BNO - What Will OPEC+ Do?

2023-11-26 11:45:11 ET

Summary

- Oil price volatility will be heightened until OPEC+ decision time.

- Fundamentally, the oil market doesn't require an additional cut, but we think OPEC+ will announce an additional coordinated cut.

- In the meantime, the oil market healing process is underway, so it will take time.

Last Friday saw oil prices surge following rumors that OPEC+ is considering deepening production cuts to offset weaker oil prices. This week will have a lot of volatility as traders front-run the prospects of deeper cuts or take profits ahead of the meeting. Either way, readers should expect a lot of back and forth.

But before we talk about what OPEC+ will do, it's important to revisit some of the things we've said and what the consensus is going into this meeting.

On Nov 8th, we published an article titled, "Is an OPEC+ coordinated cut coming?" In the article, we said:

OPEC+

As the article has already pointed out, there are conflicting views out there. OPEC+, in its monthly reports, believes that global oil demand is strong. And because of that view, OPEC+ has only resorted to the voluntary cuts from Saudi to hold balances together.

But as we argued, that simply can't be the case. The market, in our experience, has never given this many conflicting signals to a narrative. As a result, OPEC+ also needs to acknowledge that demand is likely weaker than what's being shown on paper.

In essence, Saudis will need to convince the rest of OPEC+ that this needs to be a coordinated effort.

For the Saudis, this argument will be an easy one to make. Global economic indicators continue to soften. The Fed continues to remain hawkish with rates, so tighter monetary conditions will continue. And if a recession is coming, then OPEC+ will need to cut in a coordinated matter to stave off inventory builds.

Perhaps our criticism of IEA was wrong. Maybe balances for 2024 are implying bigger builds, and if so, it will be in OPEC+'s hands to fight off not only the physical oil market balance but also the perception of the oil market.

IEA

We think outside of Russia and Saudi, the rest of the group would need to cut supplies by ~1 million b/d. For Russia, the cut needs to be material enough to reduce crude exports back to ~4.3 million b/d (-700k b/d from here) . For the Saudis, they would simply extend the voluntary production cut of ~1 million b/d.

Effectively, this would bring OPEC+ crude exports down to ~26.5 million b/d or somewhere between 2021 and 2022.

Kpler

This export level would also match the lows we saw in August that prompted heavy global oil inventory draws. If demand does weaken as the market expects, then not only will global oil inventories not build, they should continue to decline.

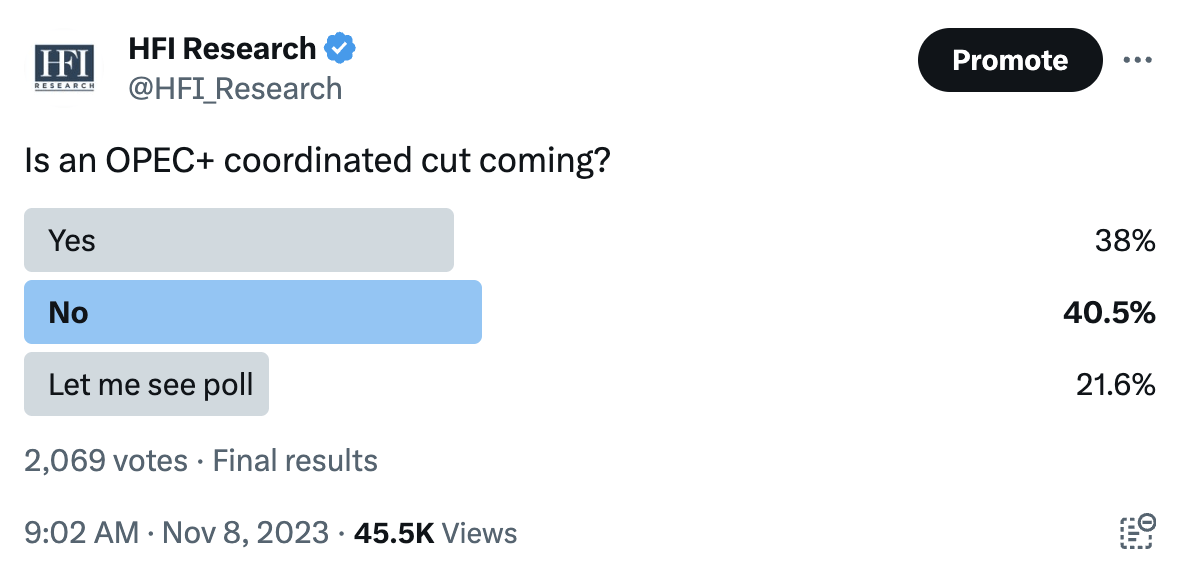

As for the consensus, we did a poll on Twitter that showed mixed results.

