LTPZ - War The Fed And The Outlook For Gold

2023-11-05 03:54:28 ET

Summary

- Gold continues to trade at a premium to real bond yields, in part due to the Israel-Hamas war, suggesting downside risks in the near term.

- However, high government debt will lead to lower real interest rates, which should be highly bullish for gold in the long term.

- On balance, gold is inferior to inflation-linked bonds, which offer high yields and less downside risk.

Gold continues to trade at a large premium to levels implied by still-high real yields, in part reflecting its response to the Israel-Hamas war, which suggests downside risks dominate in the near term even after last week's sharp drop in yields. Longer term, high government debt will necessitate significantly lower real interest rates, which should be highly bullish for gold prices, but the metal still seems like an inferior asset to inflation-linked bonds at current yields.

A Refresher On The Key Drivers Of Gold Prices

Gold is money, and government liabilities in the form of cash and bonds compete with it as a store of value. Over the long term both gold and cash tend to rise by the rate of nominal GDP, the former due to rising demand for the metal and the latter from interest payments, which tend to track the pace of economic growth. Gold is preferable to cash when real GDP growth is expected to decline as this means the real yield on cash should decline, reducing the opportunity cost of holding gold.

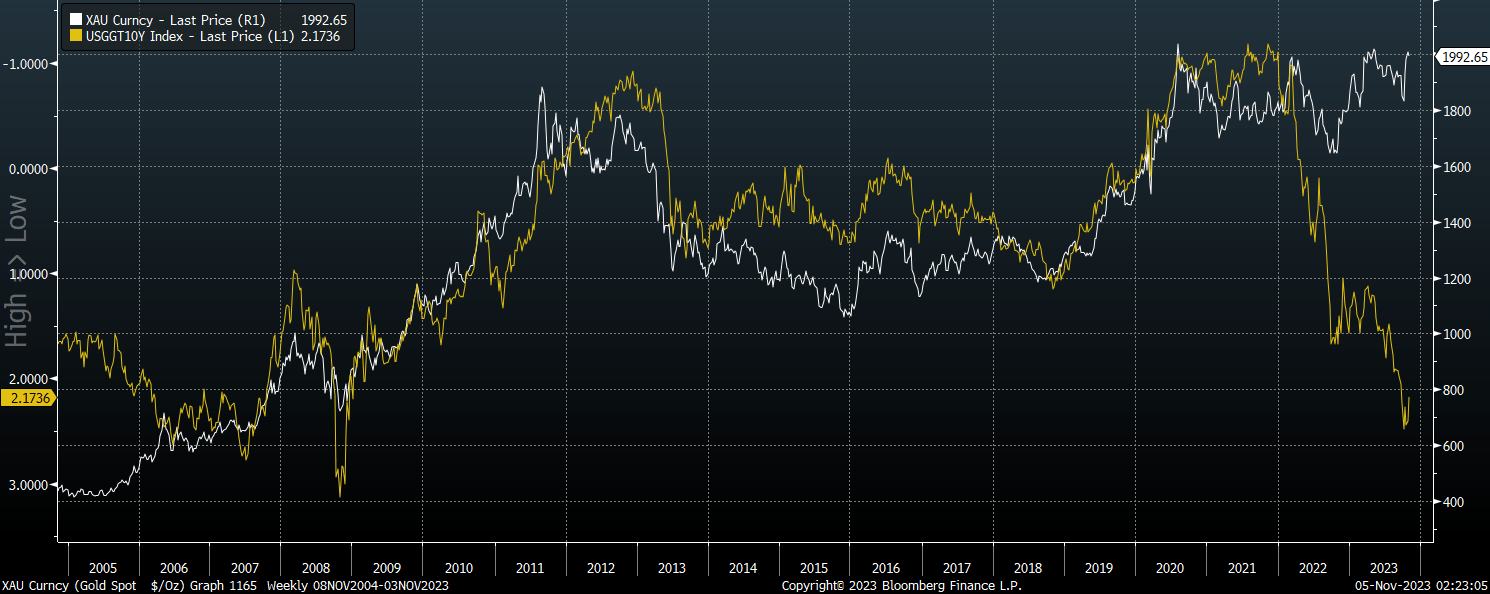

This explains the close inverse correlation between gold and the yield on 10-year inflation-linked bonds, at least prior to 2023. Typically, when investors expect cash to earn less in real terms in the future, the fair value of gold rises, and vice versa.

