GOLD - Wesdome Gold Mines: A Premium Valuation Relative To Peers

2024-01-16 11:33:42 ET

Summary

- Wesdome Gold Mines Ltd. beats its FY2023 guidance midpoint, but the 2024 suggests a soft Q1 on deck with elevated costs, and another year of costs at/above the industry average.

- On a positive note, Presqu'ile looks like a realistic opportunity to add ~20,000 ounces per annum and take advantage of excess Kiena mill capacity and the 2025 outlook is better.

- That said, with Wesdome Gold Mines trading at ~20x forward free cash flow & 1.0x P/NAV and one of the highest multiples sector-wide, I don't see any margin of safety at US$5.80.

It's been a bumpy start to the year for the VanEck Gold Miners ETF ( GDX ) in what's typically the best month of the year from a seasonal standpoint, with an average return for the sector of ~2.6% in January over the past 30 years. This is certainly disappointing for investors, especially with the metal's price notching a record seven weekly closes above the $2,000/oz level, and it can be explained by continued negative sentiment towards miners.

Fortunately, Wesdome Gold Mines Ltd. ( WDOFF ) delivered ~3% above its FY2023 guidance midpoint, which wasn't surprising with more conservatism after a rough 2022 with production of ~123,300 ounces of gold. However, 2024 won't be the year strong year that some had hoped for from a margin standpoint, with cost guidance set in line with the industry average based on the midpoint a ~$1,400/oz.

In this update we'll dig into the Q4 production results , the forward outlook, and whether the stock is offering enough margin of safety after its recent underperformance.

