AIC - Why Full Spectrum Income Investing Makes Sense Right Now

2023-08-07 15:48:20 ET

Summary

- We take a look at the allocation approach we call full-spectrum income investing which casts a wide net across many types of income securities.

- This is in contrast to many investors staying within predominantly one type of security, such as CEFs.

- Full-spectrum income investing gives investors an ability to better tailor their portfolios to the developing market environment and takes advantage of a wider opportunity set.

- We discuss these advantages and highlight a number of securities.

With so many different types of income securities out there, it's easy for investors to lean to only one or two types - those they know best. However, this can result in portfolios that carry higher than expected volatility and that lead to worse longer-term returns. In this article we revisit the concept of full-spectrum income investing , why it makes sense and how investors can go about building better income portfolios.

Elements Of Full-Spectrum Income Investing

The broader income investment space features securities of many different types. It's easier to think about this large number of different types when we break them down along a smaller number of dimensions relevant to portfolio construction and tie these characteristics into likely portfolio outcomes.

The key security characteristics to consider, in our view, are the following:

- Duration - the sensitivity of the security to changes in interest rates.

- Credit quality - the resilience of the security to macro shocks.

- Active vs. passive management - active management can but does not always deliver outperformance in credit; it also is more expensive.

- Investment wrapper e.g., senior security like a preferred or baby bond or open-end / closed-end in case of fund. CEFs tend to see higher volatility and larger drawdowns than their open-end counterparts due to the use of leverage as well as the discount dynamic. CEFs also tend to feature active management, have the ability to invest in less liquid assets and often boast higher yields and fees.

And the way these characteristics translate into portfolio outcomes is through:

- Yield/income level - how much cash flow the security generates, primarily linked to credit quality and duration.

- Drawdowns/volatility - the top-to-bottom drop and return variability of the security, linked primarily to its credit quality, duration, and investment wrapper.

- Resilience/total returns - whether the security is able to claw back its losses. Leveraged CEFs can struggle to do this if they are forced to deleverage during a drawdown.

The overall decision framework looks something like this. The process of selecting appropriate securities for the portfolio is complicated by the fact that each security has characteristics that can point in different directions with respect to overall portfolio goals (e.g., higher-quality securities tend to have smaller drawdowns, but also generate lower levels of income etc.).

Systematic Income

Sometimes the way these different security characteristics translate into investment results is not completely intuitive. For example, it makes sense that short-duration high-yield funds will have higher yields and lower resilience than longer-duration investment-grade funds.

But it is less intuitive that they could have smaller drawdowns as the interplay between duration and credit quality is not always straightforward. This allows investors to focus more precisely on their desired portfolio objectives without necessarily having to sacrifice income in the process.

The large number of investment options available in the market can also obscure the ultimate investment goals. This can make it easy to overlook some of the relevant security characteristics. For example, investors who want to hold part of their portfolio in relatively defensive assets will often focus on credit quality while overlooking the role of the investment wrapper or duration. This can cause them, for example, to pick investment-grade CEFs to fulfill this portfolio role even though CEF discounts will typically widen sharply during risk-off periods, irrespective of portfolio quality. And as we saw in 2022, rising rates can cause investment-grade bonds to underperform their sub investment-grade counterparts.

Why not just hold one security that captures all the relevant factors? The problem is this just isn't possible. No single security can be "best" at all the different roles. A security that is high-quality and low duration will have smaller drawdowns but will also feature a relatively low level of income.

A security that has a high income level will tend to have large drawdowns and lower resilience. It's a feature of the market that different securities are better or worse at providing access to a particular factor. This doesn't necessarily mean that investors should hold all different types of factors in equal measure, it just means they can achieve better investment results by a careful selection among the available securities based on the developing market environment.

Why Now

There are two key reasons why investors should consider full-spectrum investing now. One reason is that the market environment over the last 18 months has shown that it works.

Although there are many types of securities investors can consider, let's focus on three main types that we like and that are also quite different from each other to illustrate this point.

