PSCE - What Worked In 2023 What Didn't And 3 Energy Picks For 2024

2024-01-01 07:38:22 ET

Summary

- Energy had a poor 2023, but there were important differences within the sector.

- Oilfield services stocks, specifically those with offshore and international exposure, are outperforming relatively.

- I summarize my macro and energy thesis for 2024 and discuss three ideas in the sector.

Energy performed poorly in 2023

After outperforming the broader market ( SPY ) in 2021 and 2022, the energy sector ( XLE ) was the second-worst performer this year, only ranking above utilities:

Even financials ( XLF ) did better despite the five regional bank failures.

Both oil ( CL1:COM ) and natural gas ( NG1:COM ) prices were much lower compared to 2022, so this is understandable:

Nonetheless, it's worth noting that despite the recession fears that marked much of the year, a U.S. recession hasn't materialized so far. Oil demand in the U.S. and globally has been quite good too.

Instead, the weaker prices appear driven by the unexpected increase in supply, including a new record in U.S. production - or near record depending on what you make of the whole debate around the EIA methodology:

I would like to point out though that the oil prices aren't really low compared to the pre-pandemic years. Natural gas may be low and a number of U.S. gas-focused producers are generating negative cash flow, but many oil investments remain profitable.

Relative performance gaps emerged

A year ago, I speculated that as energy was completing its comeback from the pandemic lows, relative performance within the sector would start to matter more.

I predicted less upside for the large caps Exxon ( XOM ) and Chevron ( CVX ) that dominate the XLE and had led the recovery up to that point. I suggested more opportunities may be found in:

- Oilfield services stocks;

- Smaller caps;

- Stocks with exposure to the offshore capex cycle.

To a large extent, these organizing themes did play out, although the negative XLE returns make the relative outperformance of my favored subsectors less impressive.

Oilfield services did better than E&P

Oilfield services ( XES ) outdid the XLE by about 10 percentage points, though most of that was concentrated in the second half of the year:

Some of my better ideas in the OFS space included the bullish calls this spring on the fracking companies Liberty Energy ( LBRT ), ProPetro ( PUMP ), and NexTier, the latter now acquired by Patterson-UTI ( PTEN ). These stocks, which had gotten very oversold during the regional banking crisis, ended up gaining 50% by late summer.

Not all services did well, though. Apart from the highly speculative micro-cap Nine Energy Service ( NINE ) that I got very wrong, some larger players with respectable businesses are also finishing 2023 deeply in the red:

I wrote a lot throughout the year about the performance differentiators, but even in the onshore services space factors such as gas vs. oilier basin exposure, the proportion of private vs. public clients or fleets contracted long-term vs. participating in the spot market would matter a lot.

Small-caps also outperformed

Small-cap energy stocks ( PSCE ) also modestly outperformed the XLE:

However, as PSCE includes both producer and services names, I am not sure if this result isn't mostly driven by the services factor. Small-cap E&P stocks remain more discounted, but it is also becoming clear that many of the smaller shale producers are running out of core inventory, so the discounts could be well justified.

Offshore services were the big winner

Offshore services stocks, like drillers Borr ( BORR ) and Transocean ( RIG ) on which I have been long-term bullish, did quite well compared to onshore drillers like Nabors ( NBR ) or PTEN:

Despite the weakness in North America, international and offshore services demand has remained quite robust, and this trend is often emphasized by services majors like SLB ( SLB ).

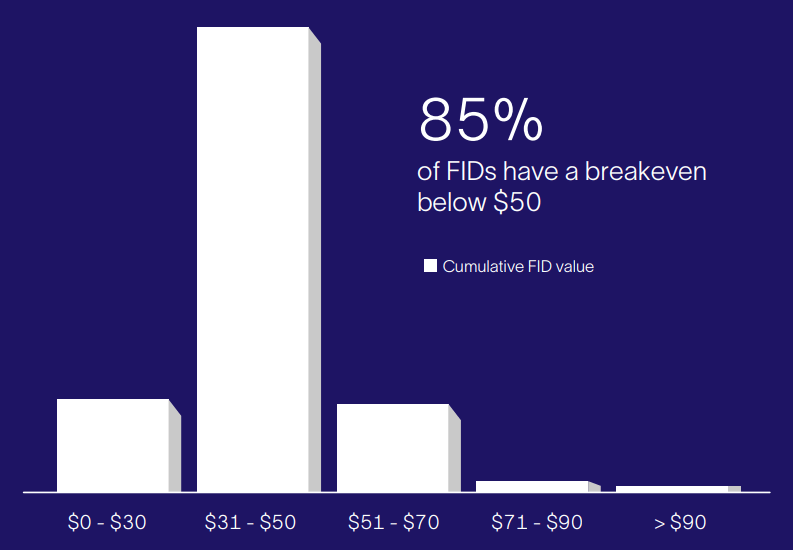

The OFS supply constraints in the offshore space are bigger, likely because offshore services were in the doghouse a lot longer, which has translated into much attrition. However, the demand is also stronger, driven by better profitability; for example, SLB believes 85% of the offshore FIDs have a breakeven below $50 :

{kind=link}

Lastly, North American oilfield activity is "demand-driven"; if the price expectations get low enough, producers will cut spending. Much of international demand on the other hand is "supply driven" as national oil companies (or NOCs) may also have to fulfill long-term energy security mandates, which makes the capex cycle more robust.

