JPMB - VWOB: Emerging Market Bonds Are At The Mercy Of 'Higher For Longer'

2023-11-11 05:26:00 ET

Summary

- In many ways, this US-led tightening cycle is different for emerging markets.

- Yet, emerging market bonds have perhaps been too resilient in the face of rising US yields.

- As relative yields normalize, VWOB’s emerging market bond portfolio could suffer rate-driven downside from here.

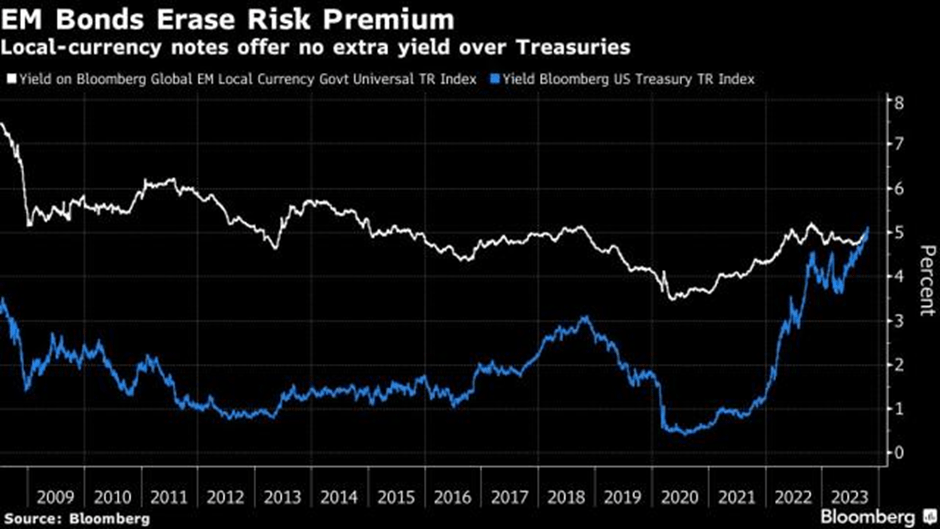

After a brief reprieve last week, a weak 30-year auction and hawkish commentary from Fed chair Powell has led to the US rate complex repricing a ‘higher for longer’ scenario. In contrast, emerging market (‘EM’) sovereigns have been relatively resilient through the volatility; as a result, we are now seeing particularly tight spreads between EM fixed income (local currency) and US treasuries. To a certain extent, the narrower relative gap is justified by better EM budget deficit and debt outlooks (per IMF projections) relative to the US. Nor are EMs contending with the kind of current account deficits that drove the ‘taper tantrum’ turbulence a decade ago.

While EMs don’t suffer from the external vulnerabilities they used to, they aren’t completely immune from the hawkish contagion. Case in point - some EM central banks have even been forced into precautionary tightening recently to defend their currencies. And with debt issuance, rather than policy rates, now in the driver’s seat for Treasuries, the bar for a reversal from ‘higher for longer’ is higher than ever.

My concern is that this scenario will continue to force many EM central banks to reverse their previous easing/neutral stances, pulling their sovereign yields ‘higher for longer’ as well. Higher rates mean more downside for the Vanguard Emerging Markets Government Bond ETF (VWOB), even with some of the downside negated via its portfolio’s dollar-denomination. Plus, VWOB’s sub-BBB-heavy portfolio is very sensitive to US rate differentials, so its current ~8% yield may not be sufficient compensation in a world where 'risk-free' T-bills yield >5%.

Fund Overview - Lowest-Cost Exposure to Dollar-Denominated EM Debt

The US-listed Vanguard Emerging Markets Government Bond ETF offers investors access to a basket of US dollar-denominated bonds issued by state and state-owned issuers in emerging market countries by tracking (pre-expenses) the Bloomberg USD Emerging Markets Government RIC Capped Index. Per end-Q3 data, the fund manages $3.5bn of assets and charges a competitive 0.2% expense ratio, well below the ~0.4% charged by comparable dollar-denominated EM bonds funds like the iShares J.P. Morgan USD Emerging Markets Bond ETF ( EMB ) and the JPMorgan USD Emerging Markets Sovereign Bond ETF (JPMB).