{kind=link}

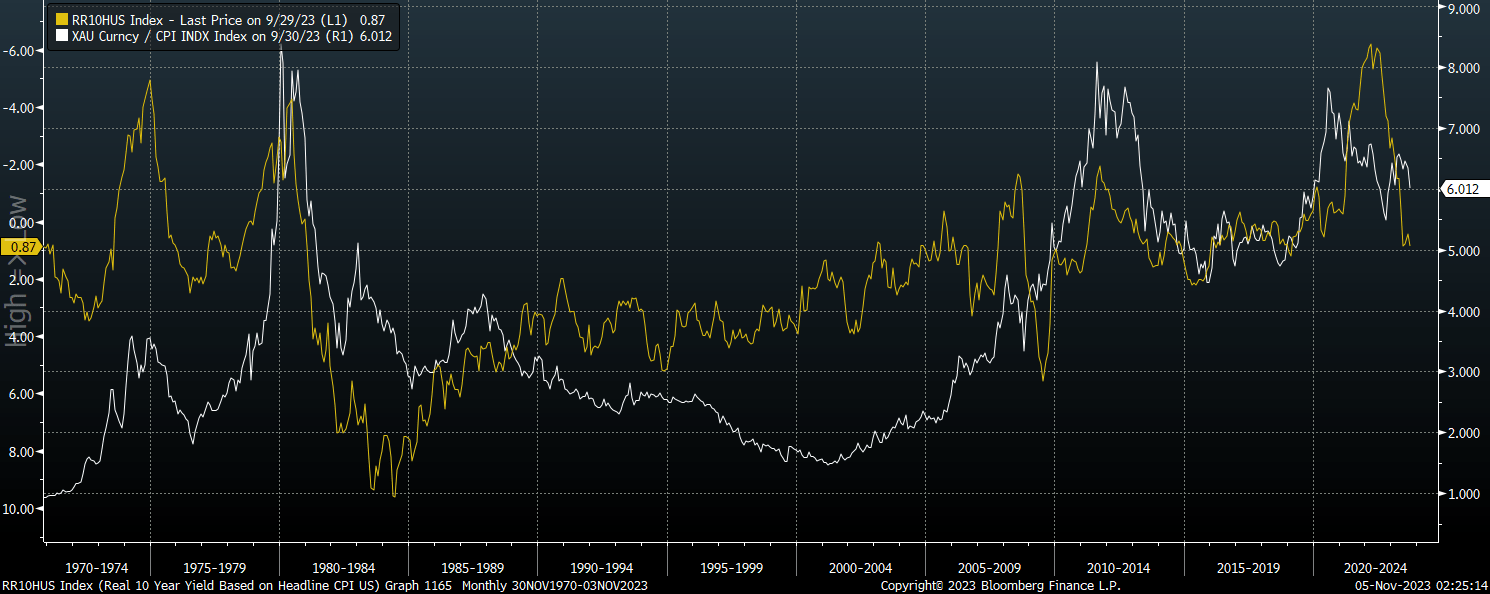

While 10-year inflation-linked bond yields only go back to 1997, the relationship can also be seen when comparing gold to real yields based on trailing headline inflation rather than long-term inflation expectations. Gold responded extremely well to the collapse in real yields in the early and late 1970s before collapsing in response to aggressive fed tightening.