Setting up for 2024

Turning to 2024, I will first lay out my macro expectations:

- No U.S. recession or at best a very modest one;

- Continued deceleration in inflation but not all the way down to the coveted 2%; probably down to 3% with some upside risk in 2024 H2;

- The Fed and other central banks cut a bit, though, pushing up commodities;

- Weaker dollar/stronger emerging markets.

In the energy space, I expect:

- Average $70-$80 crude oil ( OIL ); some push-pull between geopolitical risks and OPEC's spare capacity while U.S. shale production growth moderates;

- More downside for U.S. natural gas in 2024 H1 as we are already halfway through the winter with no major events so far;

- Sustained international and offshore capex, with flat U.S. activity and single-digit growth in Canada.

I recently posted a summary of the oil price forecasts from several major banks and research firms:

Reuters; The Energy Realist

You will note no one is predicting excessively low or high prices. Perhaps after the extreme 2020-2023 years for energy, we are finding some equilibrium. While oil price forecasts are notoriously wrong, I think this time the E&P equities seem to agree with $70-$80 oil as many companies appear fairly valued at this price range.

If you consider some of the larger U.S. independents below, enterprise value to EBITDA ratios have settled into a 10-15x range:

This implies a 7 to 10% FCF yield, which is consistent with the cost of capital. It is probably still better than what the rest of the S&P500 can offer, but these are no longer the screaming bargains of two years ago.

On the services side, I expect the international and offshore tailwinds to continue. Relative to the E&P equities, services still have a lot of headroom:

The SLB to XOM ratio is off the pandemic lows but below even 2018 which was hardly an OFS bull market.

Finally, while the long-term bull market is offshore, I have also made some shorter-term onshore services bets for 2024 that are valuation driven. Even with flat U.S. projections and modest growth in Canada, at some point, the valuation multiples can get ridiculous enough to make the risk-reward attractive as it happened with LBRT and PUMP back this spring.

Three stocks to consider for 2024

With this "big picture" view in mind, here are three stocks that are among my principal bets going into the new year.

Borr Drilling

BORR specializes in premium jack-up rigs that are used in shallow-water drilling. The supply is tight while demand is robust, which pushes up utilizations and dayrates.

The stock is rated "buy" by Seeking Alpha, although I am one of the two analysts included in the recommendation average. However, Wall Street is also quite bullish on Borr Drilling:

{kind=link}

BORR has been recovering from a correction and as I have pointed out benefited quite a bit from the Fed's dovish comments earlier this month:

TradingView; The Energy Realist

I think that tells you which way things may go if the expected easing materializes in 2024.

Ensign Energy Services

The next stock I want to call out is my short-term bet on Ensign Energy ( ESI:CA ):

You can check out the details in my recent article , but long story short, this is one of my valuation bets on the deeply discounted onshore services names I mentioned.

Enterprise value is 3.4x 2024 and also 2025 EBITDA. Ensign has significant exposure to Canada, where I expect activity to pick up in 2024 despite the potential TMX delay in the news. In the U.S. Ensign should also do well given it has higher spec equipment and the company is also present internationally in places like Argentina and Kuwait. So it benefits from the "long-cycle capex" as much as it is subject to the more uncertain U.S. shale demand.

Seeking Alpha rates the stock a "buy" but that isn't much validation as I am the only analyst covering it. Wall Street, though, appears very bullish:

{kind=link}

Technically, Ensign also looks good to me as it appears to have bounced off an important resistance level after getting quite oversold, reaching an RSI of 22.

SLB

Last but not least, I will also flag my long-term position in SLB (formerly Schlumberger), which I view as the Exxon of oilfield services.

The upside is not as much with such a large company, but the risk is less too and SLB is already paying close to a 2% dividend:

{kind=link}

Oilfield services names have considerable operating leverage, so SLB's EBITDA will continue to outpace revenue growth, and I expect margins to hit 25% at some point:

If you wonder why not the cheaper valued Halliburton ( HAL ), SLB has tilted its business more to the international and offshore side while U.S. onshore services remain a bigger piece of HAL.

SLB is also coming off a correction and is still 20% below its 52-week highs:

Bottom line

The resilience of the U.S. economy (helped by the fiscal side) and the Fed pivot are likely taking off the table a recessionary crash in oil prices for now, but I am not buying the energy crisis narrative either. We have seen in 2023 that $70-$80 oil can support adequate investment and production growth for the time being.

While I continue owning E&Ps, I don't expect wonders from them and I have tilted my energy allocation to services, which mostly includes stocks with offshore exposure plus some opportunistic bets on onshore names.

Happy trading in the new year, and feel free to share in the comments where you see the most upside going into 2024.

For further details see:

What Worked In 2023, What Didn't, And 3 Energy Picks For 2024