CUBA - Weekly Commentary | Dec 17 2023 | How To Identify If Low Coverage Ratios Are A Red Flag

2023-12-25 07:00:00 ET

Summary

- Fed signals more rate cuts for 2024, leading to a melt-up in risk assets and new all-time highs for Dow Jones.

- Inflation remains steady, with producer prices rising at the slowest pace in three years and core inflation running at 2.0% for the year.

- Money is flowing out of short bonds and into longer-dated maturities, creating opportunities to lock in yields with individual bonds.

- I remain high on Templeton Global Income Fund, soon to be Saba Capital Inc & Opps II. I have been nibbling on shares here and there with excess cash on the notion that Saba Capital does something to monetize that discount.

- In general, the NAV contains all the information you need to know about the fund. A rising NAV can heal a lot of bad things that may have occurred, as it gives the fund leeway to add leverage.

Macro Picture

The melt-up in risk assets continues, with the Fed throwing a bit of gasoline on the fire. Fed Chair Jerome Powell came out and signaled - really for the first time - more substantial rate cuts for 2024. That helped the Dow Jones (DJI) reach a new all-time high and left the S&P 500 (SP500) not far from the same feat.

ycharts

"The inflation story is over" was the title of a Bloomberg article last week after producer prices rose at the slowest pace in three years. Tuesday's report on consumer price inflation was roughly in line with estimates, with core (excluding food and energy) inflation staying steady at a year-over-year rate of 4.0%.

Wednesday's producer price inflation report surprised modestly on the downside, with core inflation running at 2.0% for the year, a tick below expectations and its lowest level since January 2021.

Money is flowing out of short-bonds and into longer dated maturities.

{kind=link}

This is something we've been pushing for many months now - admittingly a bit too soon, earlier this year. However, by locking in these yields with individual bonds, we have taken advantage of the higher rates and locked those in for many years.

The 10-yr (US10Y) is already down more than 100 bps from the peak set only 6 weeks ago. I think there is still time to lock in yields. You have not missed the boat. Rates are only back to where they are in June. This is why we have advocated slowly legging into individual bonds in order to blend the yield into the portfolio.

