LEGR - Why We Believe We Are In The Early Innings Of A Tech Recovery

2023-06-21 13:30:00 ET

Summary

- What gives us confidence in a 2H23 tech recovery.

- 1Q23 earnings takeaways: hardware bottomed, software to follow.

- As we get into 2H23, comps get significantly easier.

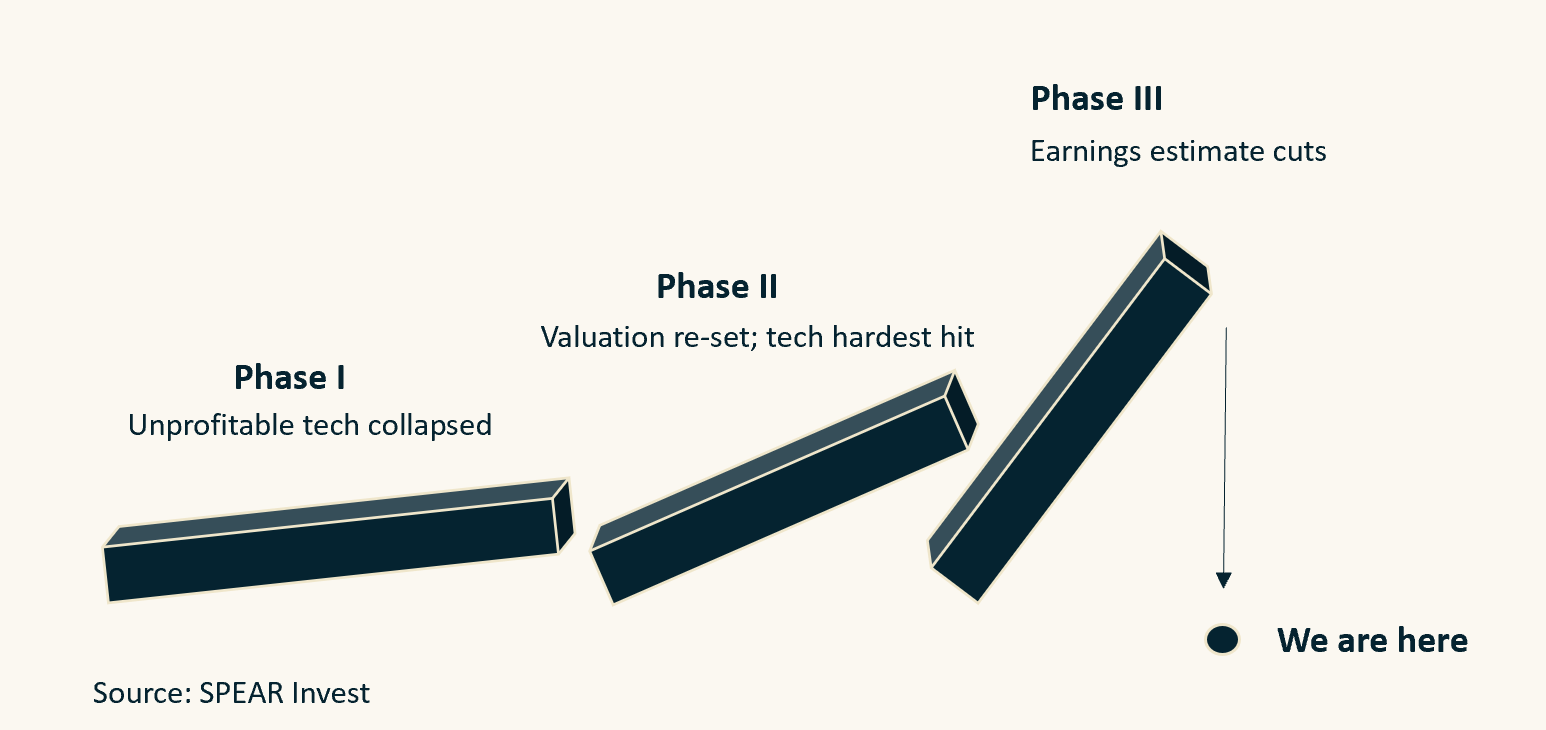

What gives us confidence in a 2H recovery

A downturn follows a typical pattern where valuations get hit first, followed by a broad-based economic weakness which impacts earnings of most sectors and companies. Earnings estimates usually take several quarters to reset, and we believe that 1H23 marked the bottom for earnings for the technology sector.

