WRDEF - Wereldhave Relative To 5 European REITs As Rates Peak

2023-07-31 05:38:33 ET

Summary

- Wereldhave cut its anticipated residential gains by 62%, from 1.60-1.85 to 0.5-0.8 EUR/share.

- Leverage has increased at all 6 REITs, driven by lower valuations and dividend payments. Occupancy likewise dropped across the board.

- Yields used for valuations were also higher at all companies except Wereldhave. The average market-implied yield jumped from 6.44% in February to 6.99% in July.

- Key risk for all companies is that valuation yields are well below market yields, hence creditors may demand additional equity injections;

- Peaking interest rates, recession resilience, and low sentiment make for a compelling risk-reward opportunity, with Mercialys the most attractively priced company.

Introduction

As semi-annual reports roll in, I wanted to write an update to my previous European REITs article which is available here and which provided a snapshot, as of year-end 2022, of Covivio (GSEFF), NSI ( NSI on Euronext), Mercialys (MEIYF), Wereldhave (WRDEF), Vastned ( VASTN on Euronext) and Cofinimmo (CFMOF).

In this article, I will pay special attention to Wereldhave as it disclosed a reduction in the anticipated residential gains.

Wereldhave operational overview

Wereldhave is focused on retail assets in the Netherlands, France, and Belgium, where it operates some offices as well:

{kind=link}

Wereldhave portfolio (Wereldhave H1 2023 Results Presentation)

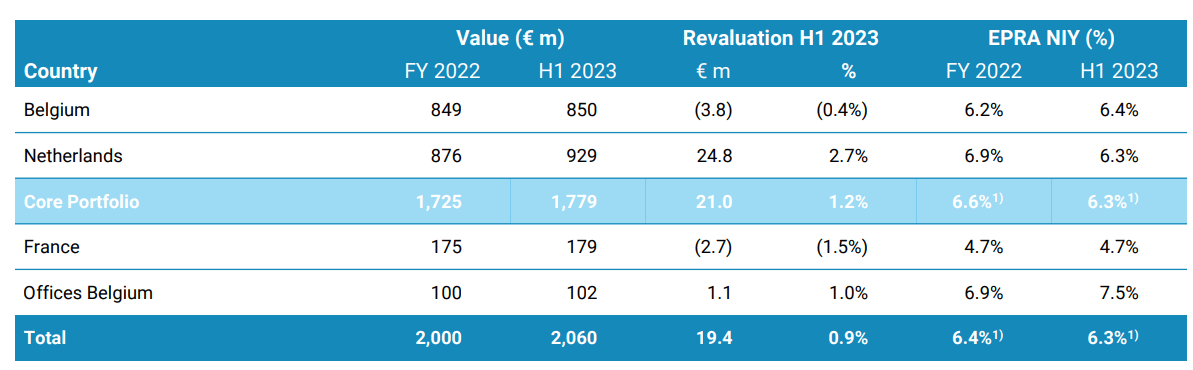

Looking at key performance indicators, here is what happened in H1 2023:

- The company confirmed its 1.65-1.75 EUR/share direct result outlook, with H1 2023 direct result coming in at 0.89 EUR/share, up 10% Y/Y.

- Leverage, as measured by net LTV , was up to 43.9% (year-end 2022 42.4%) as Wereldhave paid its dividend and continued to invest in its shopping centers.

- Occupancy was down 1% relative to year-end 2022 and now stands at 95.8%.

- The EPRA net initial yield was down 0.1% year-to-date to 6.3% on the back of valuation gains in the Netherlands.

- The average cost of debt is already at 3%, up from 2.5% at year-end 2022.

