U - White Brook Capital Partners Second Quarter 2023 Commentary

2023-07-16 05:00:00 ET

Summary

- White Brook Capital Partners' NAV increased by 16.09% in Q2 2023, outperforming the S&P 400 Midcap Index and the S&P 500.

- Year to date, the Fund's NAV increased by 13.37%.

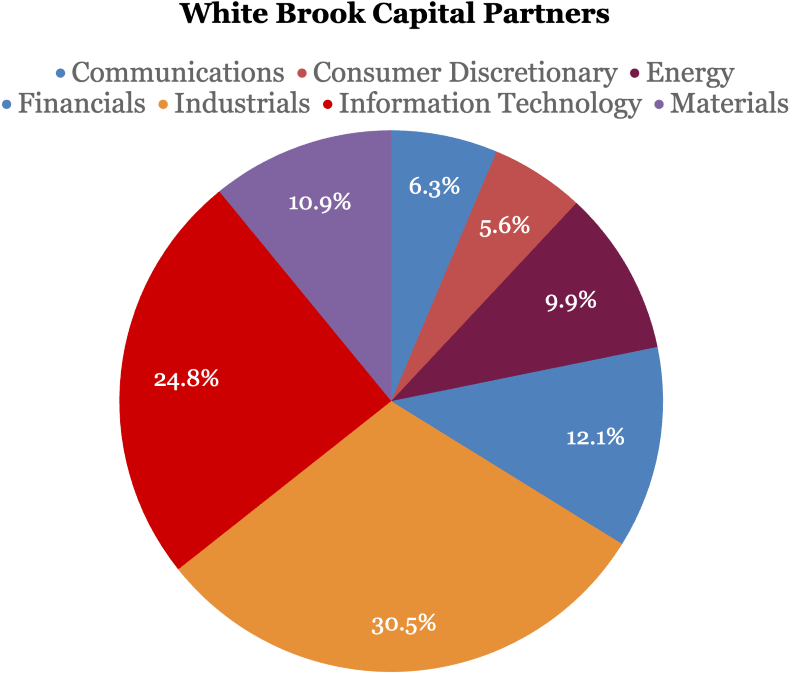

- The portfolio's top contributors were investments in industrials and financial services, while the top detractors were investments in materials and consumer discretionary.

- The fund entered a trading position in Unity Software Inc during the quarter, but did not exit any holdings.

- The portfolio remains diversified across industries.

Solid quarter

As of June 30th, 2023

| NAV increase, net

|

| CumIncept |

| AnnInception |

| PF 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2Q 2023 |

| YTD 2023 |

| WBCP |

| 84.23% |

| 16.88% |

| 17.60% |

| 19.05% |

| 37.16% |

| (15.38%) |

| 16.09% |

| 13.37% |

| S&P 400 |

| 41.86% |

| 9.77% |

| 5.72% |

| 13.66% |

| 24.76% |

| (13.06%) |

| 4.85% |

| 8.85% |

| S&P 500 |

| 59.55% |

| 13.27% |

| 9.36% |

| 18.40% |

| 28.72% |

| (18.10%) |

| 8.74% |

| 16.89% |

| The inception of White Brook Capital Partners was on August 16, 2019. Performance figures are provided by the administrator. Prior years are audited. 2023 is unaudited Performance is net of all realized and accrued fees. |

Performance Review

The second quarter was a good one for White Brook Capital Partners. The Fund’s NAV increased 16.09% vs the S&P 400 Midcap Index's 4.85% increase and the S&P 500 ( SP500 , SPX ) 8.74% increase. Year to date, the Fund’s NAV increased by 13.37%, net of all realized and accrued fees, vs the S&P 400 MidCap Index's 8.85% increase and S&P 500 Index’s 16.89% increase.

Year to date, on a sector basis, the portfolio’s top contributors were investments in industrials and financial services, while the top detractors were investments in materials and consumer discretionary.

There was a limited amount of trading during the quarter. We entered a trading position in Unity Software Inc ( U ) and did not exit any holdings.

{kind=link}

Builders First Source ( BLDR ) and B. Riley Financial ( RILY ) have been the most significant contributors year to date, while Mosaic Co ( MOS ) and Afya Ltd ( AFYA ) have been the most significant detractors. Notably, B. Riley was a top detractor during the first quarter and a contributor during the second.

The portfolio is still cheap, and risk/reward skews in our favor with the possibility of both an upward rerating of many of our portfolio companies’ cash flow streams and an upward revision in many of their forward cash flow estimates.

The portfolio continues to be diversified across industries.

Market Commentary

{kind=link}

The S&P 500 is neither under nor overvalued, with the 10-year treasury at 3.8% and the 30-year at 3.9% if company earnings continue to grow. That “if” is significant. The yield curve’s inversion, while currently less important to financial market psychology, continues to have real world implications. With short term rates high and long term rates lower, banks are more carefully weighing the risk/return of their businesses and pulling back on certain lines of business. As previously discussed, this is important any time consumers or businesses need to borrow money. As important, however, particularly moving forward, is how the yield curve normalizes, realizing that yield curve inversions are happening in many different geographies, today. Inversions, like flat yield curves that don’t pay lenders for time and the risk of non-payment over that time, are a reflection of a still broken world.

