BMWYY - Volkswagen: Don't Chase The 8.2% Yield

2023-09-08 12:15:13 ET

Summary

- Volkswagen has consistently lagged behind its industry peers in total returns over the past decade.

- Economic challenges in China, high interest rates affecting the demand for vehicle financing in Europe and the US, Germany's PMI contraction, create a perfect storm of negative events.

- VW's profit margins are the worst among its peers, and it employs far more people than its peers. This puts its future profitability in jeopardy unless there's a paradigm shift.

- The company's attractive 8.2% dividend yield is overshadowed by the expected capital depreciation, leading to negative overall returns.

Investment Thesis

Let me begin this article by expressing my admiration for Volkswagen's ( VWAGY ) ( VLKAF ) ( VWAPY ) ( VLKPF ) remarkable achievements over the past century, both as a brand and as a group. Volkswagen has evolved into a prominent and highly successful automaker, offering iconic vehicles like the Beetle to the market. Its role as a European conglomerate automaker is unparalleled, consistently providing reliable vehicles that have played a significant role in reshaping the continent.

I may have a certain bias as a European, having had the privilege of driving VW and Skoda vehicles from their portfolio, which have served my family exceptionally well. This personal connection is another reason why I feel a sense of sadness seeing the company's current trajectory, no longer resembling the powerhouse it once was and facing potential challenges in the future.

For those who are not well-acquainted with the automotive industry , it's essential to understand that Volkswagen is not just an individual brand; it plays a pivotal role in the expansive Volkswagen Group, a conglomerate with a diverse array of brands, each possessing its distinct identity and product offerings. This extensive range of brands within the group caters to various market segments and consumer preferences. From luxurious and high-performance options such as Lamborghini, Bentley and Bugatti to more practical and accessible vehicles under the Audi, VW, Seat, and Skoda banners, there's a vehicle tailored to every type of driver. Notably, Porsche ( POAHY ), which was once part of this brand portfolio, was spun off in 2022.

{kind=link}

Brand Map (VW Website)

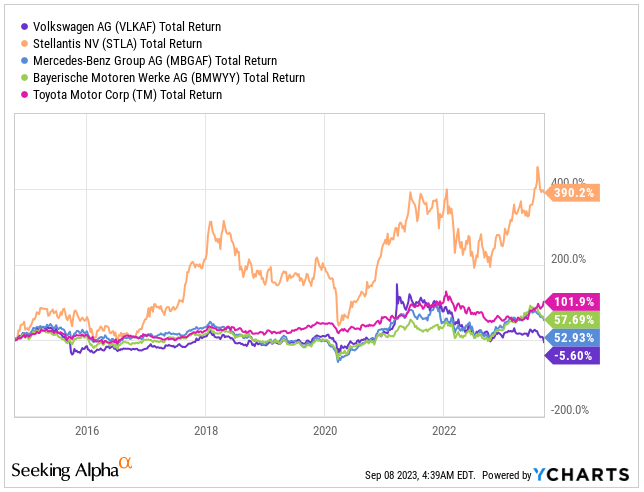

Over the span of last 8 years, the total return of Volkswagen has been significantly underperforming that of its peers. While companies such as Stellantis ( STLA ), Mercedes-Benz ( MBGAF ), BMW ( BMWYY ) and Toyota Motor ( TM ) were enjoying relatively solid returns, however, in most instances with the exception of Buffet's pick Stellantis, still underperforming the S&P 500 ( SPY ) by a large margin which over the same period delivered a total return of 178.6%.

I anticipate that this trend of underperformance is poised to persist, and investors would be better off considering alternative options. They might find more attractive prospects among the other mentioned automakers or even opt for index funds like SPY. My rationale for this recommendation stems from several key factors:

Firstly, Volkswagen faces a potentially precarious situation in one of its largest markets, due to the substantial economic challenges present in China. Additionally, there's the ongoing concern of persistent inflation in the United States and Europe, which, from my perspective, is likely to result in an extended period of elevated interest rates. This, in turn, would lead to heightened financing costs for vehicles and exert pressure on people's disposable incomes, potentially reducing the demand for new vehicles in the near-term.

Furthermore, Volkswagen historically operates with very tight profit margins, and if additional commodity price pressures emerge, these margins could further deteriorate. This scenario might either push their profitability into negative territory or necessitate further price increases, which could particularly impact its value-oriented offerings, which form the core of their business.

