WERN - Werner Enterprises: Plenty To Gain Based On Solid Prospects For Growth (Rating Upgrade)

2023-11-12 07:01:40 ET

Summary

- Werner Enterprises, Inc. has a potential upside of nearly 30% due to recent market sell-offs, making it a promising investment.

- The company operates in the transportation industry, which is a strong indicator of economic health and has solid prospects for growth.

- WERN has shown appreciating revenues and is trading below its historical sale multiple, making it an appealing investment opportunity.

Investment Rundown

The implied upside for the company right now is nearing 30% given the recent market sell-offs. Because of the solid prospects of short-term gains on investment here with Werner Enterprises, Inc. (WERN), the company will be receiving a buy from me. The transportation industry is an important part of the economy and in many ways, it's a display of how the economy is doing. A lot of activity in the industry quite often is an indication of strong economic fundamentals like plenty of capital flowing and demand at high levels. With the next earnings report being just around the corner for WERN I think investors are faced with a promising risk/reward case here where buying before is worth it. On a six-month basis the company has seen appreciating revenues, although at a low level of just 3%, it is still moving in the right direction. WERN is trading under its historical sale multiple and deserves a higher multiple given the strong performance so far. I have covered the company previously and had them as a hold back then, I mentioned then that the multiple was not very appealing to get in at. Since then the stock price has dropped by around 14 - 15% and I think it's fair to upgrade the stock now. The price is at a much better point to start or add to a position, hence I am upgrading my rating.

Company Segments

Within WERN, the company operates through two distinct segments, namely the TTS (Trucking) segment and the Werner Logistics segment. The TTS segment is further subdivided, with a dual focus on direct transport and one-way transport. Direct transport caters to specific transportation needs, while one-way transport addresses more general requirements. On the other hand, the Werner Logistics segment plays a pivotal role in providing crucial support to companies in need of frequent asset or product movement between diverse locations. In this capacity, WERN plays a key role in facilitating distribution lines and the efficient scheduling of transportation.

{kind=link}

Industry fundamentals are still appearing quite solid as the loadings have perhaps started to flatten but it has not seen the severe drawdown as in 2020 when the world shut down. I do think we are likely to see a steady climb upward from here on out. the impact of higher interest rates seems to have just been slowing momentum, but not a decline in demand. The estimates right now are that in 2024 WERN will be able to gain significantly in its bottom line and post an annual EPS of $2.84 which puts it at an FWD p/e of just 12.8, which is closer to where it has historically traded before. With the next report coming up very soon there will need to be some positive comments coming from the management team that could reassure investors that these EPS estimates are reasonable. I lean towards perhaps a slightly lower EPS estimate, closer to $2.6, partly given the history of the company meeting or exceeding projections. That still puts the company at an appealing valuation to invest.

Growth And Performance

With WERN investors are getting a company that is focused on returning a lot of value to its shareholders through both buybacks and dividends. The yield has appreciated thanks to the depreciation of the share price over the last few years and is now over 1.5%. As far as the buybacks go, the last 5 years have meant an average decrease of 2.36% which if continued gets us an immediate return of 3.86%. I do expect there to be some improvements on the EPS as well that will justify the share price going even higher as WERN trades around a 16 - 17x p/e.

The markets are a little mixed on the view of WERN but I of course lean more towards a buy at these prices. Thanks to the broader market sell in the last few months it has meant the p/e of WERN has gone down quite a lot and is not in line with the broader industrial sector. Historically WERN has traded closer to a p/e of 14.5 which implies a 14% premium to that right now. However, a buy can still be justified given the long-term outlook for the company. Given the outlook for the shipping industry is around a 7% CAGR between now and 2031 I think it's reasonable to expect similar EPS growth numbers for WERN seeing as they are a major part of the industry and hold a strong position.

{kind=link}

Above is a chart showcasing some of the volatility that the margins may experience during rising interest rate levels and times of higher gas prices too. I don't think it's reasonable to assume that gas prices will return to levels seen in 2020 during the pandemic, but I do think some short-term declines are to be expected. This could cause some one-off quarters to show strong net margin improvements but we must see a steady trend upwards develop quite soon. I do think as interest rates stabilize WERN will be able to adapt to their right now $24 million TTM interest expenses. This has not appeared to affect the buybacks though or the dividend to a great extent as these are still maintained, and this is a crucial reason why I am still a buyer of WERN.

Earnings Highlights

{kind=link}

Looking at the previous quarter's results I think that WERN provided strong numbers. The revenues may have shown a slight YoY decline for the quarter, but YTD WERN is still up 3% from last year, even as rates are higher and momentum slowing somewhat. The earnings report came out on August 4 and since then the share price has declined a fair bit, almost 25%. I think it has been somewhat unjustified as the quarter showed strong margin retention in some remarks. Operating margins were 5.8% which may be lower than the 9% last year, but we have to keep in mind that the quarter included higher gas prices as well. This is where the earnings volatility I have mentioned before is displayed.