{kind=link}

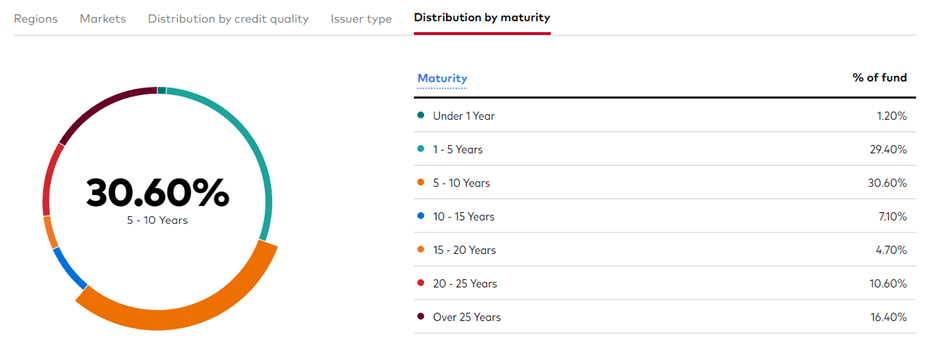

The fund is spread across 697 EM bond holdings, with an average effective maturity of 12.0 years and a yield to maturity of 7.9%. More specifically, the current portfolio composition is skewed heavily toward the one-to-five-year (29.4%) and five-to-ten-year (30.6%) maturities. Bond maturities over twenty years also feature prominently in the portfolio at a cumulative 27.0%.

{kind=link}

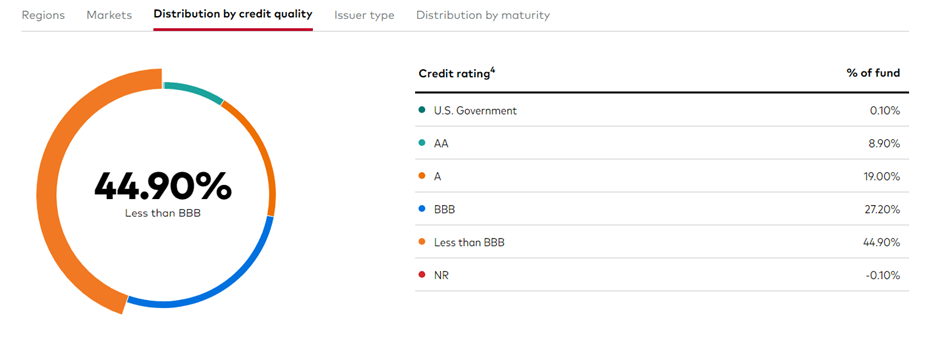

By credit quality, VWOB leans heavily toward lower-grade debt (sub-BBB), the largest portfolio contributor at 44.9%.

{kind=link}

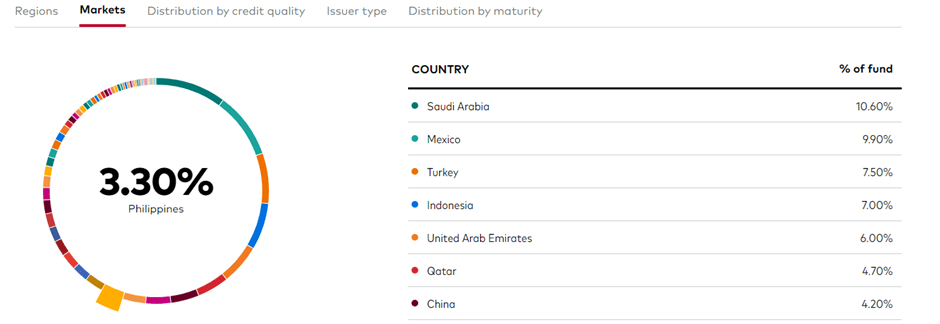

The geographic contribution is better spread out, with only five EM countries (Saudi Arabia, Mexico, Turkey, Indonesia, and the United Arab Emirates) crossing the 5% threshold.

