FREE - Whole Earth Brands: Story Remains Unchanged

2024-01-12 02:15:26 ET

Summary

- Whole Earth Brands' share price has remained stagnant in the past few months as there's no progress on the acquisition offer made in June 2023.

- In the meantime, revenue growth has slowed down, resulting in a lower guidance for 2023. This only marginally impacts valuation, though, indicating that the offer price can still be upped.

- Further, despite the underwhelming performance, the stock's attractive market multiples and positive outlook for 2024 bode well for it even if the deal falls through.

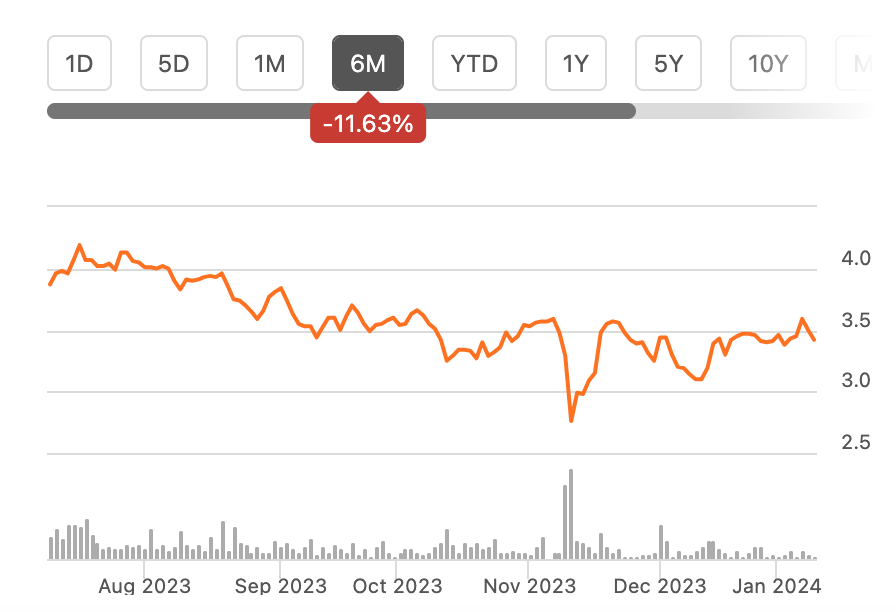

Since I last wrote about sweetener manufacturer Whole Earth Brands ( FREE ) in October last year, its share price hasn’t moved much, down by 3.5% since. I believe there's a good reason for this. Despite the acquisition offer in the middle of last year, there has been little progress on the front and the company's results released since don't change the stock story either.

{kind=link}

However, it doesn't mean that the acquisition is no longer on the cards. A little after the offer came through, the company said that the then CEO Michael Franklin would step down to avoid a conflict of interest, since the offer came from his father, Martin Franklin. The company went ahead with the decision with the two co-CEOs Rajnish Ohri and Jeffrey Robinson taking his place in October.

In the meantime, Whole Earth Brands has released another set of results for the third quarter of 2023 (Q3 2023) and the first nine months of the year (9m 2023). Here I take a look at how these latest numbers have changed the company's valuations in case the acquisition does go through. And also, whether FREE is a good investment or not in case it doesn't.

Weakening performance

Flat revenues

As I had flagged the last time, the revenue projections were at risk (see the section on ‘Revenue projections at risk’ in the first link). But they are even more so, going by the figures for 9m 2023 than I had expected.

Revenue growth slowed down to just 0.1% year-on-year (YoY) during this time compared to a 0.5% rise for the first half of the year (H1 2023), as revenues declined by 0.6% in Q3 2023. The decline came from a continued planned reduction in bulk sales for the company’s consumer packaged goods [CPG] segment to avoid incremental tariffs, which was one risk highlighted earlier.

Unsurprisingly, it has reduced its revenue guidance to a range, that would now result in growth of 0.3-2.2% from the earlier 2-5%. But even for growth to come in at the midpoint of 1.2% as per the now downgraded forecast sounds like a stretch. Here's why. Revenue would have to rise by 4.6% in Q4 2023 for this to happen, which doesn’t look likely going by the trend so far.

Unless the company reverses the decision on bulk sales, I reckon the more probable likelihood is revenue growth at the lower end of the range. For this to happen, Q4 2023 revenues would have to have risen by 1%, which is in the realm of possibility considering the higher 1.4% rise seen in Q1 2023.

