VIST - Vista Energy: High Growth And Excellent Returns

2023-10-25 13:57:06 ET

Summary

- Vista Energy is a leading independent oil and gas exploration and production firm focused on shale assets in Argentina.

- The company has a strong growth trajectory, with impressive execution and a portfolio of over 205k acres and 250MMboe of proven reserves.

- Vaca Muerta offers superior well performance and attractive project economics, leading to significant value creation.

- Vista is trading at cheaper multiples than North American shale peers with lower growth and lower asset lives.

- We believe the stock offers a more than 70% return over the next 3 years.

We present our note on Vista Energy ( VIST ), a leading independent oil & gas exploration and production firm, focused on shale assets in Argentina, with a Buy rating. We are drawn by the heavy discount to NAV, production growth, and high returns on capital and we find the risk/reward attractive. We will provide an overview of the business, an analysis of the assets, shortly discuss the political backdrop, and value Vista Energy’s equity.

An overview of Vista Energy

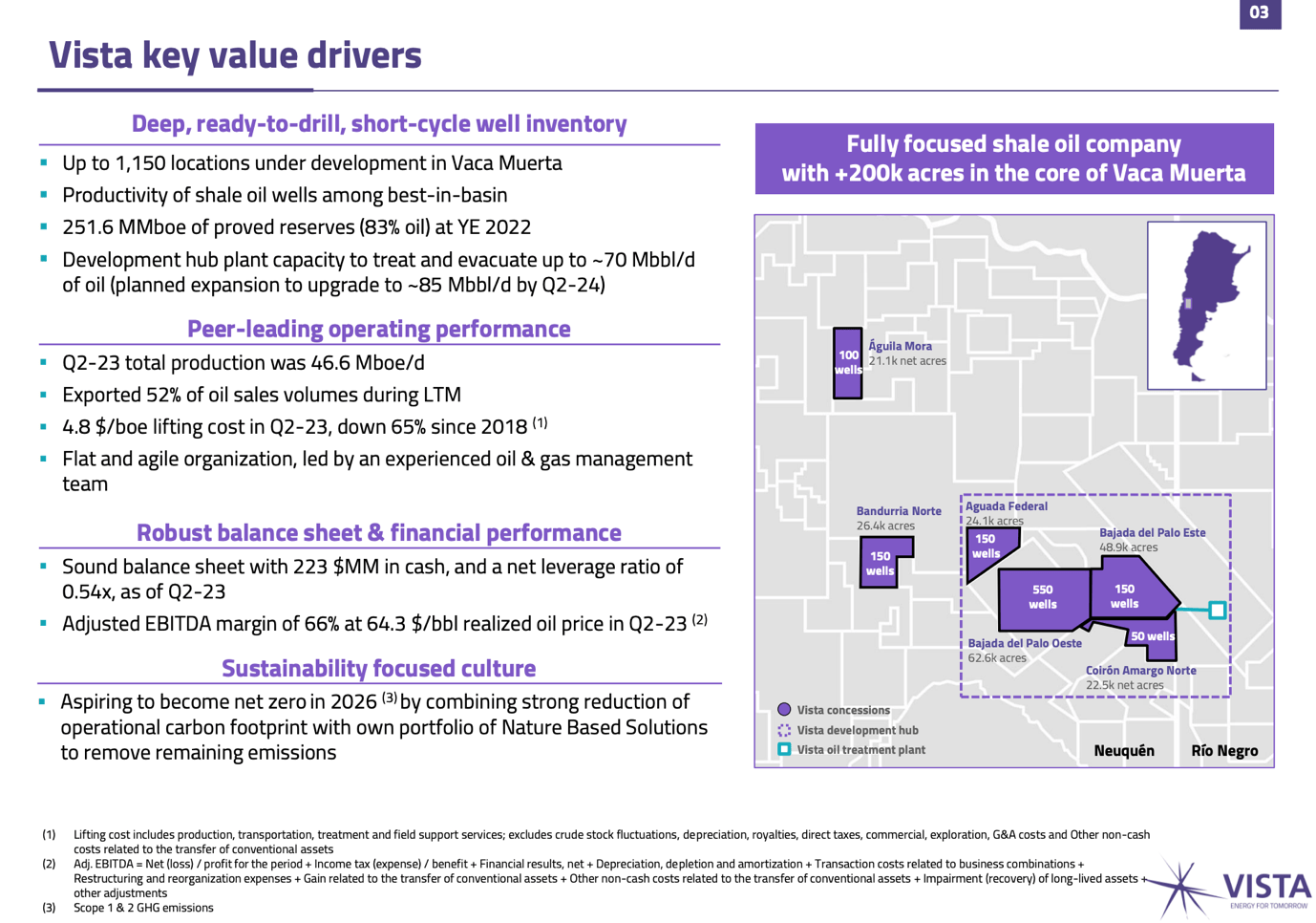

Vista Energy is an independent oil and gas operator, with shale assets in Vaca Muerta, the largest shale oil and gas play under development outside North America. The company was founded by a team of former executives of YPF – Argentina’s vertically integrated national energy company – and was initially listed as a SPAC in Mexico in 2017, and later on the NYSE in 2019. Vista has had a strong growth trajectory with impressive execution and is currently a leading independent operator in Vaca Muerta with a portfolio of more than 205k acres, 250MMboe of proven reserves, and a daily production of more than 55 kboe. The company is particularly focused on achieving cost efficiencies and reducing carbon intensity. In addition, Vista has a smaller presence in Mexico, with a 100% interest in a contract for a block in the Macuspana basin. The company has a current market capitalization of $2.7 billion.

{kind=link}

Vista's Investor Presentation - October 2023

Vaca Muerta and Vista’s targets

Vaca Muerta is a geologic formation located in Northern Patagonia, Argentina, and is a host rock for major shale oil and shale gas deposits. The significant oil discovery was made by Repsol-YPF in 2010, and shares many features of the best Permian basin assets in terms of content, pressure, etc. This is reflected in superior well performance and attractive project economics.

