LGMMY - Vonovia: Is The 8% Dividend Sustainable?

2023-03-11 09:25:43 ET

Summary

- Vonovia is trading at a third of its book value.

- The dividend is of paramount importance.

- Mr. Market is assuming a cut or suspension.

- The management team has previously committed to both deleveraging and paying a full dividend.

- Will Vonovia be forced to cut the dividend?

This is an update to my previous article on Vonovia SE (VONOY) (VNNVF) to reflect developments ahead of the earnings date next week, as well as to answer the key question: will Vonovia cut the dividend?

I recommend purchasing the stock in the German stock exchange (primarily listing) and not through the U.S. listed ADR.

Background

Vonovia is Germany's leading residential real estate company. Vonovia currently owns and manages ~550K residential units, mostly in Germany, but with some apartments also in Austria and Sweden.

Whilst rental income from holding residential apartments is its main business, Vonovia also has additional segments that include:

- Property development segment

- Recurring sales (disposal of non-core apartments)

- Value-add services (e.g., craftsmen, media, etc.)

The Thesis

Historically, the stock has traded at around book value. It is currently trading at about a third of its book value. The key reason is the heightened cost of capital, which increased markedly in the last 15 months. The interest on Vonovia's debt is in the 5% range currently, whereas the rental yield of the portfolio is in the 3%, clearly not a sustainable proposition. Whilst the funding cost has been increasing rapidly, the rental income growth is materially lagging behind market rates due to the regulated nature of the German rental property market.

Another way of looking at this is that the current valuation is factoring in an almost 40% decline in the prices of German property, whereas to date the decline is probably in the low single digits.

So to bridge that valuation gap, the solution appears reasonably straightforward and Vonovia only has to deleverage. In other words, sell properties at or near book value, repay debt as it comes due, and buy back shares. Simple, right? Well, not quite.

The problem is that executing real estate transactions at scale in Germany is challenging. The market is quasi-frozen and property market transaction volumes are quite low by historical standards, and a firesale would likely be counter-productive and destroy value for shareholders in the long term.

Investors' Perspective

Many investors see the stock as a bond proxy, given predictable cashflows and sensitivity to rates (even though management would strongly argue otherwise). The 10-year Bond currently yields around ~2.5% and therefore investors expect Vonovia to deliver a nice spread above this (e.g. 250 to 300 basis points).

As such, the dividend yield is of paramount importance. The reaction to LEG Immobilien's (LEGIF) suspension of dividends last week was telling. LEG Immobilien stock was down more than 10% on the day and continued to decline in the following days.

In this environment of high inflation, a strong dividend yield is even more important for shareholders than before.

So what will Vonovia announce in relation to the dividend on the upcoming earnings release this Friday?

The Q3 Guidance

During the Q3-2022 earnings call , CEO Rolf Buch was (almost) unequivocal in the prepared remarks that the usual Vonovia dividend policy will continue at 70% of FFO:

The dividend guidance is also unchanged, in line with the FFO guidance and that as a reminder, 70% of our group FFO for minorities, to be precise.

Later on, in the Q&A, the analysts pressed the issue further if the transaction market proves difficult:

Andres Toome

Yes, so the question was, if disposals don't come through, as you sort of alluded that transaction market is quite difficult, would the next lever for you to reduce the dividend to have a better cash flow position.

Rolf Buch

So I think we have said that the dividend several times that our business policy is now known, and it has not changed. So to repeat, we have --we are paying around 70% of the Group FFO plus minorities to be precise. And to be more formal, the management board and supervisory board we'll make a proposal in the end of Q1 beginning Q2 to the AGM and formally, the AGM as a shareholder decides the dividend. But I repeat our dividend policy, they have not changed and was around 70% of FFO.

So the management team (at least in November 2022) seemed very convincing that the full dividend will be paid. This translates to a yield of ~8%.

Based on the current pricing of the stock, Mr. Market, especially following LEG Immobilien's suspension of the dividend, is likely factoring in a dividend cut or suspension.

If Vonovia is going to maintain the dividend at 70% of FFO as per current policy, this will be a strong confidence vote that the business strategy is robust and that it is able to deleverage successfully.