{kind=link}

What is crucial is to see that the top line remains intact and that WERN continues to have a strong FCF to bring shareholder value. On an annual basis, the cash flow from operating activities improved by 2% YoY which resulted in $114.9 million in total. Net capital expenditures appreciated quite a lot though to $151 million, up from $116 million. Going into Q3 I do think investors can expect a retention in the FCF and even slight QoQ improvements too and possibly see it reach around $120 million.

{kind=link}

The company has also improved its leverage ratio very well in the last few years and the debts are quite far out until they mature. The largest amount is in 2027 at $550 million. With WERN generating close to $500 million in EBITDA in the last 12 months alone I do think we will see the debts not being an issue. With low leverage, the interest expenses for the business have not increased as drastically and resulted in WERN constantly staying profitable. As for the cash position of the company it has depreciated to $46 million, down from over $100 million at the end of 2022. This isn't a significant worry I think as the debts are still far out and that doesn't put WERN in a bad financial position.

Valuation

{kind=link}

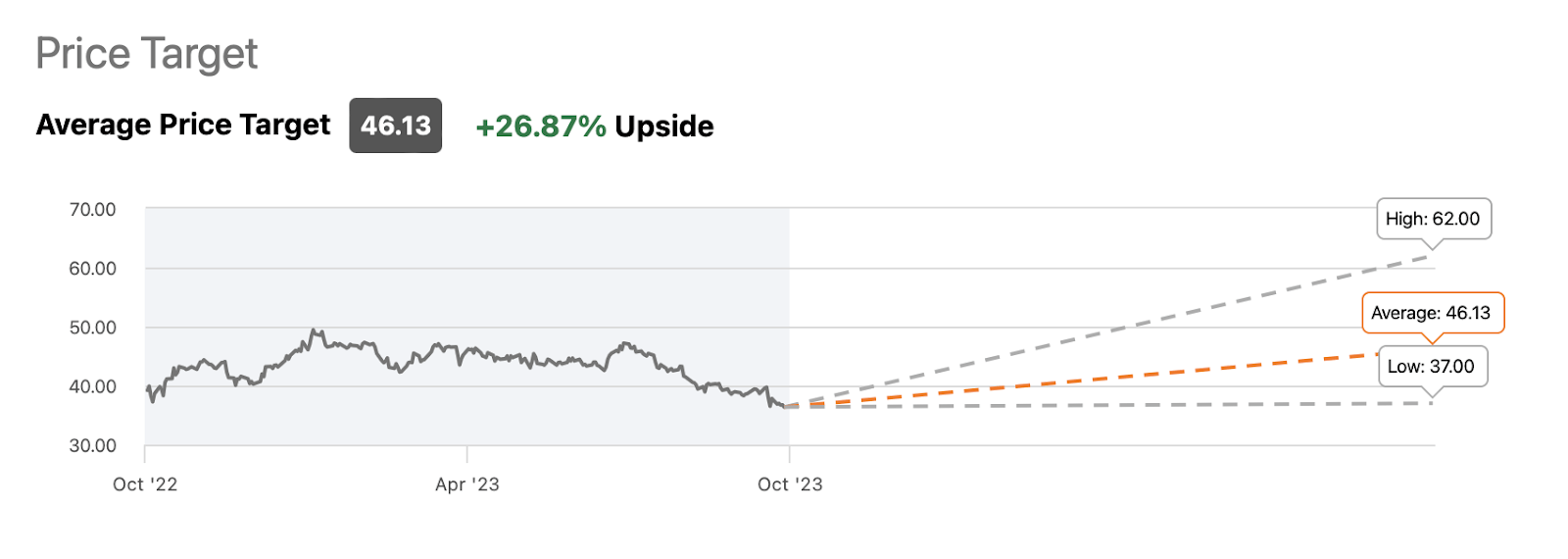

The price targets right now indicate an upside of 28.87% for the company. I think it's reasonable to assume that WERN can deliver a strong long-term return for investors. We have learned that the industry is expected to grow around 7% CAGR until 2031 and using the EPS estimates for 2024 of $2.84 and adding on the growth, in 2031 it would suggest an EPS of $4.56. Using the historical p/e of 14.5 we land at a price target of $66. Over those years that is an annual ROI of 10.3%. Adding on the buybacks and dividends that WERN has we instead get an annual return of 14.1%. That is certainly something I am willing to put my money into and it results in the buy rating I have for WERN. Disruption in the industry seems unlikely as trucking is still a significant backbone of the US economy and replacing it will take an immense amount of capital. It's one of the most efficient ways of transporting goods by land and the last miles.