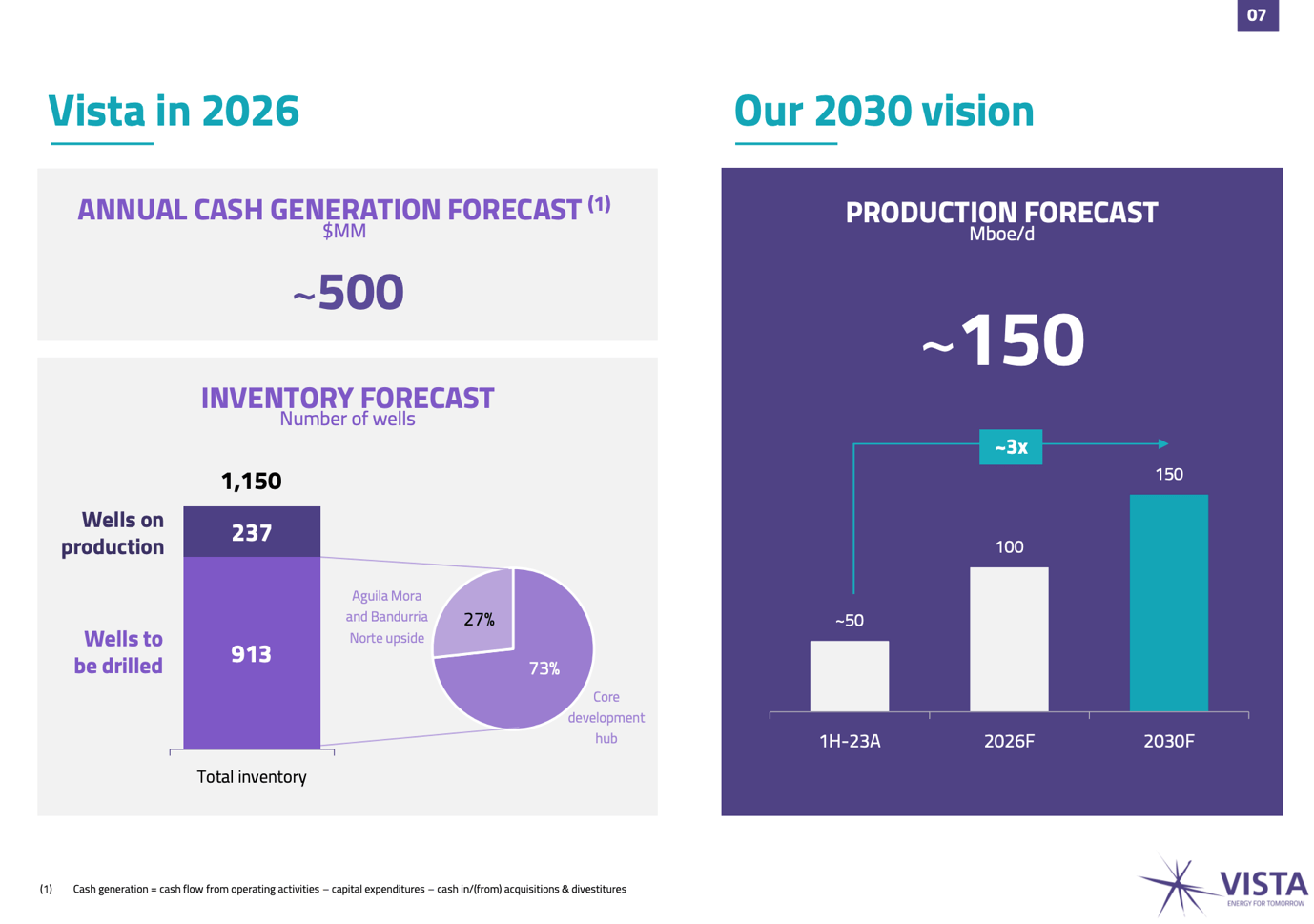

Vista has a long-term concession expiring after 2050+, consisting of more than 1150 well locations in Vaca Muerta, out of which 27% are in production and 73% are to be drilled. After removing major bottlenecks including the evacuation and treatment capacity, by 2026, Vista aims to almost double production to ~ 100 kboe/day (going up to 150 kboe/day in 2030), double adjusted EBITDA to $1.7 billion, and achieve an annual cash generation of $500 million. Lifting costs are forecasted to be low at just $5/ bbl . and capex at $10/ bbl ., leading to superior project economics, IRRs as high as 100%, and massive value creation given the 20+ years of remaining inventory.

{kind=link}

Vista's Investor Presentation - October 2023

Political support

Both main political factors in Argentina (the Peronist government and the opposition) are supportive of Vaca Muerta despite general political uncertainty. Vaca Muerta plays an important role in the Argentinian economy as the country is highly dependent on hydrocarbons and has a massive trade deficit and hence needs to obtain significant dollar flows. Both Mr. Massa and Mr. Milei, who will face off in the second round of the presidential elections in November, have expressed their support for the development of Vaca Muerta, mitigating the political risk of investing in Vista’s equity.

Valuation and investment recommendation

We value Vista Energy using forward FCF yields, NAV analysis, and an EV/EBITDA multiples analysis. In line with sell-side analyst consensus, we forecast $1.7 billion of sales and $1.2 billion of EBITDA in FY2024, and we are in line with Vista’s expectations for FY2026. We applaud Vista’s management execution and would like to point out the over-delivery of previously announced targets, which has also been reflected in the impressive performance of the equity (3x+ since listing).