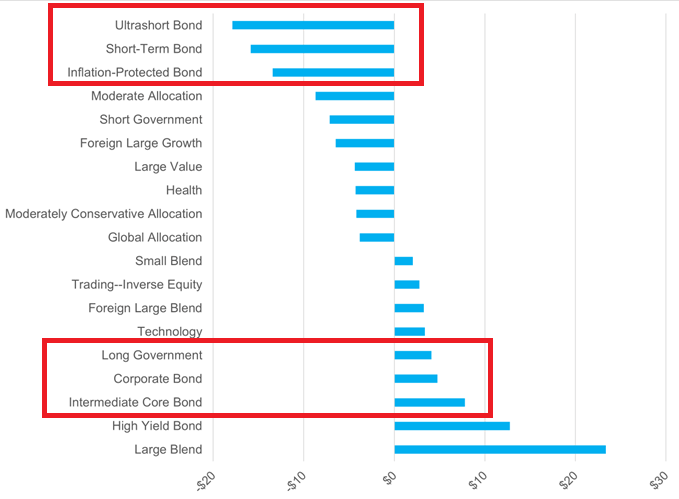

CEF Market Review

{kind=link}

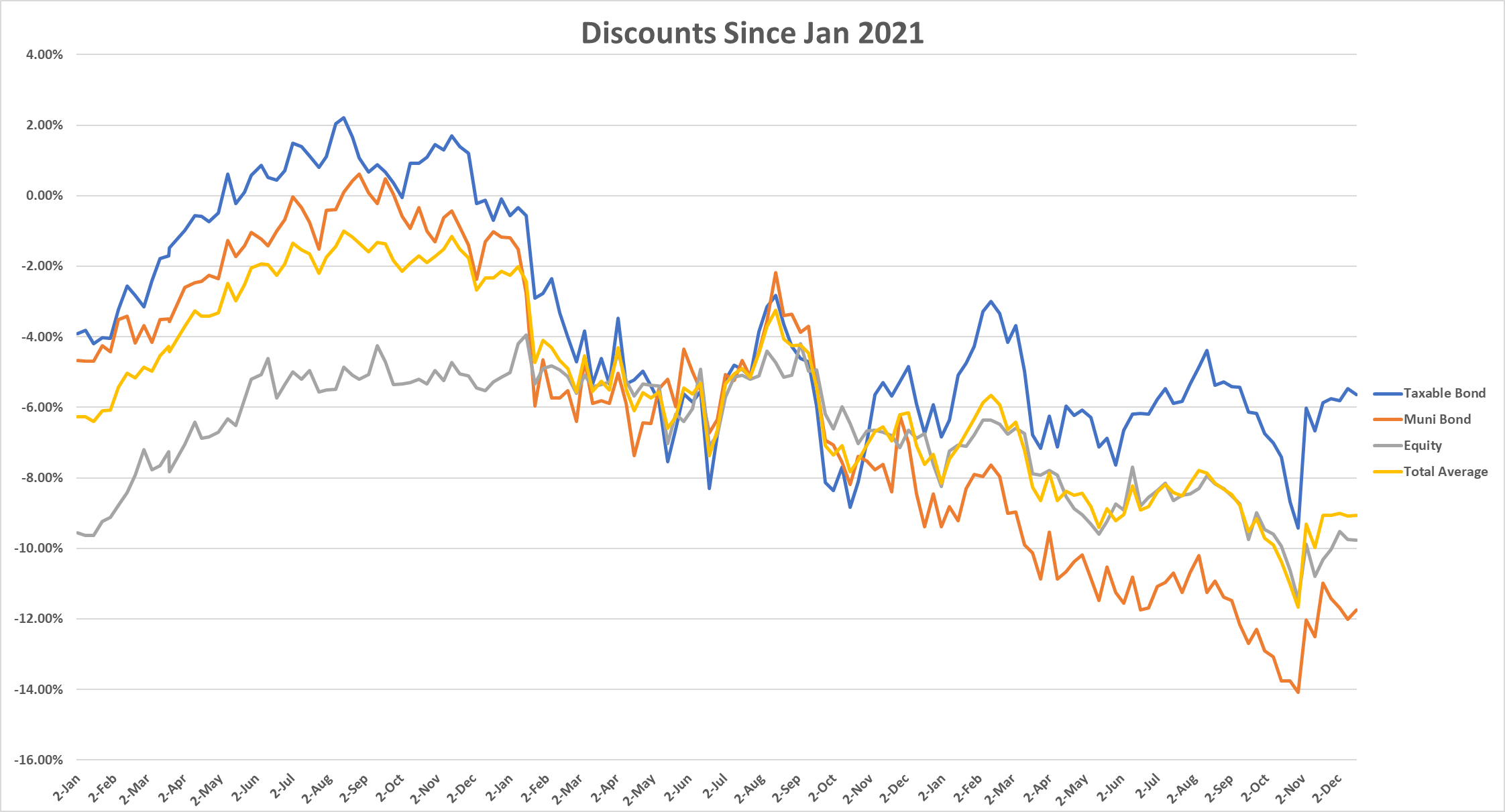

Discounts continue to trade sideways after the large rally of a couple months ago. Taxables are at -5.6%, roughly the 72nd percentile meaning 72% of the time, they are tighter.

Muni CEFs are STILL in the 99th percentile, so they have literally gained nothing in discount return since the pivot. All the gains have come from NAVs rising as interest rates have fallen.

Using the VanEck CEF Municipal Income ETF ( XMPT ) of muni CEFs as a proxy for muni CEF NAVs, we can see that they've gained about 16% since the end of October- an incredible move.

ycharts

Looking at sectors, all are up nicely in the last month as this rally has been broad. However, the best performers have been those interest rate sensitive areas like real estate (+11.5%), taxable munis (+8.5%), tax-free munis (+7.3%), and agency MBS (+5.5%).

We discussed floating rate loans recently as lower short rates will affect them with lower coupons in the future. We noted that this will be ways down the road given the lag effect between rate changes and coupons. That said, money is flowing out of the space resulting in the loan CEF NAV return to be just +2% in the last month, the lowest except for MLPs.

I have noted several times in the last couple of months of my reduced allocation to floaters simply because of the pivot. This is why the macro is important as it dictates the sectors we want to focus on and overweight.

For many months, we've been pushing longer-duration, higher-quality including munis, preferreds, investment grade corporates, and agency MBS as these are the areas that would benefit from the Fed pivot.

I continue to get asked, is it too late to get into muni CEFs or agency MBS or real estate CEFs. My answer continues to be, "no."

The rebound, as we noted several times, would be sharp and like a "slingshot." That has happened, but we are really only back to where we were a few months ago in terms of rates and valuations.