{kind=link}

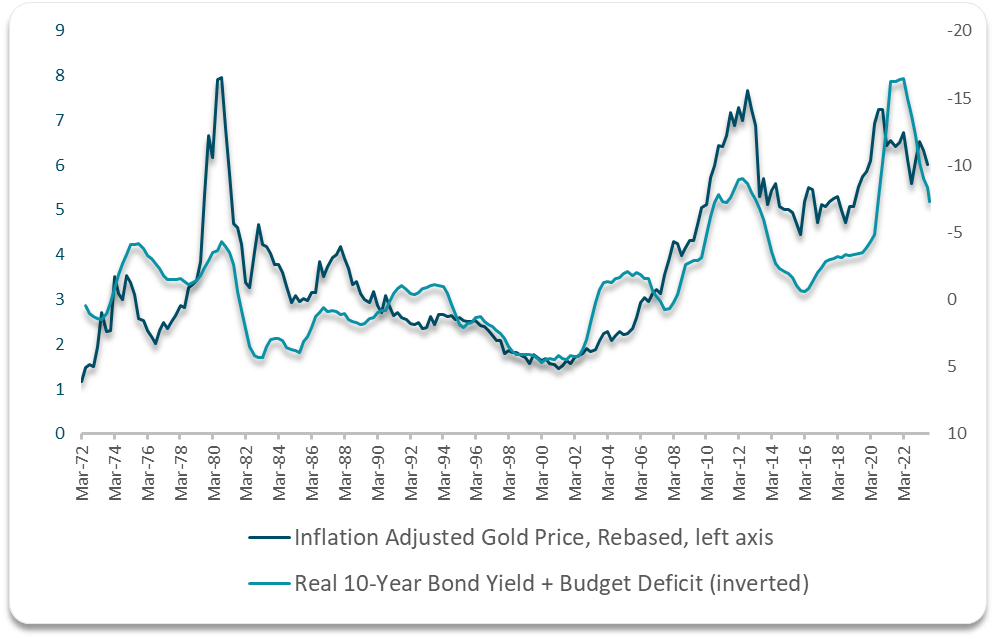

The decline in real gold prices in the 1980s and 1990s, despite a gradual move lower in real yields likely reflects declining long term inflation expectations caused by the shift from budget deficits to surpluses by the early-2000s. When we combine the impact of inflation-adjusted bond yields with the fiscal deficit, its correlation with gold improved greatly. The chart below shows the inflation-adjusted gold price alongside the sum of real 10-year bond yields and the budget deficit on an inverted scale.

{kind=link}

The War Premium And Last Week's Real Yield Reversal

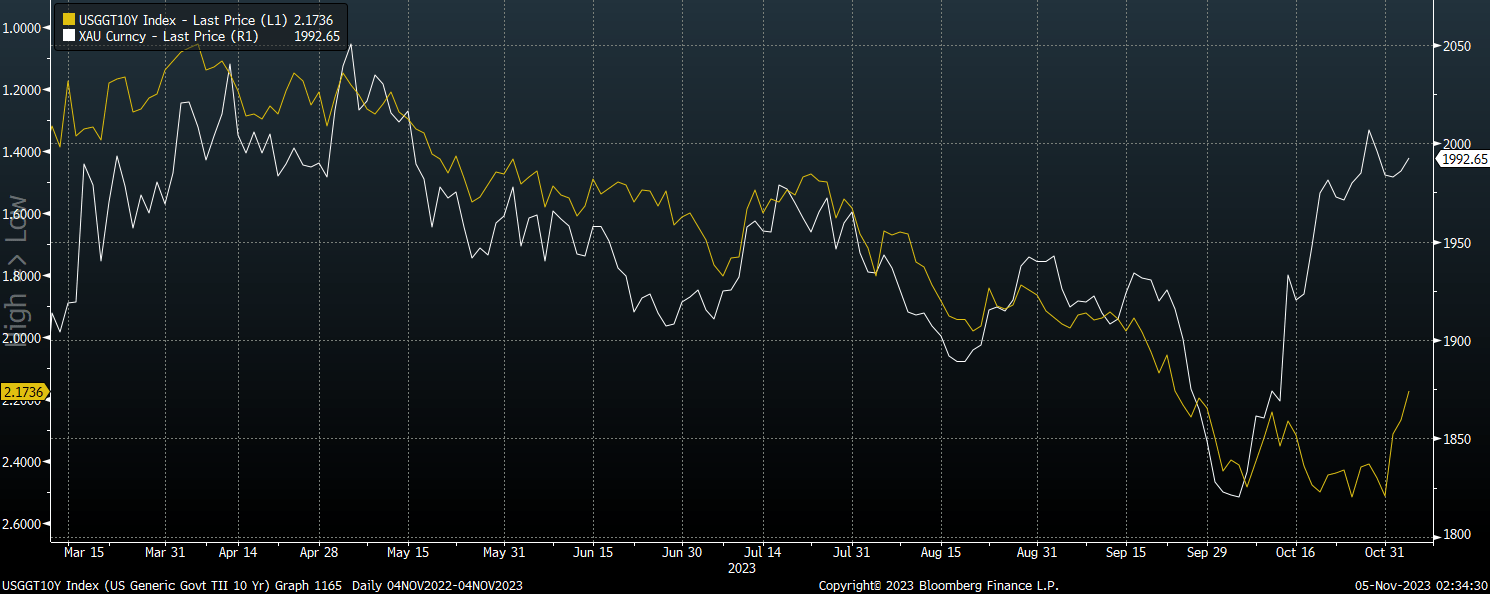

Gold had been suffering under the weight of rising real US Treasury yields before the October 7 Hamas terror attacks triggered an outsized rally in the metal. The reason gold prices deserve to rally on the onset of war is due to the expected impact on real yields. Rising oil prices and the impact of rising military spending driving on the fiscal deficit should theoretically drive down real bond yields, but they continued to move higher in response to Fed hiking fears. As we have seen over the past few years, gold price spikes that are not confirmed by declines in real yields tend not to last, and until last week gold looked extremely overvalued relative to the lofty real yields available on bonds. That was until a combined dovish Fed meeting and nonfarm payrolls miss drove a major reversal in real yields, with 10-year yields dropping 33bps. The key question now is whether real yields continue their downside reversal, providing support for gold to break higher, or remain near their highs, causing gold to head back towards its October lows.