{kind=link}

VW Performance vs. Peers (Seeking Alpha / YCHARTS)

At the start of this year, I had a significant position, constituting around 3.5% of my portfolio, which I later sold for roughly break-even price €155 ($166). This choice followed a span of several years during which the capital appreciation remained relatively stagnant. Nevertheless, it's essential to highlight that throughout this period, I consistently enjoyed a compelling dividend yield, which has recently exceeded 8.2%.

China's economic challenges will pressure Volkswagen's performance

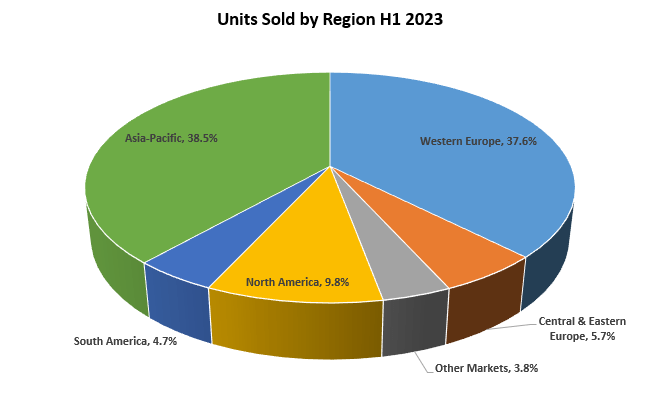

I want to kick-off the topic of economical challenges by one of its largest markets which is Asia-Pacific by units sold, from which China represents roughly 90% of Sales so far in H1 2023. At the same time, this region is viewed as a main engine for growth in the coming decade for the company, however there are many challenges at the moment.

{kind=link}

Unit Sales by Region (Author's Graph (Data VW IR))

Since the end of COVID-19 pandemic, China has been grappling with an array of challenges, both structural and otherwise. These include diminishing productivity, a declining labor force, technology restrictions imposed by countries like the United States, Japan and Netherlands, a necessary correction of the real estate bubble, elevated unemployment among younger workers, and a leadership that appears to prioritize party control and national security over economic growth. These multifaceted issues imply that China's growth trajectory will not return to the remarkable pace witnessed between 1980 and 2010 when annual growth averaged nearly 10%.

Lack of resolute measures to stimulate domestic demand, coupled with concerns of economic contagion, have led to a fresh round of growth downgrades. Several major investment banks have revised their China economic growth forecasts to below 5%. This stands in stark contrast to the global financial crisis of 2008, when China implemented the world's largest stimulus package and emerged as the first major economy to rebound from the crisis. It's also a reversal from the early days of the pandemic when China, as the only major developed economy to avoid a recession, was seen as a global economic stabilizer.

What does this mean automotive industry, and how concerning should it be to the largest European automaker?

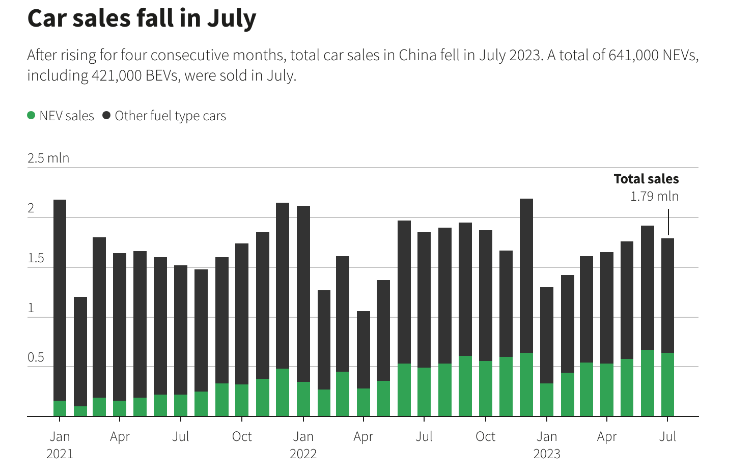

In July, China's passenger vehicle sales declined for the second consecutive month. Despite discounts and government support, consumers remained hesitant to buy cars amidst a sluggish economy and a prolonged housing market downturn. Automakers are growing increasingly concerned about a potential demand slowdown, as the world's second-largest economy loses its post-pandemic momentum. Data from the China Passenger Car Association, revealed that car sales totaled 1.79 million units in July, marking a 2.6% decrease compared to the previous year, following a 2.9% decline in June. Volkswagen's sales were not resistant neither, their sales in China experienced a 1.3% YoY drop in the first half of 2023 and I expect this to continue.

