RYN - Weyerhaeuser And West Fraser Lead The Pack In Timber/Lumber

2023-10-13 14:51:59 ET

Summary

- Timber REITs are trading at discounts to their asset value, presenting buying opportunities.

- Investment in timber REITs involves different segments with their own drivers and valuation methods.

- Housing construction is the largest driver of wood product demand, and the industry is currently undersupplied.

Timber REITs are presently trading at deep discounts to the value of their assets while profit outlook is strong. There are a couple of excellent buying opportunities in the sector but also some pitfalls. This article will be a full analysis of the sector and detail why Weyerhaeuser ( WY ) and West Fraser ( WFG ) are opportunistic.

Investment in timber REITs involves multiple segments of business which each have their own drivers and methods of valuation. This article will discuss the various layers of the timber REITs and what is opportunistic given the present state of the market.

We will begin our discussion with a distinction and overview of the sector.

Timber versus lumber

Timber refers to the raw logs while lumber is the term for the processed form of wood such as a 2" by 4" plank that would be used for construction. These are separate business segments with quite different economics.

Timber is low cost and low revenue and is more of a land appreciation play. The timber businesses will sell their trees to sawmills which produces a small to moderate profit per acre while the land appreciates and can be sold for "higher-better-use". It is a very steady business. The trees are always growing and the land is always appreciating (on average).

Lumber has high input costs from buying the felled trees as well as the labor and equipment involved in milling them. On the flip side, it can turn substantial profits selling the finished product to end users. The cost structure is relatively steady while the sale price fluctuates rapidly with commodity prices. Lumber will have amazing years but also some weak years.

The investable stocks in the space have varying exposure to each segment.

- Rayonier ( RYN ) is the closest to a pure-play timber company. It owns a lot of land and sells the trees.

- Weyerhaeuser and Potlatch ( PCH ) are hybrids, each having substantial timber businesses but also enough mills to make a large chunk of revenue from finished wood products.

- West Fraser Timber, despite the name, is not a timber company at all. They are a pure-play lumber company with extensive mill and manufactured wood products operations.