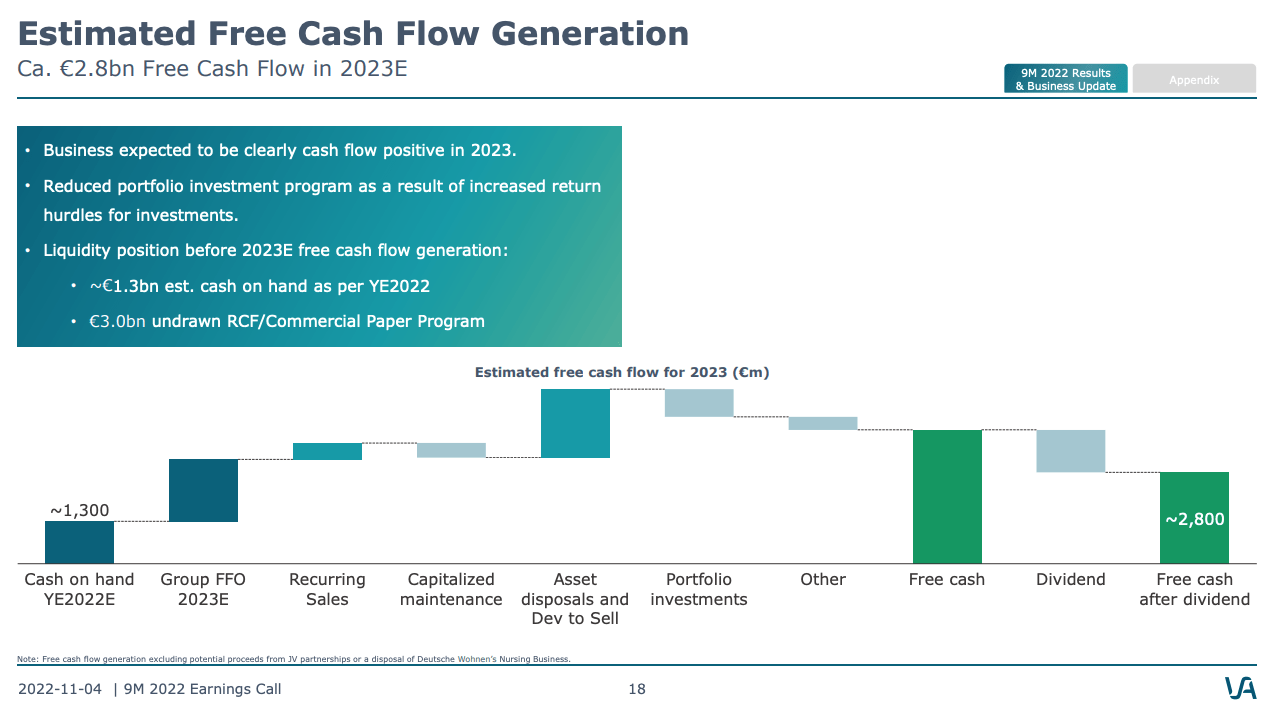

In the Q3 earnings release, Vonovia outlined a projected path to generating EUR2.8 billion of free cash flow (post dividend). This is represented in the below chart:

{kind=link}

So by the end of 2023, Vonovia is guiding for EUR2.8 billion cash balance.

