VZIO - VIZIO: Wait For A Dip

2023-04-04 07:14:17 ET

Summary

- VIZIO is in the early growth phase to expand its user base. The connected TV ad spending is still on the rise at a high rate.

- Management's guidance suggests a more competitive environment in Q12023 as it indicated further gross margin compression in the platform+ segment.

- The company does not have a strong market position, and the potential upside return of VZIO stock is not high enough to offset the downside risk from the competition.

Investment thesis

Our analysis below suggests that:

The company is in the early growth phase to expand its user base. The connected TV ad spending is still on the rise at a high rate.

However, management's guidance suggests a more competitive environment in Q12023 as it indicated further gross margin compression in the platform+ segment.

Thus, considering the risks and rewards potential, we do not think the stock is currently attractive as we think our base and bull case probabilities are 50/50. Given the company does not have a strong market position, and the potential upside return of the stock is not high enough to offset the downside risk from the competition, we rate this stock as neutral.

Company profile

VIZIO (VZIO) was founded in 2002 and its mission is to deliver immersive entertainment and compelling lifestyle enhancements that make our products the center of the connected home.

The company operates two businesses: Device and Platform+.

- Device: They sell smart TVs and sound bars, through retailers, distributors, and direct-to-consumer channels in the U.S.

- Platform+: It sells ads through its SmartCast platform and data through Inscape technology.