Risks

One of the primary concerns for companies operating in the transportation sector is the inherent sensitivity to fluctuations in economic activity, resulting in diverse demands that can vary from one fiscal year to another. When scrutinized on a year-over-year basis, these fluctuations may give some investors pause, as they appear as short-term challenges. However, it's crucial to adopt a long-term perspective, as these fluctuations often represent smaller, manageable hurdles.

{kind=link}

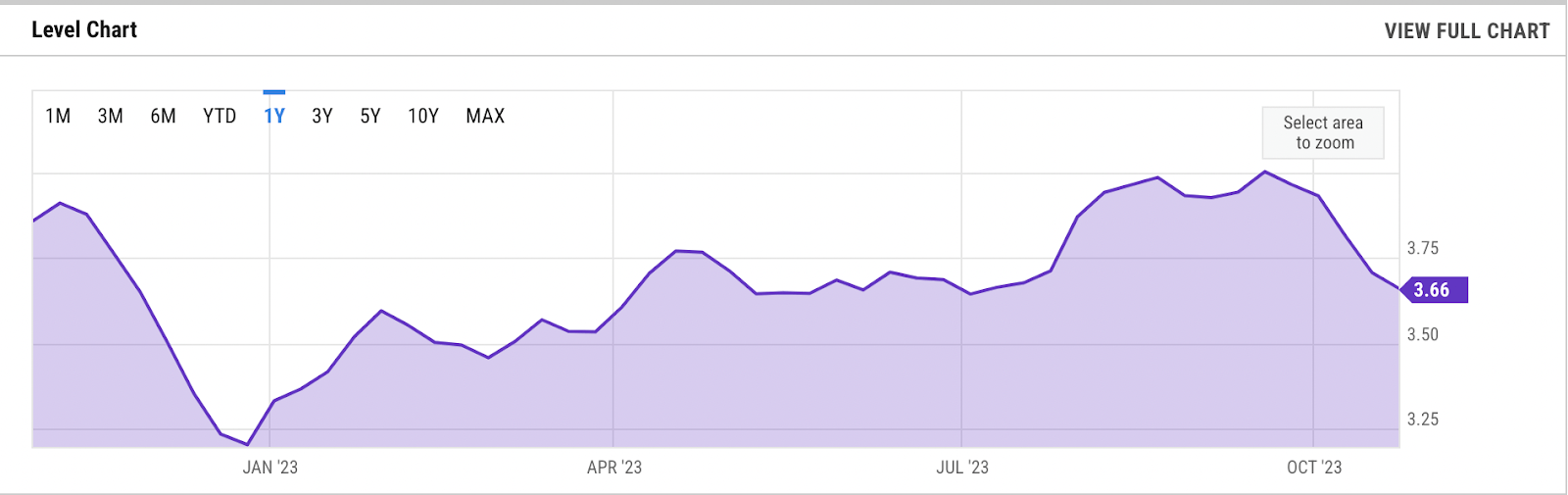

In addition to reduced demand, the inherent volatility of fuel prices poses challenges for the transportation industry, making it difficult to predict quarterly results. As the chart displays the price of gas in the US has been rising in the last quarter and will likely impact the bottom line for WERN. Estimates are for an EPS of $0.49 which is a QoQ decline of nearly 6%. I do expect the following quarters after that to show some levels of recovery.

{kind=link}

The company has a mixed history as we can see with beating or meeting earnings estimates. Demand can certainly be lower as higher interest rates are putting a toll on consumers' capabilities of spending. What I do see as a possibility is that after 2024 and beyond both people and businesses will get used to an elevated level of interest rates and adjust their spending accordingly. 10 years ahead this will seem like a small short-term headwind that doesn't drastically affect the growth potential of WERN. I still estimate them to be able to grow the EPS by around 7 - 8% at least CAGR from now and 10 years ahead. This I think is reasonable to assume given the strong FCF of the company which gives way to continued buybacks of shares.

Final Words

WERN has a market cap of $2.3 billion right now and over 5000 dedicated trucks. This has netted WERN to be the sixth-largest dedicated carrier in the US. The broader sell-offs in the markets resulted in the share price falling for WERN as well and also opened up a very good buying opportunity. My price projections indicate an annual return of around 14% up until 2031 should it manage to deliver a similar EPS growth as the industry and continue to buy back shares. As stated in the beginning, I have covered WERN before and had them as a hold then. I now think the stock is at a great point to add or start a position in. The valuation has reached more realistic and fair levels, which results in me upgrading it to a buy now.

YCharts

For further details see:

Werner Enterprises: Plenty To Gain, Based On Solid Prospects For Growth (Rating Upgrade)