{kind=link}

The benefit of investing in an index is that the index may be able to go from one strength to another. Over the first half, many companies’ valuations benefitted from their perceived nearness to the development and use of artificial intelligence. The largest stocks in the country are all benefitting from the rise of AI, and therefore so are the [[QQQ]]s and, to a lesser but still strong degree, the S&P 500. Google’s ( GOOG , GOOGL ) stock, for instance, initially suffered when it appeared to be behind OpenAIs general artificial intelligence, but as it became clear it is facilitating the use and development of AI at every level it has products, its stock performance improved. The spread between the QQQ and every other index that benefits less from the inclusion of those companies in their index is wide. Economic growth is inherently an inefficient process, and the temporary spike in valuation for those that are actively providing value and those that only appear to be, is reasonable - until the future sorts itself out.

In other parts of the S&P 500, financials’ earnings should continue to be under pressure, consumers are finally beginning to trade down for consumer goods that have spent the past 3 years increasing price more than cost, and services demand, while still strong, is starting to wane. Slowing inflation implies companies are enjoying less pricing power than they did a year ago. At the same time, freight transportation measures indicate that stores are replenishing their shelves and distribution centers at below-normal velocity. Positively, unemployment is low, wage growth is strong, and consumer and corporate balance sheets are healthy. As I’ve written in these commentaries in the past, we are under-housed in the United States, as the number of residential units built has significantly lagged the number of households formed since the Financial Crisis. Home construction is a significant economic activity, and the strength in that sector makes a significant economic downturn unlikely. There are, unfortunately, few large sector-wide economic activities with similar tailwinds. As a whole, therefore, it’s unclear the path of earnings in 2023 and 2024, and as long as treasury bills are at this or a higher level, for the S&P500 as a whole to perform.

Notable Positions

B Riley Financial, Inc: B. Riley was a significant outperformer during the quarter as the problems with the short thesis began to emerge, and the company continued to execute. While over 95% of our long position was lent to shorts at a rate paid to us of ~14%, annually, during the first quarter, today, that amount is closer to 80% and the rate has dipped below 10%, indicating that shorts have begun to vacate their positions or at least feel less strongly about the short thesis given the elevated cost. The Company also engaged in several corporate actions in the regular course of its business and continues to build value.

Greenbrier Companies, Inc: Greenbrier posted a solid quarter with beats on revenue and margins and indicated continued strength in the business model in line with what we’ve noted in these commentaries in past quarters.

Mosaic Inc. (MOS): Mosaic has been a significant disappointment through the first 6 months. El Nino historically has distorted their markets, and that has been true this year as well. Additionally, a labor dispute at the port in Canada may depress earnings for the rest of the year. I still expect cash flow to be strong this year and their share buyback to be effective in creating value as free cash flow growth reemerges next year.

Unity Software Inc (U): We took a trading position in Unity Software during the quarter. A trading position is one where I expect the duration of the investment to be relatively short at the time of investment. During the first quarter, I completed much of the work and viewed Unity as attractive based on valuation, but decided to pass. Behind that decision were fundamental questions around corporate governance and the probability that Apple, at the unveiling of their headset, would either go alone in providing tools for developers to produce content for their new augmented and virtual reality efforts or also announce a wide settlement with Unity’s primary competitor, Epic Games, of all outstanding legal matters and a new partnership. Instead, Unity is being relied upon to help developers. Due to continuing concerns around their incentive plan and the strength of the board, it is unlikely that the position will prove to be a multiyear holding, but they are very likely beneficiaries of growth in artificial intelligence and virtual reality in the short term.

Unity theoretically benefits from several trends coming together at once.

- Augmented and virtual reality were unveiled too early, they’re not permanent busts. Artificial Intelligence advances should improve automation efforts that make it easier for developers to produce more intricate and complex environments and games in three-dimensional space. Improvements in chip development, notably Apple Silicon, but also by competitive chip manufacturers like NVidia and AMD, should also improve playback and interaction of three-dimensional worlds.

- Unity’s digital twin platform for producing digital versions of real objects is a competitive advantage. Their development platform is relatively easy to use and can be used across platforms as developers try to monetize, Apple, Meta, and any other competitive AR/VR platforms.

- Unity’s ad network is important, both as a cash flow stream today for the company, but also for developers as they need to play a role in the chicken and egg paradigm seeding a new platform with an initially limited audience.

- Epic Games’ lawsuit, the “bad blood” between the companies, and its partial ownership by Chinese giant Tencent, favors Unity in the US market.

I don’t expect White Brook Capital Partners to maintain a position over the long term, but we benefit from a good entry price and a positive backdrop.

MidCap Opportunity

{kind=link}

As an update to a longstanding and self-serving thesis that midcap stocks have underperformed and are set to outperform. The opportunity in middle capitalization stocks continues to be significant and I continue to be a proponent of increasing exposure.

Midcaps outperformed during 2022, but have underperformed by more so far in 2023 and continue to dramatically underperform large caps since 2016. The stocks are cheap, both relatively and absolutely.

As always, feel free to reach out to discuss this or any of your investments at White Brook Capital. I thank you for your support and will strive to continue to earn your trust.

Sincerely,

Basil F. Alsikafi,

Portfolio Manager, White Brook Capital, LLC

| All investments involve risk, including loss of principal. This document provides information not intended to meet objectives or suitability requirements of any specific individual. This information is provided for educational or discussion purposes only and should not be considered investment advice or a solicitation to buy or sell securities. The information contained herein has been drawn from sources which we believe to be reliable; however, its accuracy or completeness is not guaranteed. This report is not to be construed as an offer, solicitation or recommendation to buy or sell any of the securities herein named. We may or may not continue to hold any of the securities mentioned. White Brook Capital LLC and/or their respective officers, directors, partners or employees may from time to time acquire, hold or sell securities named in this report. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

White Brook Capital Partners Second Quarter 2023 Commentary