{kind=link}

Q4 & FY2023 Production

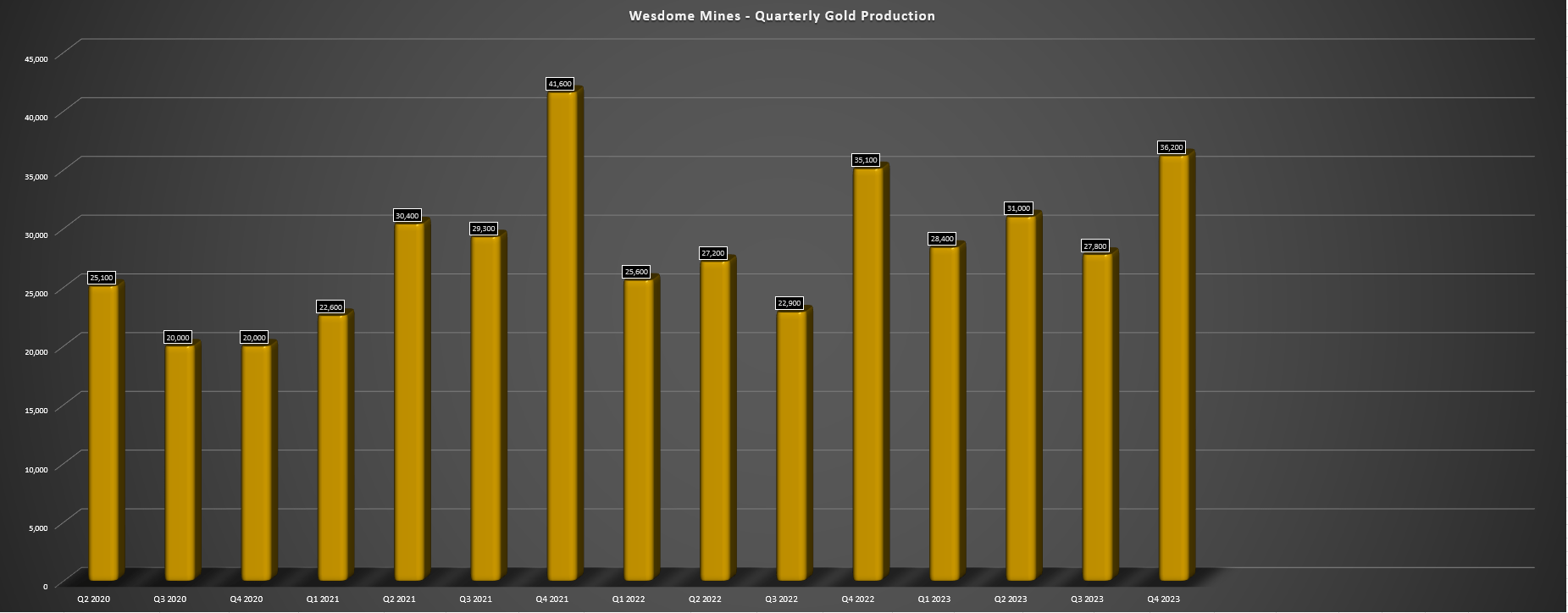

Wesdome Gold Mines Ltd. ("Wesdome") released its Q4 production results this week, reporting quarterly production of ~36,200 ounces of gold, a 3% increase from the year-ago period. This solid quarter helped Wesdome to beat its annual guidance midpoint of 120,000 ounces for FY2023, but this was not much of a feat given that the bar was set extremely low, with it representing a decline in production on a two-year basis even if the midpoint was met, and a 30% drop from initially provided 2022 guidance (170,000 ounces). That said, this is certainly a step in the right direction to winning back the market's trust after a brutal 2022. Additionally, the company delivered slightly ahead of schedule regarding Kiena mine development, with production from the Kiena Deep A Zone expected early in Q2 according to the most recent disclosure.

Wesdome Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

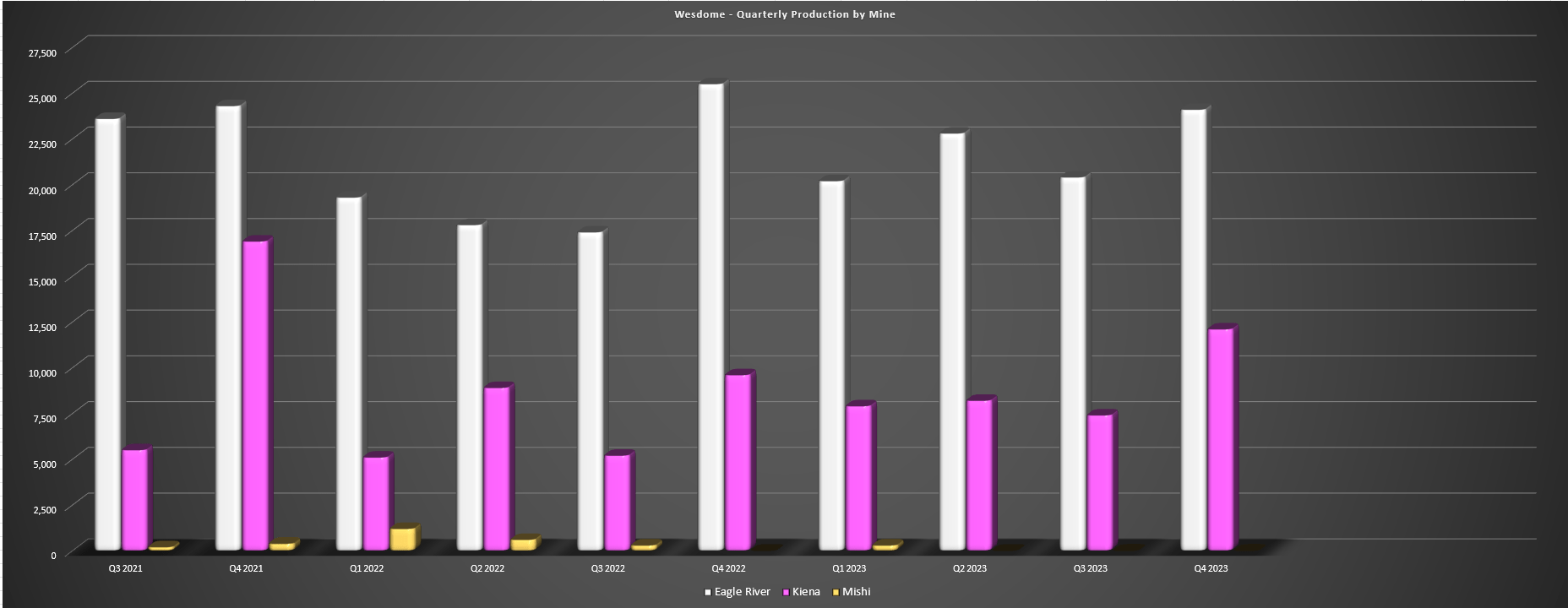

Digging into the production results a little closer, Eagle River produced ~24,100 ounces (down 6% year-over-year), with slightly higher grades unable to offset the lower throughput in the period (~54,700 tonnes vs. ~58,300 tonnes). However, the mine tracked to the high end of guidance for head grades in FY2023 of 11.5 - 12.5 grams per tonne of gold (actual: 12.4 grams per tonne of gold), and production improved year-over-year to ~87,800 ounces, albeit up against very easy comparisons after a difficult 2022 for the mine (leach tank failure, manufacturing defect in new hoist rope). And looking ahead to 2024, production is expected to look similar, with 85,000 ounces at the midpoint, with an average grade of 12.2 to 13.4 grams per tonne of gold.

