MAA - Winners Of REIT Earnings Season

2023-08-10 15:23:24 ET

Summary

- Nearly 200 U.S. REITs have reported second quarter earnings results over the past month, providing critical information on the state of the commercial and residential real estate industry.

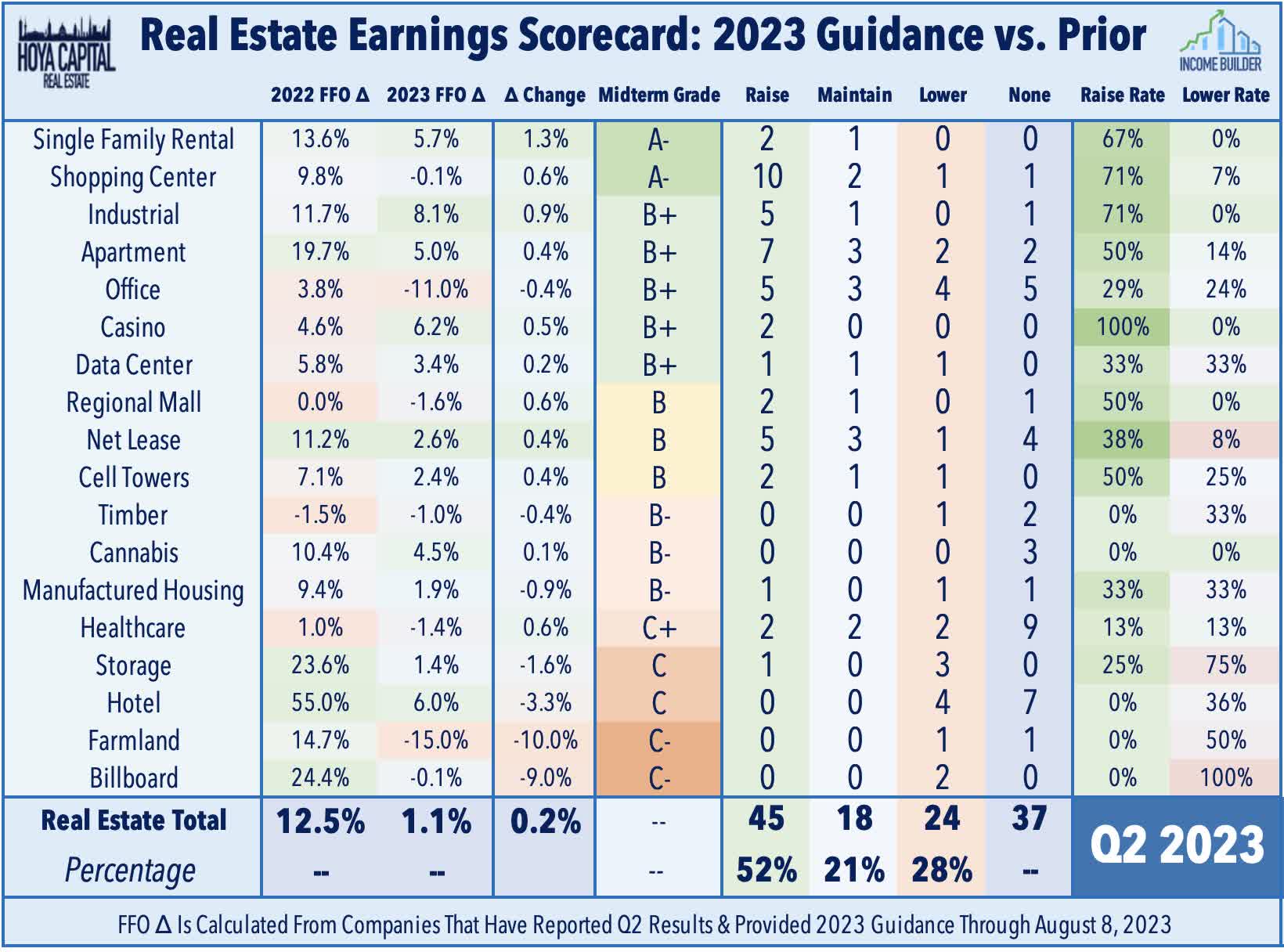

- Of the 86 equity REITs that provide full-year Funds from Operations ("FFO") guidance, 52% raised their full-year earnings outlook while 28% lowered guidance, a "beat rate" that was below Q1.

- Buoyant residential rent growth- particularly in the supply-constrained single-family space - was one of the prevailing themes of the quarter, fueling a particularly strong set of reports from residential REITs.

- Retail REITs have enjoyed an under-discussed revival over the past 18-24 months as store openings have considerably outpaced store closings over the past two years, driving occupancy rates to record highs and fueling impressive double-digit rent growth.