{kind=link}

Adjusted EBITDA forecast marginally revised upward

It's not all bad though. Flat revenues have resulted in an improvement in the adjusted EBITDA (A-EBITDA) margin to 14% from 13.1% in H1 2023. The company has also slightly upgraded the A-EBITDA target to USD 78 million at the midpoint from the earlier USD 77 million. This also implies a margin improvement to 14.4% for the full year 2023 if revenue growth comes in at the lower end of the guidance range.

This is possible if there’s an accelerated contraction in operating expenses from the 2.2% seen during this period. But it’s quite possible it won’t happen as well. If the number increases at the average level seen during each quarter of the 9m 2023, it’s more likely to come closer to USD 75 million, resulting in a margin of 13.9%.

What the numbers mean for the acquisition price

The real question though, is, what the latest figures mean for the company’s valuations, which in turn determine the acquisition price. Here, the enterprise value [EV] is calculated based on both revenues and A-EBITDA. If the revenue for 2023 comes in at the lower end of the range at USD 540 million, the implied EV is USD 572.4 million at the company's current forward EV-to-sales (EV/S) at 1.06x.

However, this is lower than that for the consumer staples sector at 1.69x. If the offer price were to rise to the median level for the sector, the market capitalisation would have to rise by USD 340 million, making its target price USD 11.2 compared to the initial offer price of USD 4. This is lower than my earlier estimated valuation of USD 12.7 per share but it’s still way higher than the offer price.

Similarly, valuing the company in terms of the forward EV/EBITDA, if the A-EBITDA comes in at the company's target level of USD 78 million for 2023, the per share price offer price can rise to USD10.3, the same as the estimate yielded the last time.

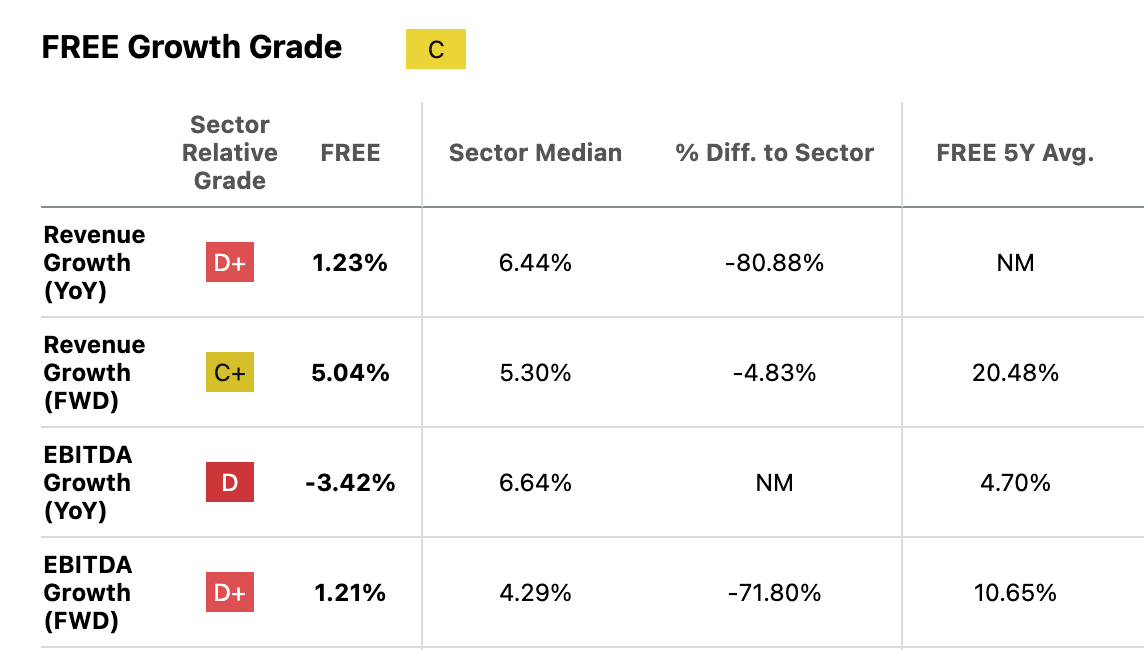

Comparison of Revenue and EBITDA Growth With The Median For Consumer Staples (Source: Seeking Alpha)

{kind=link}

However, there's a downward drag on the potential valuation too considering that neither its revenues nor its EBITDA are expected to grow at the rate of the consumer staples sector (see table above). However, its average 5-year growth rate and more optimistic analyst estimates for 2024 can still pull up the EV from its current valuation levels.