Wesdome Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

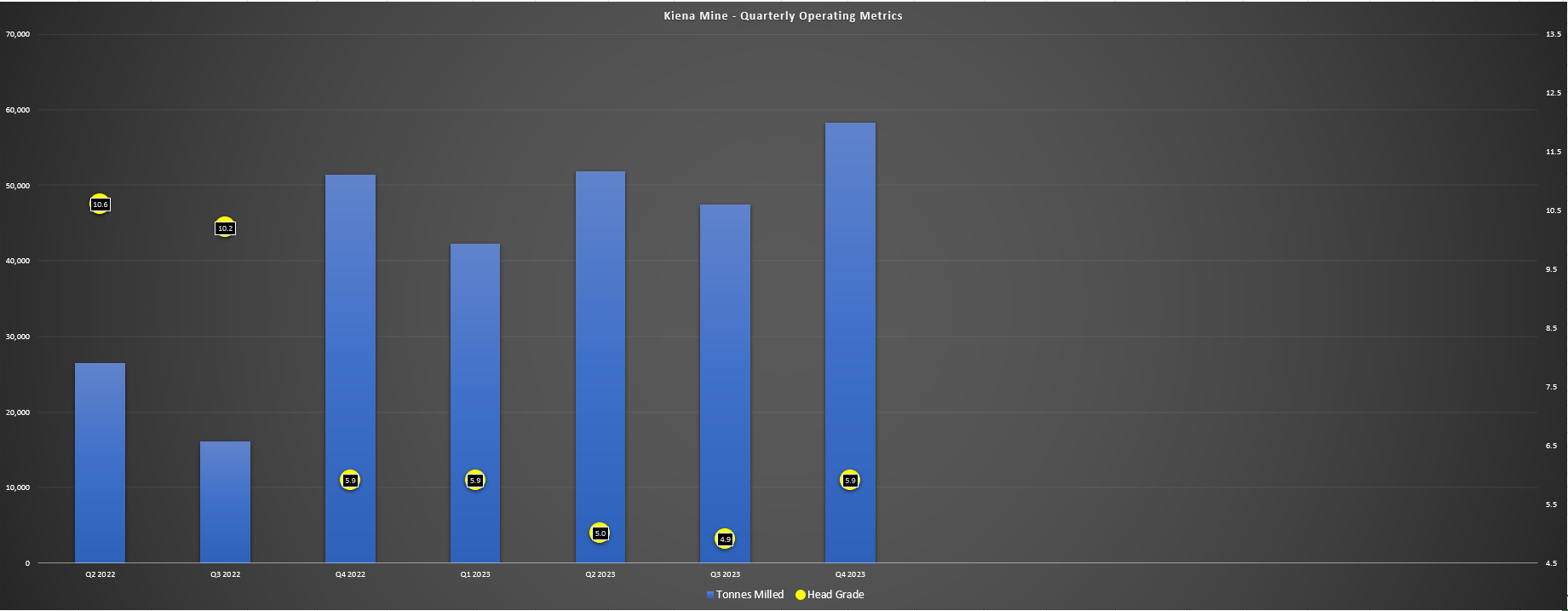

Moving over to Kiena, the mine produced well above its planned grades of 3.7 to 4.7 grams per tonne of gold in 2022, with an average grade of 5.9 grams per tonne of gold in Q4, and 5.9 grams per tonne of gold for the year. This translated to production of ~12,100 ounces in Q4 and ~36,200 ounces for the year, beating out the guidance midpoint of 35,000 ounces. Notably, the 2024 outlook of 80,000 to 90,000 ounces appears to be de-risked with the company sharing that delineation drilling has "confirmed a substantial portion of 2024 planned mining areas," and if Kiena can deliver on plans, investors can look forward to much better margins at this asset in 2024 after 18 months of disappointing production and margins relative to the plans outlined in 2021. Let's take a look at the consolidated 2024 outlook below.