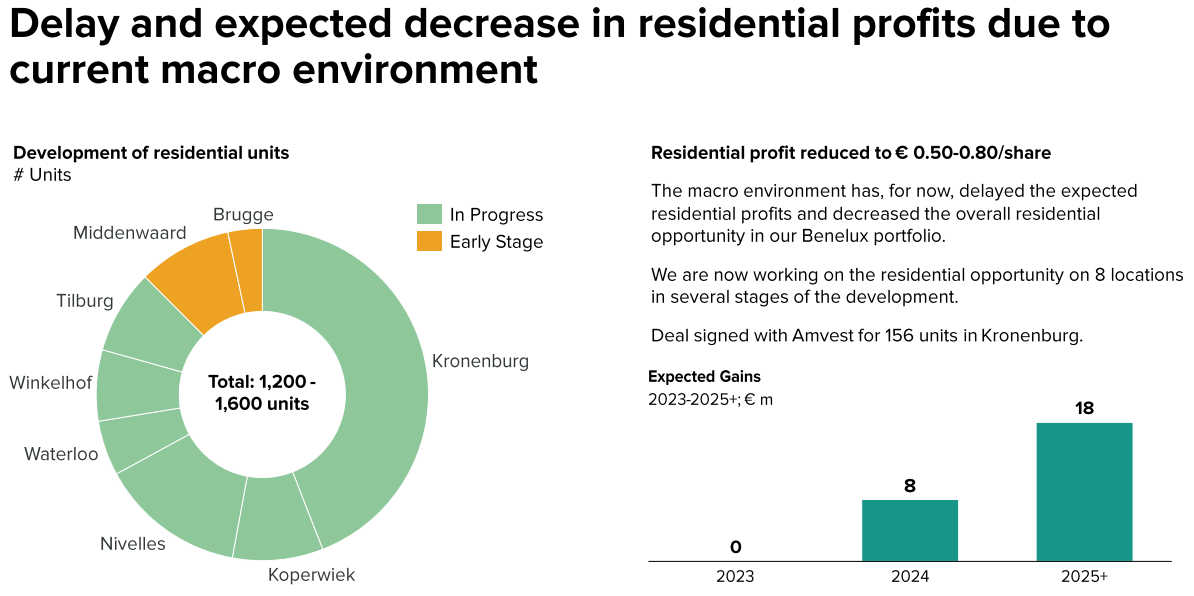

While I was positively surprised by the gain on valuation in the Netherlands, the big disappointment was definitely the cut in expected residential profits, from 1.60-1.85 EUR/share previously to 0.50-0.80 EUR/share:

{kind=link}

Wereldhave new residential outlook (Wereldhave H1 2023 Results Presentation)

To me, the residential redevelopment potential was the main differentiator for Wereldhave relative to other REITs. Furthermore, while the fall of the Dutch government puts uncertainty on the new REIT regime to take effect into 2025, my current expectations are that the changes go ahead and Wereldhave takes a 5% hit to its direct result, with an uncertain effect on the valuation of its Dutch properties.

The 62% cut in expected residential profits leaves little leeway for them to compensate for the hit from the new REIT regime.

Let's now turn our attention to the other REITs in my series.

Covivio

Covivio's portfolio is largely stable versus year-end 2022, with a slight increase in the share of hotels ( +1 %):

{kind=link}

Covivio Portfolio (Covivio H1 2023 Results Presentation)

Covivio continues to benefit from hedging its cost of debt. It stood at 1.46% in H1 2023, versus 1.24% at year-end 2022. The scrip dividend was also 79% subscribed, which helped strengthen the balance sheet.

Occupancy was 93.1% for European offices, 99.1% in German residential, and 100% in Hotels/Non-strategic.