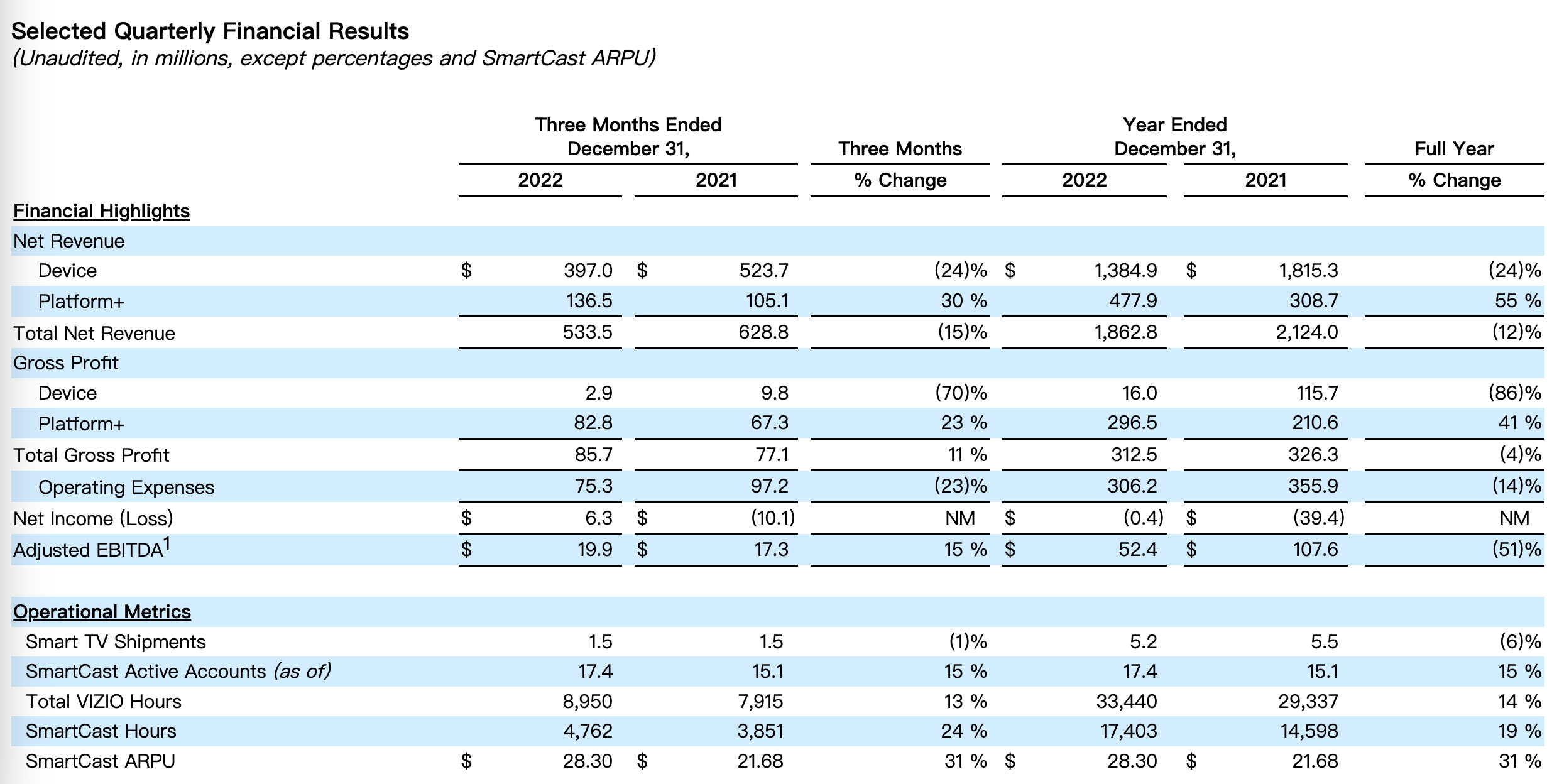

The company generated $1.8 billion in revenues and adjusted EBITDA of $52 million in 2022. They sold 5.2 million TV units in 2022 and had 17.4 million SmartCast active accounts as of Dec 2022.

{kind=link}

Key takeaways from the Q4 2022 earnings:

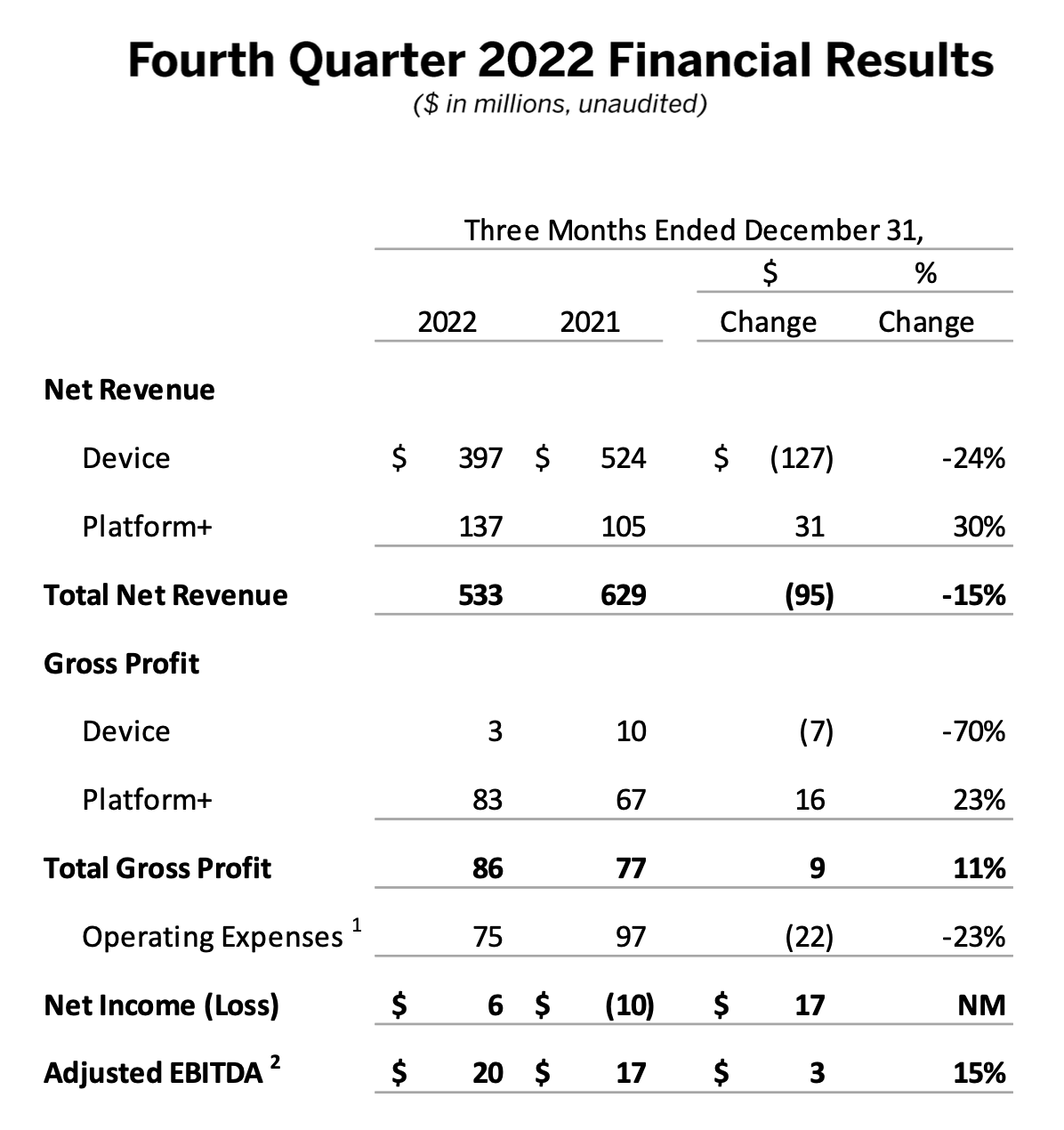

In Q4022, its revenue declined 15%in the yoy and gross profit grew 11% yoy and adjusted EBITDA grew 15%.

{kind=link}

The company expected platform+ revenue to grow at 14% with a 58.6% gross margin. Total adjusted EBITDA in the range of flat to positive $5 million. The management saw a flattish environment in the TV market in 2023. Thus, they will be focusing on cost control this year.

