WMC - Western Asset Mortgage Capital: Little Chance Of Recovery In My Opinion

2023-05-31 02:25:54 ET

Summary

- Western Asset Mortgage Capital Corporation struggles to recover from the pandemic shock and rising interest rates, with management considering a sale or merger.

- WMC's Q1 2023 results show improved earnings and asset prices, but book value remains significantly down from previous years.

- The mortgage market faces challenges in 2023, with higher interest rates discouraging refinancing and home sales, but overall performance remains robust due to low unemployment and strong household income.

Investment thesis

Western Asset Mortgage Capital Corporation ( WMC ) has been struggling for approximately 3 years and the company cannot recover from its pandemic shock since. The rising interest rates have been hurting the company's portfolio and the book value has been on the decline for years. The management is in review of strategic alternatives to a sale or merger of WMC. The slowing mortgage market and lower new MBS issuances will not help WMC during the rest of 2023.

Earnings Highlights

WMC has experienced improved first-quarter results in 2023, attributable to higher earnings and better asset prices. The company reduced recourse debt through the sale, repayment, and pay downs of investments amounting to approximately $67 million. The GAAP book value per share increased by 4.8%, and the economic book value per share rose by 1.8%. However, it is still significantly down from its previous years' figures. Its book value has stayed flat in the last 6-7 months but the current $100 million is far from even 2021's $190-$200 million average. In Q1 2023 the NII increased, which was driven by higher net interest margin and increased income from interest rate swap positions. Furthermore, operating expenses declined, leading to distributable earnings of $2.2 million or $0.36 per share, exceeding the $0.35 per share dividend for the quarter. The company maintained its focus on balance sheet strengthening and liquidity enhancement in the face of market volatility.

Mortgage Market 2023

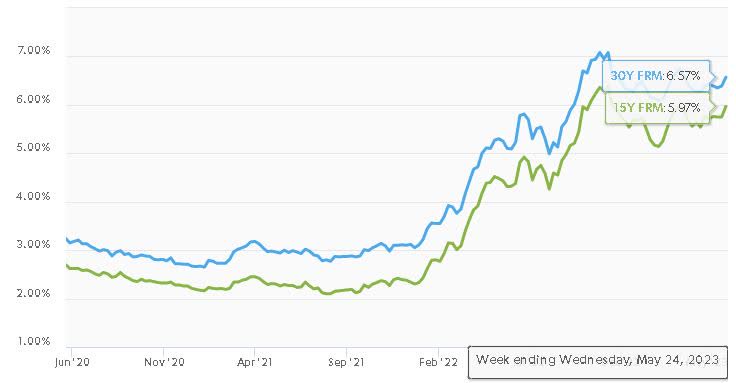

The 2023 outlook for the U.S. mortgage market suggests several challenges along with relative stability. The average mortgage interest rate has been largely consistent, hovering between 6 and 6.5%. This stability, following a record rate increase in 2022, is seen as a positive development for the housing market. In addition, I think that the mortgage rates will start to come down in the second half of the year as the Fed starts to signal interest rate cuts. However, the swift rate increase last year has reduced the number of loans suitable for refinancing, with only about $60 billion of the over $7 trillion worth of 30-year mortgages securitized by Freddie, Fannie, and Ginnie in a position favorable for a rate-and-term refinance. This higher interest rate environment is also encouraging potential homebuyers to stay put due to rate lock-in, contributing to fewer listings and sales but keeping inventory tight and spurring remodeling activity.

Despite these challenges, the mortgage performance remains robust overall, largely due to the low unemployment rate (3.4%, April) and strong household income supported by excess savings. The delinquency rate is low, with only 1.38% of all mortgage loans serviced being seriously delinquent as of the fourth quarter of 2022. Looking ahead, the outlook is focused on home sales, house prices, and mortgage originations. I strongly believe that the broader macroeconomic conditions, coupled with the dynamics of the housing and mortgage markets, will be significant factors shaping the sector's trajectory in 2023.

Mortgage rates (freddiemac.com/pmms )

{kind=link}

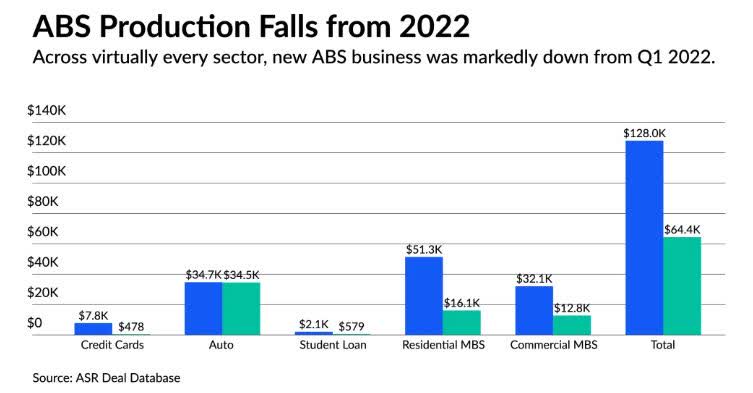

The volume of new originations decreased significantly, falling to roughly $64.4 billion by the end of the first quarter, marking a 49.7% reduction from the previous year's figures, as per the Asset Securitization Report Scorecard deal database . Contrastingly, issuers had introduced $127.9 billion in asset-backed notes into the market by the end of Q1 in 2022. The database monitors activity in main asset categories such as credit card loans, automobile loans, student loans, as well as residential and commercial mortgage-backed securities. Both CMBS and RMBS issues are down by significant numbers, WMC's portfolio consists of securitized commercial loans and residential whole loans. Approximately 90% of the investment portfolio is in these two types of assets.

