REYN - WD-40 Company: Even A Stellar Quarter Can't Grease These Wheels

2024-01-10 07:40:00 ET

Summary

- WD-40 Company reported strong financial results for the first quarter of its 2024 fiscal year, exceeding forecasts and reiterating guidance.

- Revenue increased by 12.4% and earnings per share jumped to $1.28, beating analysts' expectations.

- Despite the positive results, WDFC stock is considered expensive and may require a pessimistic outlook if it continues to climb.

January 9th ended up being a very positive day for shareholders of WD-40 Company ( WDFC ). The company, well known for its flagship product, WD-40, reported financial results covering the first quarter of its 2024 fiscal year. This data came out after the market closed. With management exceeding forecasts on both the top and bottom lines and reiterating guidance for the 2024 fiscal year in its entirety, shares of the business shot up almost 7%. While this is great news for investors in the firm, the stock truly is looking rather expensive. Even without factoring this after hours move, shares are trading at multiples that simply don't make sense. Multiples for the company at this time are not at their all-time highs. But they aren't far off. And while I would not go so far as to rate a high-quality company a ‘sell’, I do think that if the stock continues to climb, such a pessimistic outlook might be necessary.

A great quarter

In many respects, I have been a fan of WD-40 Company for a long time. I love quality companies, particularly those that either have a single product or that rely largely on a single product. But as an investor, I have not been able to get behind the stock in a supportive way recently. As an example, back in March of 2023, I wrote an article about the firm wherein I talked about the pain the enterprise had seen leading up to that point. I acknowledged how optimistic management was for the then-current 2023 fiscal year. But because of how expensive shares were, I ended up rating the company a ‘hold’ to reflect my view that the stock would be unlikely to outperform the market for the foreseeable future. So far, I have been proven wrong. While the S&P 500 has jumped 21.4% since then, shares of WD-40 Company have skyrocketed 38.8%.