The state of the industry

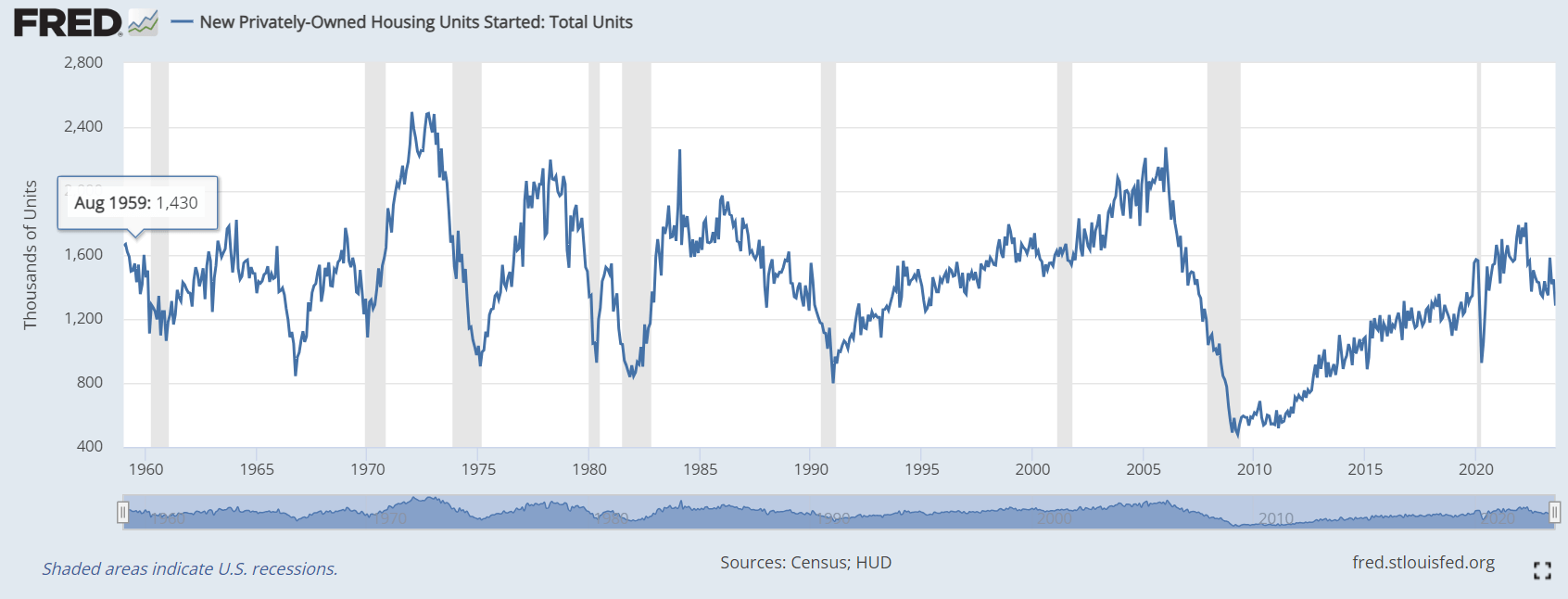

While there are various drivers of demand for wood products such as furniture or car interiors, by far the largest driver is housing construction.

Many commercial real estate buildings tend to be primarily metals with relatively less wood used while single-family homes almost universally have wooden structures. As such, lumber demand is highly correlated to homebuilding.

Homes in the U.S. are significantly undersupplied so there is a long trajectory of above-normal building volume, but the pace of delivery will depend on multiple factors. A reasonably strong economy has been stimulating construction activity which was rising nicely until high mortgage rates made home ownership rather expensive.

{kind=link}

Mortgage yields cresting over 7% seem to have slowed demand a bit yet the state of undersupply keeps demand at least moderate.

In the short term, construction volumes will be inversely tied to mortgage rates while the undersupply ensures healthy construction volumes over a longer period of time.

Turning to the supply side of the equation, we can look at both timber and lumber supply.

Timber is very regional in nature as the price per ton is so low that transportation costs make long distance movement cost prohibitive. Usually, the timber will be milled locally and then the lumber which is much higher value per pound will be shipped. Presently, there are 3 major supply events affecting timber and lumber.

- Canadian wildfires.

- European exports.

- Southern subsidized planting.

The Canadian wildfires and European beetle epidemic are interesting examples of how seemingly similar events (natural destruction of trees) can have opposite impacts.

As you know, wildfires have been destroying millions of acres of Canadian forests. I certainly do not mean to celebrate the ecological tragedy, but this is unequivocally beneficial to U.S. timber. It equates to millions of tons of competing timber supply that is just gone, literally combusted into smoke.

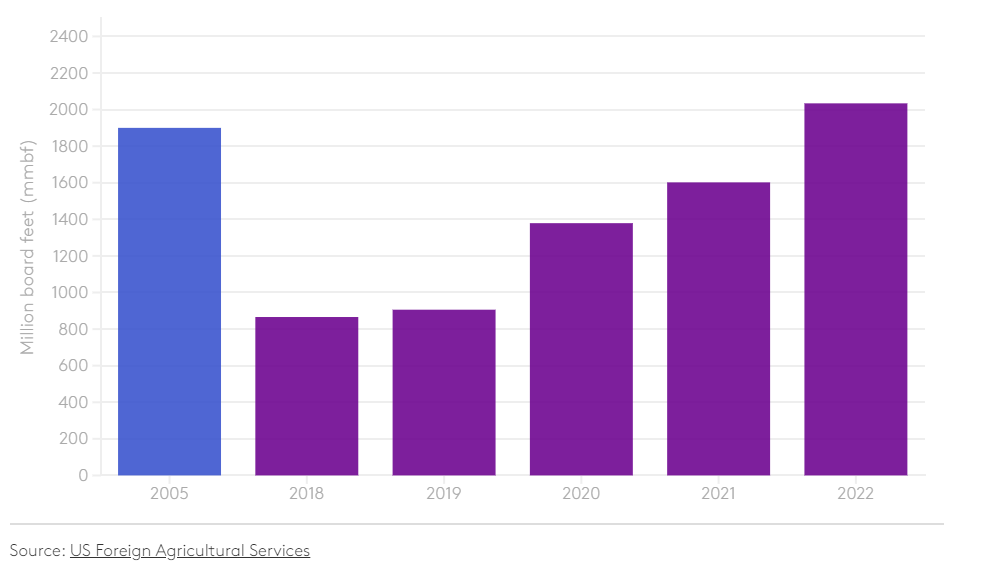

The bark beetle epidemic in Europe is different in that while these beetles can kill the trees, the timber itself is mostly still perfectly usable. Thus, these beetle outbreaks represent an acceleration of supply. Trees are harvested in mass to try to get ahead of the beetles. That timber is then milled creating a supply glut in Europe. They have had more lumber than they can digest internally and began shipping it to the rest of the world.