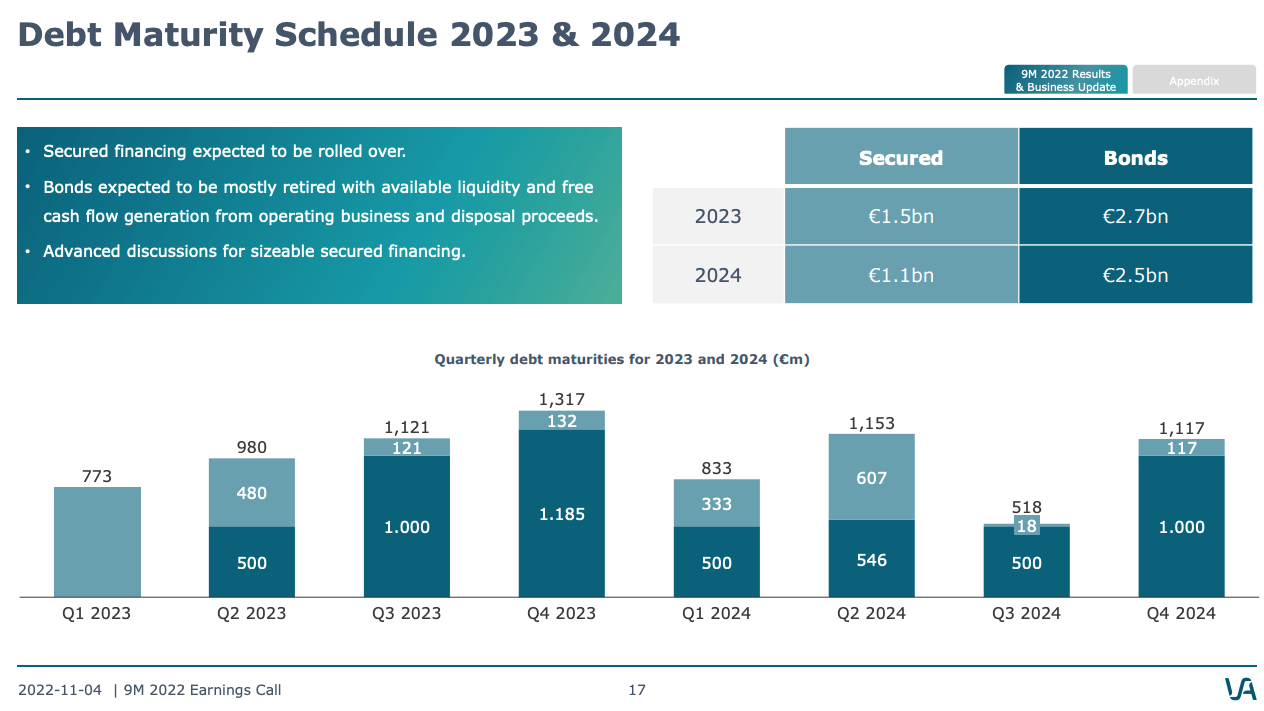

Now let us consider the debt maturity profile for 2023 and 2024:

{kind=link}

Vonovia highlighted that it intends to roll over the secured debt (bank financing) and repay the bonds in 2023 and 2024.

Now later in November 2022, Vonovia has taken advantage of a favorable capital markets window and has raised EUR1.5 billion from the bond market. It utilized EUR1 billion to buy back bonds maturing across 2023 and 2024 maturities and EUR500 million cash remaining to pay upcoming maturities. So the remaining outstanding maturities for 2023 are ~ EUR2.3 billion and 2024 ~EUR1.9 billion.

Based on their Q3 guidance of EUR2.8 billion free cash flow and an additional EUR500 million from the November liability management exercise, Vonovia should have ~EUR3.3 billion in cash for 2023 and outstanding maturities of ~EUR2.3 billion. So in conclusion, the debt maturities for both 2023 and 2024, look to be very comfortably manageable for Vonovia.

Importantly, the above cashflow projections, exclude the following upside:

1) Disposal of the nursing portfolio (~EUR1.2 billion on a pre-tax basis)

2) Any JV structures

but incorporate the payment of the dividend fully at 70% FFO.

Naturally, the above assumes that Vonovia can deliver on the asset disposal program, which some analysts are doubtful of. In Q3, the management team sounded very confident:

So we are given you slides, where we are saying that this management team is committed to have under the explanation that Philip is doing a free cash flow of EUR 2.8 billion after dividend payments. So this was a commitment, like our commitment over rental cost like our commitment on offer if all, or normally, you know that we as a management team, are normally doing guidance, which we can fulfill. So and of course, some players feel that they're playing, we can do a little bit more this non-core, you can do a little bit more multifamily home. So there's a lot of pillars which we have to play, but in the end, we will feel very comfortable that we will deliver the EUR 2.8 billion free cash flow and assumptions laid out in page 18.

