VLKPF - Volkswagen: Lamborghini Upside And EU Volume Recovery

2023-11-24 02:46:55 ET

Summary

- Lamborghini 9M results exceeded 2022 full-year numbers.

- Volkswagen confirmed its market share gain in the first ten months in the European Union.

- Downside protection from luxury brands, including P911 development.

- A solid balance sheet, dividends confirmed, no intention to lower car prices, and reverse working capital effects make the company a strong buy.

Post Q3 results, we still need to update our readers on Volkswagen (VLKAF) (VWAPY) (VWAGY). The company is Europe's largest carmaker and a leading player in commercial vehicles. Volkswagen's portfolio comprises 12 brands and covers all segments, from heavy trucks to supercars such as Bentley and Lamborghini. Today, we aim to comment briefly on the company's results and update our investors on two of our current upsides. Before moving forward with the specific update, we suggest our readers check our previous analysis, which is focused on the EU's Positive Macro Upside .

Q3 Results and Our Take

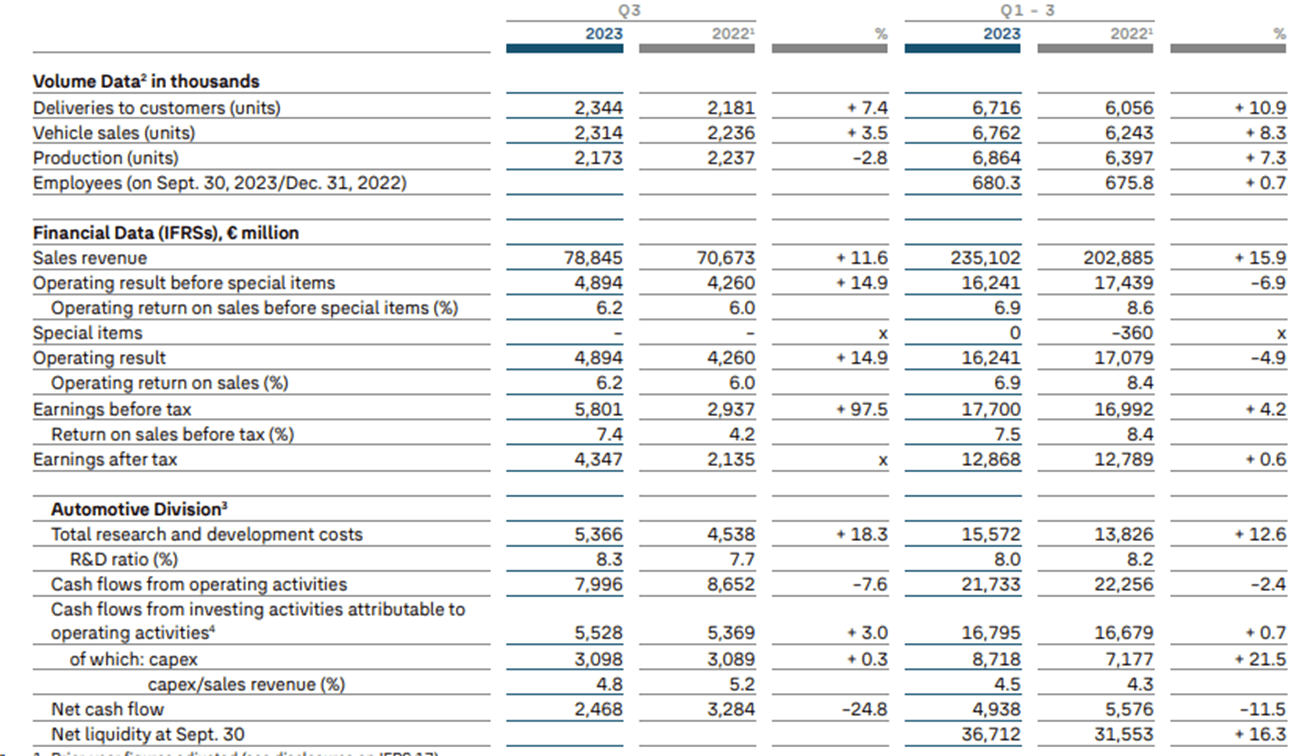

- Q3 deliveries to end clients increased 7.4% to 2.34 million units vs. Q3 2022. YTD, the company is up by 10.9%. Q3 production was slightly impacted by the Slovenian floods , which disrupted Europe's automotive supply chain;

