VIVHY - Vivendi SE: Analysis Signals It's Overpriced Practice Patience

Summary

- Vivendi shows good results from its 2nd biggest revenue generator but is flat on Canal+.

- It has the potential to boost revenue further if the acquisition of Lagardère is approved by the European Commission.

- Financials and valuation models point to overvaluation and uncertainty in the EU economy calls for patience.

Investment Thesis

Vivendi SE ( VIVHY ) is about to report FY22 earnings, so I decided to have a look at France's media giant to see if there is any opportunity for a long-term investment. With growth estimates provided by analysts, my growth estimates are a bit more optimistic, yet the company is still trading at a premium and would not be a great investment right now.

I will go through some assumptions on the revenues that the company is producing and will try to come up with some reasonable growth numbers that I can see by analyzing previous financial reports and any upcoming catalysts that can propel this growth further.

Revenue Potential

In the most recent years, the growth has not been particularly high, with the main revenue generator, Canal+ growing at around 0%-1%, and it seems to have penetrated most of the market by now. Havas Group on the other hand has been growing low double digits and can become a major contributor of revenues in the future. For my DCF valuation, I have separated Havas Group into its own category as I wanted to model higher growth for this segment than the rest of the business segments. Over 60% of total revenues come from Canal+, so I pooled all the other revenues into Canal+ as they would not make as big of an impact as Havas Group.

Havas Group is a major player in the advertising space globally and I believe it will continue its growth at a similar pace in the future years as the company acquires more to add to its portfolio of assets. In the first half of 2022, they acquired majority interests in five different businesses, Tinkle, Inviqa, Search Laboratory, Frontier Australia, and Front Networks. These acquisitions will keep boosting its revenue growth in the future years. This is the reason why I decided to go with slightly higher revenue growth estimates for the future than the growth estimates I gave to the main revenue segment which includes the rest of the business segments with Canal+.

Other notable segments that either grew quite considerably or managed to lose their market share over time are Gameloft, which grew around 48% q-o-q and low double digits in the first 9 months of 2022, and Editis which has been declining in recent times in low single digits will be fully sold by Vivendi to finance the acquisition of Lagardère, a French media group. Currently, the company owns over 55% of the Lagardère. Vivendi is currently running into anti-competition issues with the European Commission as they believe if Vivendi acquires Lagarde, there will be less competition in the book publishing market in France and less diversity.

Lagardère

Let’s look at Lagardère’s financial situation and how it can help Vivendi in the future. Lagardère recently announced its FY22 results, and the numbers were excellent. The company makes almost €7B in revenue, 35% y-o-y increase, and operating margins have also improved. There are many synergies for Vivendi if they are to acquire Lagardère and the management seems very optimistic about the future, especially in the travel segment which has recovered considerably.

There could be potential synergies between Vivendi's existing businesses and Lagardère Travel Retail's operations. For example, Vivendi could use its expertise in content creation and distribution to enhance the in-store experience for travelers, such as by offering exclusive music, films, or books. Lagardère Travel Retail segment went from -€81m to +€136m EBIT as the pandemic has eased all around Europe and all restrictions have been lifted. Lagardère recently completed its acquisition of Marché International which primarily operates within travel and leisure locations, such as airports, train stations, and zoos. The acquisition further cements its strategic ambition to become the top name in this segment. This type of synergy may not be the main one for Vivendi, but it could also be a good way to diversify its portfolio a little more. Vivendi and Lagardère both stand to benefit if the acquisition happens in the next 12 months and could propel Vivendi’s revenue growth further.

Financials

With no-so-exciting revenue potential as of right now, let’s have a look at how the company is being managed.

