ONL - Vornado Suspended Its Dividends: Are Your Dividends Safe?

2023-05-01 08:23:58 ET

Summary

- Vornado recently suspended its dividend after paying a consistently high dividend for 30 years.

- 28 office REIT dividends were evaluated for safety based on yield, coverage ratios, and price/book value.

- I recommend investors who own office REITs review their positions, particularly if consistent dividends are a primary concern.

Background

After paying a reliable dividend for 30 years, Vornado Realty Trust ( VNO ) recently announced that it will postpone dividends on its common shares until the end of 2023 with plans to invest retained cash towards debt reduction and/or share repurchases. VNO plans to pay a 2023 dividend upon finalization of its 2023 taxable income including the impact of asset sales. From management perspective, it might make sense to repurchase shares and reduce debt; however, investors are rightly disappointed.

Since VNO is an office REIT, this analysis will focus on the dividend safety of companies across the office REIT sub-sector. Recent VNO trends are a logical starting point.

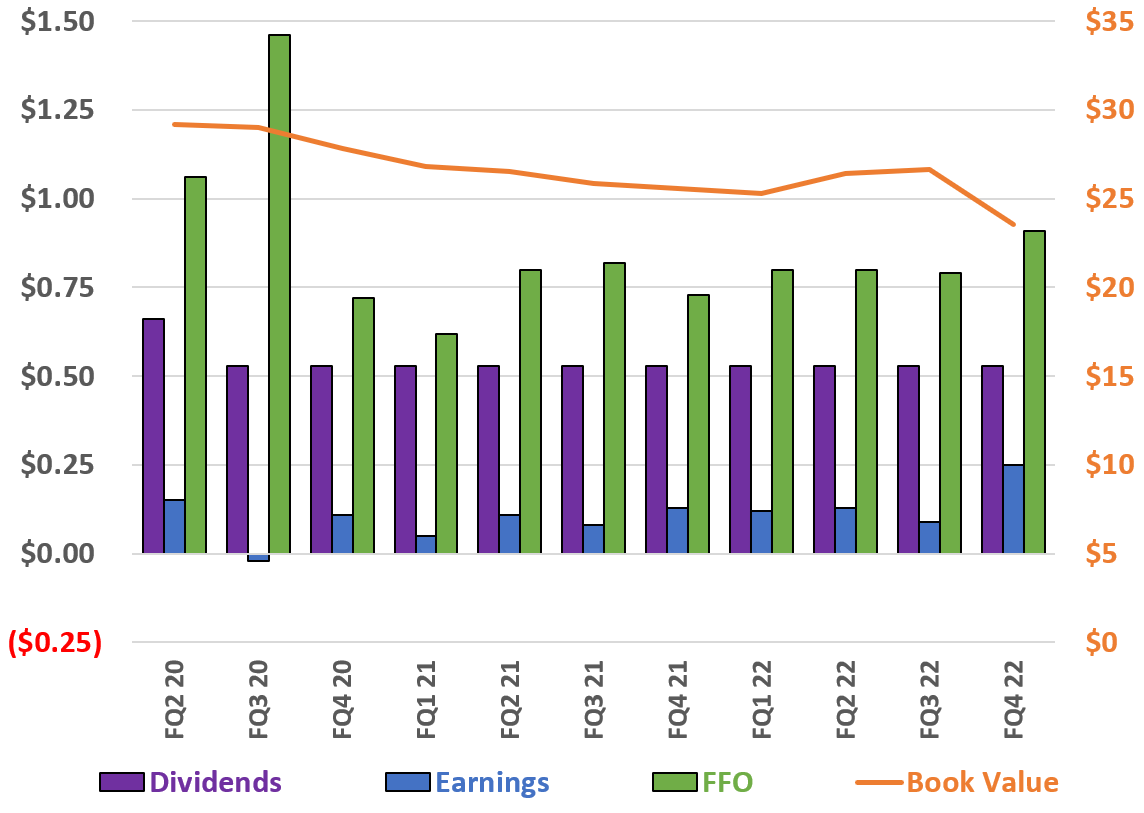

VNO: Dividends, Earnings, FFO, & Book Value (per/share values)

{kind=link}

Dividends, earnings, and FFO are plotted against the left axis while book value is plotted against the right axis. Since FQ2 20 VNO has paid dividends substantially greater than its earnings. However, dividends were well covered by FFO (funds from operations). Notably, FFO is a less rigorous dividend coverage ratio. Further, REITs are only required to pay dividends equal to 90% of earnings (equivalent to 111% earnings coverage ratio). Finally, book value/share has generally declined over the period.

How Safe Are Office REIT Dividends?