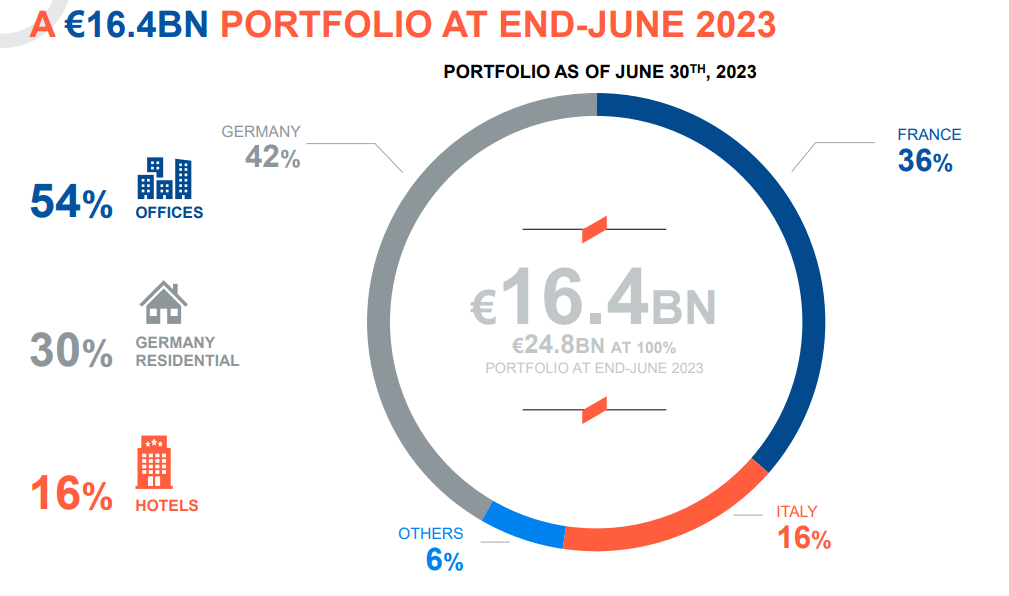

NSI

NSI, which focuses exclusively on offices in the Netherlands, also saw its cost of debt increase to 2.6 % in H1 2023, relative to 2% at year-end 2022.

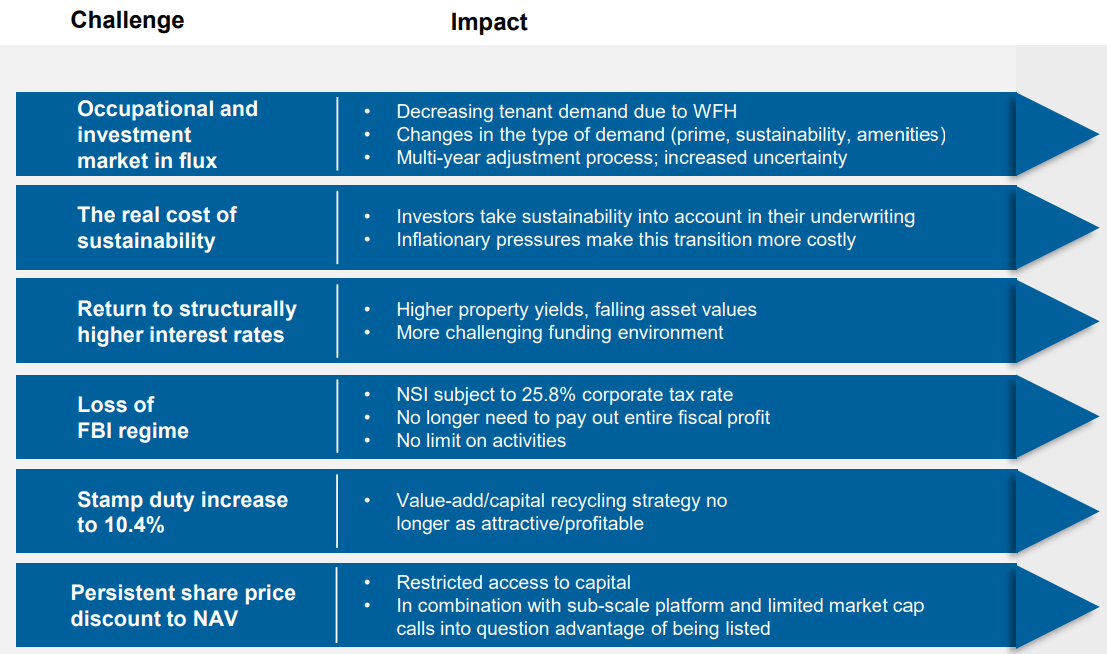

Given numerous challenges, from work from home to the new Dutch REIT regime, the company is undergoing a strategic review:

{kind=link}

Strategic review challenges (NSI H1 2023 Investor Presentation)

Despite its conservative leverage, NSI has seen a substantial (close to 50%) share price decline over the past year, making it a prime candidate for a turnaround should the narrative around offices change.

Mercialys

Mercialys focuses exclusively on shopping centers in France:

{kind=link}

Portfolio overview (Mercialys H1 2023 Results Presentation)

The company saw its cost of debt increase by 0.1% in H1 2023, now standing at 2.1 %. Mercialys also confirmed its target of 2% recurrent earnings (FFO) growth in 2023, with a payout of 85-95%.