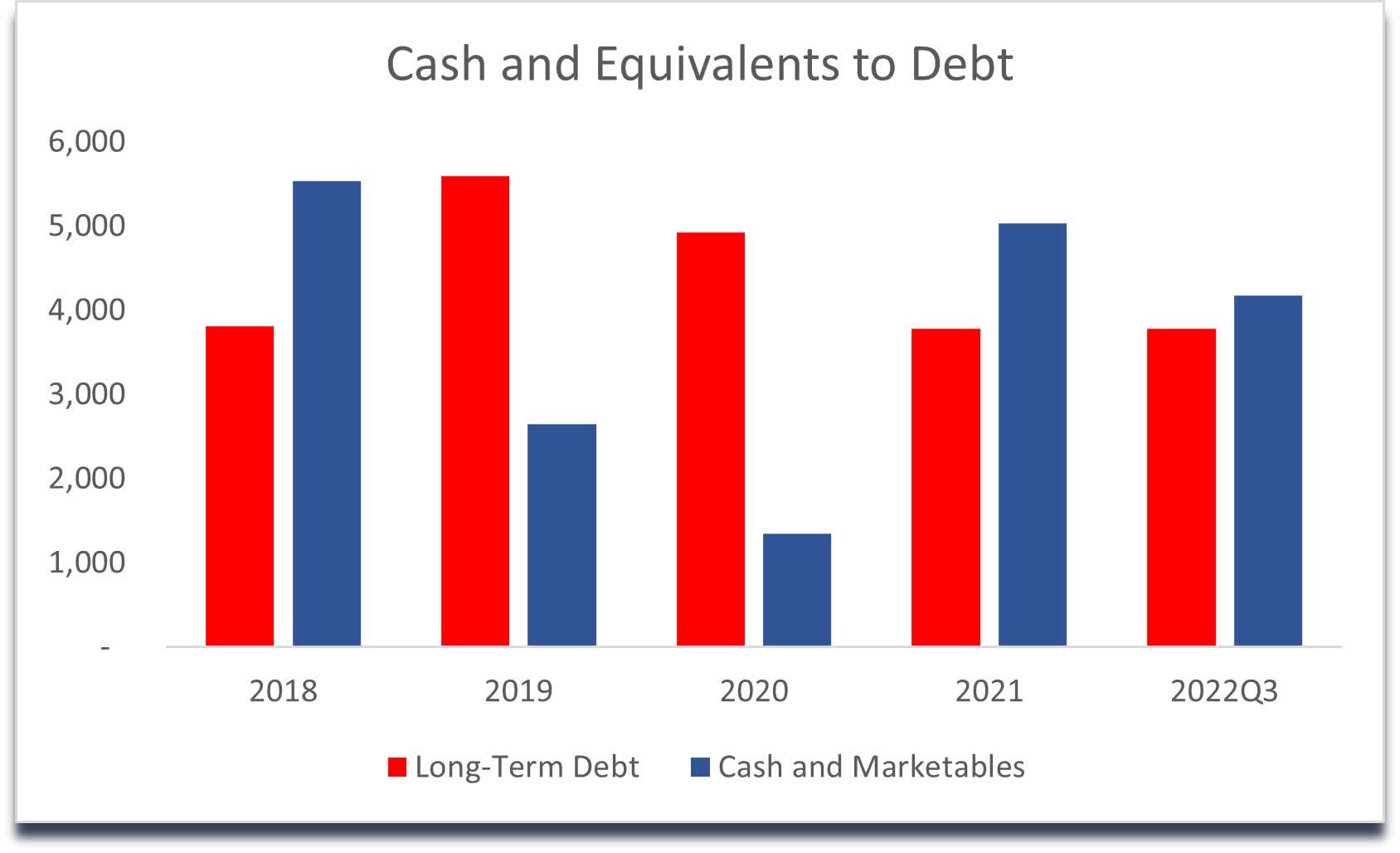

Cash and equivalents have been improving against the long-term debt of the company. During 2019 and 2020 it looked a bit worrying, however, Vivendi has been paying down debt while keeping its liquidity in check. They do not seem to have trouble covering their interest expenses on debt as the ratio sits around 5.0 right now.