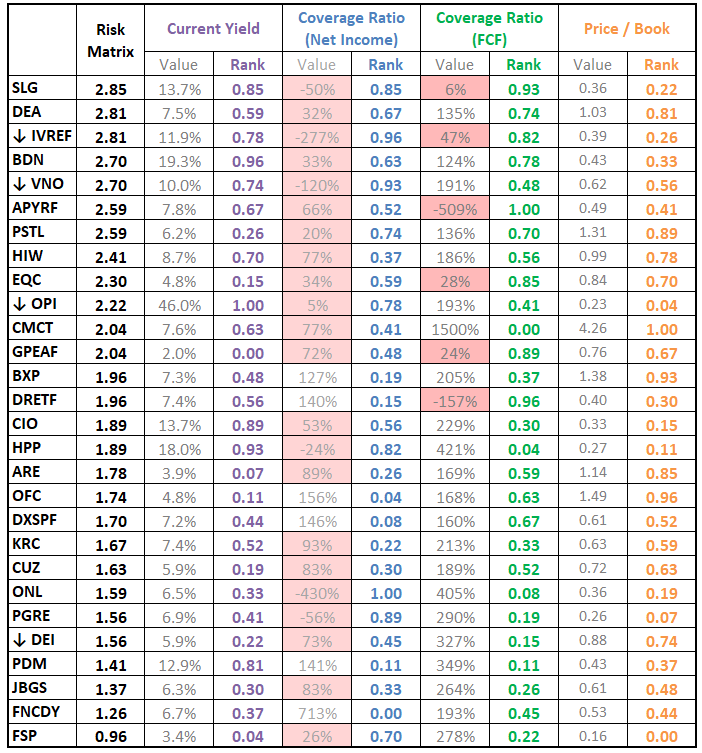

Dividend safety for 28 office REITs were compared using a risk matrix with the following factors:

- Current Yield - A higher dividend was considered more risky

- Coverage Ratio (Net Income) - A lower coverage ratio was considered more risky

- Coverage Ratio ((FCF)) - Free cash flow was substituted for FFO as it is a similar but more consistently reported metric, A lower coverage ratio was considered more risky

- Price/Book Value - A higher value was considered more risky

The values for each company's factors were normalized by means of statistical percent ranking with relation to the group. The risk matrix was calculated as the sum of the percent ranks of the factors.

Risk Matrix Chart

{kind=link}

The above chart is sorted in descending order from highest dividend risk (highest risk matrix score) to the lowest risk (lowest risk matrix score). Note, coverage ratios less than 100% are highlighted in red; a coverage ratio less than 100% indicates a higher risk dividend in most cases. VNO values do not reflect the recent dividend cut for the sake of comparison. Notably, VNO (at 5th riskiest) is not an extreme outlier by any metric. Down arrows indicate a dividend that has already been cut recently.

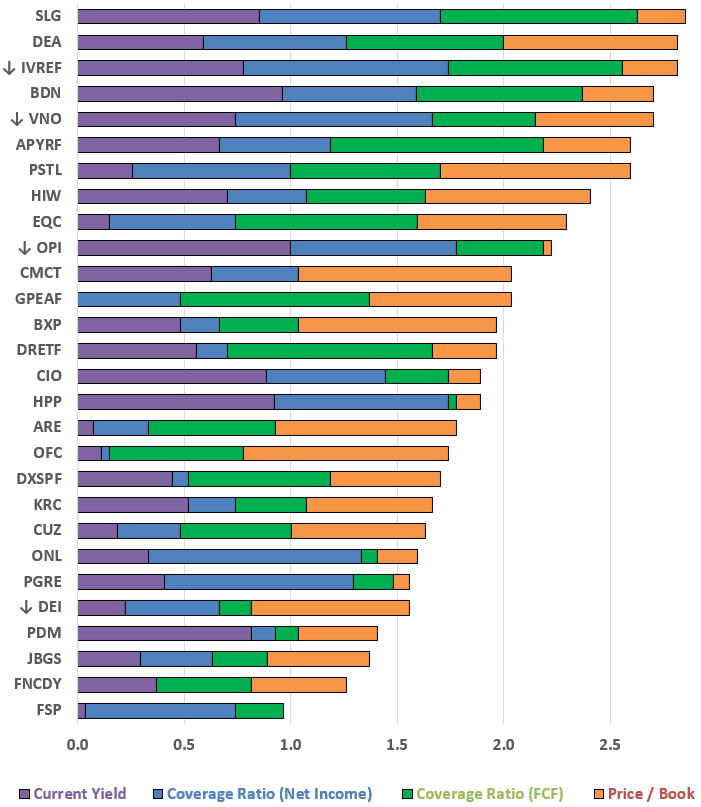

Risk Matrix Plot

{kind=link}

The risk matrix is presented graphically in the stacked bar chart above with cumulative inputs for each factor. Based on this analysis, the most risky dividends in the group are likely to include:

- SL Green Realty Corp. ( SLG )

- Easterly Government Properties, Inc. ( DEA )

- Inovalis Real Estate Investment Trust ( IVREF )

- Brandywine Realty Trust (BDN)

- Allied Properties Real Estate Investment Trust ( APYRF )

Based on this analysis, the safest dividends in the group are likely to include:

- Franklin Street Properties Corp. ( FSP )

- Covivio (FNCDY)

- JBG SMITH Properties ( JBGS )

- Piedmont Office Realty Trust, Inc. ( PDM )

- Douglas Emmett, Inc. (DEI)

Quality Matrix Limitations

Investors should consider the risk matrix a screen only. The matrix and its factors, normalization method, and weights could all be adjusted and yield different results. Further, the matrix is based on the most readily available and common metrics. These metrics can change rapidly with share price or as new company reports are released. The risk matrix does not include company-specific data available in quarterly reports and presentations.

Conclusions and Recommendations

The value matrix is a blunt instrument; finesse, judgement and discernment are left to investors. Investors are advised to consider the risk matrix as nothing more than a starting point for their own due diligence. Nonetheless, a higher risk matrix score suggests a dividend is more likely to be cut.

I recommend investors who own office REITS review their positions, particularly if consistent dividends are a primary concern.

Information is a source of learning. But unless it is organized, processed, and available to the right people in a format for decision making, it is a burden, not a benefit. - William Pollard (Physicist and Theologian).

For further details see:

Vornado Suspended Its Dividends: Are Your Dividends Safe?