{kind=link}

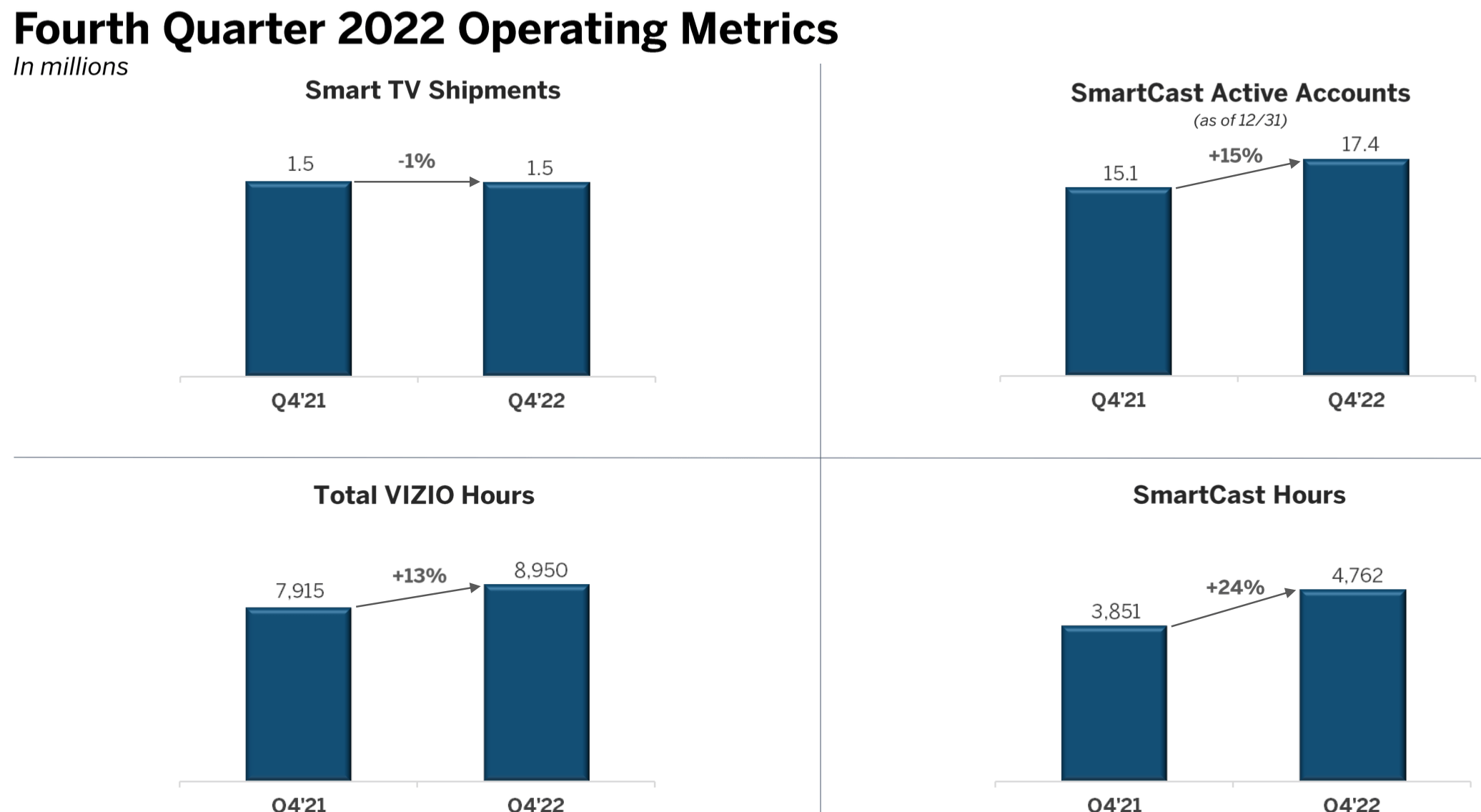

Smart TV shipments decreased 1% yoy, SmartCast active accounts grew 15% yoy, and SmartCast hours increased 24% yoy in Q42022.