Kiena Mine - Quarterly Throughput & Grades - Company Filings, Author's Chart

{kind=link}

2024 Outlook

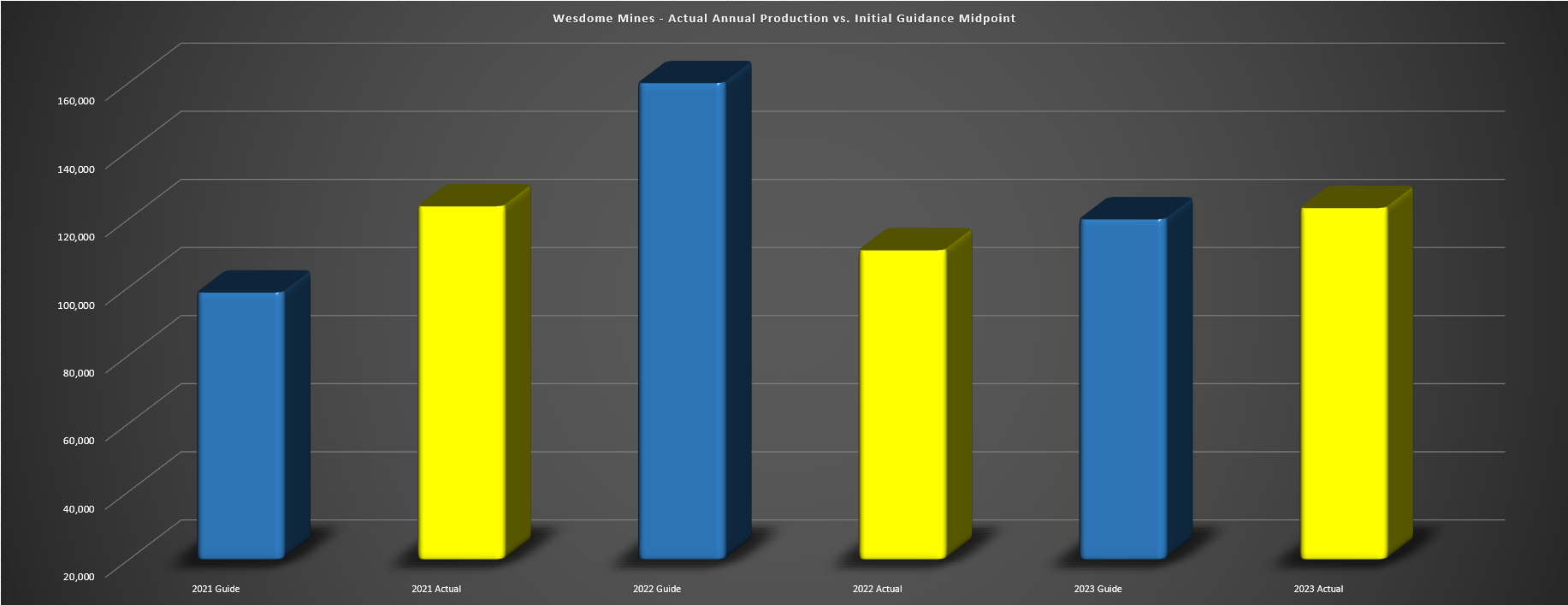

As for the 2024 outlook, Wesdome is guiding for production of 160,000 to 180,000 ounces (in line with my previous estimates of 168,000 ounces), and at all-in sustaining costs of $1,325/oz to $1,475/oz. This translates to a midpoint of 170,000 ounces at $1,400/oz AISC, placing it behind companies like Karora Resources ( KRRGF ) and Argonaut Gold (ARNGF), which have much lower market caps. However, the higher costs can partially be attributed to elevated sustaining capital of ~$75 million, which was well above the ~$41 million budgeted for 2023. That said, these results are a little disappointing relative to 2022 guidance of 170,000 ounces at $1,070 oz at the midpoint, with production in line (albeit arriving two years later) and costs up ~30% from the previous outlook. In addition, this should result in softer Q1 results, with higher capex spread over sales of ~35,000 ounces.

Wesdome Actual Annual Production vs. Initial Guidance Midpoint - Company Filings, Author's Chart