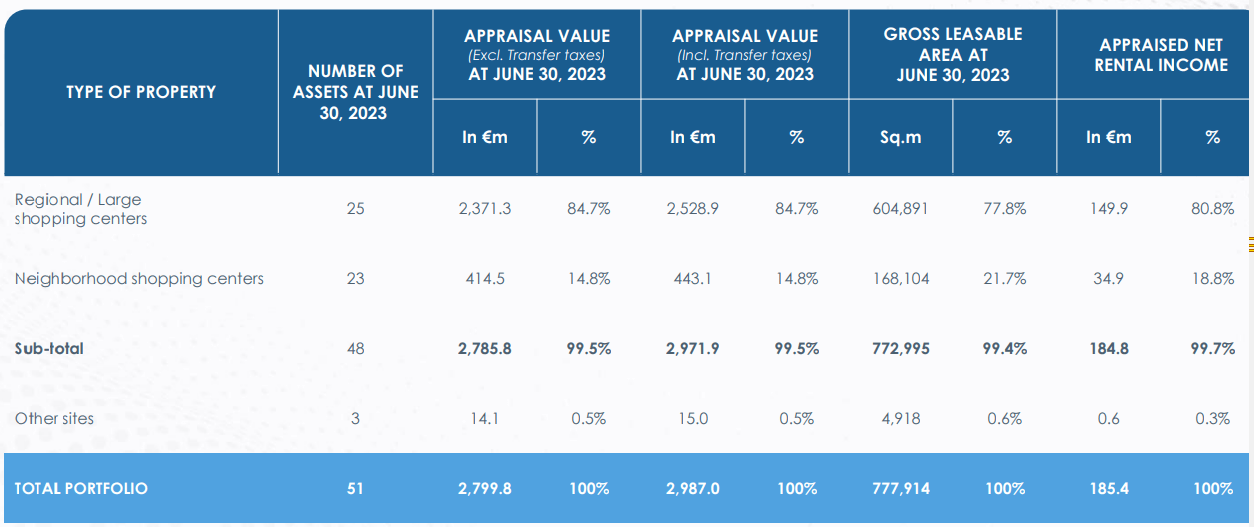

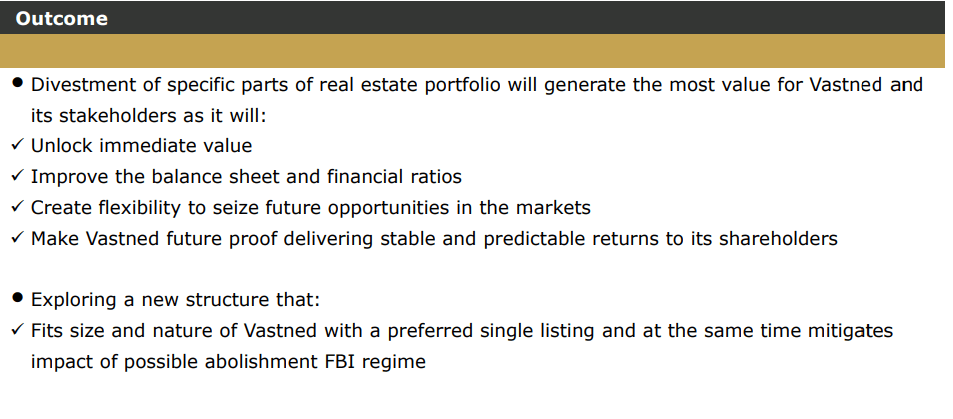

Vastned

Vastned is focused on retail properties in several countries, specifically the Netherlands, France, Belgium, and Spain. The company also concluded its strategic review , setting out to divest assets and create a single listing (currently, there is a separate listing in Belgium, as is the case for Wereldhave):

{kind=link}

Strategic Review Outcome (Vastned H1 2023 Results Presentation)

As with other REITs, the average cost of debt increased to 2.5%, from 1.9% at the end of 2022. The direct result outlook of 1.95 to 2.05 EUR/share was confirmed.