Shown below is the amount of lumber imported to the U.S. from Europe.

U.S. Foreign Agriculture Services

{kind=link}

Since they need to get rid of the excess supply, the sales were at fairly depressed prices which has been holding back lumber prices. Fortunately, 2022 appears to have been the worst of it and the latest reports from the timber REITs have discussed a material slowdown in imports from Europe.

Finally, timber is perpetually in high supply in the U.S. South due to government programs decades ago which financially incentivized individuals to plant forests. These incentivized forests have reached maturity resulting in enormous timber volumes.

Impact on prices

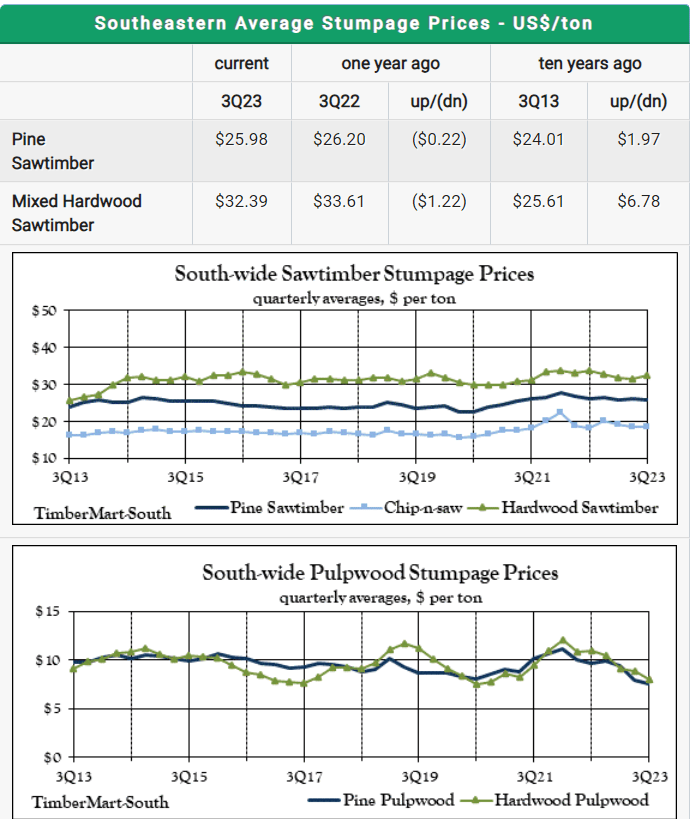

Due to the high volume of trees, timber prices in the South are very low. Stumpage prices sit at $26 per ton for pine and $32.39 for hardwood timber, while pulpwood stumpage is below $10 per ton.

{kind=link}

For clarity a stumpage price is the price you receive for someone else to come harvest the standing trees. If a company harvests the trees and delivers them they will get what is called a "delivered" price which is significantly higher.

In contrast to the South, if you were to look at prices in the Pacific Northwest where they did not have as much government incentivized forest growth, prices are much higher.

This really cheap timber in the South has 2 key impacts for the industry.

- Cheap inputs for southern sawmills.

- Lower value per acre for southern timberland.

Timberland in the South might go for something like $1500-$2000 per acre whereas the Pacific Northwest would be closer to $4000 per acre.

While the prices of timber are low, they are quite steady over time. The timber REITs generate steady revenues and profits from their timber divisions with any bumps caused by voluntary changes to harvest volume. The companies may slow harvesting during wet seasons and increase harvesting when doing so is cheaper.

