NPFD - Weekly CEF Commentary | Dec 3 2023 | CEF Discounts Take A Breather

2023-12-08 08:30:00 ET

Summary

- November saw strong performance in equity and fixed income markets, with the S&P 500 rising 9% and the Bloomberg US aggregate bond index rising 4.5%.

- Economic data shows a slowdown, with the PCE index rising 0.2% and continuing jobless claims hitting a 2-year-high.

- Fed Chair Powell suggests that rate increases may not be over and that the economy has not yet felt the full impact of past rate hikes.

- FS Credit Opps (FSCO). The shares rallied big on Friday, perhaps in anticipation of a distribution hike. However, the release is typically around the 8th to 10th of the month.

- We discuss holding individual bonds and the mentality one should subscribe to when investing in them. They should be buy and forget as we know the return we will achieve if held to maturity.

(We publish this weekly commentary every Sunday)

Macro Picture

We closed out November on a strong note, with markets broadly rising. The S&P 500 rose a bit over 9% on the month, while the Bloomberg US aggregate bond index rose just over 4.5%, its best month since May 1985. Commodities were the only asset class to lose ground in November, led by a 6% decline in oil prices. The combination of strong equity and fixed income performance lifted the Bloomberg 60/40 index by 7.5% last month.

The economic data this week confirmed the 'pause' with the PCE index rising just 0.2% m/m and +3.5% y/y. That was down from +0.3% and +3.7%, in September.

We also had continuing jobless claims hit a 2-year high at 1.93m, showing possible future softness in the labor market.

Personal spending rose 0.2% in September, its smallest increase in six months, while personal incomes rose at the same pace.

Powell said on Friday that it is premature to speculate on when the Fed may ease policy, adding that the central bank is prepared to tighten more if it becomes appropriate and that policy is now well into restrictive territory. The Fed chair said it would be premature to conclude with confidence that rate increases are over, though he noted that the economy has not yet felt the full impact of past rate hikes.

The comments helped push the yield on the 10-yr down to 4.21%, an almost 3-month low.

Mohamed El-Erian summed it up in his opinion article :

This extraordinary November was propelled by four key factors: Goldilocks economic data, declining yields, falling oil prices, and a surge in the deployment of cash sitting on the sidelines. Together, they created an unusual convergence of the three primary risk factors shaping market returns and correlations. Extrapolating all this forward, however, is subject to important qualifications that might well be underestimated during a period of understandable euphoria.