{kind=link}

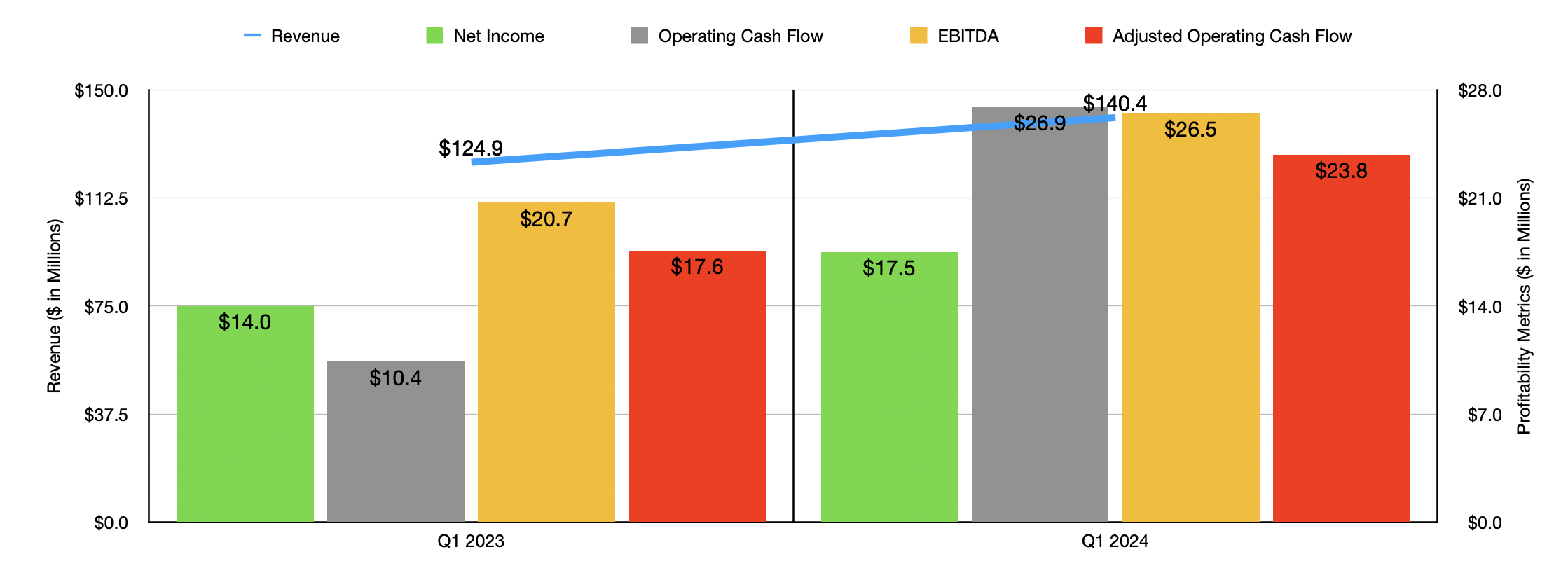

Once again, this upside does not factor in the after-hours move on January 9th. I can certainly understand why investors would be excited. Take, as an example, revenue for the first quarter of 2024. Total sales for the business were $140.4 million. That represents an increase of 12.4% over the $124.9 million the company generated the same time one year earlier. Sales also came in $6 million higher than what analysts anticipated . The vast majority of this increase was attributable to the company’s core WD-40 Multi-Use Product. Revenue for this category jumped 13.8% from $94.6 million to $107.7 million. In the US and Latin America, sales increased because of higher volume thanks to robust demand from customers. But in the EIMEA (Europe, India, Middle East, and Africa) regions sales growth was driven not just by higher volumes, but also by strategic price increases implemented by management.

{kind=link}

There is another lens through which to view this data. And that involves a focus only on components that make up the company’s geographic results. In the Americas, for instance, total revenue benefited to the tune of $1.8 million because of average higher selling prices and by $3.6 million because of increased volumes. Foreign currency impacted the company positively to the tune of $0.7 million. In the EIMEA region, higher sales volume helped the company to the tune of $3.7 million, while higher average selling prices helped by $0.7 million. Another big driver on this front was a $3.6 million benefit from foreign currency fluctuations. In the Asia Pacific region, meanwhile, foreign currency fluctuations hit sales negatively to the tune of $0.4 million, while average selling price increases pushed revenue up by $1.6 million and volumes pushed sales up $0.3 million.

The rise in revenue for the company pushed profits up as well. Earnings per share jumped to $1.28. That compares to the $1.02 per share reported the same time one year ago. This translated to net profits climbing from $14 million to $17.5 million. What makes this particularly interesting is that management exceeded analysts’ forecasts by $0.28 per share. Other profitability metrics for the company performed even better. Operating cash flow, for starters, nearly tripled from $10.4 million to $26.9 million. If we adjust for changes in working capital, it rose from $17.6 million to $23.8 million. Meanwhile, EBITDA for the firm came in at $26.5 million. That's comfortably above the $20.7 million reported for the first quarter of 2023.