{kind=link}

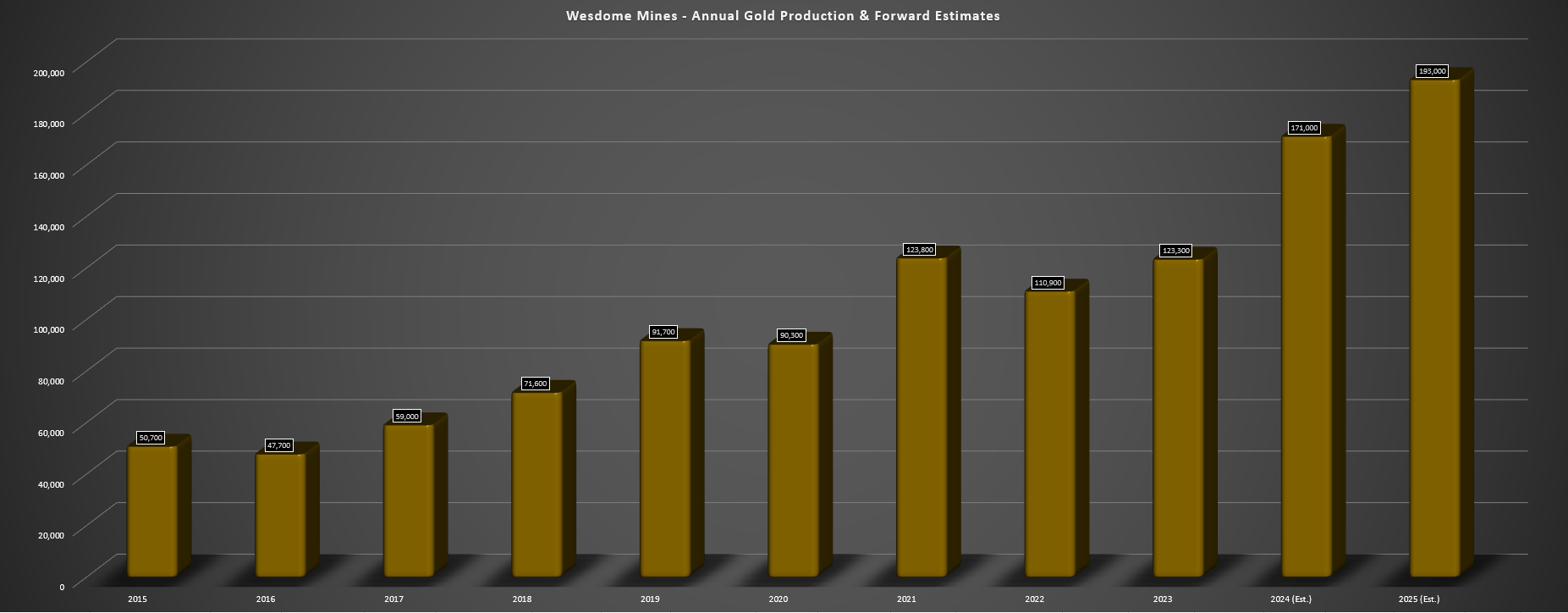

The positive takeaway from this guidance is that production beat the midpoint last year, suggesting there might be some upside in this guidance to 175,000 ounces if we see positive grade reconciliation in the deeper levels of the Kiena Mine. In addition, while 2024 will be another transition year as Kiena ramps up mine production from its higher-grade zones, the 2025 outlook is more robust with expectations to produce ~192,000 ounces based on the guidance midpoint. Plus, the company provided early results from a scoping study at Presqu'ile (1.3 kilometers west of Kiena), noting that there's the potential for this deposit to provide 250 to 400 tonnes per day of feed in late 2025 and provide an incremental 15,000+ ounces per annum at lower grades. Notably, this incremental output for this nearby deposit will come at a relatively low cost, and internal plans are to connect the exploration ramp to the main mine infrastructure in 2025.

Wesdome Mines Annual Gold Production & Forward Estimates - Company Filings, Author's Chart

{kind=link}

Overall, the 2024 outlook and plans pave a path to higher production, and it's nice to see that Presqu'ile looks like a very realistic opportunity to take advantage of excess capacity at the Kiena Mill. However, with elevated capex (~$94 million) to invest in both operations (deferred development and investments in infrastructure), back-end weighted production this year, and elevated sustaining capital, Wesdome will struggle to generate much free cash flow unless gold prices head to new all-time highs.

Let's see if this softer near-term outlook is priced into the stock.