The iShares iBoxx Investment Grade Bond ETF ( LQD ) is still more than -20% off the highs. Of course, for it to get to new highs, rates would need to go back to zero, which is highly unlikely, but it does show the potential for further gains as rates fall.

ycharts

The cheapest sectors are primarily munis and a few of the interest rate sensitive areas like mortgages and preferreds. Loans are actually one of the more expensive CEF sectors despite the narrative winds shifting.

We saw some decent movement again this past week in discounts/valuations reinforcing my view that this is a good environment for alpha swaps - the trading of more expensive CEFs in a sector for cheaper replacements in the same sector.

{kind=link}

I noted on First Trust Mortgage Income Fund ( FMY ) last week as the valuation became rich (though I noted I didn't sell). That discount has since widened back out with the NAV rising rapidly. This is obviously a good time to add to CEFs and I think FMY is a great place to put money for your 'safer' money. The fund is primarily agency MBS- very safe assets that are interest rate sensitive and will do well as rates fall.

CEFConnect

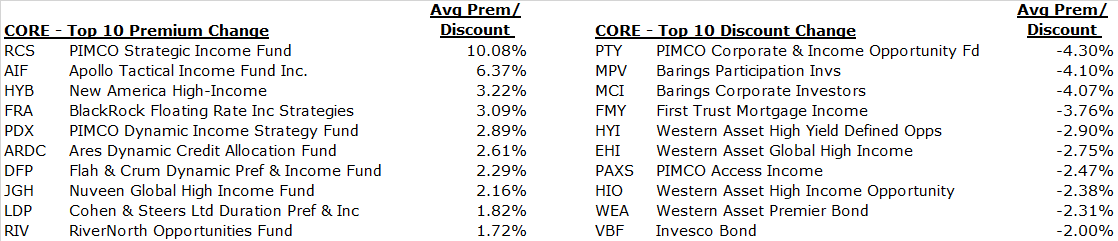

Among the PIMCOs, PDI remains decent here around a 5% premium, while my model suggests PDO is slightly overvalued and PAXS near fair value. PTY was the largest "loser" on the week, losing more than 4% in premium on the week. The fund is now around a 20.7% premium and closer to its long-term average. I would still focus on the lower premium names, especially as the January distribution announcement comes around when PIMCO has been known to make changes.

I remain high on Templeton Global Income Fund ( GIM ) , soon to be Saba Capital Inc & Opps II, trading under ticker SABA. I have been nibbling on shares here and there with excess cash on the notion that Saba does something to monetize that discount (even though they just concluded a tender offer). The shares are cheap and the transition to Saba occurs at year end.

On the expensive side, Apollo Tactical Income Fund ( AIF ) remains a sell as the share prices zoomed for reasons that escape me. The fund did end up raising the distribution but only mid single digits. Not enough to account for a nearly 7% discount return in a month.

CEFConnect

Had a few questions on Ares Dynamic Credit Allocation Fund ( ARDC ) which hit new highs last week. The fund is now sub-7% discount which is well inside the long-term average of -9.7%. The fund is mostly high yield bonds and floating rate loans. The CLO allocation remains near the highs that I can remember at ~30%. I would sell the shares here and rotate into something like Brookfield Real Assets Income Fund ( RA ) or First Trust HY Opportunities 2027 Term ( FTHY ) if you want to keep the same exposures. Otherwise, use the opportunity to reduce risk and go into something like BlackRock Taxable Muni ( BBN ).

A number of other funds that look like clear sells are: KIO, EFT, DSU, PHT, EFR, RCS, VVR, and BIT.

In munis, BlackRock 2037 Muni Target Term ( BMN ) remains my top pick and I added to it again this week. The discount is back out to -8.4% with a yield of 4.73% (CEFConnect is wrong).

Nuveen Muni High Income ( NMZ ) is another top pick and another added to this past week. The discount is nearing -9% which, historically, has been wide and a good area to add.

I also like Pioneer Muni High Income ( MIO ) in the high yield muni space at a -16.6% discount and 4.92% tax-free yield.

Lastly, MainStay MacKay DefinedTerm Municipal Opportunities Fund ( MMD ) remains in my buy zone at a -4.5% discount and 4.43% yield.

Eaton Vance Muni Inc 2028 Term ( ETX ) was one of my top picks last week and the week before and the discount tightened up back towards fair value. I would wait to buy more if the discount widens back out to -7.5% or -8% or wider.