{kind=link}

Inferior To Inflation-Linked Bonds At These Yields

From a short-term perspective, I think the risks outweigh the reward. The recent drop in real yields reflects widespread expectations of rate cuts starting in 2024, which have been made less likely by the strong recovery in risk appetite since their decline, which has dramatically eased financial conditions. This raises the risk of a gold price fall in the short term.

From a long-term perspective, however, gold stands to benefit from the ongoing deterioration in the US economy, most notably in terms of its fiscal health. To prevent Treasury funding costs from rising out of control amid rising interest costs and huge primary deficits, I would not be surprised to see real yields move back into negative territory over the next few years, driving up gold prices as we have seen in the past.

{kind=link}

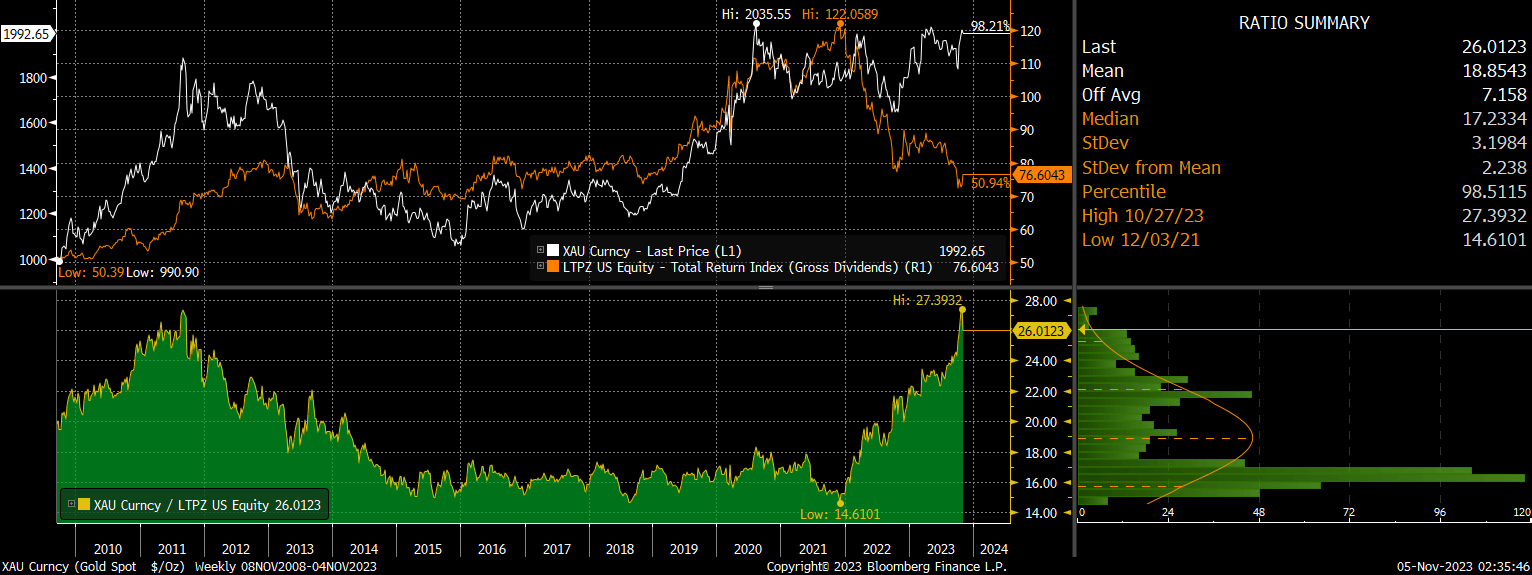

That said, anyone looking to gold as a bet on lower real bond yields is better off buying inflation-linked bonds themselves in my view, which offer high real yields and much less downside risk in the event of loss of the 'war premium' resulting from a return to some form of stability in the Middle East. The PIMCO 15+ Year US TIPS ETF (LTPZ), for instance, has similar volatility as gold and has moved closely in line with gold since its inception in 2009 and pays a yield of 2.5% over and above the inflation rate.

For further details see:

War, The Fed, And The Outlook For Gold