VRIG - VRIG: Could Keep Delivering A 6.3% Yield Well Into 2024

2023-12-08 18:27:41 ET

Summary

- VRIG is an actively managed fixed income ETF that invests primarily in high-grade variable rate instruments.

- Despite holding collateral with longer maturities, VRIG maintains a low duration profile due to its floating-rate nature, reducing sensitivity to interest rate changes.

- The fund's portfolio is diversified with a focus on high-grade bonds, treasuries, and securitization sectors to mitigate credit spread risk. Single issuer concentration is kept minimal.

- VRIG has shown a robust performance since 2021, outperforming the SPY total return since the beginning of the Fed hiking cycle. Even in a lower rates environment, it's expected to maintain stability around $25/share, though with a lower yield.

Thesis

The Invesco Variable Rate Investment Grade ETF ( VRIG ) is an actively managed fixed income exchange-traded fund. The fund aims to invest at least 80% of its holdings in a portfolio of investment-grade variable rate instruments. The vehicle falls in the cash parking vehicles category via its ultra-short duration and high-grade collateral, but takes more credit risk when compared to very short-dated fixed coupon bond funds. More than 30% of the fund's collateral has maturity dates in excess of 5 years, which translates into potential gap-downs in price during an outside event like Covid:

During normalized economic times or even regular recessions, the fund performs robustly with very shallow drawdowns.

The fund comes with a 1.88% annualized volatility and had a very modest -2% drawdown during the 2022 market sell-off. The fund is currently delivering a 6.3% 30-day SEC yield, and it should continue to do so until the Fed cuts rates. In a dedicated section below we go through the reasons for which the Fed will not cut until mid-2024, validated by the jobs report today.

We like what this fund does and its analytics and are a buyer until the Fed starts cutting rates when fixed rate funds become more attractive.

Analytics

- AUM: $0.77 billion.

- Sharpe Ratio: 0.48 (3Y).

- Std. Deviation: 1.34 (3Y).

- Yield: 6.30%.

- Premium/Discount to NAV: 0%.

- Z-Stat: n/a.

- Leverage Ratio: 0%.

- Effective Duration: 0.11 years

- Composition: Corporate Bonds

Composition

The fund invests in a portfolio of high grade bonds:

Ratings (Fund Fact Sheet)

Unlike the fixed rate ultra-short bond fund cohort, the vehicle is more focused on higher-rated bonds in order to manage credit risk. Credit risk is manifested through lower prices during times of market distress. The higher the original credit spread, the higher the sensitivity. Non-floating rate ultra-short bond funds have large BBB buckets for example (one customarily sees that sleeve at above 50% of the collateral pool).

Despite its 2.2 years weighted average maturity, the fund has a very low duration profile due to its floating rate collateral:

Duration (Fund Fact Sheet)

Constructing a low duration fund via high grade floating rate collateral is an alternative to the short-dated fixed rate bond funds. It achieves the same result, albeit with a slightly higher credit spread risk.

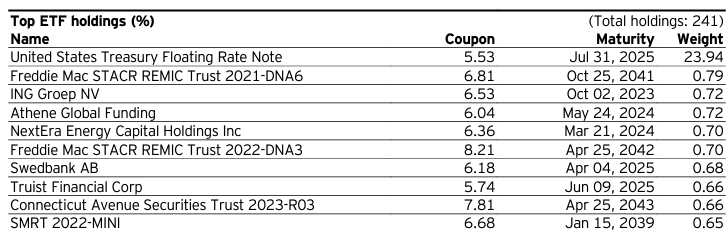

The fund has a robust build, being very granular when it comes to single issuer concentration:

{kind=link}

Outside treasuries, no other name represents more than 1% of the collateral pool. A retail investor should want to see granularity here as a way to manage credit risk.

The fund contains large treasury and securitization buckets:

Sectors (Fund Fact Sheet)

Other short-dated funds contain corporate bonds exclusively, but not here. Via this build the vehicle tries to reduce credit spread risk.

When is the Fed going to cut rates?

The market loves to speculate because speculation can generate high rewards. It was only October when yields were still skyrocketing and the talking heads on television threw out 13% rates:

{kind=link}

Fast-forward to December, and before today's job reports the market was pricing 5 cuts for 2024, with the potential first one in March 2024! Do you think this is sclerotic? We surely do. Fortunately, reality works a bit differently.

You need to understand that the market is made up of traders, and traders can make loads of money when they buy options for outside events. If enough traders buy options to speculate for a March 2024 rate cut, then they end up moving the market, even if fundamentally nothing has changed.

The jobs report today came stronger than expected, which has prompted yields to move higher and bets on a March cut to be pared back. A stronger job market means the Fed will need to keep rates higher for longer to fight inflation. A strong job market is what has kept inflation elevated, on the back of strong service purchases. It is as simple as unemployed people do not have the income to buy any services outside of basic survival ones (food, shelter, healthcare). We really need to see a broken job market with high unemployment for the Fed to start considering cutting rates.

A retail investor needs to understand that today's high inflation is the result of a troubled Fed which kept rates at zero for too long, and the worst case scenario for the Fed is to cut too soon and see a resurgence in inflation. It would undo all that they worked so hard for in the past two years. We are of the opinion that the Fed will not cut until we see a meaningful spike in unemployment, and although they are saying they are shooting for a 'soft landing', in reality, they will need a 'soft recession'.

Performance

Since the start of the Fed hiking cycle VRIG has produced a 7.7% total return with an annualized volatility sub 2%:

While not exciting, the total return is not volatile and generally upwards sloping, beating the SPY total return and not exhibiting a stomach-churning -22% drawdown. When uncertainty prevails it pays off to be conservative and still clipping yield.

VRIG is going to keep producing results at the current yield until the Fed starts cutting rates, which the market is now pricing toward mid-2024. Even when the Fed cuts, do not expect a price decrease here, just a lower 30-day yield. VRIG will keep hugging the $25/share mark, but in a lower rates environment will just end up yielding less.

Conclusion

VRIG is a fixed income ETF. The fund is composed of floating rate investment grade collateral, delivering a 6.3% dividend yield. The fund takes more credit risk than other short-duration funds via a longer maturity profile for its collateral, a risk which is mitigated by its very high grade composition. Outside a systemic event like Covid, do not expect more than a -2% drawdown here. The vehicle has been a very robust expression of floating rate low duration since the start of the Fed hiking cycle, and will continue to be a robust producer. Even when the Fed starts cutting, do not expect a lower price, just a lower yield. We like the fund's build and what it will deliver into 2024, and are a potential buyer here.

For further details see:

VRIG: Could Keep Delivering A 6.3% Yield Well Into 2024