The current market value implies a forward EV/EBITDA ratio of just 2.8x and an EV/EBITDA 2026e (not taking into account EV changes) of 1.9x. We believe this is excessively low given the production profile, growth runway, and underlying asset returns, and does not reflect the true value of Vista. North American shale peers with much lower growth and inferior returns trade at ~5x EBITDA. We believe there should be a lower multiple for Vista given the location of the assets and associated risks vs. American peers, however, the current valuation reflects little to no growth and poor execution of the targets. We value Vista at an exit multiple of 3x 2026e EBITDA (due to visibility) and discount to the present using a 10% discount rate (12% cost of capital – 2% growth rate). We arrive at an EV of $5.1 billion and an equity value of $4.7 billion in FY2026, discounted to $3.5 billion today implying 30% upside today or a share price of $40. Alternatively, this can be translated to a 75% return over three years.

We also value Vista using FCF yields, by discounting an FCF of $500 million by a target FCF yield of 10% (see explanation above) and arriving at an EV of $5 billion. This methodology effectively produces a valuation in line with EV/EBITDA ratios and implies returns over 70% in a 3-year time frame. Given the long duration of the concession and long asset life, an NAV approach produces similar valuations, implying a heavy current discount to NAV.

We believe Vista Energy represents one of the most attractive opportunities in the shale E&P space.

Risks

Risks include but are not limited to weaker macroeconomic conditions, lower than expected oil and gas prices resulting in lower earnings, political instability, unfavorable legal and regulatory changes, excess profit taxes, higher than expected capital expenditure leading to lower returns, delays in production, worse than expected operational performance, higher than expected operational costs, misallocation of capital, accidents, and weather events.

Conclusion

We see an attractive risk/reward situation with various upcoming catalysts, and we recommend buying Vista Energy shares.

For further details see:

Vista Energy: High Growth And Excellent Returns