Valuation

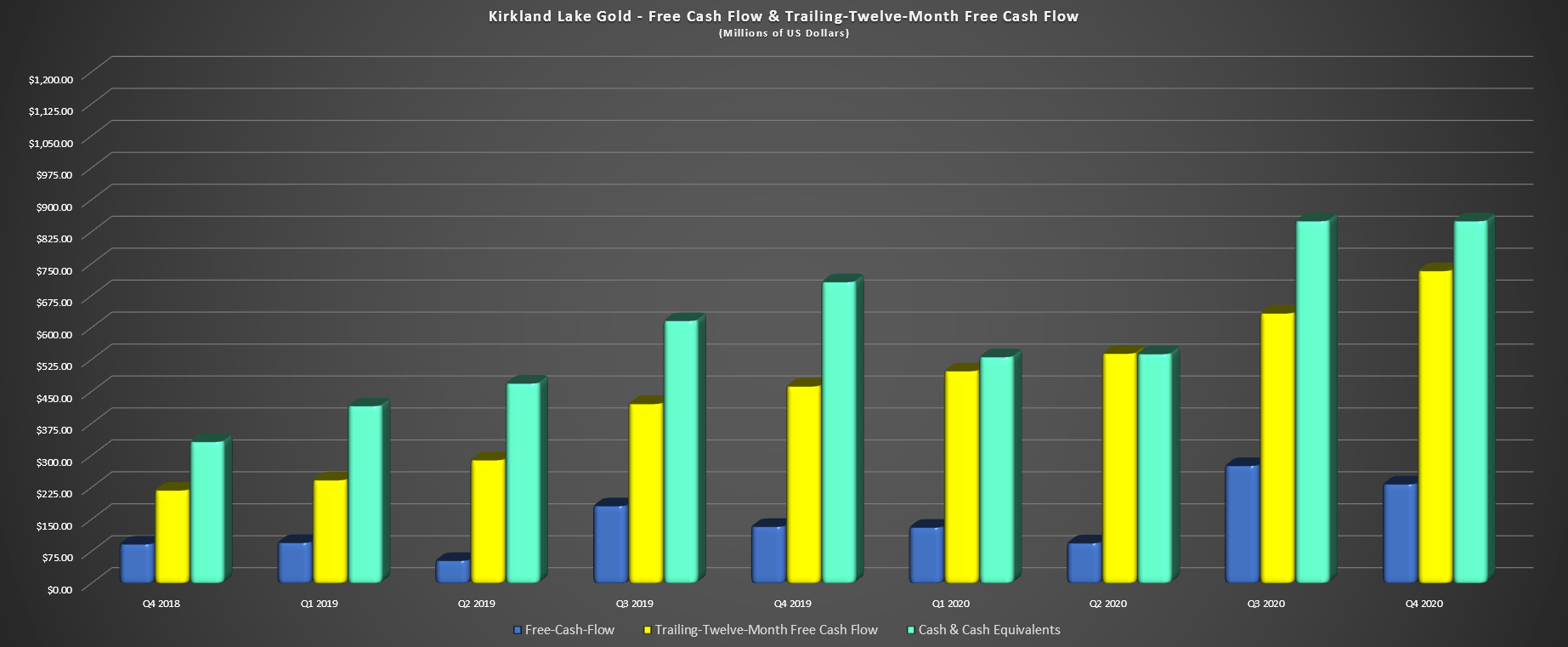

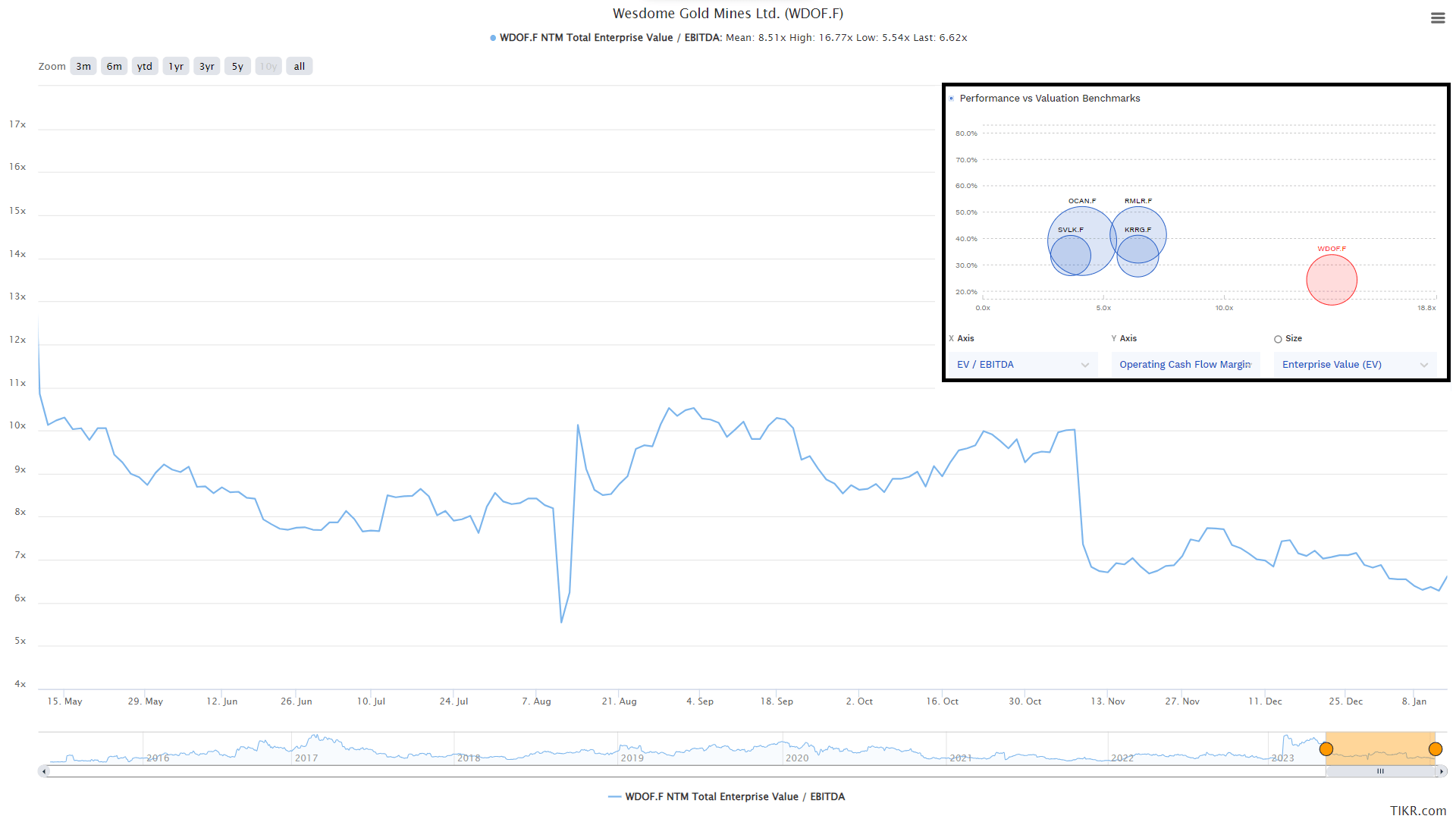

Based on ~153 million fully diluted shares and a share price of US$5.81, Wesdome trades at a market cap of ~$890 million and an enterprise value of ~$900 million. This leaves Wesdome as one of the higher capitalization names in the 150,000 ounce to 300,000 ounce producer space in Tier-1 jurisdictions, well ahead of other companies with similar or higher production levels like Karora, Argonaut, Silver Lake Resources ( SVLKF ), and Ramelius ( RMLRF ). Meanwhile, assuming a more conservative assumption of $40 million in FY2024 free cash flow, Wesdome is trading at over 20x forward free cash flow, one of the higher free cash flow multiples in the small-cap producer space, and a higher multiple to Kirkland Lake Gold (~17x) when it peaked above $50.00 per share. And while I think a premium of this magnitude could be justified if Wesdome was a 400,000+ ounce producer at sub $750/oz AISC (KL was a ~1.0 million ounce producer at the time with ~$800/oz AISC), this isn't the case with a 2024 outlook of ~170,000 ounces at ~$1,400/oz.

Kirkland Lake Gold Quarterly & TTM Free Cash Flow & Cash Position (2019-2021) - Company Filings, Author's Chart Wesdome EV/EBITDA Multiple & Valuation/Margins vs. Peers - FinBox, TIKR