{kind=link}

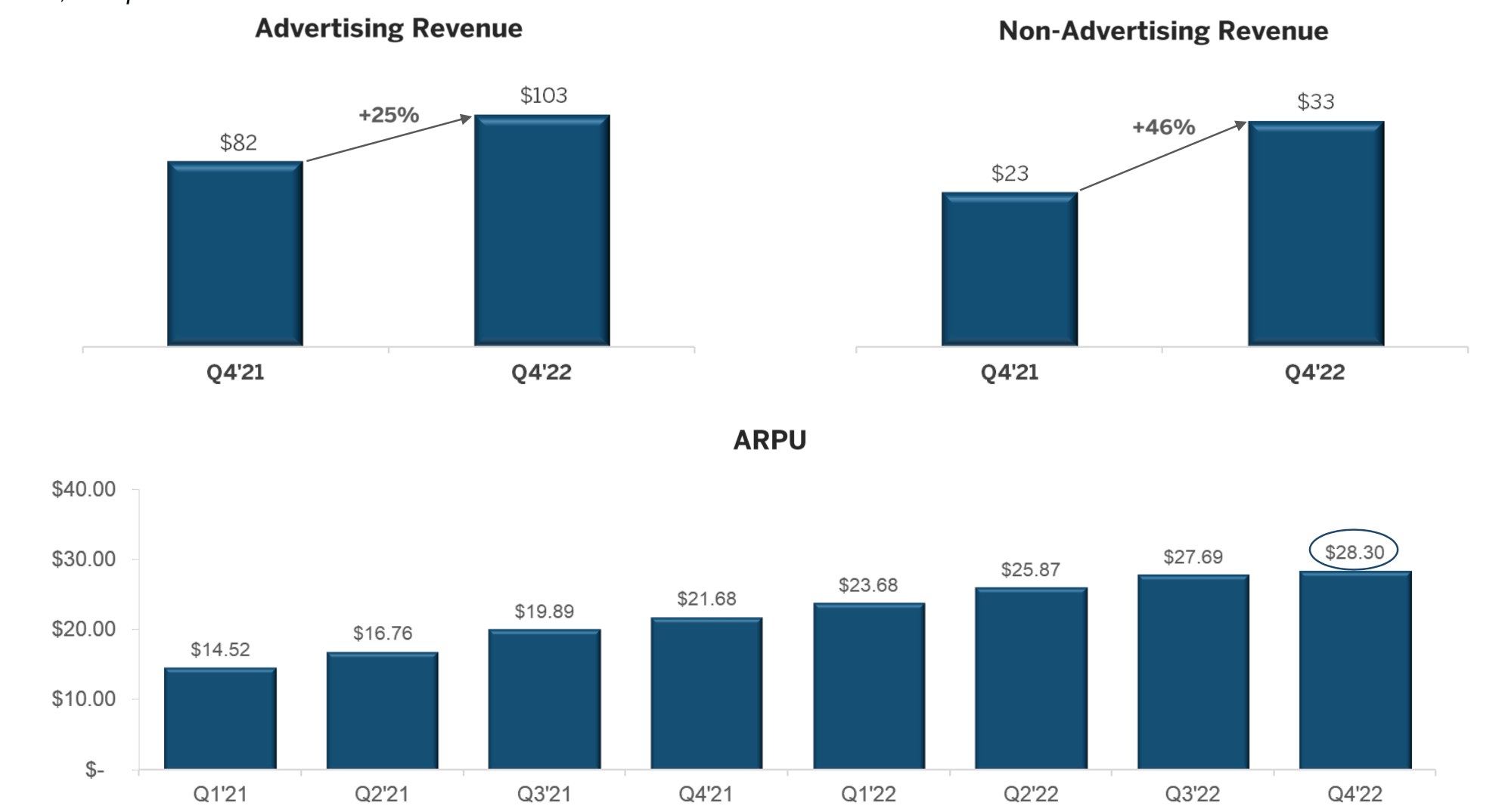

In the platform+ segment, the Ads and non-ads revenues grew by 25% and 46% in Q42022. ARPU was $28.3 for the quarter.

We have the following comments regarding the Q4 performance:

1. Management's guidance suggests a more competitive environment in Q12023 as it indicated further gross margin compression in the platform+ segment.

2. Vizio's device gross margin is slightly above zero in 2022, while Roku, a larger peer, has already started to sell devices with negative margins. Vizio continued to grow its SmartCast users and this could improve its competitiveness in the mature TV market.

3. Its user engagement continued to grow. SmartCast hours per active account increased from 2.63 hours to 2.74 hours in Q42022. Its ARPU was at $28.3 while ROKU was at $41.6. This implies there is room for growth in its platform+ segment.

4. Device unit sales grew flat in the quarter and a huge improvement from down 15% in Q32022. Based on data from CTA , the U.S. TV market was in decline since 2020 due to the ease of COVID. The good news is that it seems the company still gained market share in 2022 despite a challenging environment.

