SANM - Why Celestica Remains Among The Top Rated Stocks Heading Into 2024

2023-12-12 19:21:37 ET

Summary

- Celestica's stock initially dipped after its third quarter earnings report in October, but the "Strong Buy" quant score prevailed and shares rebounded.

- Stock rating among its peer comparisons reviewed.

- The company's strong Q3 results, including increased revenue and adjusted free cash flow, contribute to its positive stock grades.

Before Celestica ( CLS ) appeared as the third top-rated stock on the screener, the electronics manufacturing services firm already gained more than 140%. Markets priced in strong results in Celestica's stock ahead of its third quarter earnings report. Even after meeting expectations, the stock initially dipped.

Readers will not know whether the rising stock market or the normal course issuer bid of up to 11.76 million subordinate voting shares compelled the stock to rise again. What matters is that Celestica has a “Strong Buy” quant score.

Celestica A Top Rated Stock

According to Seeking Alpha’s Top Rated Stock screener, refreshed daily, Celestica is third. It scores a 4.98/5.00, matching Journey Medical ( DERM ) and Rolls-Royce Holdings ( OTCPK:RYCEY ). However, the latter two have stronger SA Analyst and Wall Street Ratings, pushing DERM and RYCEY’s ratings to first and second, respectively.

{kind=link}

Seeking Alpha Premium

The Seeking Alpha screener for top-rated stocks applied the filters: Quant Rating of buy to strong buy, SA Analyst Rating of buy to strong buy, and Wall Street Analysts Rating of buy to strong buy. The valuation, growth, profitability, momentum, and EPS revisions filters are from A+ to B-.

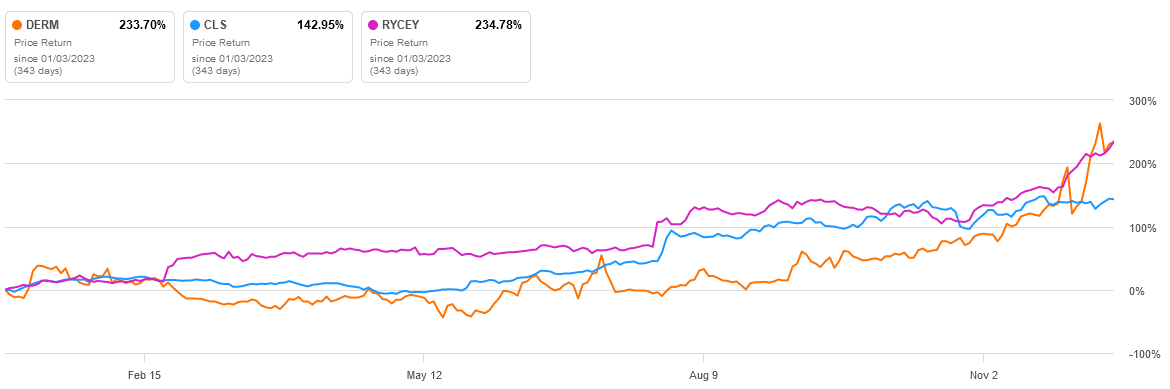

Year-to-date performance of these top-three stocks:

{kind=link}

Seeking Alpha

The stock grades reflect Celestica’s strong Q3 results. Revenue increased in two segments. Return on invested capital increased to 21.5%, up from 19.2% last year. Adjusted free cash flow rose to $34.1 million, up from $7.4 million.

Celestica raised its non-IFRS adjusted FCF expectation to $150 million, up from $125 million . In the quarter, the company did not buy back any shares. As guided on the call, the firm announced the NCIB program on Dec. 12, 2023.

Peer Quant Grade Comparison

Celestica's peers include Sanmina ( SANM ), Plexus ( PLXS ), Fabrinet ( FN ), and Universal Display ( OLED ). Celestica has a buy rating or higher, as does Fabrinet.