{kind=link}

China Sales Development (Reuters)

Another aspect is the diverging strategies employed by Chinese automakers and Volkswagen. While Chinese automakers are increasingly focusing on overseas markets due to a slowdown in domestic growth, as evidenced by a remarkable 63% surge in exports in July, Volkswagen remains committed to seeking growth within China itself. This divergence in approach and lack of diversified growth in other regions may have conflicting implications for the company's future performance.

Inflation in US and Europe, elevated Interest Rates and "Sick man of Europe"

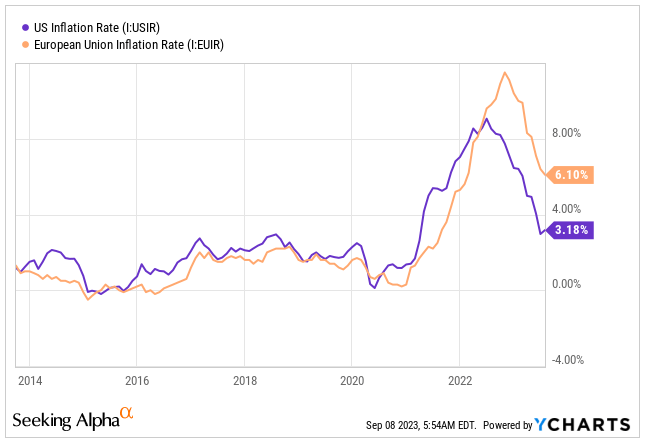

As we're all quite aware, inflation has been the talk of the town for the past couple of years, even reaching levels reminiscent of the 1980s. I won't dive into the nitty-gritty details of what caused it or who may have missed the boat on predicting it. What's really worth noting is that since that big spike in 2020-2021, inflation has continued to linger at elevated levels, well above the 2% targets set by both the ECB and the FED.

{kind=link}

Inflation Development (Seeking Alpha / YCHARTS)

Both the ECB and the FED have embarked on the path of quantitative tightening and interest rate increases. However, I find myself in the camp that believes inflation won't subside quickly enough. This implies that both the ECB and the FED may need to raise rates at least once more, and these elevated rates could persist for the foreseeable future. I don't foresee a rate decrease before the end of 2024, and even then, any reduction is likely to be minimal.

The impact of increased interest rates is particularly pronounced in industries like automobiles, which are highly sensitive to market cycles. This could lead to a delayed new car purchase or a shift towards buying used vehicles, which could adversely affect Volkswagen's sales in both the US and Europe as long as rates remain elevated.

{kind=link}

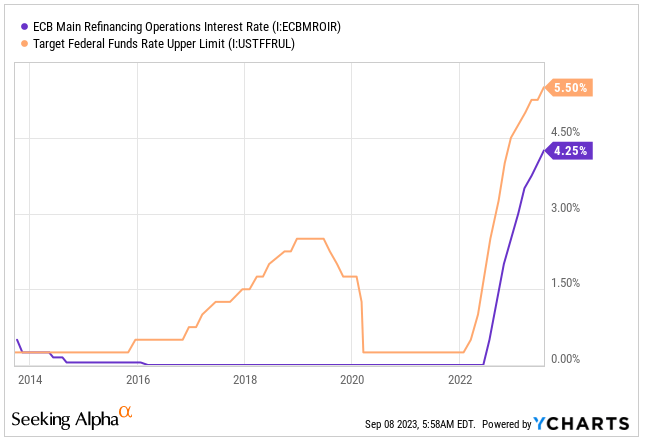

Central Bank Interest Rates (Seeking Alpha / YCHARTS)