{kind=link}

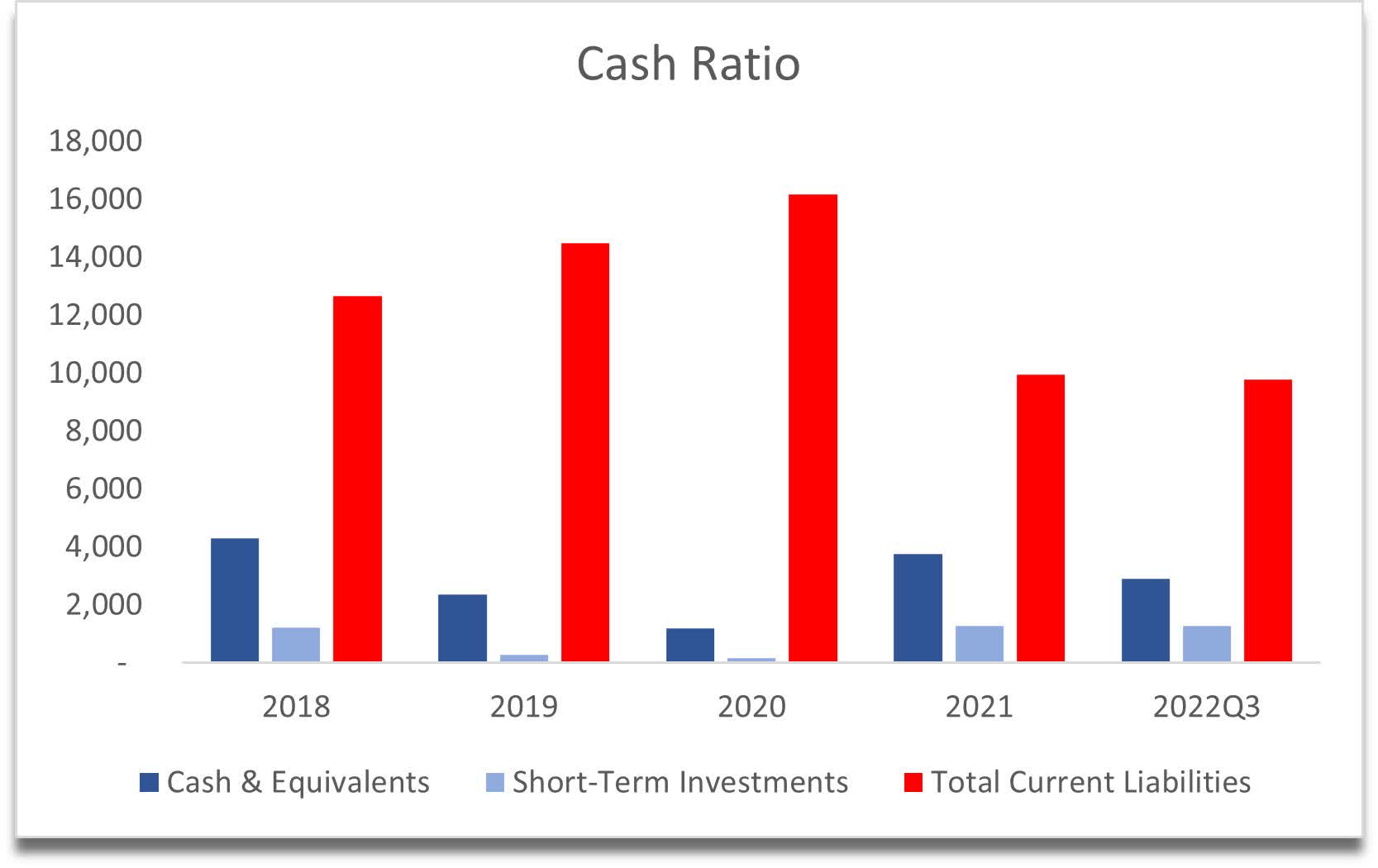

The cash ratio is not looking good here. I like companies that can cover their short-term obligations with the available cash on hand, however, it is just another more scrutinizing metric that investors like to use, and it does not mean that the company is in any danger of defaulting.

{kind=link}

Return on invested capital is also nothing outstanding, fluctuating at mid-single digits.