{kind=link}

Seeking Alpha

Celestica’s Notable Q3/2023 Highlights

Celestica posted Advanced Technology Solutions (“ATS”) revenue rising by 12% Y/Y. Management expects Q4 ATS revenue to grow in the low single-digit percentage range year-over-year. It will benefit from double-digit growth in its industrial and A&D businesses, offset by the ongoing market softness in capital equipment.

The communications end market will fall in the mid-teen percentage range year-over-year. The weakness is consistent with telecom stocks like Nokia ( NOK ), Cisco Systems ( CSCO ), and Ciena ( CIEN ) underperforming in the last quarter while the technology sector rose.

The Connectivity & Cloud Solutions (“CCS”) grew by 2%. Hyperscale is the fastest-growing aspect of the sector. However, Celestica is counting on OEMs that sell into the hyperscaler. Markets are not concerned that those businesses are working through excess inventory challenges. The industry has expectations that growth will return next year.

Balance Sheet Strength

Unless they're posting strong revenue growth, investors are wary of companies with high debt. Celestica ended the quarter with ample cash and gross debt to non-IFRS trailing 12-month adjusted EBITDA leveraged at 1.1 turns. This is down by 0.1 turns Q/Q and down 0.4 turns Y/Y.

{kind=link}

Celestica Q3/2023 Presentation

Celestica has a good chance of continuing its uptrend. Its net debt will fall as revenue rises sequentially from $2.04 billion in Q3 to up to $2.15 billion in Q4:

{kind=link}

Celestica Q3/2023 Presentation

The adjusted earnings per share of up to $0.71 is above the non-GAAP EPS of $0.65 posted in the third quarter.

Celestica benefits from the surge in demand for artificial intelligence applications. Revenue grew from programs ramping up. In addition, proprietary compute from hyperscaler customers supporting AI applications continued in the quarter.

Celestica’s enterprise end market has strong momentum. Executives expect revenues will increase in the high 20% range year-on-year. It has tailwinds from demand strength in proprietary compute programs from its hyperscaler customers.

The company’s inventory balance fell by $85 billion sequentially to $2.26 billion. Inventory days net of cash deposit days fell from 85 to 72 year-over-year . Management anticipates inventory days will improve over the coming quarters. It's benefiting from material lead times as they continue to normalize.

All of these metrics indicate strong customer demand and rising momentum.

AI Tailwinds

Hyperscales are growing at nearly 30% this year for Celestica. Demand is so strong that the company increased its material availability through the end of the year. It expects to clear the material in the early part of next year.

Top customers are drawing down Celestica’s inventory related to networking products. While demand for proprietary compute increases, the company will start ramping up its 800G programs in the second half of 2024.

Celestica scores a B on growth. If forward future cash flow grows, Celestica’s overall grade could move the stock to the first or second position of Seeking Alpha’s top rated stocks.

Seeking Alpha

Celestica expanded its capacity to meet AI-related server demand. It has 80,000 square feet in capacity coming online in Q1/2024 in Southeast Asia. It's working with its customers to expand capacity in Thailand, adding more than 50,000 square feet. When they're online, both capacity expansionary initiatives will support AI growth. Most importantly, Celestica and its customers have investment interests. This decreases any competitive threat or contract cancellation risks.

Still, Celestica’s customers rely on its expertise in complex, proprietary compute modules. For example, they require water cooling. When customers add new programs, they need Celestica to scale the solution reliably. Shareholders recognize that the revenue from existing customers is growing.

CLS stock does not trade at a premium. When other AI stocks are over-valued, CLS stock could trade even higher. The value score is A-. Only the PEG GAAP and price/book have a grade just below that.

Seeking Alpha

Your Takeaway

Thanks to strong stock grades, more readers will discover Celestica’s fundamental strength. The ATS and communications units posted healthy growth. The business strength continued in the third quarter and has the momentum to accelerate throughout the next 12 months.

AI is a tailwind. Unlike stocks that trade on the AI momentum, Celestica is solidifying hyperscaler revenue growth in partnership with its customers. This should lift the stock higher again and earn it a top pick rating for 2024.

For further details see:

Why Celestica Remains Among The Top Rated Stocks Heading Into 2024