{kind=link}

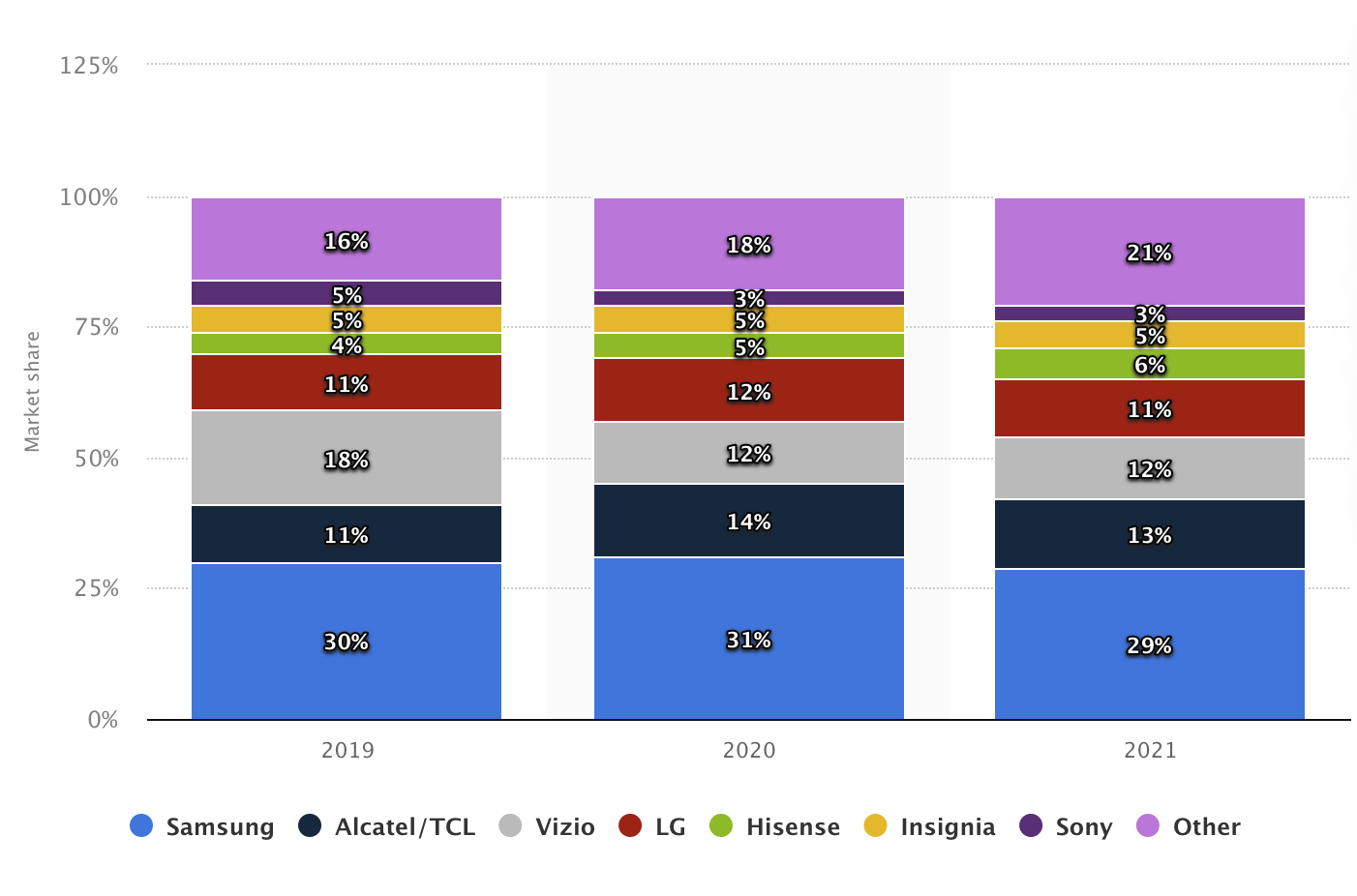

The company relies significantly on Taiwanese suppliers and does not have a strong market position

The company competed with Samsung, TCL, LG, Sony, Hisense, and Insignia in the TV segment. It ranked 4 in market share in 2021. We consider it to have weak pricing power given the TV market is really mature and the #4 rank is relatively behind.