{kind=link}

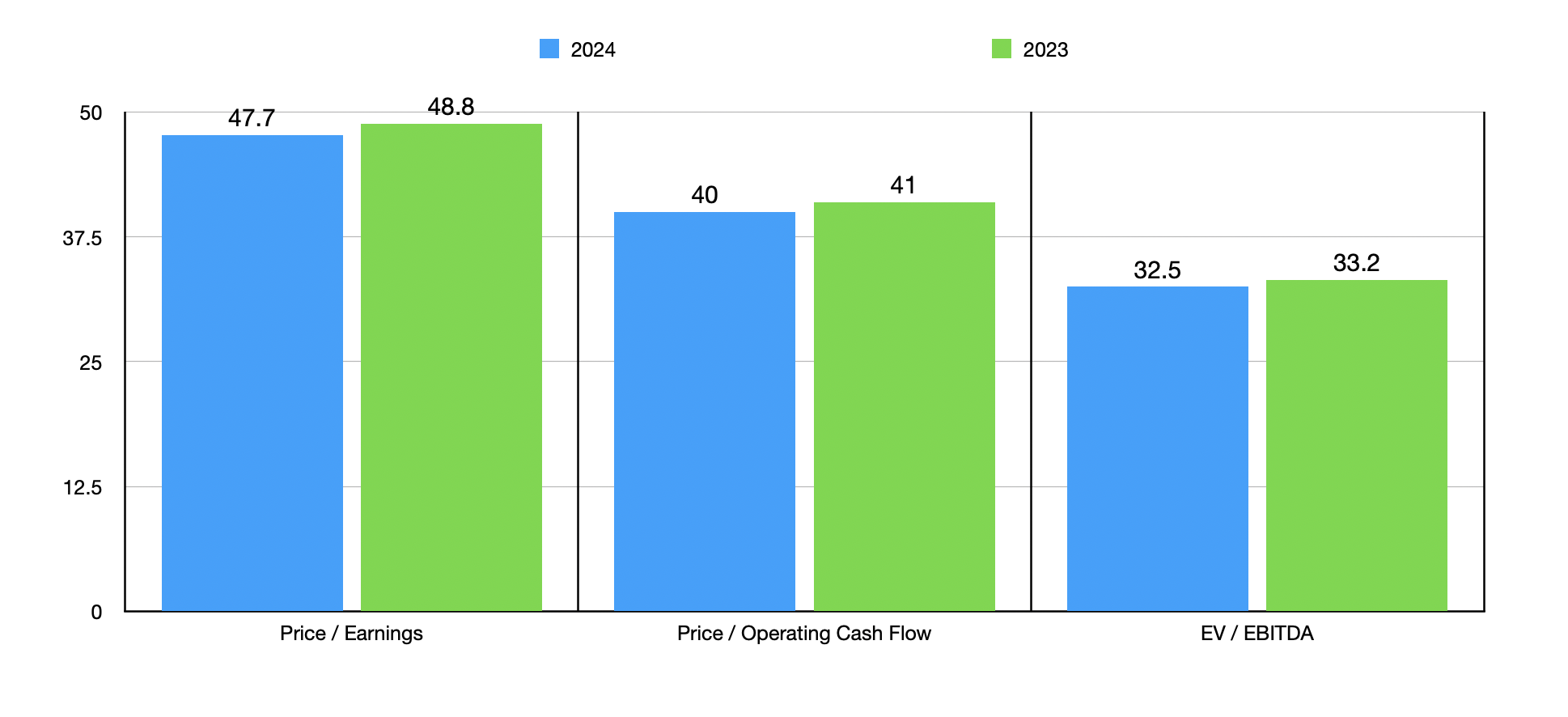

When it comes to the 2024 fiscal year in its entirety, management reiterated prior guidance that revenue should be between $570 million and $600 million. Net profits are expected to come in at between $65 million and $70 million. If we assume a similar growth rate for other profitability metrics, then we should anticipate adjusted operating cash flow for the year of $80.4 million and EBITDA of approximately $100.9 million. As part of my analysis, I then took these figures, as well as data from 2023, and valued the company as shown in the chart above. Shares look very expensive no matter the lens that we look at them through, especially on a price to earnings basis. If the business were growing rapidly, that might be a different story. But that is not the case. But it’s not alone. In the table below, I compared the company to five similar firms. Although it was the most expensive of the group on a price to operating cash flow approach, one company was more expensive than it when it came to earnings, while two were more expensive on an EV to EBITDA basis.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| WD-40 Company |

| 48.8 |

| 41.0 |

| 33.2 |

| Energizer Holdings ( ENR ) |

| 16.2 |

| 5.8 |

| 11.5 |

| Spectrum Brands Holdings ( SPB ) |

| 1.8 |

| 16.9 |

| 153.8 |

| Central Garden & Pet Company ( CENT ) |

| 20.7 |

| 6.8 |

| 10.9 |

| Reynolds Consumer Products ( REYN ) |

| 21.3 |

| 10.9 |

| 12.6 |

| The Clorox Company ( CLX ) |

| 207.8 |

| 17.6 |

| 41.8 |

The fact that there are similar firms that are more expensive than WD-40 Company is likely one of the reasons why the stock can remain at such lofty multiples to begin with. But there are probably other contributors as well. As an example, in the chart below, you can see that while shares are expensive, they aren't at their all-time highs. As a note, I wanted to include the price to operating cash flow multiple on this chart. But I could not because a single massive spike caused the scaling of the chart to look absurd, with the other two lines appearing virtually flat as a result. But I digress. Adding to the optimism is also likely the fact that management, for the most recent dividend, hiked the payout by 6% on a per share basis year over year. On top of this, last year, the company announced a new $50 million share buyback program. And from its effective date on September 1st through the end of the first quarter of this year, management repurchased $2.4 million worth of units. This optimism in management to buy back the stock, even though it is very expensive, certainly has sat well with shareholders.

Takeaway

In the long run, I fully expect that WD-40 Company will go on to generate attractive cash flow growth. But as things stand, I cannot get behind the stock. Yes, management exceeded forecasts and reiterated guidance for 2024. That is all great news. But the thought of paying 30 to 50 times cash flows or earnings, especially when growth is nowhere near meteoric, is foreign to me. Given these factors, I do believe that the ‘hold’ rating still applies to the business. But if shares do climb much further, a downgrade to something more bearish could be in the cards.

For further details see:

WD-40 Company: Even A Stellar Quarter Can't Grease These Wheels