- Q3 top-line sales increased by 11.6% to €78.84 billion. YTD, Volkswagen is up 15.9%. Therefore, the company was able to pass price increases to end customers;

- Conversely, the company's operating results are down YTD but signed a plus of 14.9% in the quarter. At the yearly level, operating results were impacted by higher raw material inflationary pressure and fair value adjustments on derivatives. On an adjustment basis, we also see a positive impact from R&D capitalization for €1.3 billion (this represents 27% of the Q3 core operating profit). During the call, the CFO confirmed that derivatives on FX and higher production costs will be limited in 2024. As a reminder, sales, operating profit, and FCF were already pre-released;

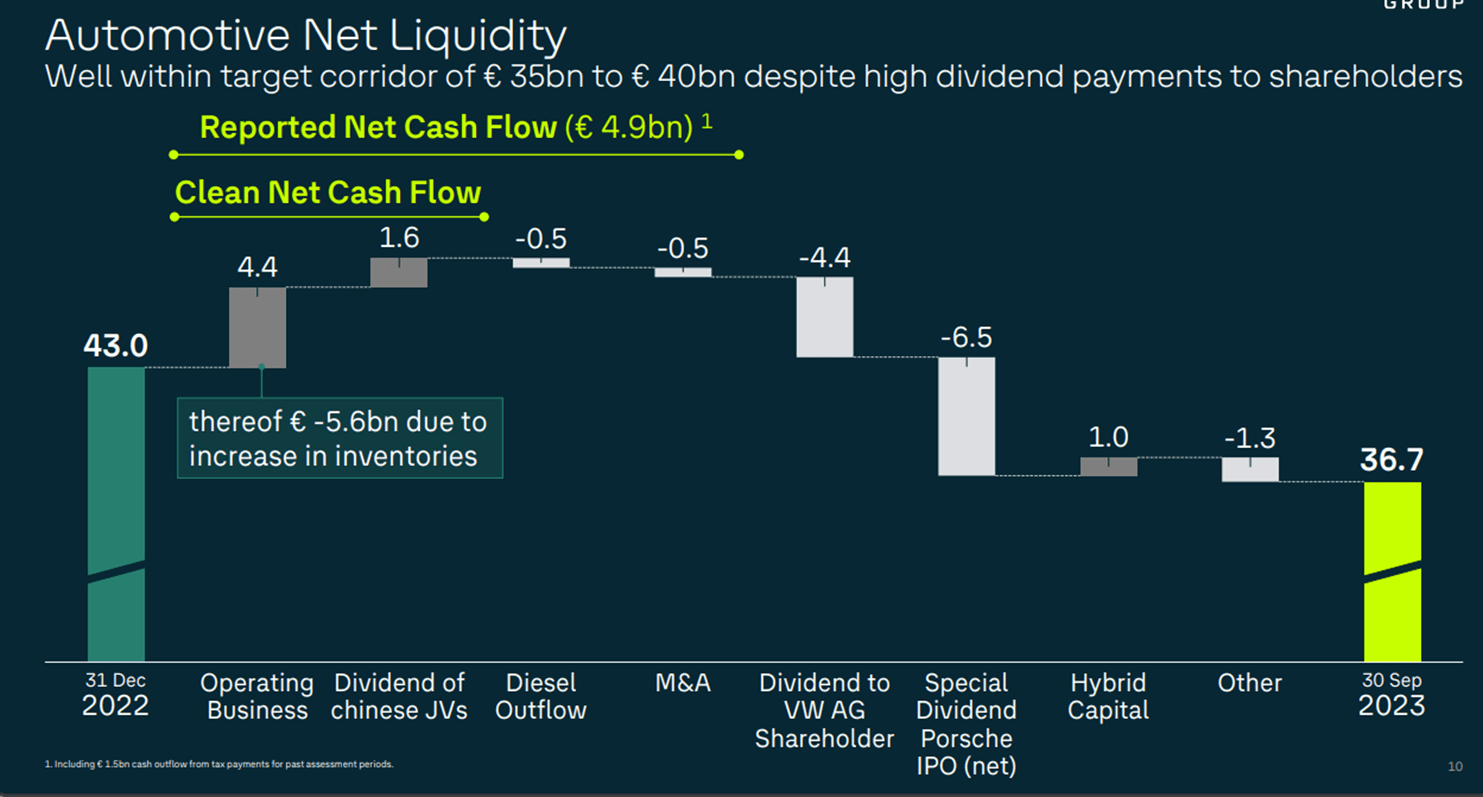

- On a positive note, the company has liquidity of €36 billion, already penalized by higher working capital requirements;

- To address the Chinese EV competition, Volkswagen is investing around $700 million in Chinese electric-car maker XPeng to purchase a 4.99% stake in the company;

-

Looking ahead, CFO Arno Antlitz's tone remained positive for Q4 development and beyond, with 1.4 million cars still in the backlog for the Western Europe area;

-

In addition, the company confirmed the yearly outlook. This means that the dividend policy will also be kept the same. Looking at the evolution of cash flow, the company can pay the dividend. On average, they make €2 billion FCF per quarter (€8 billion per year) and pay €4.4 billion in dividends. Therefore, FCF covered dividends by 2x.