{kind=link}

In addition, the company heavily relied on 4 suppliers, 56% purchased from related parties. It is not too hard to guess the related party is Hung Hai Technology (TWSE:2317) and AmTran Technology (TWSE:2489). The company was supported by its shareholders, a group of Taiwanese manufacturers, to compete with Korean, Japanese, and Chinese manufacturers. It's hard to say whether the company has an advantage over its peer but this relationship definitely gives the company extra support to compete with standalone peers such as Roku.

{kind=link}

DCF model analysis and Catalysts

Base case

We make the following assumptions based on management's guidance and current market conditions:

- 20 % WACC

- 3 % terminal growth rate

- 5% free cash flow margin

- Net debt -346 million (Q42022)

- Outstanding shares 202 million (Q42022)

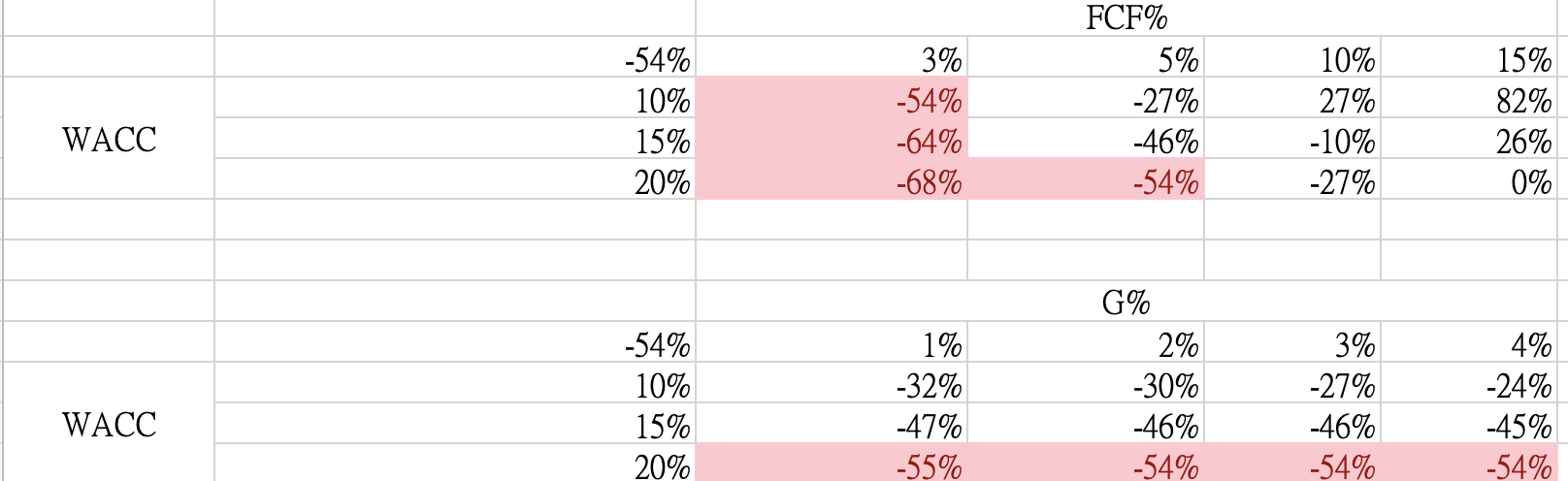

Applying the DCF method, we can arrive at an equity value of 961 million ($4.7 per share), which implies a 48% decline from the current stock price.

With the sensitivity test below, we can see that the stock is undervalued only if the WACC dropped to the 10-15% range, its free cash flow margin rises above 5% or the terminal growth rate assumption rises above 4%.

In this scenario, it requires catalysts such as the fed starting to lower the rate, its platform+ business continuing to impress, or its TV segment grabbing market shares. We think given the management focuses on cost-cutting at the moment, there could be some upside in margin improvement but unlikely to hit the 10% or above level. So the stock is not really contractive in our base case analysis.