Other Constraints for The Dividends

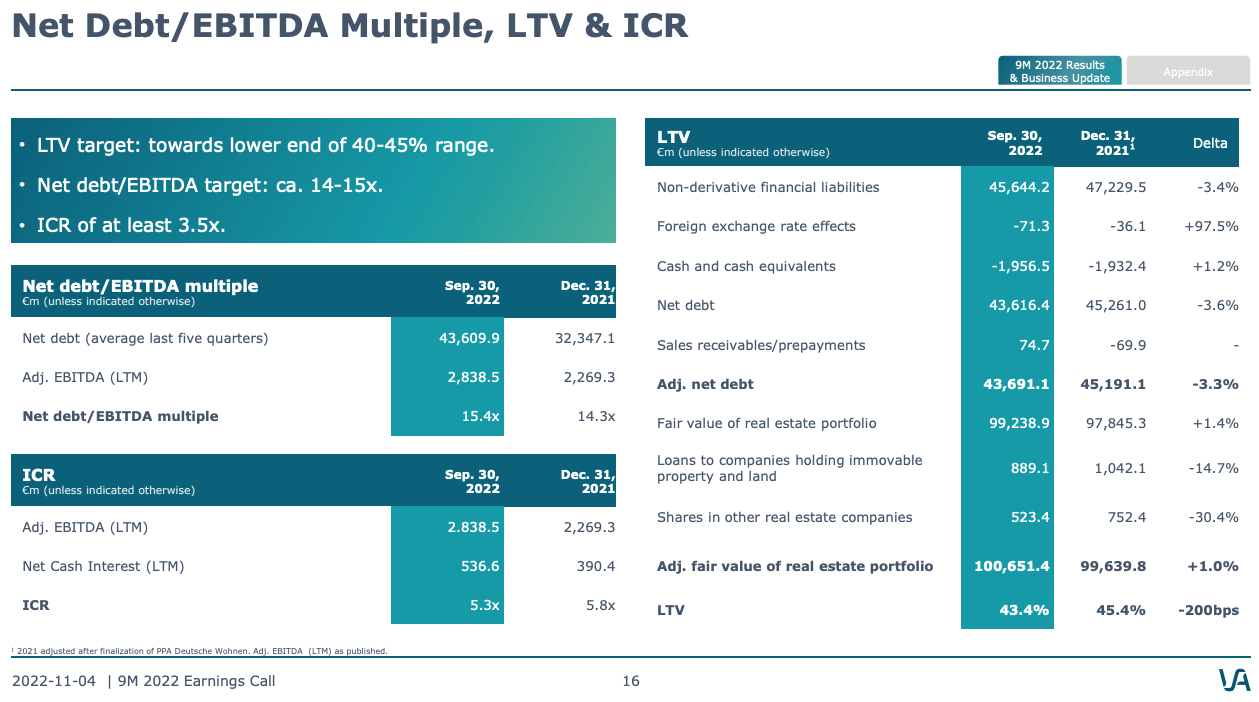

Of course, the other constraint for the dividend is the need to achieve targeted leverage ratios, as highlighted below:

{kind=link}

The binding constraint for Vonovia is probably going to be the LTV target of between 40% and 45%. Given that, I expect (as per LEG results as well) a low single-digit decline in the valuation. This may put some pressure on the LTV ratio and push it toward the 45% zone or slightly higher. Albeit, the Vonovia management team may be comfortable with a slightly higher LTV temporarily, provided they project stability in the book valuation and/or a clear path for further deleveraging (e.g. JVs or sale of the nursing portfolio).

My Projection for The Dividend

My base case (50% probability) is a dividend cut by ~40% to ~60% or a dividend yield of between 3% to 5%.

The bear case (20% probability) is a complete suspension of the dividend and applying the full proceeds to reduce debt.

My bull case (30% probability) is for Vonovia to retain the current dividend policy and ~8% dividend yield.

Final thoughts

The German property market rental yield is kept artificially low by regulation and significant lag in rent increases. It worked when the eurozone interest rates were 0% or negative. In the current rate environment and inflationary settings, this is no longer sustainable. It is clear that the construction of units is coming to a standstill in Germany, and the chronic shortage of property in urban areas is getting worse every year. In the medium to long term, these demand-supply dynamics are strongly playing in favor of Vonovia's business model. In the next few years, rents are going to appreciate markedly. For example, the recent Munich rent index increased rents by an astounding 21%.

In the short term, the market is going to see Vonovia as a bond proxy and therefore the dividend yield is of paramount importance. The management team knows this and communication around the dividend policy is going to be absolutely scrutinized by investors.

I remain very bullish regardless.

For further details see:

Vonovia: Is The 8% Dividend Sustainable?