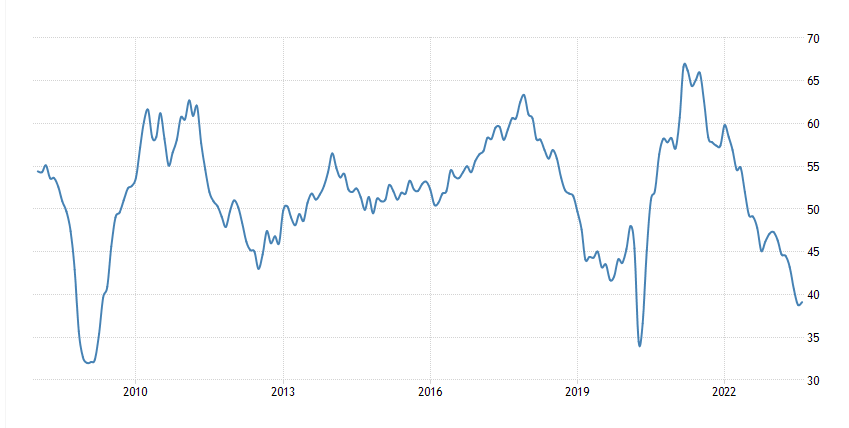

If the elevated interest rates alone are not a compelling enough reason to consider, Germany, which constitutes Volkswagen's largest market in Europe and contributes more than 27% of the total units sold in the region, has already slipped into a mild recession in the Q1 2023. Recent weeks have witnessed the resurgence of the label "Sick man of Europe" , aligning with the ongoing challenges faced by the manufacturing sector in the largest economy of the region and the country's struggles with surging energy prices. The country's PMI has dropped below 40, indicating a contraction in the manufacturing segment—a level not observed since the industrial slowdown during the pandemic and, prior to that, in 2009.

{kind=link}

PMI Graph (Trade Economics)

The situation ties closely to the automobile industry, which is essentially the lifeblood of Germany's economy, with so much riding on its performance. Last year, cars took the spotlight as Germany's primary export, making up a significant 15.6% of the total value of goods sold abroad, as per data from the federal statistics office. What's worth noting is the notable shift that occurred in May 2022, when Germany reported a foreign trade deficit. This marked the first time in decades that the nation was bringing in more than it was sending out, amounting to €1 billion ($1.03 billion).

This development strongly suggests that Germany is already facing economic challenges, and it doesn't seem like there's any immediate relief in sight. Looking ahead to the coming winter, the situation could potentially worsen if energy prices continue to rise, and the manufacturing index contracts further. All of this spells trouble for Volkswagen, especially in one of its crucial regions.

Growing threat from Chinese EV Automakers

Whether you're a fan of EVs taking over the automotive industry or not, the current trends strongly suggest that they're gaining popularity and are here to stay. In all likelihood, they'll eventually dominate the market that was once ruled by traditional combustion engine vehicles. I'm not here to pass judgment on which automaker produces the best EVs or which technology is leading the way. What's really concerning for Volkswagen and other European and American automakers is the growing appeal of Chinese vehicles. They seem to be winning customers over with their quality and competitive pricing. As discussed recently on CNBC , Chinese EV manufacturers are posing a significant threat to Europe's auto industry.

As I mentioned earlier, Chinese vehicle exports saw an impressive 63% growth worldwide in July. According to KPMG , Chinese EV automakers are on track to grab more than 15% of the European EV market by 2025, a notable increase from their current market share of less than 10%. This shift was unmistakably evident at the latest car show in Munich , where nearly 40% of the presenters came from Asia. What's more, the number of Chinese exhibitors at the event more than doubled, going from 29 in 2021 to 75 this year. It's becoming increasingly clear that Europe , and eventually the United States, are the next major markets that the Chinese EV industry is aiming to conquer.

{kind=link}

Title CNBC (CNBC)

Undervalued but Razor Thin Profit Margins

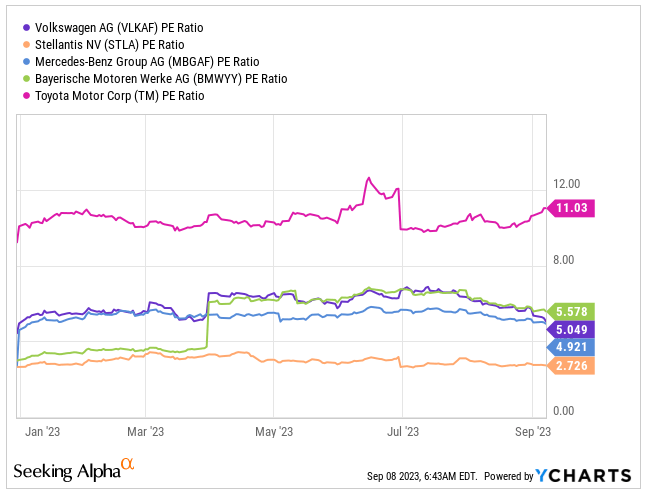

Right now, the company's trading at a relatively low valuation, specifically at 5.05x times its expected 2023 earnings. This is less than its five-year average of 6.7x times and significantly lower than the broader sector, which is at a much higher 12.37x times.

But here's the interesting part: It's not the cheapest option among its fellow legacy automakers. Take Stellantis, for example; it's trading at a bargain 2.73 times. Mercedes-Benz is at 4.92x times, while BMW is slightly pricier at 5.58 times. Toyota, on the other hand, comes in at 11x times, making it one of the costlier choices in this group.