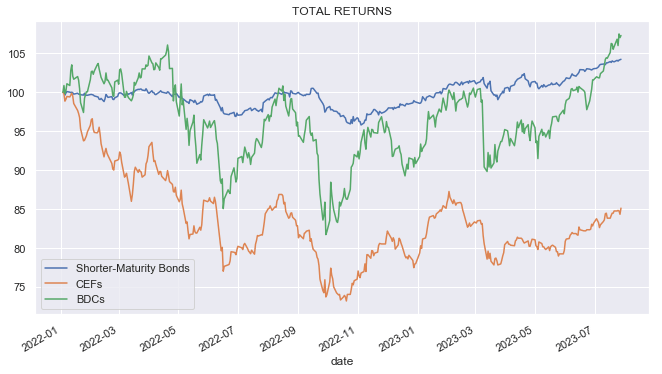

The chart below shows total returns of shorter-maturity bonds, CEFs and BDCs since the start of 2022. Shorter-maturity bonds are baby bonds with maturities of 1-5 years which have a relatively low-beta profile, in part due to their shorter maturity as well as their higher-quality profile relative to the common shares of CEFs and BDCs. The bonds return in the chart is proxied by a handful of bonds we have held in our Income Portfolios for some time while CEFs and BDCs are proxied by the ETFs Amplify High Income ETF ( YYY ) and VanEck BDC Income ETF ( BIZD ) respectively.

{kind=link}

What we see is that, as expected, shorter-maturity bonds have held up extremely well since 2022, with a total return drawdown of less than 5% and a total return of about +4% since then. BDCs have been quite volatile but have benefited from their floating-rate portfolio profile and have raced ahead. CEFs, however, have lagged quite a bit and remain at relatively depressed levels. Clearly, not all CEFs have performed this way but, by and large, CEFs have not performed particularly well since 2022.

There are several key drivers of these divergent results. Discounts to NAV which both CEFs and BDCs feature can significantly increase volatility and drawdowns. Duration exposure, which is the highest in the CEF space (and can be high in preferreds as well), can significantly hurt performance in a period of rising short-term rates and only modestly impacted shorter-maturity bonds. A jump in short-term rates has turbo-charged BDC net income and, largely, hurt CEF net income levels outside of loan and unleveraged credit CEFs.

The advantage of allocating across (at least) these three types of securities is that they provide investors with different risk profiles, allowing them to tailor their income portfolios to the developing market environment.

For example, in our own allocation, we downsized CEF exposure (falling orange bars below) and topped up BDC exposure (growing purple bars) in late 2021.

Systematic Income

The two key catalysts for shifting allocations are valuations and market turning points and this is the second reason why full spectrum investing is worth a look today. While CEFs have been hurt relative to BDCs and shorter-maturity bonds by their typically longer-duration profile, leverage, net income vulnerability to rising short-term rates and the discount dynamic, this is not something that we should extrapolate forever.

Specifically, if we see a deterioration in the broader environment causing credit spreads to push wider, discounts to widen, and weaker macro indicators, CEFs will start to become marginally more attractive in income portfolios. This will also be a time when the Fed will consider lowering rates which will benefit most CEF net income profiles.

Recently we have lightly trimmed our BDC allocation as valuations (both discounts and credit spreads) became a bit too frothy and reallocated the capital to bonds and unleveraged open-end funds which are likely to remain significantly more resilient if/when valuations reverse.

Full Spectrum Ideas

In this section we highlight a number of securities of different types that we continue to hold in our Income Portfolios.

The mortgage REIT Arlington Asset 2026 bond ( AAIN ) has a relatively short duration and trades at an 8.16% yield. The bond has been very resilient since 2022, generating a positive total return through the drawdown. The company will likely be merged into Ellington Financial.

Open-end funds can also be significantly more resilient without giving up on yield. We recently topped up our allocation of the Janus Henderson B-BBB CLO ETF ( JBBB ) which allocates to investment-grade tranches of CLOs. The fund's portfolio yield is north of 10%.

We continue to see pockets of value in CEFs such as the Western Asset Mortgage Opportunity Fund ( DMO ). DMO allocates primarily to non-agency residential mortgages which provide a nice diversifier in the income portfolio. The fund raised its distribution recently and trades at an 11.2% current yield.

In the preferreds space we like the Agency mortgage REIT AGNC Series G ( AGNCL ) which has a modest duration and is linked to the 5-year Treasury rate - an attractive feature given the highly inverted yield curve. AGNCL trades at an 8.77% stripped yield.

In the BDC space, we like the Blue Owl Capital Corp ( OBDC ) - an upper middle-market focused direct lender with a strong performance track record and a double-digit total NAV return over the past year. It trades at an 11% yield and a 7% discount.

For further details see:

Why Full Spectrum Income Investing Makes Sense Right Now