{kind=link}

Bull case

We consider its long-term TV market share potential and upside for its platform+ business:

- Maintain annual 5 million TV unit sales in the next 10 years and its SmartCast users grow at 2 million per year

- ARPU to grow to $50 in 10 year

- 20 % WACC

- 3 % terminal growth rate

- 20% Platform+ EBITDA margin

- Net debt -346 million (Q42022)

- Outstanding shares 202 million (Q42022)

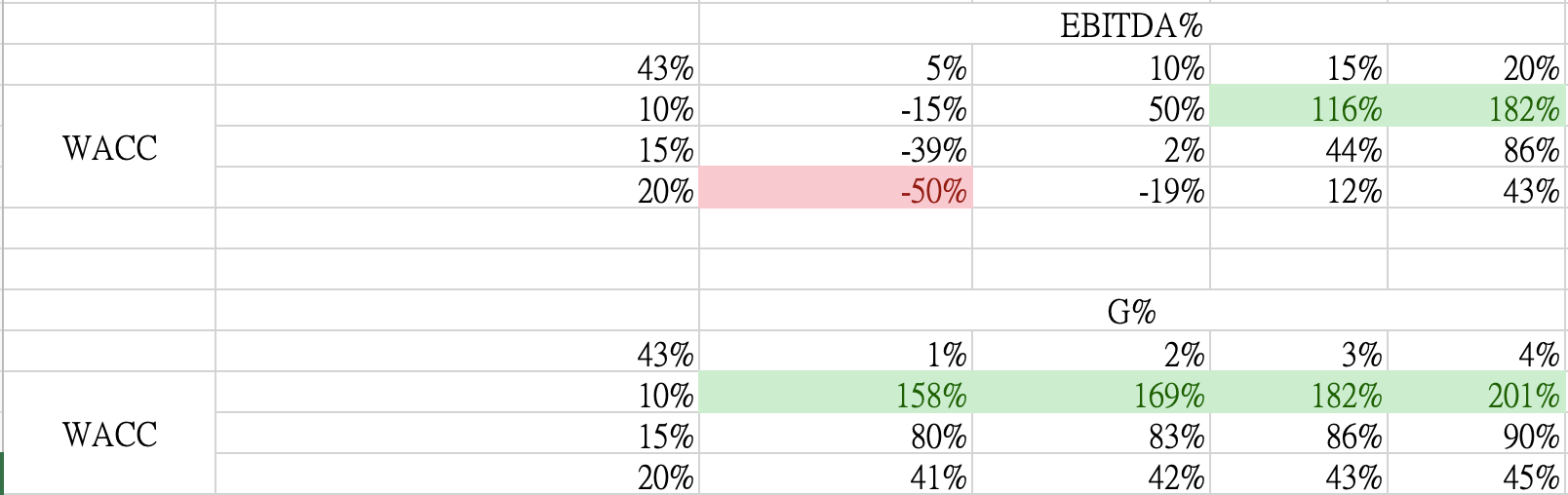

Applying the DCF method, we can arrive at an equity value of 2,666 million ($13.2 per share), which implies a 43% increase from the current stock price.

With the sensitivity test below, we can see that the stock is overvalued only if its EBITDA margin fails to stay above 10%. The catalyst for the bull case is obviously the continue grow in ARPU and its user base. On the other hand, the U.S. connected TV ad spending is still growing at a high rate. Multiple research sources( Grandview research , eMarketer ) indicate high single-digit to low teen growth for the next 5 years. We think the bull case scenario is likely given the market potential and that the company is still in the early stage to grow its user base.

{kind=link}

However, considering the risks and rewards potential, we do not think the stock is currently attractive as we think our base and bull case probabilities are 50/50. Given the company does not have a strong market position, and the potential upside return of the stock is not high enough to offset the downside risk from the competition, we rate this stock as neutral.

For further details see:

VIZIO: Wait For A Dip