HDSN - WESCO International: Bullish Numbers Deserve A Bullish Rating

Summary

- WESCO International continues to post strong sales, profit, and cash flow numbers for the most part.

- This proves the company is in good health and the future for the enterprise is likely to be positive as well.

- The stock may be pricey compared to some similar firms, but they are cheap on an absolute basis.

When I rate a company, that rating always stands in relation to what the broader market achieves. For instance, I consider a 'buy' rating a success so long as the company in question outperforms the S&P 500 by a measurable amount. That's true even if shares of the stock end up generating a negative return for a time. One good example of this playing out can be seen by looking at WESCO International (WCC), a business focused on producing and selling fasteners, cutting tools, safety products, and more. It's also involved in network infrastructure, security, inventory management, product packaging, etc. Recently, the financial performance achieved by the company has been very impressive. But even so, shares have taken a step back, likely because of concerns over the economy more broadly. Given how cheap shares are, however, I don't see the downside that the stock has experienced lasting for all that much longer. Because of the fundamental condition of the business and how attractive the stock is, I believe that a 'buy' rating for it is still appropriate at this time.

The market is ignoring great results

Back in the middle of August of 2022, I found myself looking favorably upon WESCO International. Up until that point, I had rated the company a 'hold'. But because of shares falling more rapidly than what the market did, I felt as though the stock had finally gotten cheap enough to upgrade to a 'buy'. Of course, my decision was informed by more than just the share price movement. Fundamental performance achieved by the company was also looking quite positive. All of these factors combined led me to the aforementioned 'buy' rating. Sticking true to my definition of what constitutes a 'buy', the market has since agreed with me. Although the S&P 500 is down 7.7% since the publication of that article, shares of WESCO International have seen downside of only 5.3%.

{kind=link}

This outperformance may not seem like much. And in fact, it's not as much as it probably should be. To understand why I believe the company should be performing better than this, I need only point to results covering the third quarter of its 2022 fiscal year. During that time, revenue totaled $5.45 billion. That's 15.2% above the $4.73 billion generated one year earlier. This 15.2% increase was driven by strength across the board. Most notably, the Utility & Broadband Solutions segment of the firm reported a 28.6% rise in organic growth. This was followed closely by a 14.9% increase in organic sales for the Electronic & Electrical Solutions segment. And finally, the Communications & Security Solutions segment brought up the rear with a 9.6% rise in organic growth. All told, organic sales for the company expanded by 16.9%, driven by a combination of price increases and robust demand. But this growth was offset slightly by a 1.7% decline caused by foreign currency translation.

{kind=link}

On the bottom line, the picture for the company has also been positive. Net income of $225.3 million dwarfed the $105.2 million reported one year earlier. Although operating cash flow for the company declined from $69.9 million to negative $106.1 million, this figure actually rose from $195.5 million to $303.6 million if we adjust for changes in working capital. And finally, EBITDA for the business went from $330.3 million to $465.9 million. The kind of performance the company enjoyed in the third quarter of last year was very similar to what the company enjoyed through the first half of the year and through the first nine months of the year as a whole. During the first nine months of 2022, sales of $15.86 billion beat out the $13.37 billion reported the same time one year earlier. Net income more than doubled from $254.9 million to $598.5 million. Operating cash flow unfortunately went from $172.7 million down to $410.6 million. But if we adjust for changes in working capital, it would have jumped from $475.7 million to $836.1 million. And finally, EBITDA for the business shot up from $856.1 million to $1.22 billion.

For 2022 in its entirety, management has forecasted revenue growth of between 15% and 17%. Earnings per share were forecasted at between $15.80 and $16.20. At the midpoint, this would translate to $582.9 million. Meanwhile, EBITDA was forecasted at around $1.68 billion. it is worth noting that the picture for the company has been muddied a little bit by the firm's purchase, that was completed on November 1st of 2022, of Rahi Systems, a leading provider of global hyperscale data center solutions. That enterprise cost the company $217 million and should bring in $400 million in revenue with $28.9 million of EBITDA. Assuming a 21% tax rate and the completion of the transaction with cash only, net income can be increased by $22.8 million while cash flow can be increased by the same amount. The increase for EBITDA would be the same $28.9 million. Based on my own assessments, this would translate to adjusted operating cash flow for the company for 2022 of $877.9 million and EBITDA for the year of $1.71 billion. I also decided to apply these increases to data analyzing the company through the lines of its 2021 fiscal year.