{kind=link}

Half of the people thought it was "no", and the other half thought it was "yes".

Looking at sell-side estimates, no one is expecting a coordinated cut. Instead, the market expects Saudi and Russia to extend their voluntary production cut into 2024.

What will they do?

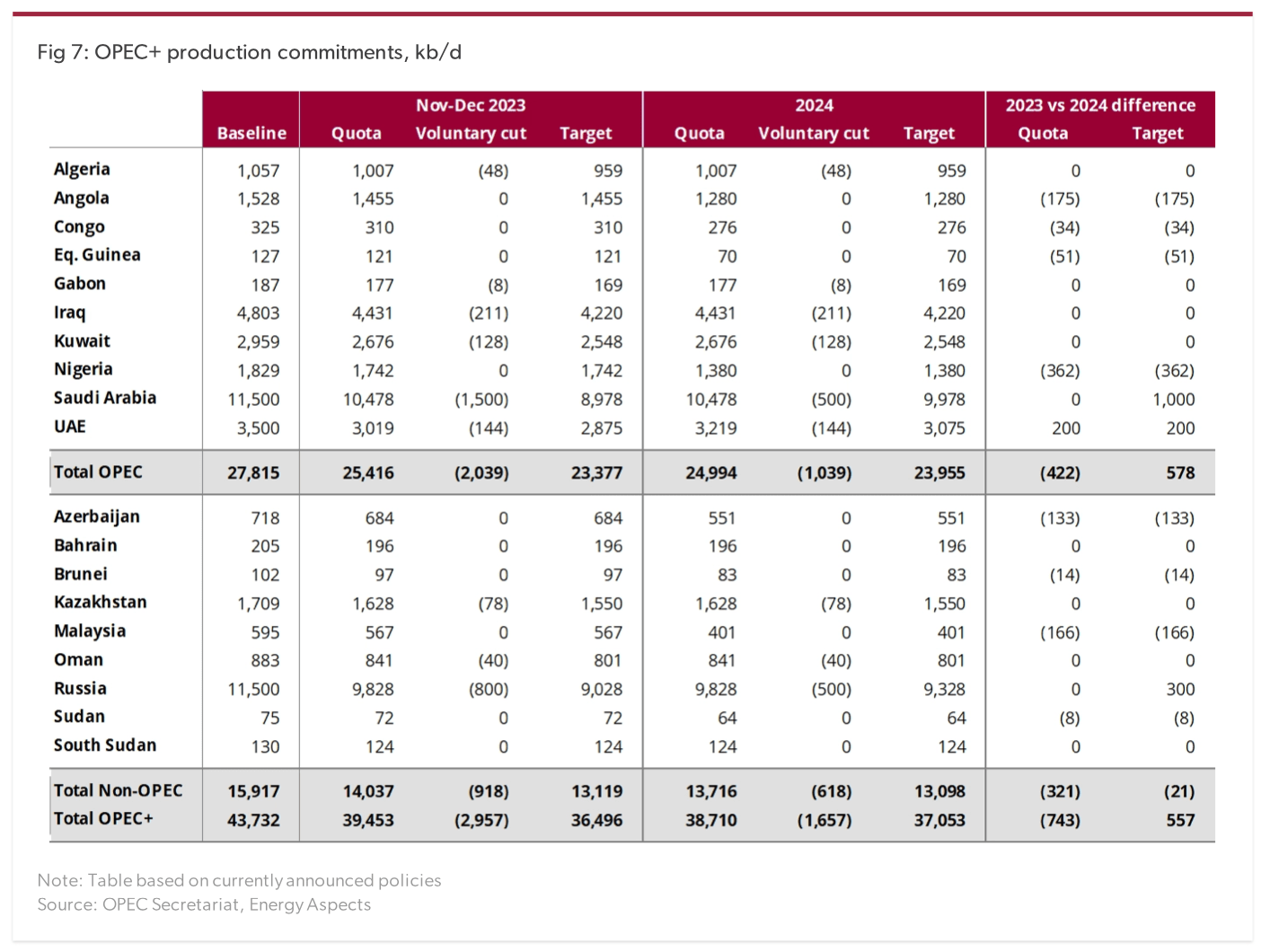

Here is the current baseline for OPEC+:

{kind=link}

As you can see, total OPEC+ supplies will increase by ~557k b/d in 2024. Most of that increase will come from Saudi increasing production back to ~10 million b/d. UAE is expected to increase production by ~200k b/d under the current quota system.

Now we argued in our write-up back on Nov 8 that a coordinated cut is possible. The main reason for this argument is that demand is much lower than what OPEC+ is seeing. In our years of following the oil market, we have never seen such a large conflict in data and narrative. If the bulls (we are bulls) argue that demand is strong, then why aren't we seeing it in the physical market? For example, why are there so many unsold cargoes resulting in physical market weakness?

In addition, if demand was so strong, why are refineries forced to reduce throughput? These contrary data points suggest to me that demand is not really that strong, and OPEC+ needs to look at the possibility of demand disappointing to the downside.

But this time, it can't just be the Saudis that do the heavy lifting. They've already done all the heavy lifting. As a result, this has to be a coordinated effort. UAE, Kuwait, and Iraq will all have to participate to meaningfully reduce supplies.

Looking at the table, it looks difficult to squeeze out another ~1 million b/d. UAE may agree to reduce production by ~200k b/d, Kuwait may reduce by ~100k b/d, and Iraq may reduce by 200k b/d. All-in-all, this only leaves us with ~500k b/d. Other cuts, if agreed upon, would be symbolic in nature, so from the market's perspective, they would be irrelevant.

This means that the best outcome we could see out of this meeting would be:

- Extension of voluntary cuts from Saudi and Russia (~1.3 million b/d total) to the end of June 2024.

- Additional ~500k b/d of voluntary cuts from UAE, Kuwait, and Iraq to the end of June 2024.

Now I'm not saying that the Saudis wouldn't cut production further, but at ~9 million b/d, we think that's the most they are willing to go without infuriating the US and fear of losing market share.

Is it a supply issue or a demand problem?

I think it's a bit of both.

Supply:

- US oil production surprised ~250k b/d to the upside (12.9 million b/d was our original forecast).

- Iran's production at ~3.4 million b/d is ~600k b/d higher than most expected at the start of 2023.

- Brazil is about ~100k b/d higher than most analysts forecast today.

- Russia is not really cutting ~300k b/d.

End result is a total supply side surprise of 1.25 million b/d.

Demand:

- OECD countries continue to underperform 2019 baselines.

- China's apparent oil demand of ~17 million b/d must include a lot of "stockpiling".

But like all black boxes, we don't know demand until after the fact, so the market is our only real guide. However, we do know that at this moment in time, the market is balanced to a small deficit, so it's not good news when you go into H1 2024 when it's seasonally the lowest demand period.

This is why I think for OPEC+, the least risky route is to announce a coordinated cut. Headline figures may look like an additional coordinated cut of ~1 million b/d, but the reality will be a cut of ~500k b/d (UAE, Kuwait, and Iraq). Everyone else will just produce as is, and have their quotas reduced to look like a larger cut.

For the oil market, this may be enough to push speculators away and let fundamentals heal on their own. As we've written numerous times in the past week, every reader should be watching refining margins, when that recovers, you know the oil market healing process is underway. And fortunately, it is.

{kind=link}

Conclusion

Our view is that OPEC+ will announce a coordinated cut. While on paper, it's not needed, I think for both sentiment and the possibility of weaker demand, it's needed. If they announce an additional cut of ~1 million b/d, only ~500k b/d will be the real effective cut. For the market, this will be viewed positively, and the fundamental healing process will be accelerated.

Either way, oil market volatility will be high this week as traders attempt to front-run any news.

For further details see:

What Will OPEC+ Do?