Volkswagen Q3 and YTD Financials in a Snap

{kind=link}

{kind=link}

Our Two Ongoing Upside: Lamborghini and EU Market share

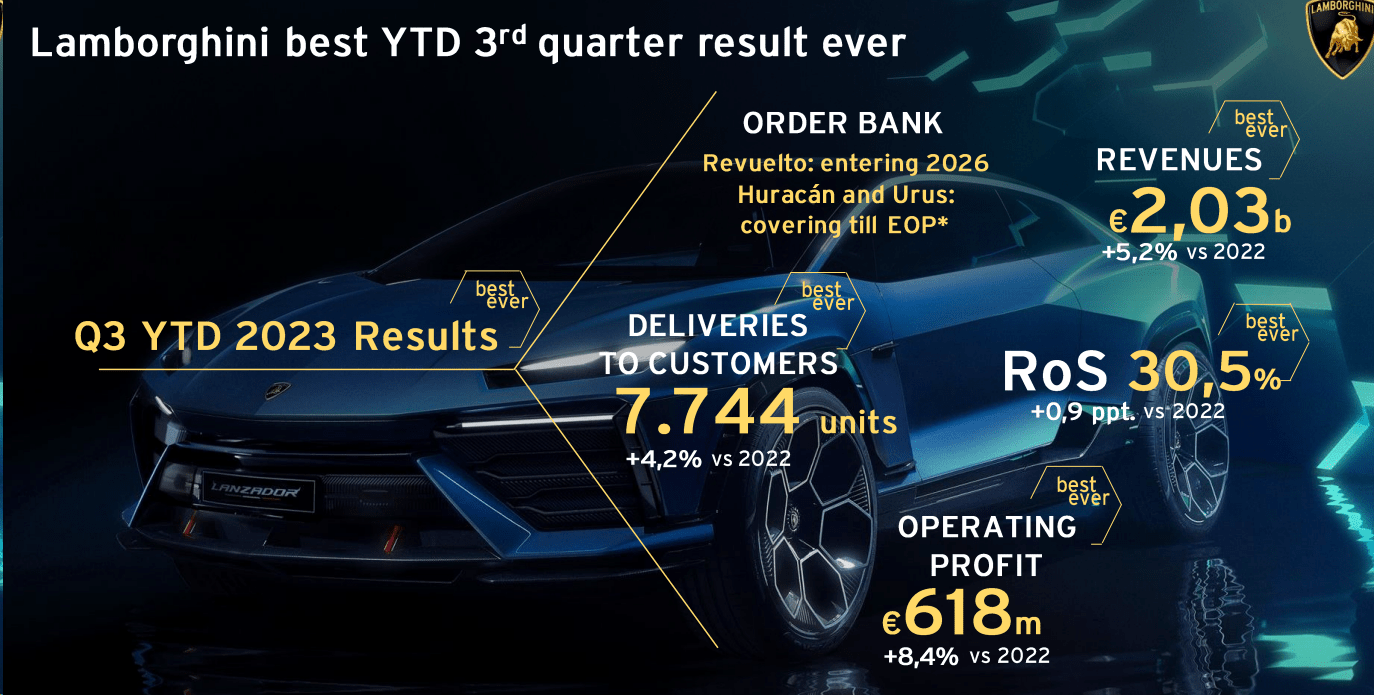

Starting with the Italian supercar development, even if it is not a listed company, Lamborghini presented its Q3 results. In the first nine months, Lamborghini reached new historic financial milestones with records in turnover and profitability. The Italian company exceeded €2 billion in sales thanks to a Q3 increase of 5.2% compared to the previous year. The operating results are already above the entire 2022 with €618 million. Regarding deliveries, the company recorded 7,744 cars (+4.2%), mainly thanks to URUS and Huracan models. In addition, the company presented the new Lanzador concept car (fully electric model), which will be ready in 2028. We see this move as a clear commitment to electrification and sustainability.

Lamborghini Q3 results in a Snap

{kind=link}

The company's growth is also reflected in the expansion of its sales network, with the opening of five new dealerships in Q3. Lamborghini now has 182 dealers spread across 54 markets. The CEO also expects a positive trend in Q4. Despite that, he also explained that IPO is not a short-term optionality and the company is " in an excellent financial situation ." To support Lamborghini's valuation, we should also check Ferrari . The Maranello-based company recently reached €60 billion in market cap (Ferrari: Outlook Appears To Be Conservative ), and we believe that Lamborghini is not lagging behind its closest peer. Revenue growth, margins, deliveries, and a rock-solid balance, supported by car desirability, make the two companies alike. Even applying a 50% discount (which we believe is unrealistic), Lamborghini could be valued at €30 billion, making half of the current company's market cap.

{kind=link}