What the latest results say about the stock

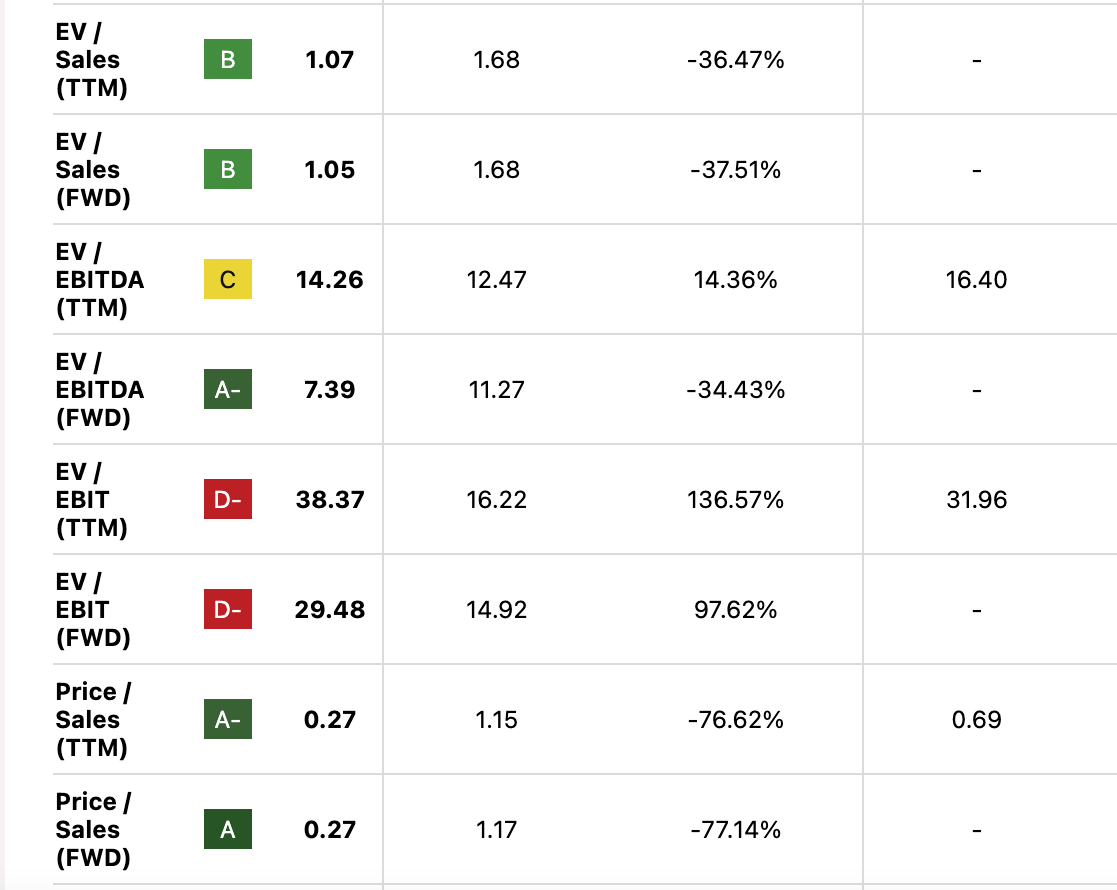

Despite the underwhelming performance, two factors are going in FREE's favour. One, its forward market multiples are largely attractive compared to the sector (see table below) and its trailing twelve months [TTM] multiples look good compared to its 5-year performance. The only exception is the EBIT multiples, which can improve too, if the company's operating expenses continue to shrink.

Two, the next year is expected to be positive for the company as per analysts' estimates linked above. Considering that a planned reduction in bulk sales has affected revenue growth this year. Improved performance can impact the stock positively too.

Market Multiples Note: Col 2: FREE Col 3: Consumer Staples Col 4: Difference from Consumer Staples Col 5: FREE, 5y avg (Source: Seeking Alpha)

{kind=link}

What next?

The key point emerging from the discussion is that the Whole Earth Brands story remains unchanged from the last I checked, with some differences in valuations. Its performance is still weakening, the market multiples are still largely competitive compared to the sector, and there’s still an upside to the offer price made for the acquisition in mid-2023.

Even if the acquisition doesn’t go through, 2024 looks like a better year for the company going by analysts’ estimates. Considering that its price hasn’t moved much since the last results further indicate that there’s little to lose by buying the stock right now. On the contrary, there’s still a definite upside to it if it gets acquired and if its performance improves in 2024. I’m retaining a Buy rating on FREE.

For further details see:

Whole Earth Brands: Story Remains Unchanged