RFMZ - VTEB: The Place To Go For Your Muni-Fix

2023-08-31 07:33:14 ET

Summary

- Vanguard Tax-Exempt bond fund won't make you rich.

- But it will help you dodge those nasty taxes.

- The fund has some high-grade quality bonds in it and offers a safe, albeit low, yield.

Municipal bonds enjoy government backing and are tax advantageous. The backing we speak of comes from the state, city, county and other local level government entities that issue these, not the federal kind. These bonds are a source of funding the daily operations, pay for capital projects, extend a helping hand to entities such as hospitals or schools etc. The interest earned from these type of securities is exempt from federal tax. The interest inflows are even exempt from state taxes, if the holder resides in the state of issuance of the security. The investor in these calculate the take-home yield after baking in the federal and/or state tax exemption into the equation. The one-two punch of the government backing and tax advantage helps municipal bonds an attractive option for a few investors.

The Fund

The Vanguard Tax-Exempt Bond ETF (VTEB) gives investors access to a diversified portfolio comprising these investments. This fund has been in existence since 2015 and purses the performance of the Standard & Poor's National AMT-Free Municipal Bond Index. This index measures the investment-grade segment of the U.S. municipal bond market and the ETF's portfolio at July 31 reflects the same attribute.

{kind=link}

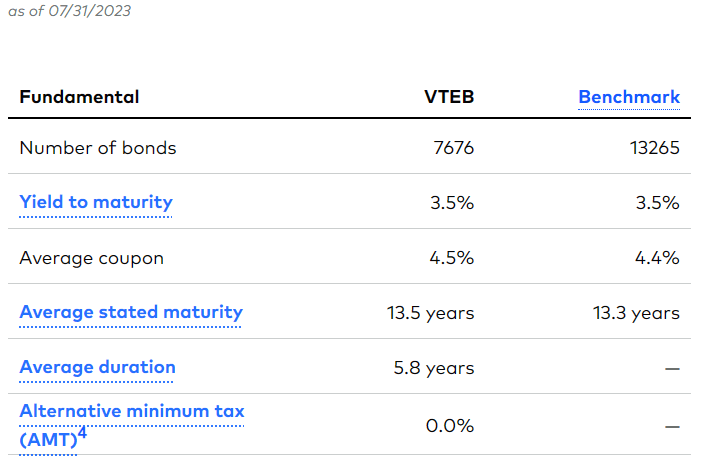

VTEB uses the sampling method to select securities from the index and ordinarily aims to invest 80% of its assets in the index incumbents. One reason for sampling is the sheer size of the market that makes holding every single security, inefficient at times. Under normal circumstances, it also aims to have the same proportion, i.e. 80%, in securities producing federally tax-exempt income. The ETF considers the maturity of the securities during the selection from the index as it is also focused on maintaining a dollar-weighted average maturity homogenous to the index. The July 31 numbers showing the 13.5 years in average portfolio maturity versus the 13.3 years for the index attest to VTEB's success in the endeavor.

{kind=link}

A few additional insights that can be gleaned from the above data. A 3.5% yield to maturity versus a 4.5% average coupon at the portfolio level indicates that VTEB is buying/holding these securities above par. Normally, buying above par comes with the risk of a realized capital loss if the security is callable and actually is called. In the current environment this risk is on the low side as financing is no longer gushing.

With a 5.8 year average portfolio duration, investors are exposed to a very modest risk in terms of interest rate hikes. Duration risk is an indicator of the extent to which the value of a portfolio declines with a 100 basis points increase in the applicable risk free rate. This inverse relationship also applies when the rates fall.

Based on VTEB's last monthly distribution of $0.01171 and the current price of $49.43, it yields around 2.8%. Considering the yield to maturity, net of expenses 0.05% in annual expenses for holding this fund, there is still room to grow the distributions.

Performance

On a net asset value or NAV basis and taking into account the annual fund expenses (which the index is not subject to), VTEB has done a good job in tracking the benchmark index. Since inception, the drag has been about 4 basis point versus the 5 basis points for expense ratios.

{kind=link}

On an absolute basis, the returns are pretty modest. One should keep in mind though that for majority of the period since its inception (2015), the risk-free rates were incredibly low.

Verdict

We prefer the municipal offerings from Vanguard over those of most other behemoths. The expense control and distribution discipline make it a clear winner in our eyes. The credit risk is also pretty low with highest percentage being AA rated. So even in an absolute market massacre, VTEB is likely to hold up well and defaults should be extremely unlikely. We also prefer VTEB over the plethora of closed end funds in this space. Most of them have been left holding 4% yielding bonds financed with 6% interest rates on their leveraged portion. That alongside large non-interest expenses means that these funds are going to struggle to sustain a 3% total return. Funnily, many funds are still in denial and distributing far in excess of what they can realistically generate over the long run.

{kind=link}

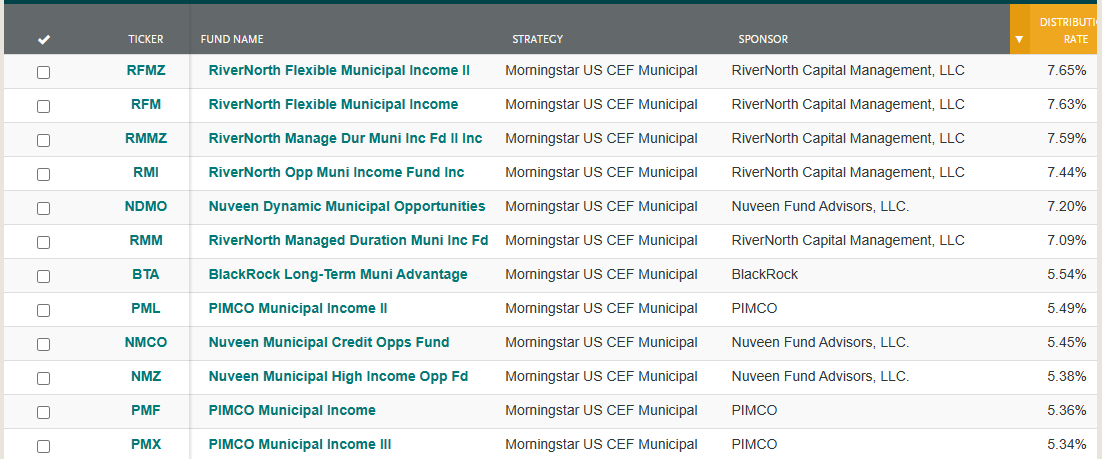

RiverNorth Flexible Municipal Income II ( RFMZ ) for example is paying 7% on NAV and 7.65% on market price. Bulk is coming from return of capital.

{kind=link}

So when investors ask why we don't chase those, there is your answer.

VTEB is a simple, albeit less high-yielding, alternative. If the after-tax yield works for you, go for it.

Schwab

Municipal bond funds, when forming a small portion of a portfolio, are not a bad choice. For us, it remains a hold. We have our eyes on a few low-leveraged municipal closed end funds that we might pick up at a wide discount in a market swoon.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

VTEB: The Place To Go For Your Muni-Fix