Lplblog.com

CEF Market Review

{kind=link}

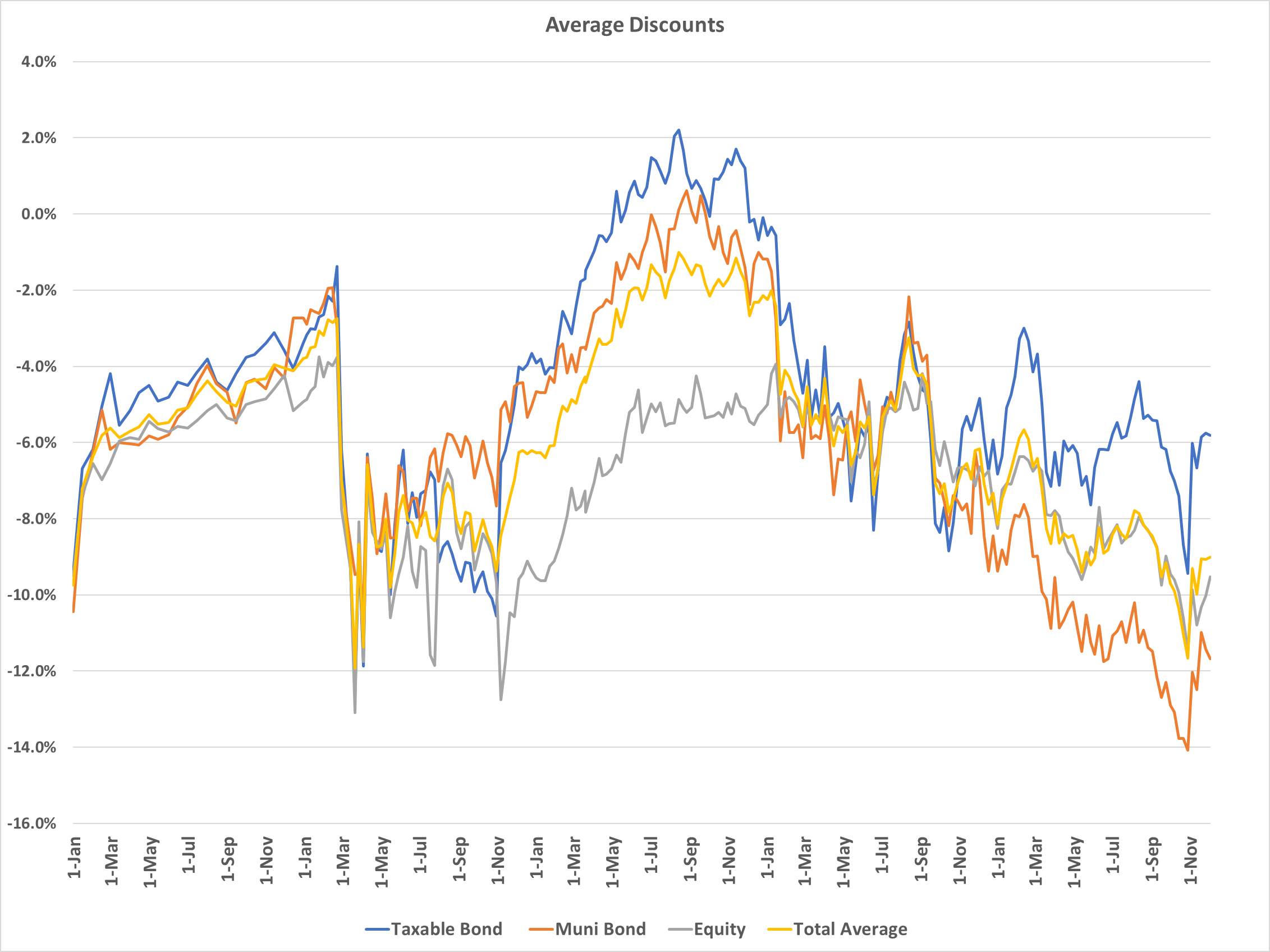

Since 5 weeks ago, when discounts peaked at their widest levels of the cycle, we've seen significant buying activity as CEF investors feel that the Fed is giving them the "all-clear" on rates.

However, discount tightening on taxables has stabilized in the last three weeks around -5.8% with munis around -11.5% discounts. It wouldn't surprise me to see discounts widen out a bit from here as we get a bit more tax loss selling pressure in December.

alpha gen capital

Overall, taxable discounts remain fairly wide at the 77th percentile, while munis remain at the 99th percentile.

The only sector that was down on price last week was Emerging Market Equity, down about 70 bps. All other sectors rose on price with real estate, MLPs, and equities doing the best and munis not far behind.

alpha gen capital

Muni CEF NAVs were up about 2.5% across the board, another strong week for them. Over the trailing month, muni CEF NAVs were up over 10%. Only real estate has done better, at +14%.

So should you buy here after the big move?

Let's walk through the drivers of muni CEF returns first.

1) Long term rates: The 10-year yield falling means the bond price moves up, which is pushing up NAVs. Prices then follow. Even without the wide discount closing, you still see a gain. This is what we saw this month.

2) Short-Term Rates: This is controlled by the Fed. When the Fed lowers rates, leveraged funds can earn a spread again. Net investment income increases, distributions go up, investors are attracted, and prices go up.

Hard to see when number two happens. The market is pricing in 100 bps of cuts for 2024. That's a start but doesn't get us even near where we were two years ago in terms of the spread earned by CEFs.

Additionally, I think the market is pricing in too many cuts too soon, which means that the benefit from this is really a 2025 event.

On the first point, I think we've seen the benefit of the 'pause' and may even have realized some of the 'pivot' in terms of long-rates coming down. The 10-yr has come down a whopping 80 bps in a month. That typically only happens when something breaks and a recession is inevitable. We are not there yet.

The question then becomes will discounts tighten up? Without the second point occurring, I have a hard time envisioning much closure of the discount. The only thing we have to look towards is the January Effect, which is an annual phenomenon where discounts tighten up a bit.

In summary, I think muni CEFs have rallied nicely off the bottom and completed some of their slingshot back. However, they have a ways to go but it remains unclear whether the ingredients are all there for the rest of the rebound.

In my portfolio, I remain long an array of muni CEFs - some buy-and-rent and some tactical to play the January Effect. MMD, VFL, ETX, BMN, MUI, RMMZ, NBH, BFK, NMZ, MVF are the largest positions for those that want to piggyback.

Below is the 3-year muni CEF index. You can see the move in the last month is but a small climb of the loss we saw. Thus, there is room to run.

ycharts

Moving on to the other big story maker this week, FS Credit Opps ( FSCO ) . The shares rallied big on Friday, perhaps in anticipation of a distribution hike. However, FSCOs press release on their distributions typically occur around the 10th of the month, so we have to wait another week or so to see if they hike.