Lumber prices

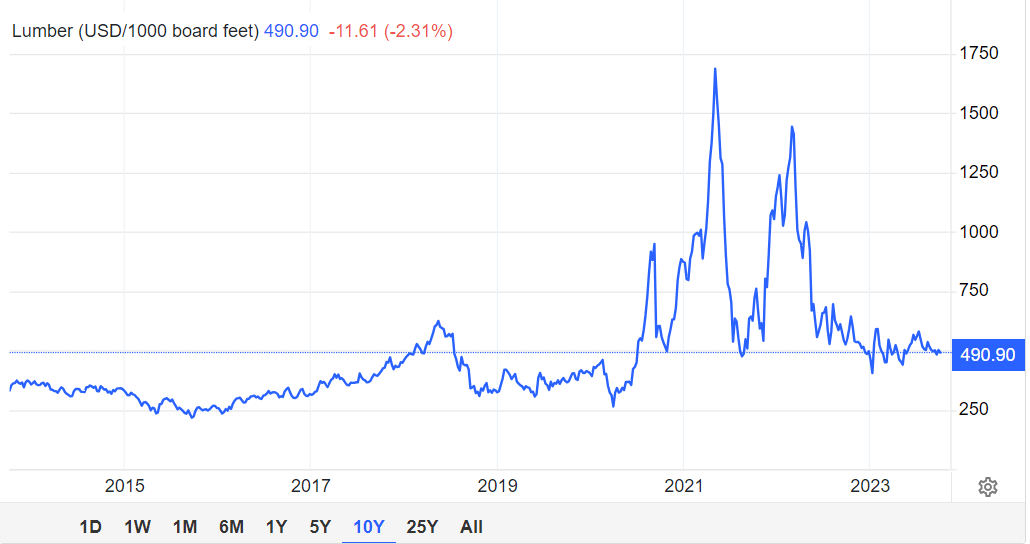

Today lumber prices are at a fairly normal level just under $500 per thousand board feet.

{kind=link}

There was some anomalous pricing in 2021 and 2022 caused by a sudden surge in homebuilding and home renovation at a time when production was still being constrained by pandemic-related distancing.

Mills operated with barebones crews so as to maintain social distancing at work. They could not keep up with demand for lumber which resulted in prices going through the roof. It was a wildly profitable time for WFG, WY and PCH.

Going forward, mill production volumes are more in balance with demand for lumber which is keeping pricing rangebound. The cessation of European imports helps a bit so I would anticipate lumber prices floating up slightly to just over $500. The biggest short-term factors are likely to be mortgage rates and the housing construction that results from that.

This present level is healthy, and the wood products segments can turn a nice profit at this pricing.

