ENIC - While Enel Chile Continues To Advance It's Hard To Cheer Its Value Proposition

2024-01-03 00:25:21 ET

Summary

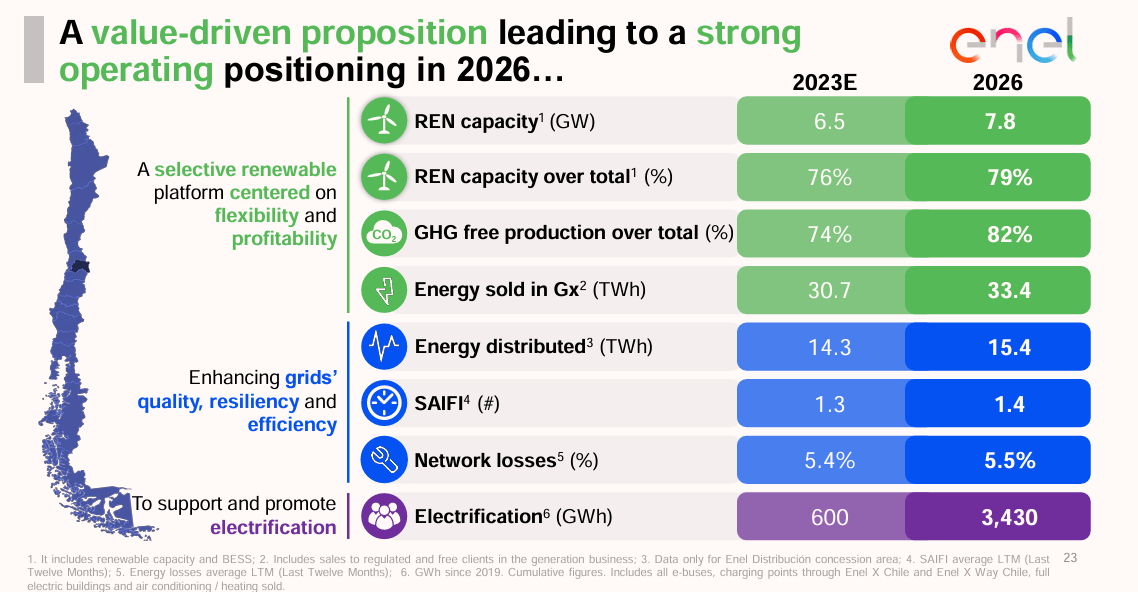

- Enel Chile plans to increase its renewable energy capacity to nearly 80% by 2026.

- The company aims to expand its battery and energy storage capacity by 700 MW, with an estimated cost of $0.6 billion.

- Enel Chile is advocating for regulatory and remuneration reforms in Chile's distribution segment to support extensive electrification.

- Shares do not offer a bargain at today's levels.

Enel Chile ( ENIC ), is predominantly owned by the Italian company Enel SpA ( ENLAY ) with a 64.9% stake and listed on both the Santiago Stock Exchange and the New York Stock Exchange via its ADRs. The company's holdings include a 94% stake in Enel Generación Chile and full ownership of Enel Green Power, positioning it significantly in Chile's generation sector, primarily comprising 63% hydro and renewable energy sources.

Chile is taking proactive steps by placing the distribution business regulatory model at the forefront. Additionally, there are ongoing discussions in Congress regarding a structural reform in the generation business that involves the management of batteries, storage systems, and remuneration for ensuring supply safety. ENIC recently laid out its 3-year strategy and the latest guidance doesn't propose significant deviations from previous directives but it does reassert ENIC's outlook of transforming its capacity to be nearly 80% derived from renewable energy. Despite the current guidance not indicating substantial changes from prior directives, in my view the stock is fairly valued today and does not present compelling upside at present levels.

Strategy Overview and Update

ENIC operates on a vertical utility model. Enel Chile is committed to being active in generation, gas commercialization, and power distribution, positioning itself to capitalize on the energy transition and the anticipated rise in electrification. At the most recent investor day , the CEO emphasized a "balanced" approach in their Business Plan, aiming for equilibrium across geographical reach, business mix, spot markets, and client profiles. When questioned about a $300 million investment in distribution with seemingly modest returns, management highlighted their belief in a future shaped by energy transition and electrification. They view grid infrastructure as pivotal, making this expenditure a strategic investment. Additionally, ENELCHIL is increasingly confident in the returns of forthcoming greenfield generation projects due to improved industry conditions.

Over the next three years, the company plans to expand its capacity by 1.3 GW, reaching a total of 9.9 GW by 2026, with 79% of this capacity sourced from renewable energy. The overall capital expenditure is expected to increase from $1.7 billion to $2.3 billion, primarily allocated to bolster battery energy storage systems (BESS). A portion of this investment will follow a stewardship model, maintaining project control while alleviating pressure on the balance sheet. The company is notably boosting spending on storage systems, scaling up from 0.2 GW to 0.7 GW, and focusing on solar projects in the central region for distributed generation.