Commentary

There was a question about the importance of coverage ratios and evaluating the long-term health of a CEF. Many investors think that a coverage ratio needs to be at 100% or greater in order for the CEF to be 'healthy.'

A distribution can be classified as any or all of the following:

- Ordinary income

- Short-term capital gains

- Long-term capital gains

- Return of Capital ("Roc").

In that last category, there are numerous sources of RoC distributions. It can be pass-through income from MLPs or option strategy funds, or div income from REITs.

It can be "constructive" as in from unrealized capital gains or it can be destructive from the cannabalization of holdings (selling shares of positions) that erodes the NAV of the fund.

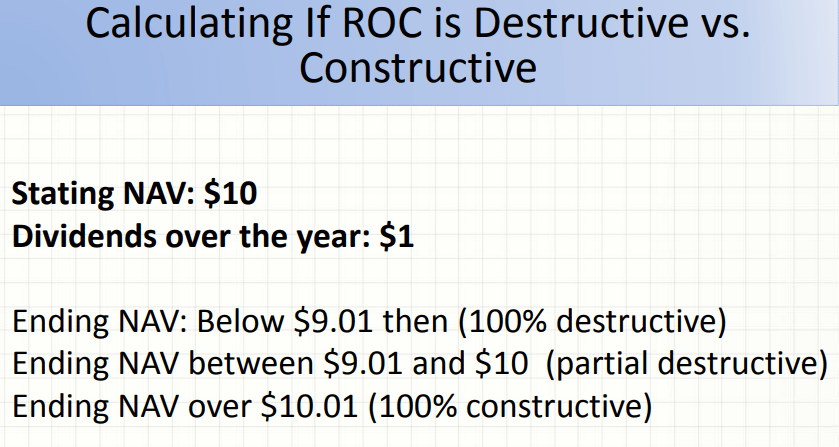

The best way to assess the health of a fund's distribution policy and sustainability is simply to look at the NAV. If the NAV is rising, than any RoC in the distribution is ok. If the NAV is in a sustained downturn, then the distribution is destructive.

Below is a simple example of that from CEFA:

{kind=link}

In general, the NAV contains all the information you need to know about the fund. A rising NAV can heal a lot of bad things that may have occurred as it gives the fund leeway to add leverage, which in turn adds more holdings, which then adds more net investment income, improving the coverage of the distribution.

CEF News and Corp Actions

Distribution Increase

abrdn National Muni Inc ( VFL ): +15.4% to $0.0375

Mexico Fund ( MXF ): +10% to $0.22

Apollo Tactical Inc ( AIF ): +6.4% to $0.133

Barings Part Investors ( MPV ): +2.94% to $0.35

Barings Corp Inv ( MCI ): +2.7% to $0.38

Apollo Sr Floating Rate ( AFT ): +1.5% to $0.137

Distribution Decrease

abrdn EM Equity Inc ( AEF ): -10% to $0.09

Blackstone Long-Short Credit Inc ( BGX ): -8.04% to $0.103

Blackstone Strategic Credit ( BGB ): -7.8% to $0.094

Blackstone Sr Floating Rate ( BSL ): -4.2% to $0.114

Special Distribution

TCW Strategic Inc ( TSI ): $0.115, payable 1/12/24

Nuveen Taxable Muni Inc ( NBB ): $0.4823, 12/26 ex date, 12/29 payable date

Nuveen Mortgage Opp ( JLS ): $0.0566 12/26 ex, 12/29 payable

Rights Offering

Herzfeld Caribbean Basin ( CUBA ): Subscription price= $2.35. 14,371,838 shares were requested to be tendered and 7,150,673 tendered.

NXG Cushing Midstream ( SRV ): Preliminary results showed 728,317 at a subscription price of $33.20.

Saba Activity

They bought a big chunk of BlackRock Innovation & Growth Trust ( BIGZ ) in the last week, adding nearly 600K shares and taking their ownership stake up to 17.4%.

They also added to BCAT and ECAT decently as well as they continue to attack Blackrock (I think for good reason too).

They also accumulated more ClearBridge Nrg Midstream Opp ( EMO ) and that position is now over 23%.

Saba is also going after Western Asset Intermediate Municipal ( SBI ) which is merging into sister fund, MMU. They accuse them of stripping voting rights from shareholders.

- The Court found such vote stripping to be in violation of the Section 18(i) of the Investment Company Act and ordered rescission of the provisions in question.

For further details see:

Weekly Commentary | Dec 17, 2023 | How To Identify If Low Coverage Ratios Are A Red Flag