{kind=link}

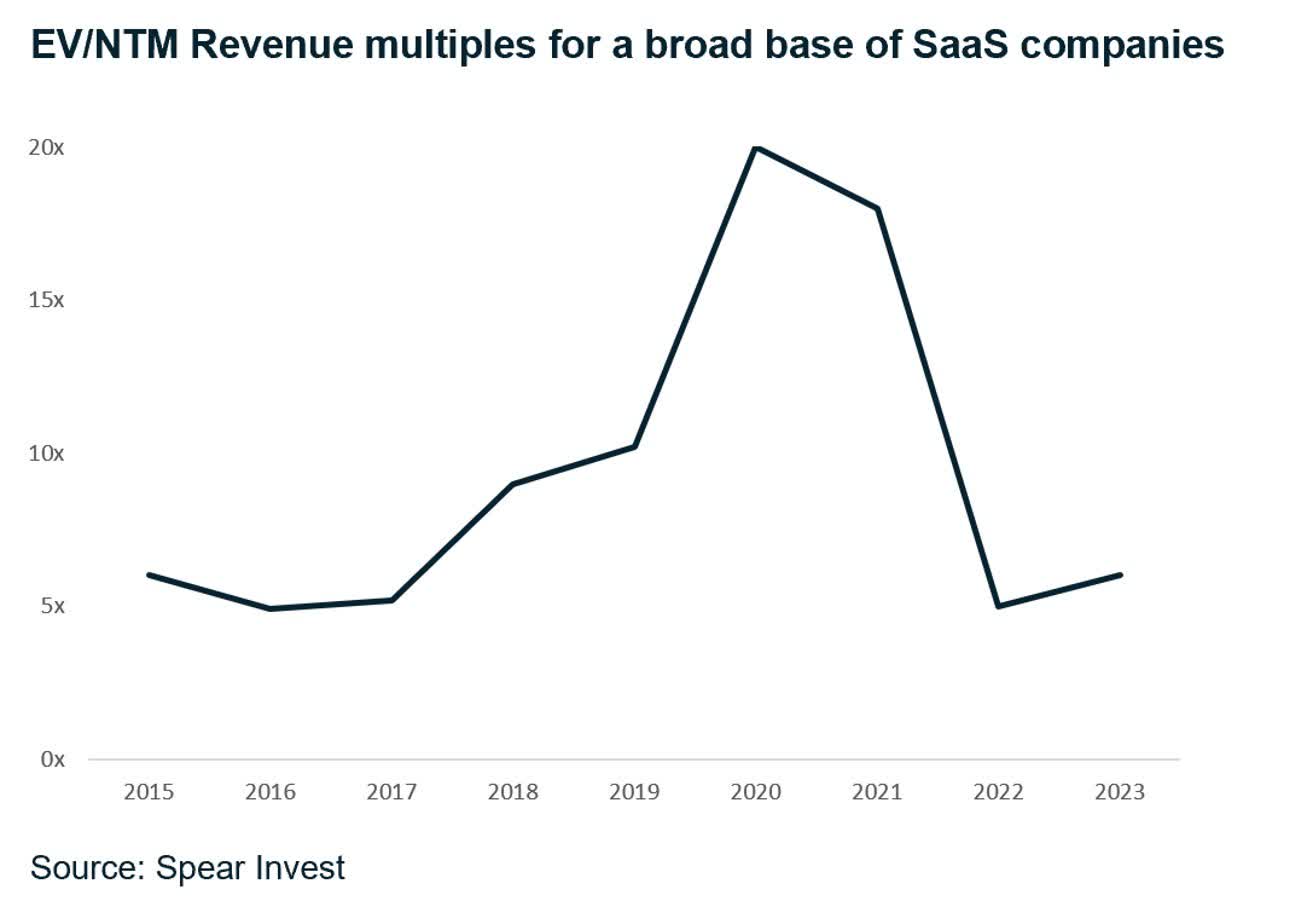

As interest rates stabilized this year (range-bound between 3.5-4% for 10Y), valuations bottomed. Despite the sharp move off the lows for many technology companies and the media noise of a "new bubble", the average software multiple is only up to ~6x EV/NTM Revenues vs. 5x at the bottom last year, and ~8x historical (10-year) average.