{kind=link}

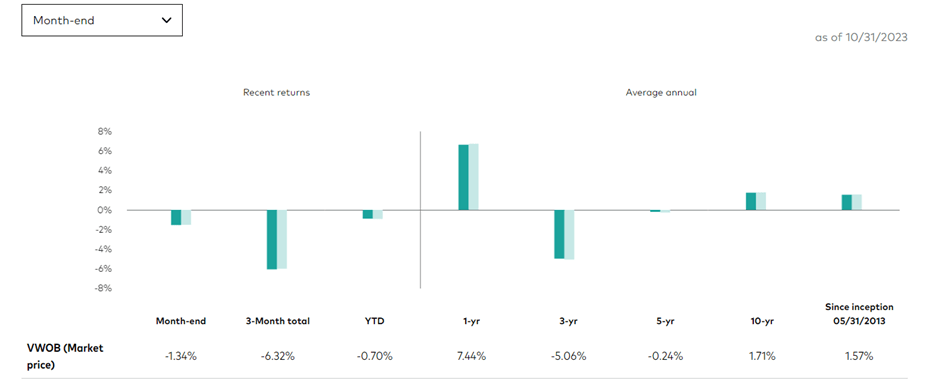

Performance-wise, VWOB’s +2.3% return year-to-date is best-in-class, along with its distribution yield (paid monthly) at 7.7% (30-day SEC basis). That said, the fund hasn’t returned enough historically to justify its risk profile. Since inception, the fund has only generated annualized total returns of +1.5% in NAV terms (+1.6% in market price terms). Over longer five and ten-year timelines, total returns stand at a similarly unimpressive -0.2% and +1.8%, respectively. By comparison, EMB’s higher-grade EM debt portfolio is slightly ahead over the last ten years (+1.9%). JPMB’s more diversified portfolio, which maintains a similar credit quality and duration profile to VWOB, is also ahead over the last five years (+0.4%).

{kind=link}

Examining This Year’s EM Bond Outperformance

In contrast with the taper tantrum a decade ago, EM bonds have been surprisingly resilient this year against pressure from higher US rates. Historically, a tightening spread between the US ten-year and comparable EM debt would be a clear relative value signal. But things are different this time.

{kind=link}

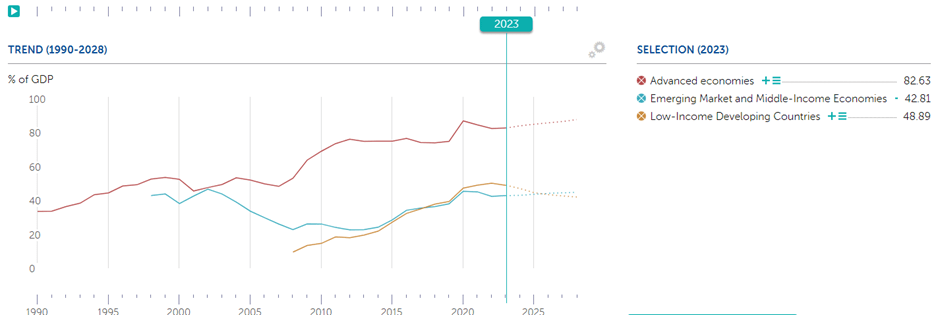

Per the latest IMF fiscal monitor , overall fiscal balances are narrowing for EMs heading into next year, in stark contrast with the US, where high-single-digits % deficits are the new normal. Even adjusting out debt servicing costs, IMF estimates of primary deficits indicate EM is running ahead of the curve. This means that, unlike their developed market counterparts, EMs are far better equipped to de-lever following widespread debt increases through the COVID-impacted period. And outside of a select few EMs headed for tightly contested near-term elections, domestic political stability should allow for a clear path to de-levering in the years to come. Tighter fiscal policy in EMs bodes well for bonds, not only by boosting their ability to service the debt but also by creating room for a faster monetary policy pivot.

{kind=link}

That said, it’s probably too soon to write off US Treasuries as the de facto global ‘risk-free’ asset. In the likely scenario that emerging markets, especially the high yielders in VWOB’s portfolio, get assigned higher credit risk premiums, expect significant foreign outflows to drive yields higher across the EM rate complex. Monetary policy is the other channel through which EM bonds could suffer selloffs, given many EM central banks have already begun cutting rates and markets have repriced accordingly. Yet, higher energy and food prices have seen spikes more recently, while relative FX weakness (vs. an appreciating USD) threatens to halt (or even reverse in Indonesia’s case) easing cycles.

In the face of contagion, VWOB’s dollar-denominated focus should allow for outperformance vs EM local currency debt in a ‘higher for longer’ US rate backdrop. On the other hand, in a world where the ‘risk-free’ option is T-bills at >5%, owning VWOB, dollar-denominated or not, isn’t particularly attractive here.

At the Mercy of ‘Higher for Longer’

The US Treasury may have temporarily delayed ‘un-inverting’ the yield curve with its decision to focus issuance on <12-month maturity T-bills over longer-dated bonds. If this week’s 30-year auction was any indication, though, there’s still a clear path higher for yields at the long end. Higher US long-end rates could have repercussions for the EM rate complex – even with many of these economies now on a lower budget deficit path and far less external vulnerabilities than before. A lot of these positives are already reflected in tight EM-US spreads this cycle, so it’s probably worth being cautious about EM bond exposure here. Expect more upward pressure in the near future as EM central banks are forced into defensive tightening, with VWOB’s relatively low-quality (but dollar-denominated) EM portfolio likely to bear the brunt.

For further details see:

VWOB: Emerging Market Bonds Are At The Mercy Of 'Higher For Longer'