Cofinimmo

Cofinimmo currently has 20% of its assets in office, 7% in distribution networks, and 73% in Healthcare. The average cost of debt was 1.4 %, up 0.2% versus year-end 2022.

Cofinimmo confirmed its net result from core activities target of 6.95 EUR/share.

Comparison Table

For all companies in the below comparison, I will use the market price in EUR. I will also implement this approach to estimate the market-implied net initial yield:

Market-implied net initial yield = Valuation net initial yield / Division factor where:

Division factor = Price/NDV Ratio * (1 - Loan-to-value ratio) + Loan-to-value ratio

NDV stands for Net Disposal Value, a common metric reported by European REITs as a proxy for Net asset value.

Also where available, I will adjust the NDV to account for the market value of fixed-interest debt (for some REITs the NDV is artificially inflated due to the low prices of bonds they have issued). Where possible, I will generally use the EPRA net initial yield for valuation net initial yield.

Here is the calculation for Covivio as an example:

1. EPRA NDV = 87.8 EUR/share (93 EUR/share reported minus 5.2 EUR/share mark-to-market of fixed rate debt)

2. Loan-to-value = 40.7%

3. Valuation net initial yield = 3.9%

4. Price at the time of writing = 43.92 EUR

You get a P/NDV Ratio of 43.92 / 87.8 = 0.5, a division factor of 0.70 (0.5 * (1-0.407) + 0.407). The EPRA NIY is 3.9% which divided by our unrounded division factor of 0.7 gives us a market-implied net initial yield of roughly 5.54%:

| Company\Metric |

| LTV |

| Valuation NIY |

| Market NIY |

| Occupancy |

| Covivio |

| 40.7% |

| 3.9% |

| 5.54% |

| 95.8% |

| NSI |

| 31.5% |

| 4.7% |

| 7.32% |

| 92.7% |

| Mercialys |

| 36.1% |

| 5.63% |

| 9% |

| 95.3% |

| Wereldhave |

| 43.9% |

| 6.3% |

| 7.41% |

| 95.8% |

| Vastned |

| 44.7% |

| 4.4% |

| 6.07% |

| 98.2% |

| Cofinimmo |

| 47.6% |

| 5.5% |

| 6.61% |

| 98.5% |

Source: Author calculations based on company disclosures.

Conclusions

Relative to year-end 2022 and the table in my previous article , occupancy is down across the board, generally between 0.2% to 1%.

While the average market-implied yield was 6.44% in February, it now stands at around 6.99%, or up 55 basis points.

Wereldhave was an outlier with its reported drop in valuation net initial yield , with all other REITs using a higher net initial yield in their valuations.

Leverage was also up at all companies, with property valuations down and dividend payments weighing on cash balances.

What to buy

I am generally optimistic about the property sector largely because:

- Interest rates have peaked or are close to peaking;

- It is a defensive sector and should be less affected in a recession;

- Sentiment is low;

However, some risks still remain:

- Valuation yields are well below market yields, hence creditors may demand additional equity injections;

- Interest rates may stay elevated;

From a company perspective, clearly, Mercialys comes out ahead, even though there was insufficient disclosure on the value of fixed rate debt, hence my estimated 9% marked-implied yield may be closer to 8.6%, which still would make it the most attractive stock. The problem of course is the France-only exposure with the on-and-off protests affecting retailers.

As for the other companies, they are good picks for diversification and income generation, say through covered calls/cash-secured puts.

What does it mean for Wereldhave

With a reduced residential profit outlook, I see Wereldhave tracking the sector's performance going forward. A neat way to gain exposure to the company is through its illiquid Wereldhave Belgium listing, which currently trades at a market-implied yield of around 8.15%.

Furthermore, Wereldhave Belgium will not be affected by the change in the REIT regime in the Netherlands. Last but not least, Wereldhave plans to dispose of its 2 last assets in France. Given the valuations Mercialys trades at, the price achieved may not be attractive and the sales may well get delayed. Currently, Wereldhave's last two assets are in the books at a yield of 4.7% while the previous 4 assets were sold at a yield of about 7.5% back in 2021.

Thank you for reading.

For further details see:

Wereldhave Relative To 5 European REITs As Rates Peak