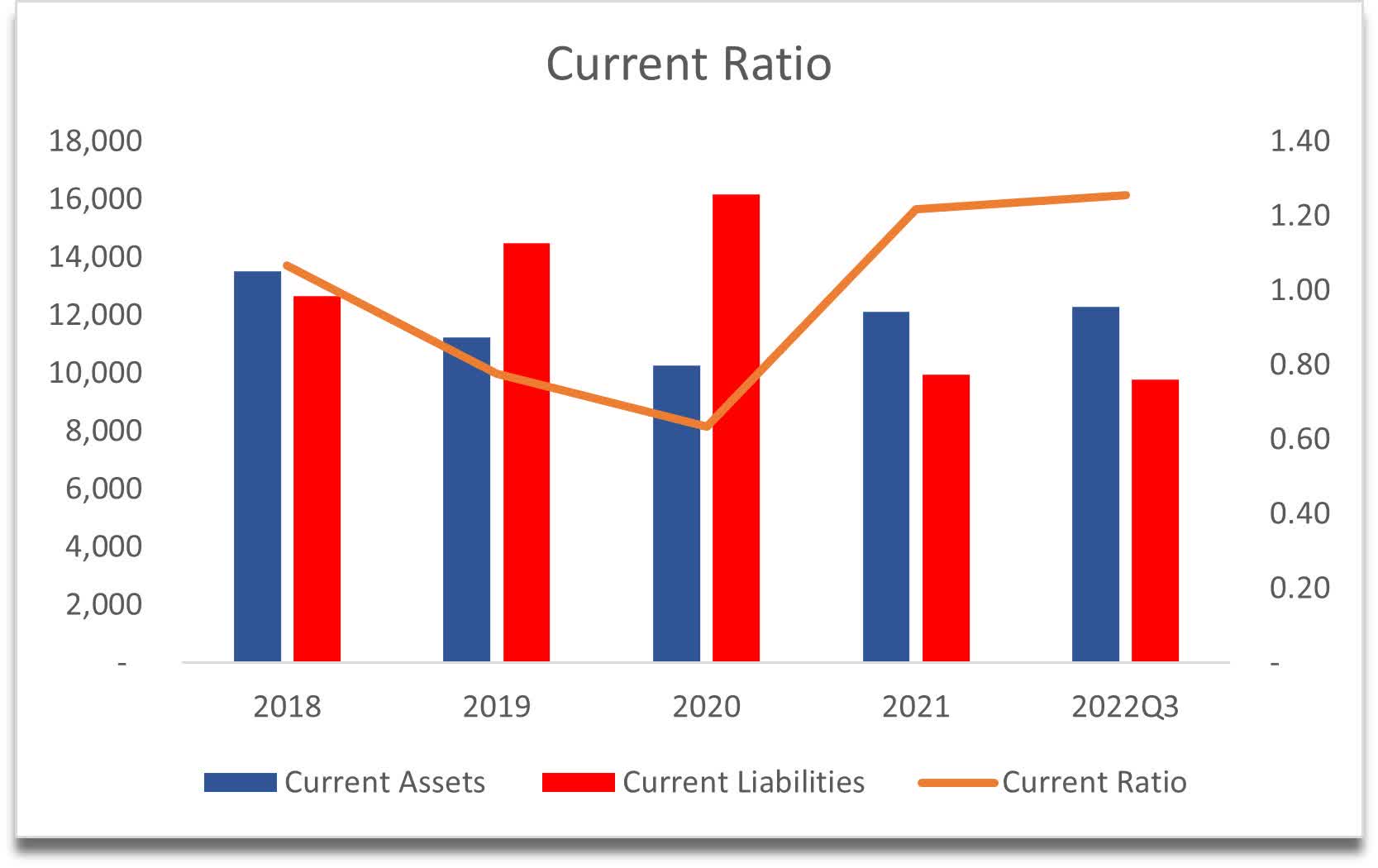

The current ratio is around 1, which is also nothing to write home about, with more recent years ticking up a little bit.

{kind=link}

Overall, the books have left me with a lot to be desired, and at this point, it may look like the company might be overvalued at a 20x forward P/E ratio (according to Seeking Alpha). With such growth prospects, I believe 20x forward P/E is a bit high for what the company can produce. I would also like to see an improvement in the above financial metrics.

DCF Valuation

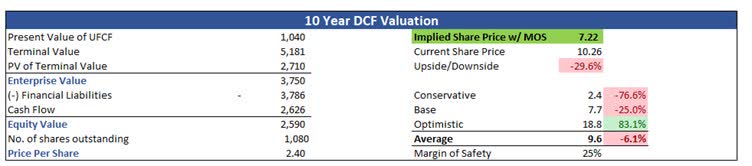

With the above-mentioned growth prospects, I have no reason to believe that the company could achieve high double-digit growth over the next 10 years. Analysts are saying that the company will grow at around 2%+ in the next couple of years, however, I am not that pessimistic, and I have modeled the growth of Canal+ and other revenue excl. Havas Group at an average of 6% per year and revenue for Havas Group at an average of 8% per year in the base case scenario. The percentage growth in revenues is modeled in US terms as are all the figures in US$. Havas Group has grown in low-double digits in Euro, however, since the deterioration of the currency against the US$, the growth has been smaller.

I also modeled the worst-case scenario where I took 2% off from the base case and an optimistic case where I added 2% to the base case. Total revenue in the base case average is 7%, 9% in the optimistic, and 5% in the worst-case scenario. Now since these numbers are just my estimates and will vary from other valuation analyses on the website, and I like to give myself a good margin of safety of 25% to the final implied share price to account for any wrong estimations in my assumptions.

The implied share price with a 25% margin of safety comes to $7.22 per share, meaning around a 30% downside to the current price of the stock.

{kind=link}

Dividend Model

Since the company has been paying some dividends over the last few years, I decided to do a dividend valuation model as well. Excluding the special dividend it gave to its shareholders in 2021, the dividend has dropped by around 60% bringing it to around 26 cents a share. If I assume that the company is going to be able to increase its dividend by 5% in perpetuity, the price per share sits at $9.4, and if I apply a 25% MoS here too, I get $7.03 per share.

Closing Remarks

Have I beaten down the stock too much in my models? Maybe, however, there is a lot of uncertainty still in the world. The inflation rate in Europe still sitting at 8.6%, which is only slightly down from last month. The Ukrainian crisis is still ongoing after a whole year. These sorts of uncertainties make me a bit more pessimistic, no matter how well the company looks in the long run, in the short run, macroeconomic worries will affect every stock market out there, and I would rather practice patience than jump in and buy at the wrong time. Until we see the full year's results and how the global events unfold in the next couple of months, I suggest a sell for now if you believe my growth prospects for the company are justified. I have it on my watchlist, and price alerts are much lower than what the company currently trading at.

For further details see:

Vivendi SE: Analysis Signals It's Overpriced, Practice Patience