Secondly, we check the monthly EU unit car deliveries to support our buy rating. Two days ago, Acea released the October data , and the Old Continent car market significantly increased, with new registrations of more than 14.6%. This marked the fifteenth consecutive month of growth and showed a volume recovery story. In detail, we should report a double-digit percentage increase in three of the most important markets: France (+21.9%), Italy (+20%), and Spain (+18,1%). However, the German car market recorded a modest increase of 4.9% yearly. Looking at the automaker development, Volkswagen increased by 9.9% in October, and more importantly, the company confirmed its market share gain in the first ten months in the European Union.

{kind=link}

Conclusion and Valuation

The company had already profit-warned with the pre-release and moved its 2023 operating profit target to approximately €22.5 billion. In the post-Q3 call, there were no additional comments about 2024, but the CFO explained that the company is running behind its order intake. Here at the Lab, our 2024 numbers are set on a core operating profit of €24.9 billion with a margin of 7.7%, arriving at a cash flow evolution of €15 billion. To support our buy, the CEO confirmed that he will not cut prices and expects a reverse in raw materials prices in 2024, bringing margins back to an attractive level. Looking at the valuation, the company's PE is at 3.5x with an EV/EBITDA of 1.35x. This company sells nine million vehicles annually with an annual turnover projection of €300 billion. Therefore, even if we are not chasing a dividend yield, Volkswagen trades at an FCF yield of almost 25%, and based on our 2024 estimates, post Q3 results, we arrived at an NTM EPS of €28, which is in line with its historical average . Applying a P/E of 7x supported by Volkswagen luxury brands ( Porsche AG included ), we reiterated our buy rating of €196 per share.

For further details see:

Volkswagen: Lamborghini Upside And EU Volume Recovery