{kind=link}

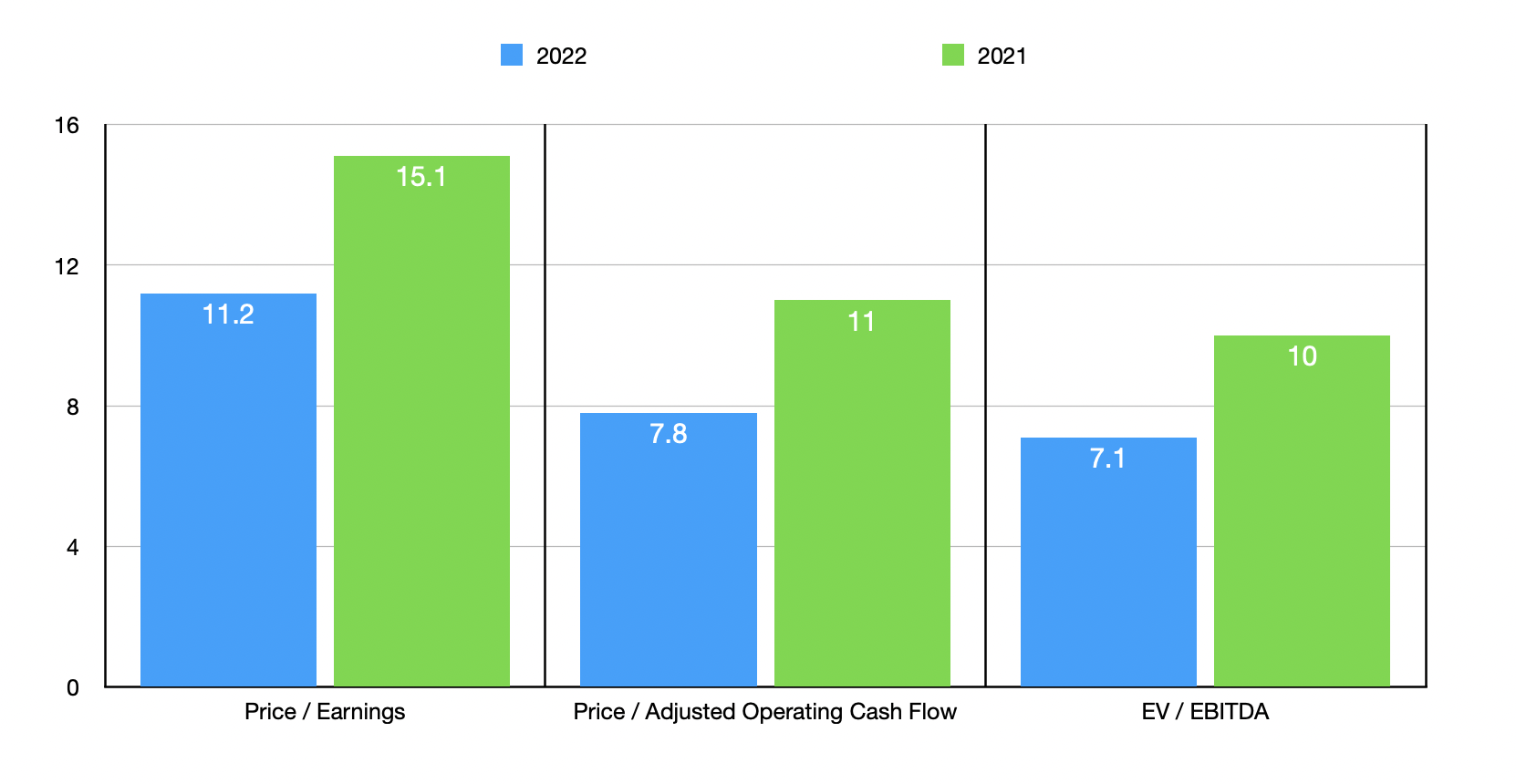

Taking these figures, I calculated that the firm is trading at a price-to-earnings multiple of 11.2. The price to adjusted operating cash flow multiple should be 7.8, while the EV to EBITDA multiple has been calculated at 7.1. Using the data from 2021, these multiples would be 15.1, 11, and 10, respectively. I also, as part of my analysis, compared the company to five similar companies. On a price-to-earnings basis, these firms ranged from a low of 0.5 to a high of 5.5. And using the EV to EBITDA approach, the range would be from 0.5 to 4.2. In both cases, WESCO International was the most expensive of the group. And finally, using the price to operating cash flow approach, we would end up with a range of between 3 and 8.1, with three of the five companies being cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| WESCO International |

| 11.2 |

| 7.8 |

| 7.1 |

| BlueLinx Holdings ( BXC ) |

| 2.4 |

| 3.0 |

| 1.5 |

| Veritiv Corporation ( VRTV ) |

| 5.5 |

| 8.1 |

| 4.2 |

| Hudson Technologies ( HDSN ) |

| 4.5 |

| 8.1 |

| 3.4 |

| Marubeni Corporation ( MARUY ) |

| 4.9 |

| 6.2 |

| 4.2 |

| Barloworld Limited ( BRRAY ) |

| 0.5 |

| 3.6 |

| 0.5 |

Takeaway

Relative to similar firms, WESCO International may be a bit expensive. But on an absolute basis, shares don't look unreasonably priced at all. This is especially true when you factor in the growth that management has achieved and the robust cash flows the company is capable of generating. Due to these factors, I believe that a 'buy' rating still captures the firm's potential in relation to the broader market.

For further details see:

WESCO International: Bullish Numbers Deserve A Bullish Rating