The price hit $6.00 per share on Friday afternoon relative to a NAV of $7.01, or a -16% discount. It did trigger some sell orders that I had out there, and roughly one-third of my position was gone by the end of the day.

I still think FSCO has room to run. For me, the position was my largest among all CEFs, taxable or muni, by a decent margin too. I was happy to reduce it to get it more in line with my risk bands.

For those with smaller positions, I would keep an eye on it but not be in a large hurry to sell. I think we could see more tightening of the discount over the next two months, especially if they raise the distribution, which I believe to be a high probability.

FSCO discount chart:

cefconnect

Lastly, PIMCO Dynamic Income Strategy ( PDX ) announced their January distribution, which was a bit of a disappointment given that they kept the quarterly schedule, for now, and didn't raise. We will see what comes out of PIMCO in January with regard to this fund.

My theory is that they continue to hold about 30%+ in equity MLPs (which pay quarterly divs) and would rather keep that kind of distribution frequency for now. Given the new mandate for the Fed whereby 25% or more will always be allocated to the energy sector, this could be the case perpetually. However, I doubt it.

The discount has closed nicely in the last several of months since the announcement. Since May, the discount has closed about 7 points. It will need that distribution catalyst to further close.

A couple of "safer" CEF options that I would look at here:

- First Trust Mortgage Income Fund ( FMY ) , discount -8%, yield 8.82%

- BNY Mellon Alcentra Global Credit Income 2024 ( DCF ) , discount -5.13%, yield 5.28%.

- Black R ock 2037 Muni Target Term ( BMN ) , discount -6.83%, yield 4.69%

- Putnam Muni Opps ( PMO ) , discount -9.6%, yield 4.20%, chart below:

cefconnect

Commentary

Individual bonds have rallied sharply in the last month. Some of my positions are up over 8% in just 5 weeks time. However, while it feels good, it doesn't matter. These are buy-and-HOLD positions. We are intent on holding to maturity, even if the maturity date is beyond our likely lifetime.

The benefit of individual bonds are that we know the return we will achieve the day we buy them. This is true even on a 30-year bond. Bond math is easy and that YTM will be very close to your total annual return achieved. This is a HUGE benefit of owning bonds.

While there is a quantitative benefit, there is also a massive qualitative one. The fact that you can buy these individual bonds and 'forget about them' provides an unquantifiable psychological benefit to the investor. That sleep well at night factor is huge and cannot be understated, especially for those investors who tend to squirm at market volatility.

This was from the chat feature on Seeking Alpha:

{kind=link}

"All I care about is the income."

This is the type of thinking I want all of the newbie individual bond investors to subscribe to.

It can be hard as the brokerage sites tend to show every bp of change in each position every second. I know some investors who have their individual bonds in other accounts - they open a separate account for the sole purpose of housing their individual bonds- just so they don't see the marks/changes in price.

CEF News and Corporate Actions

Distribution Increase

JH Income Sec ( JHS ): +47.1% to $0.1277

Invesco Bond ( VBF ): +46.1% to $0.0992

Nuveen Multi-Asset Inc ( NMAI ): +33.3% to $0.40

JH Investor ( JHI ): +27.1% to $0.2648

Nuveen Real Asset ( JRI ): +14.9% to $0.10

Nuveen Pref & Inc Opp (JPC): +13.4% to $0.0475

Royce Value Tr ( RVT ): +11.5% to $0.29

EV Sr Income ( EVF ): +8.9% to $0.061

Nuveen Variable Rate Pref & Inc ( NPFD ): +8.1% to $0.0935

Nuveen Taxable Muni ( NBB ): +8.1% to $0.0735

Nuveen Muni Inc ( NMI ): +7.9% to $0.034

Nuveen CA Select Tax- Free Inc ( NXC ): +4.6% to $0.0455

EV Limited Dur Inc ( EVV ): +4% to $0.0779

MFS Interm High Income ( CIF ): +3.4% to $0.01411

EV Short Dur Div Inc ( EVG ): +3.2% to $0.0768

Distribution Decrease

N/A

Special Distribution

DoubleLine Yield Opps ( DLY ): $0.063

AB Global High Inc ( AWF ): $0.0209

Distribution Change

OFS Credit Company ( OCCI ): The CLO changed the distribution from quarterly to monthly and reduced the rate to $0.10, or 30c per quarter from 55c previously.

Activism

Saba bought additional shares of: MAV, NMAI, VTN, VPV, ENY, KSM, BIGZ, BMEZ, ECAT, BCAT, BFZ, DMF, ASA, EMO, CEM, CTR, CEV

Bulldog: Bought more NDP , Tortoise Energy Independence

For further details see:

Weekly CEF Commentary | Dec 3, 2023 | CEF Discounts Take A Breather