{kind=link}

PE Ration vs. Peers (Seeking Alpha / YCHARTS)

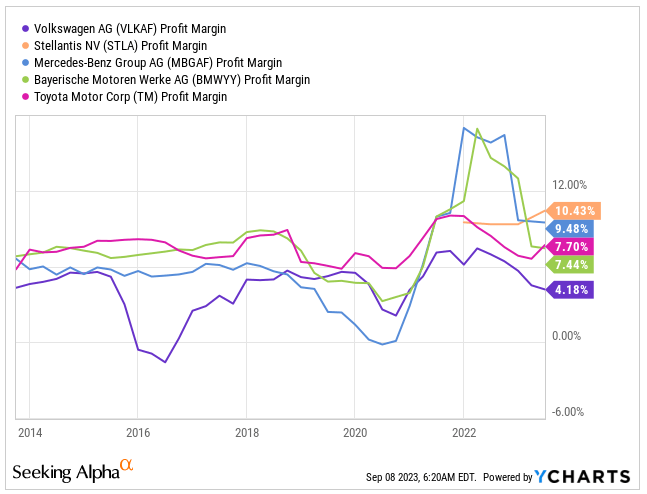

What truly worries me is Volkswagen's efficiency. Historically, the company has maintained incredibly slim profit margins, and they currently sit at just 4.18%, which happens to be the lowest among the group.

{kind=link}

Profit Margin vs. Peers (Seeking Alpha / YCHARTS)

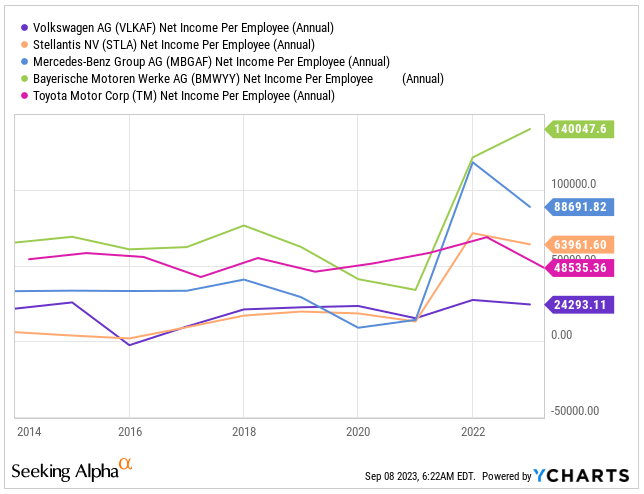

The situation doesn't improve when we consider Net Income per Employee. Historically, Volkswagen has grappled with low profitability while maintaining a significantly larger workforce compared to other automakers. To put this into perspective, Volkswagen generates approximately €24.3K per employee, while its peers, on average, earn more than €60K per employee. This translates to a stark difference of 246%.

For a straightforward comparison, let's take Toyota, the largest automaker by units sold in 2022, which outperformed Volkswagen by selling 26% more units. Toyota achieved this with a workforce of 375K employees worldwide, in stark contrast to Volkswagen's 676K employees during the same period. This challenge is partly rooted in Volkswagen's European operations, especially in Germany, where the company has various agreements with local governments, incentivizing them to employ a specific number of people through subsidies and tax incentives. While this approach may have short-term benefits, it leaves Volkswagen vulnerable to declining profitability in an increasingly automated world, potentially leading to significant troubles down the road.

{kind=link}

Net Income per Employee (Seeking Alpha / YCHARTS)

Despite having a favorable valuation compared to the industry average and certain peers, along with an enticing 8.2% dividend yield, which is significantly higher than the industry average of just 2.13%, the company appears poised for underperformance in the upcoming years.

Conclusion

While Volkswagen is currently trading at the lower end of its historical valuation range, the company is confronted with significant challenges in its key markets. China, which was expected to be a growth engine for the company in the coming years, is witnessing a decline in sales compared to previous years. This situation doesn't seem to be improving due to a lack of government support and economic reforms.

The scenario isn't much brighter in Europe and the United States either. Inflation has prompted central banks to embark on a path of interest rate hikes, leading to higher financing costs for new vehicles. Moreover, Germany, Volkswagen's largest market in Europe, has already slipped into a mild recession in Q1 2023, with the PMI showing further contraction.

Given these circumstances, I am initiating a SELL rating on Volkswagen.

For further details see:

Volkswagen: Don't Chase The 8.2% Yield