{kind=link}

This is in line with our expectations, as interest rates are higher than the historical average (4% vs. 2%) and NTM growth estimates are lower (15% NTM vs. 25% 10Y median). While we don't expect meaningful upside from interest rates in the near term, as we assume that rates will stay elevated for a longer period of time, we believe that earnings estimates are at an inflection.

Hardware earnings bottomed in 1Q23; software to follow

Semiconductors are considered to be the "canaries in the coal mine" due to the early-cycle nature of the business. As soon as there were signs of economic weakness in May 2022, distributors started reducing inventories, which exacerbated the impact from weak demand. Nvidia ( NVDA ) reported two quarters of dismal results and wrote off >$1bn of inventory (April/August '22). Consumer-levered semi companies such as AMD felt the impact early on, and data center-focused ones, such as Marvell ( MRVL ), slightly later.

As we get into 2H23, comps get significantly easier and companies are starting to be able to beat lowered expectations. In addition to the cyclical upturn, we expect significant boost to demand from investments in artificial intelligence ((AI)). This is not a one-quarter hype but a multi-year investment cycle. Per Nvidia, there is 1 trillion of data center hardware that is not accelerated and will need to be upgraded to accommodate AI workloads.

1Q23 Earnings Highlights

Most semiconductor stocks that reported pointed to confidence in a 2H23 recovery (AMD, Marvell, Broadcom ( AVGO )), and the strongest (fundamental) result this quarter was from Nvidia, which is uniquely positioned in AI with 80%+ market share in data center GPUs. Highlights from the reported earnings below:

- Nvidia guided to 2Q24 (August 23) revenues that were 50% above consensus. Analysts raised their forward estimates by 40% in the current and out-years. The company pointed to substantial increase in capacity in 2H23.

- Marvell reported an in-line result but guided for AI-driven revenues to double in 2024 and 2025 ; $200M in AI sales for FY23; $400M+ for FY24; $800M+ for FY25 (on a run rate of ~$5bn).

Interestingly, despite posting (by far) the strongest result, Nvidia was not the best performer in our coverage universe for the month of May (not even in top 5). This was because "the idea of semiconductor bottoming" set a floor for the rest of technology, and consequently, investors rushed into the areas of tech that could drive the next leg up.

But if we step back, Nvidia was the only company that raised estimates commensurate with the stock price movement (+50%), which we believe provides a solid fundamental support and therefore remains a top idea in industrial technology with significant earnings runway ahead (see our report " Nvidia: The One-Stop AI Shop ").

Software (enterprise + cloud + cybersecurity)

Software earnings generally lag semis by 6 months. There are different areas of software that bottom at different times depending on the end-market and business model (consumption- vs. subscription-based).

Revenue estimates for our software universe continued to decline, with the median NTM growth estimate now at only 15% vs. the 10-year average of ~25%. Hyper-growth companies are now growing at only ~30% vs. 70%+ previously. Companies are still citing elongated sales cycles, smaller and staggered deals, execution challenges, etc. Reported earnings were far from stellar, with many companies reporting negative net-new ARR.

But the interesting development was that relatively small surprises got aggressively bought, and big misses were able to retrace losses. This is usually a sign of a bottom, as investors are willing to look out past this quarter if they can get confidence that we are at a bottom.

Strong results:

- Zscaler ( ZS ) - Reported 40% billings growth in a tough macro, after a difficult last quarter.

- GitLab ( GTLB ) - Guided to revenue growth of +27-28% above consensus of +25%, following a 15%+ guide down last quarter.

- MongoDB ( MDB ) - Beat/raised post a very conservative guide (+19% from +17%).

Weak results from Cloudflare ( NET ), Snowflake ( SNOW ), and SentinelOne ( S ) citing a tougher macro than originally expected were brushed off. Cloudflare and Snowflake were able to retrace loses. SentinelOne remains TBD but bounced significantly off the lows.

As we look into 2H23, comps get significantly easier as we are coming to the anniversary of 3Q/4Q22, when we started experiencing fundamental weakness. In addition, companies have been postponing spending in anticipation of a recession for several quarters, creating potential pent-up demand.

But what about the recession?

Most of the companies we cover went through significant earnings cuts in anticipation of a recession. We therefore don't expect that small changes in economic growth (+/-1%) will drive a meaningful difference for earnings results for technology companies.

However, the severity and duration of the recession (if it ever comes) could affect the slope of the recovery. We therefore look to invest in well-capitalized businesses with strong fundamentals.

Original Source: Author

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Why We Believe We Are In The Early Innings Of A Tech Recovery