{kind=link}

The updated guidance for ENIC shows minimal alterations. The expected EBITDA by the end of 2023 stands at approximately $1.25 billion (mid-range), with a projected increase of around 15% by 2026, reaching $1.4 billion (mid-range). However, the cumulative EBITDA for 2024-2025 in the new plan sees only a marginal 3% rise. The company aims to achieve a leverage rate of <=2.5x net debt/EBITDA by the end of 2026, aligning with the previous plan's 2025YE target. Simultaneously, it plans to maintain a minimum earnings payout of 50%, consistent with the previous strategy. Anticipated net income attributable to shareholders in 2026 is expected to be lower compared to 2023 (pro forma), primarily due to increased participation by minority stakeholders associated with growth capital expenditure within the stewardship model. Projections indicate that the company's EBITDA might trend towards the lower end of the guidance range from 2024 to 2026.

Enel Chile strongly advocates that Chile's current regulatory framework isn't suited for a scenario of extensive electrification since hydroelectric generation is highly reliant on both rainfall and snowmelt, both of which cannot be relied upon with a high degree of certainty. The management team emphasizes the critical need to overhaul both the regulatory and remuneration models in Chile, particularly within the distribution segment. Progress on this front within the legislative arena has been limited, but there's a noticeable increase in political awareness and market consensus compared to the previous year. Politicians and lawmakers appear convinced of the urgency to reform distribution regulations, with expectations that these discussions might gain momentum following Congress's resolution of the new tariff stabilization mechanism. ENIC is eagerly anticipating the conclusion of the 2020-2024 tariff review, with initial analyses indicating potential revenue upside. The regulator has already commenced the 2024-2028 review process, fostering a slightly more optimistic outlook for the final outcome and expecting a more efficient process compared to the ongoing delayed reset.

Battery and Energy Storage Capacity to Rise

Enel Chile is planning to expand its battery and energy storage capacity by 700 MW, with an estimated cost of $0.6 billion. Presently, the company is assessing the feasibility of incorporating either 2-hour batteries at a cost of $0.9-1 million per MW or longer-duration 4- to 5-hour batteries, which would be more expensive. The final decision on the type of batteries will hinge on the investment's returns. The company's strategy involves linking these batteries with its own generation initiatives, ancillary services, and opportunities for shifting energy. However, the compensation structure for grid safety through battery deployment remains unclear. Although an auction was proposed in the energy bill being deliberated, the specifics of its organization and potential success are uncertain.

ENIC confirmed favorable market conditions, presenting an opportunity to engage in negotiations for various prospects, including significant contracts with major mining clients. There's optimistic traction towards securing long-term contracts for renewable projects with promising profitability. However, despite declining to specify a precise figure, the CEO indicated that the price range of $40-50/MWh for new Power Purchase Agreements (PPAs) no longer aligns with the current market dynamics. This shift is driven by factors such as certain market entities stabilizing spot price fluctuations, constraints in transmission capacity, and additional risks involved.

Leverage Reduction Planned

ENIC aims is to reduce leverage, aiming for below 3.0x by 2023 and further below 2.5x by 2026 . Efficiency gains from capacity additions should drive higher margins. Coupled with developing new capacity through partnership models, this strategy is expected to enhance returns, optimize capital allocation, and strengthen the company's financial standing.

ENIC Valuations Do Not Represent a Good Risk Reward Today

With the investor day outlining more of the same and only minor tweaks, it is quite likely that we will see a "steady as she goes" approach in the coming quarters. Against this backdrop, ENIC valuations do not represent a bargain.

{kind=link}

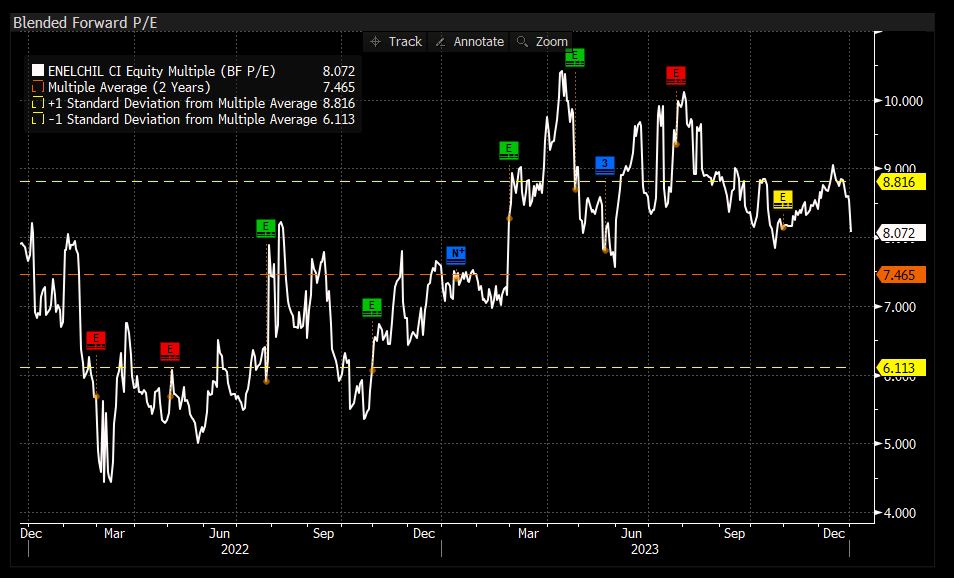

When analyzing the company's valuation on a forward P/E basis, we see that ENIC trades at a forward P/E of 8.1x and ~8%% higher the two year average of 7.5x