ABS production Q1 2022 vs Q1 2023 (asreport.americanbanker.com)

{kind=link}

Future of Western Asset Mortgage

The COVID-19 pandemic had a detrimental effect on WMC's investments, mainly in commercial holdings, which resulted in a noteworthy dip in the value of the portfolio and stock price. Neither the price nor the company's asset-backed portfolio has recovered. Therefore, over the past two years, the management's fundamental objective was to enhance and ensure the long-term profitability of the investment portfolio and to stabilize future earnings power. During 2022, the book value per share declined and despite a small uptick in Q1 2023, I cannot see this trend changing in the near future. The Q3 and Q4 2022 results highlighted the effects of fluctuating interest rates and changes in asset values, resulting in a growth of spreads between WMC's investments. In the first quarter, the interest rates rose further so the spreads widened further.

There are two major issues investors need to be aware of when investing in WMC. Since my last article , the fundamentals of the company worsened. The first one happened in July 2022. In the summer the management had to do a 1-for-10 reverse stock split which is a big red flag for me. Stocks that are trading under $1 for more than 30 days have to be removed from the NYSE and WMC came quite close to that threshold. Before the reverse stock split it was trading at around $1.2 per share. Without the reverse split, now it would be trading at around $0.8-$0.85 per share. So as usually happens after a reverse stock split (if the fundamentals remain the same or worsen) the price has fallen further. The second issue was published in the Q4 2022 earnings call and further emphasized in the Q1 2023 call when the management authorized a review of strategic alternatives to a sale or merger of WMC. This raises the question of all shareholders if they want to remain owners in a company that plans to sell its operations.

I'd like to remind you that, last August the company's Board of Directors authorized a review of strategic alternatives aimed at enhancing shareholder value, which may include a sale or merger of the company. No assurance can be given that the review being undertaken will result in a sale merger or other transaction involving the company." - Larry Clark - Investor Relations

The Chance of a Potential Recovery

The management of WMC e xpects a positive 2023, focusing on strengthening the balance sheet and increasing liquidity amidst the ongoing volatility in equity and fixed-income markets. They improved Q1 results by driving higher earnings and asset prices across most of the portfolio, which enabled them to further reduce recourse debt. If the Fed stops raising interest rates and the external economic factors change in favor of WMC's portfolio there might be no need for the potential sale or merger of the company. The management also highlighted the credit quality of their portfolio and remain confident in its performance. They intend to further strengthen the balance sheet and maintain the earnings power of the portfolio, focusing on building value for their shareholders.

Valuation

The book value has been eroding further since my last article approximately a year ago. Despite efforts from the management, the economic book value eroded in the last year, and in 2022 alone the economic book value declined by 43% from $30.3 to $17.23 (reverse split-adjusted). At the end of the first quarter, it is standing at $17.54.

The dividend yield might suggest a great deal for investors to buy in but it is a value trap, without the underlying value. The dividend yield jumped to 20% in late 2022 and then stabilized around 15% at the beginning of 2023 and now it is trading at almost 19% again.

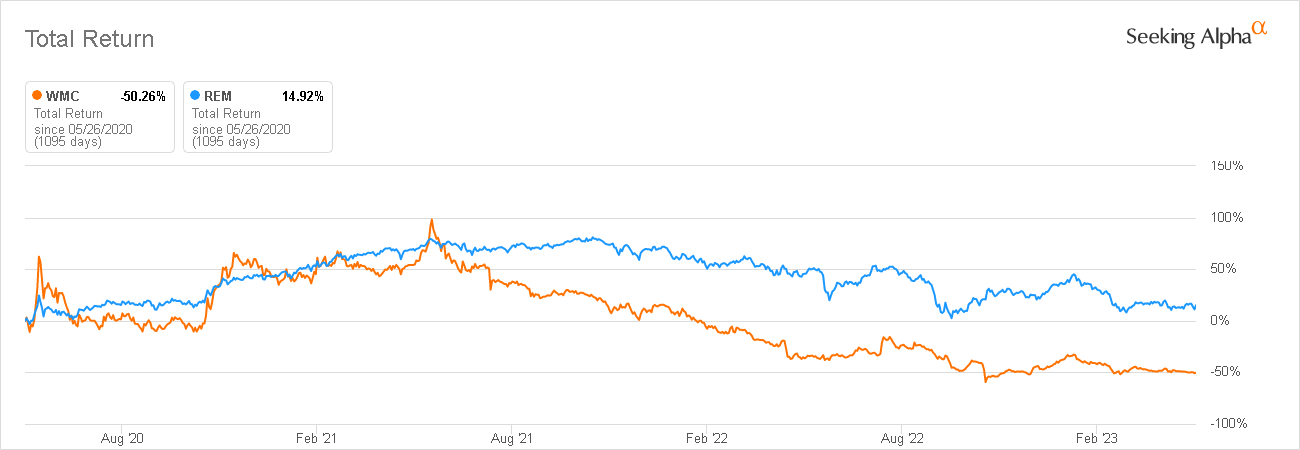

The tighter lending did not help mortgage REITs as a whole. However, if we compare one of the largest mREIT ETFs, iShares Mortgage Real Estate Capped ETF ( REM ) to WMC the difference is significant. Starting after the pandemic when most of the sector was hit very hard, REM had a total return of almost 15% while WMC had a negative 50% return.

WMC vs REM Total Return (Seeking Alpha)

{kind=link}

Final thoughts

In my opinion, long-term investors of WMC are destined to lose, and the only hope is the sale or merger of the company. I cannot see the chance that they can recover the portfolio in this economic environment and I believe the only way out is the sale or merger of the company. Those already owners might hold onto the stock hoping for a sale and a 20-30% premium price offer on the current stock price but those who want to invest in WMC could find much better options.

For further details see:

Western Asset Mortgage Capital: Little Chance Of Recovery In My Opinion