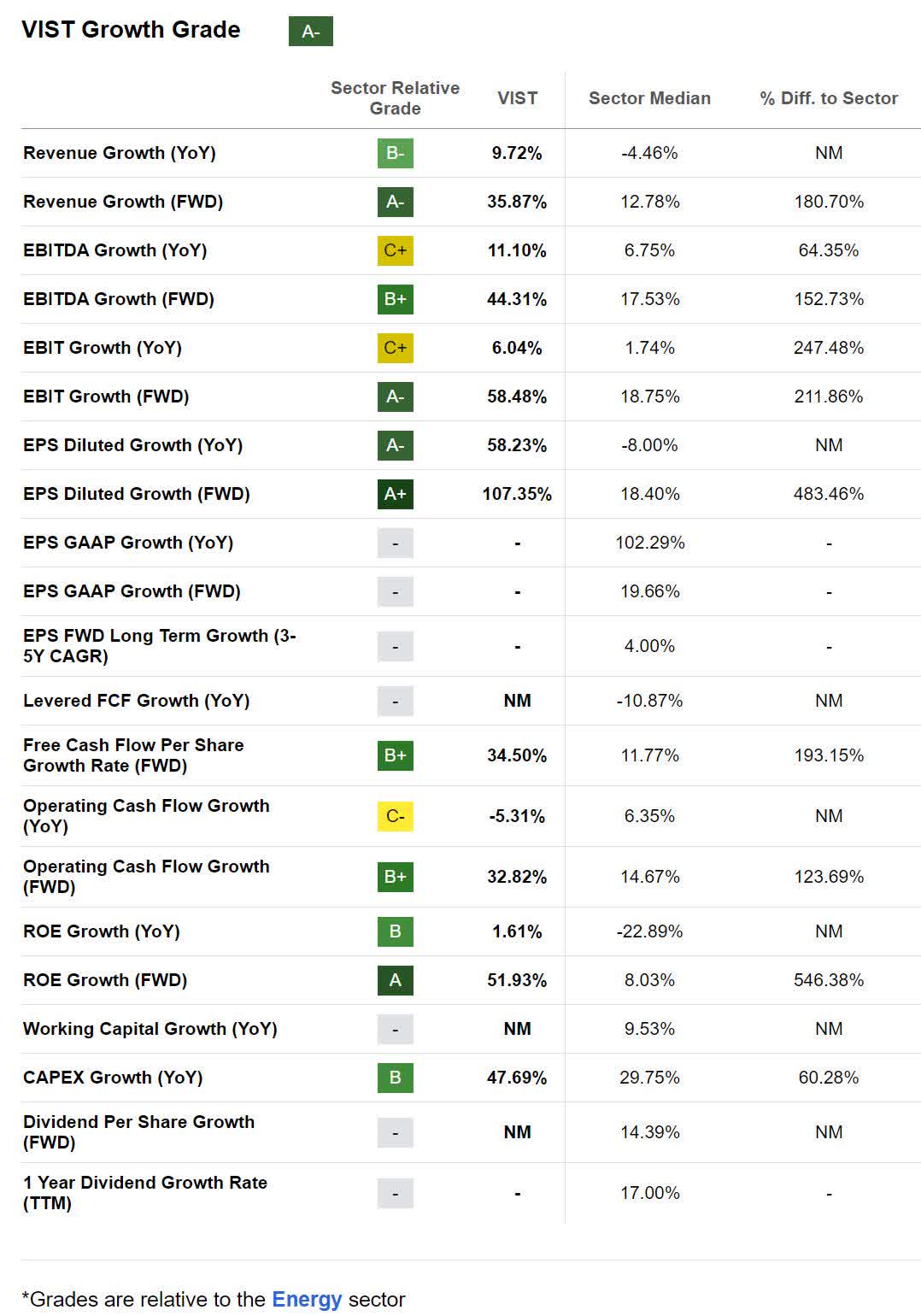

As of December 26th, 2023, Vista had a market capitalization of $2.85B and traded for $29.90 per share. They do not pay a dividend, and have a forward P/E of 6.89x. I cannot find an estimate for their EPS Long-Term CAGR, so I am instead using their the estimates for their other growth metrics . Using their forward revenue growth of 35.87% produces a PEGY estimate of 0.1921x and an inverted PEGY of 5.206x.

Using their forward EBITDA growth of 44.31% produces a PEGY estimate of 0.1555x and an inverted PEGY of 6.431x.

Using their forward EBIT growth of 58.48% produces a PEGY estimate of 0.1178x and an inverted PEGY of 8.488x.

Using their forward Free Cash Flow Per Share Growth of 34.5% produces a PEGY estimate of 0.1997x and an inverted PEGY of 5.007x.

All of these estimates imply the company is presently significantly undervalued.

{kind=link}

{kind=link}

Risks

Vista is an oil & gas producer so their topline revenue is heavily affected by changes in the prices of those commodities. Anytime the prices decline and stay low for an extended period of time, their ability to generate cash flow would be negatively affected.

Catalysts

In addition to facing a potential risk from the price of oil or gas falling, Vista also stands to benefit anytime the prices rise and then stay elevated.

As they are currently increasing their future output potential by establishing new wells, when the current phase of expansion is complete, their CapEx should shrink and their cash flow should improve.

Conclusions

Vista Energy is making progress toward completing their established goals. They have begun exporting oil and still have a significant number of additional wells they are planning on installing. While I have yet to notice any statements from management about paying a dividend, I believe they are on track to eventually begin offering one. Even if they don't plan on offering a dividend, when the current phase of expansion is complete, they will have to put their future cash flows to good use by either entering a new phase of expansion or possibly begin repurchasing shares. At the moment, this appears to be a success story in the making.

For further details see:

Vista Energy: A Success Story In The Making