{kind=link}

{kind=link}

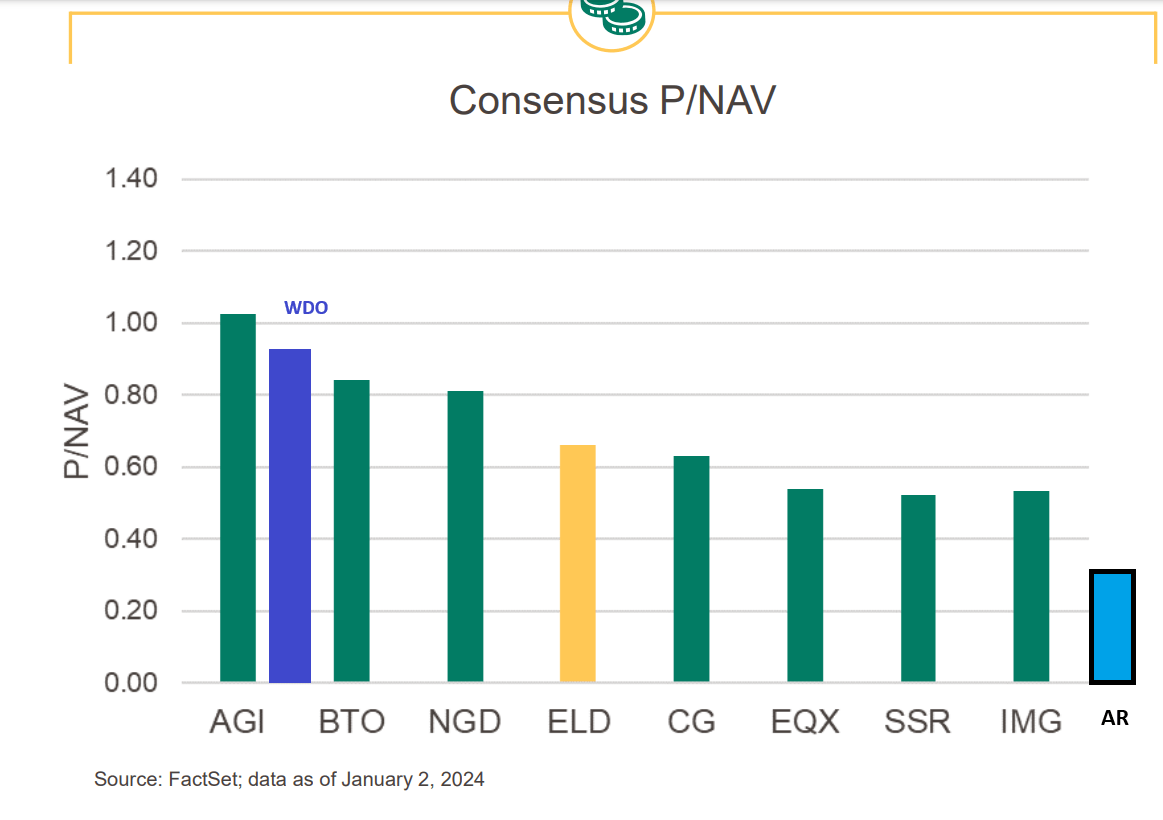

As for Wesdome's P/NAV multiple, the current valuation leaves a lot to be desired on this metric as well, with Wesdome trading just shy of 1.0x P/NAV which is in line with Barrick Gold ( GOLD ), a more diversified producer and the #2 producer by scale sector-wide, and only slight behind Alamos Gold ( AGI ) which has a path to ~600,000 ounces at ~$1,000/oz AISC in 2026. Meanwhile, if we compare Wesdome to smaller Tier-1 jurisdiction junior producers, the stock is trading at over double the multiple of Argonaut Gold, with Argonaut having an estimated net asset value of ~$1.11 billion (Wesdome: ~$920 million), but trading at less than half the market cap of Wesdome at just ~$360 million. Hence, if I wanted to bet on a North American turnaround story in the gold space, I think Argonaut is the far more attractive setup here from a reward/risk standpoint, trading at less than 2x FY2024 P/CF and ~0.30x P/NAV vs. Wesdome at ~9.0x P/CF and ~0.96x P/NAV, respectively.

So, what's a fair value for the stock?

Based on what I believe to be fair multiples of 1.10x P/NAV (a premium to peer group) and 7.5x P/CF and a 65%/35% weighting to P/NAV vs. P/CF respectively, I see a fair value for Wesdome of US$7.20. This points to a 24% upside from current levels. However, I am looking for a minimum 35% discount to fair value when it comes to starting new positions in small-cap producers to ensure a margin of safety, and would prefer closer to 40% to compensate for the risk of owning a less diversified company in a cyclical sector. And if we apply this discount to Wesdome, the stock's updated low-risk buy zone comes in at US$4.70 or lower, suggesting that the stock would need to pull back at least another 12% to become attractive from a fundamental standpoint. Obviously, a pullback of this magnitude may not materialize, I think there is far better value elsewhere than paying above US$5.80 for Wesdome here.

Mid-Scale & Junior Producers Estimated P/NAV Multiples - Eldorado Presentation, FactSet, Author's Notes (WDO/AR)

{kind=link}

Summary

Wesdome's 2023 results met my expectations, as I figured that the company would guide conservative for the year after a rough 2022 and with no permanent CEO in place. That said, free cash flow generation in 2024 will come in a little weaker than I expected without help from the gold price due to a year of significant investment (+20% year-over-year), and it's hard to argue that Wesdome is offering any margin of safety at current valuation of ~1.0x P/NAV and over 20x forward free cash flow. This doesn't mean that the stock can't go higher and a rising gold price will lift all boats if it materializes, but I see Wesdome Gold Mines Ltd. as one of the more expensive ways to get exposure to gold, and continue to favor names elsewhere in the sector.

For further details see:

Wesdome Gold Mines: A Premium Valuation Relative To Peers