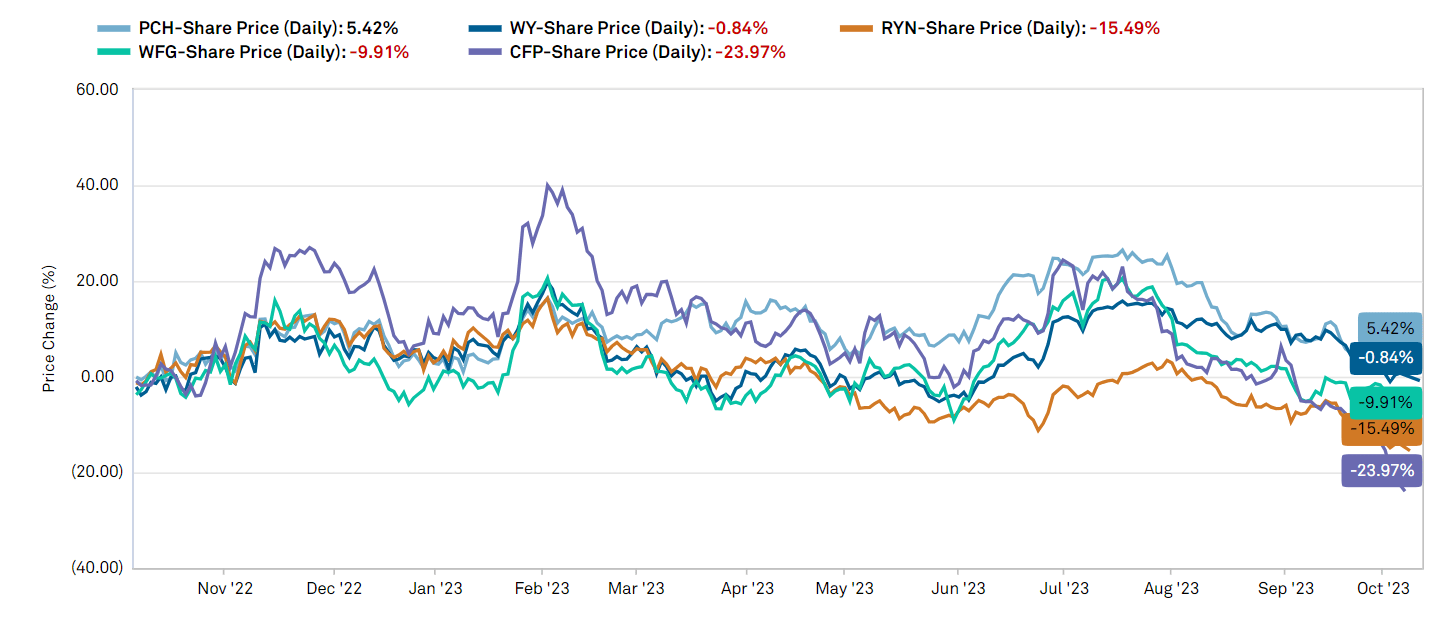

Market pricing of the timber REITs

The market tends to have a short-term memory, so when it sees lumber prices falling from $1300 to $490 it sells the sector. Most are down significantly, with the more pulp focused ones down more.

S&P Global Market Intelligence

{kind=link}

RYN sells much of its timber to its spin-off Rayonier Advanced Materials ( RYAM ) to make specialty fibers. Everything pulp and fiber seems to be challenged right now so that is likely why it is down.

Canfor and WFG are heavily mill focused, also with some pulp products and are down on the weaker commodity prices.

WY and PCH have held up relatively better in market pricing.

Valuation

Timber REITs are more complex to value than more traditional property REITs because there are so many moving parts. The approach we take is to value them as a sort of sum of their parts inclusive of the land, the timber inventory and the milling business.

Note that timberland should have a very high earnings multiple while the mill business should have a multiple more akin to a cyclical company in which one accounts for the current earnings relative to the average across the cycle. In other words, it should be at its lowest multiple when earnings are the highest within the cycle. If one were to just look at multiples alone they would always end up selecting the milling companies. Notice that the pure-play milling company WFG trades at 4.4X 2024 EBIDTA while the hybrids trade in the teens and the pure-play timber REIT trades at 21X EBITDA.

Analyst consensus estimates from S&P Global Market Intelligence. Market data as of 10/6/23

{kind=link}

Directionally, these multiples are correct. However, the spreads between the multiples might be too large or too small which we will uncover as we go through the full valuation.

Let us begin by valuing the mills.

WY has 35 mills or other wood products manufacturing facilities. Potlatch has 7 and RYN has 0. These facilities range greatly in value with some recent transactions of industrial scale facilities going for $55 million and others for $300 million. That gives us the following implied valuations for their milling businesses.

Source: 2nd Market Capital based on compiled data from company filings. Market data as of 10/6/23

{kind=link}

WY's facilities are on the large side averaging about 290 mmbf in annual production per mill. This is quite close in size to the mill that was recently purchased by WFG for $300 million. Thus, I would spot WY's mill value at close to that end.

Potlatch mills are more medium in size/production. Thus, I am spotting their mill value in the middle of the range.

Land and trees

These companies are some of the largest landowners in the country. WY controls 24.6 million acres, RYN 2.8 million, and PCH 2.176 million.

Source: 2nd Market Capital based on compiled data from company filings. Market data as of 10/6/23

{kind=link}

The location and ownership structure of the acres matter. The Canadian government owns most of the timberland in Canada and leases it out to companies like WY for harvesting. Thus, the 14.1 million acres WY controls in Canada are not owned by the company so they will not get a residual value on the land. Rayonier's New Zealand land is similar. Thus, it is not the total acres column in the table above that matters so much as the total owned acres column on the right.

In valuing the land, we must also consider stocking level. A clearcut acre is not worth as much as an acre filled with trees ready for harvest. We like to value the standing inventory separately from the land.

WY's land is the best stocked at 56 tons of standing trees per acre compared to 49 tons at PCH and 32 tons at RYN.