{kind=link}

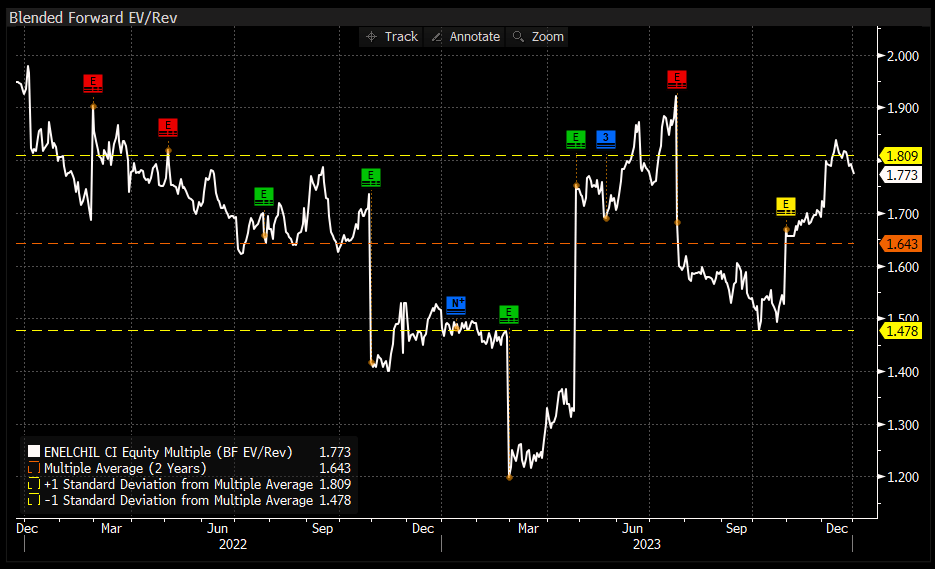

On an EV/Revenue basis, the company trades at 1.8x versus its historical average of 1.6x, or about 12% higher than average.

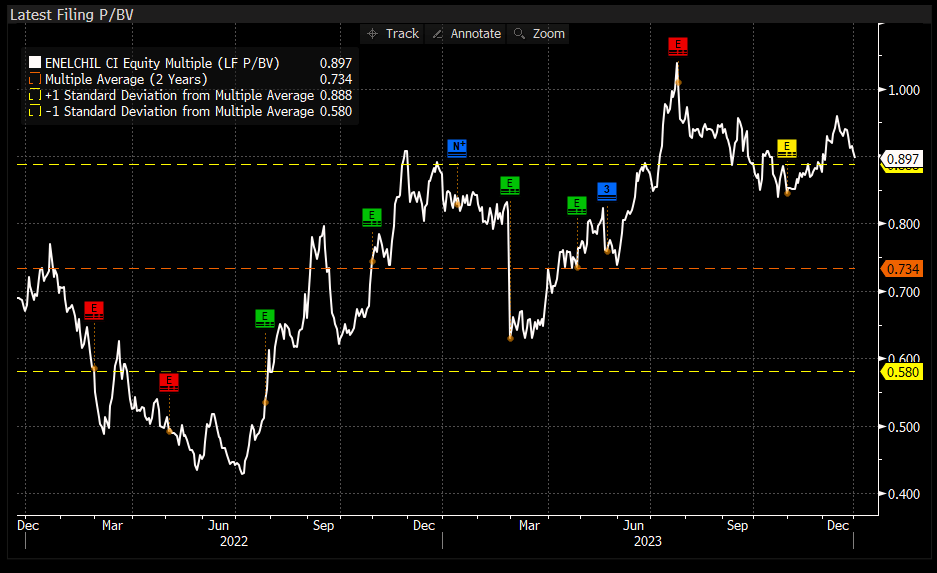

When looking at ENIC on a book value basis, the shares also appear expensive.

{kind=link}

The average book value multiple for ENIC has been 0.7x. When compared to its current valuation of 0.9x, this represents a 29% premium.

The valuations must be evaluated from a perspective that ENIC is a reasonably stable company which has traded in a fairly tight range as far as multiples are concerned. The company becomes a much better buy when its P/E multiple is below 7x and its P/B ratio is closer to average.

Conclusion

The fresh guidance presented at the latest investor day doesn't hint at any substantial alteration in guidance, affirming my belief that the stock does not represent a bargain value. My suspicion is that over time, its P/B ratio might creep higher as investors begin paying a premium for the higher mix of renewables in ENIC's portfolio. However, between then and now, investors who have an eye on this name will likely find better buying opportunities when valuations drop below the historical averages.

For further details see:

While Enel Chile Continues To Advance, It's Hard To Cheer Its Value Proposition