Source: 2nd Market Capital based on compiled data from company filings. Market data as of 10/6/23

{kind=link}

Those trees can and will be sold. The value per ton will vary depending on pulp percent, location and species. Averaging these buckets with the weighted average of their typical harvest volumes I spot the value of standing inventory at about $17.50 per ton. It will almost certainly sell for much more than this, but that is my estimate for the realized value after harvesting and shipping costs.

So now that we have estimates for the values of the mills and the standing inventory we can back into the value of the land that is implied by the market price of the stocks.

Source: 2nd Market Capital based on compiled data from company filings. Market data as of 10/6/23

{kind=link}

Since we know the acres owned by each company we can calculate the implied value per acre.

Source: 2nd Market Capital based on compiled data from company filings. Market data as of 10/6/23

{kind=link}

Rayonier's valuation per acre looks about right to me. $2065 per acre is perhaps slightly high for southern timberland but quite low for northern timberland so given their mix between the two categories that strikes me as being in the right ballpark.

WY and PCH look significantly undervalued with the land portion of their businesses trading at implied values of $795 and $672 respectively.

2 buys and a pitfall

From a valuation perspective the entire sector looks fairly attractive with the timber REITs all trading at a price to NAV in the mid-70% range.

The value trap

RYN, despite the higher implied EV per acre, is also in a mid-70s price to NAV. However, I think it might be a value trap. I am of the belief that timber is structurally oversupplied which will make earnings from that business somewhat weak for the foreseeable future. This will be somewhat offset by land values shooting up across the country which amps up the appreciation component of the land. However, HBU is more of a long-term plan so I prefer the companies that are generating more serious cash flow while we wait.

Rayonier is too exposed to the oversupply which is made worse by not having its own internal use for the timber. It does not have mills to send its own timber to and since the spin-off it does not even have a place for its pulp. This subjects RYN to market prices of the raw materials which I think will remain weak.

The buys - WY and WFG

The hybrids, WY and PCH are well positioned because they can send a large portion of their timber production to their mills. This bit of vertical integration provides excellent margin on the milled products and I do anticipate lumber realizations coming in strong.

The European exports headwind is subsiding and eventually people will get used to higher mortgage rates. People need somewhere to live and homes will be built so lumber demand has a great outlook.

I view WY as slightly better than PCH. They trade at similarly cheap valuations, but WY has 2 key advantages:

- Superior scale.

- Operational excellence.

WY has a continual focus on efficiency resulting in higher EBITDA margins. I think that warrants some sort of a premium yet WY trades at 74% of NAV and 13.5X EV/EBITDA.

West Fraser is the more aggressive way to play the space. It does not have the land appreciation as a cushion against volatility in commodity prices, but it has explosive potential.

- In 2021 WFG generated $4.6B in EBITDA.

- In 2022 WFG generated $3.3B in EBITDA.

This is a company with a current EV of $5.26B. The market is not giving any credit to those numbers because the extreme earnings numbers were associated with the anomalous spike in lumber prices that took place in 2021 and 2022. It is unlikely to repeat at that extreme of a level, but the profits obtained during that period did wonders for the balance sheet.

Due to the cash generated, WFG now has negative debt as nearly $1B in cash is greater than their debt. So while earnings may be volatile depending on where commodity prices go, WFG is well-positioned to handle weak times and capture huge gains during the good times.

Looking forward, even with lumber prices at the moderate level of today, WFG's earnings look quite good with a forward EV/EBITDA multiple of 4.4X.

What the market is missing

Mortgage rates breaching 7% have scared the market into selling off any related sectors. I get that coming from an environment of 3% mortgages that 7% seems unacceptably expensive, but I think this is a short-lived phenomenon.

It is not that mortgage rates will necessarily drop back down, but rather the emotional response to 7% mortgages will subside. It will simply become the new norm.

There is a certain inevitability to homebuilding. It is not like other products which can be foregone. If people drive less in a given quarter those gasoline sales are just gone, whereas if fewer homes are built in a quarter, that remaining demand is still there. People can put off buying a home but eventually they need one.

The market is pricing in a nearly 20% discount to housing-related stocks due to mortgage rates. I view it as a complete non-factor in the long run. Time will tell who is right.

For further details see:

Weyerhaeuser And West Fraser Lead The Pack In Timber/Lumber