- Office REITs have posted the strongest stock performance this earnings season as results have been "less bad" than feared, and there are signs that the "return to the office" has picked up steam. In Part 1 of our Earnings Recap, we discuss the Winners of REIT Earnings Season.

Real Estate Earnings Recap

Nearly 200 U.S. REITs have reported second quarter earnings results over the past month, providing critical information on the state of the commercial and residential real estate industry. As discussed in our Halftime Report, REIT earnings season was off to a strong start, led by the residential, strip center, and industrial sectors - while even the beaten-down office sector delivered surprisingly solid results - but results in the back-half of earnings season were considerably less impressive, with many of the most pro-cyclical property sectors reporting a surprising degree of demand softness later in the quarter. Of the 86 equity REITs that provide full-year Funds from Operations ("FFO") guidance, 52% raised their full-year earnings outlook (down from 63% in Q1), while 28% lowered guidance (up from 18% in Q1). By comparison, FactSet reports that 60% of S&P 500 companies increased their full-year EPS guidance, while 40% of companies lowered their full-year outlook.

{kind=link}

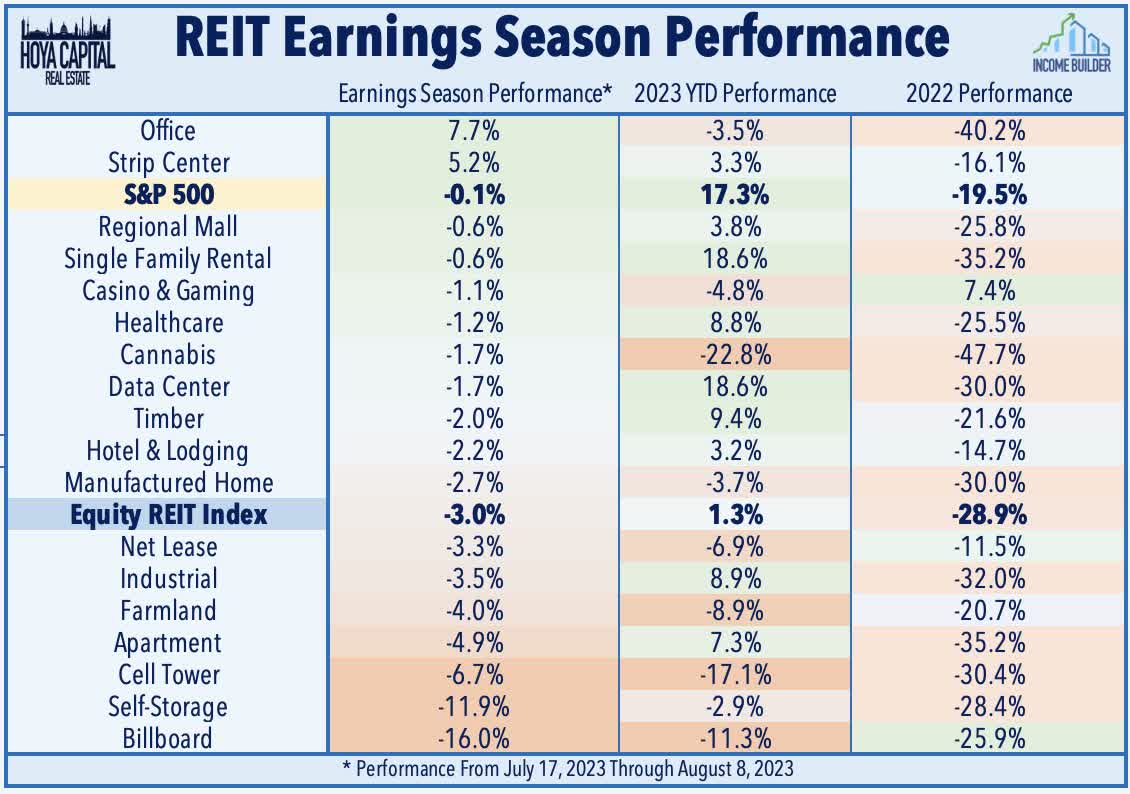

Pressured by the recent jump in benchmark interest rates, which sent the 10-Year Treasury Yield to the cusp of 15-year highs, the Equity REIT Index has lagged the S&P 500 since the start of earnings season, and these renewed macro headwinds obscured some of the positive trends on display across the majority of the REIT sector. Buoyant residential rent growth - particularly in the supply-constrained single-family space - was one of the prevailing themes of the quarter, fueling a particularly strong set of reports from the two largest SFR REITs, and mostly solid results across the multifamily and senior housing sectors. Retail REITs - particularly within the open-air strip center format - also have enjoyed an under-discussed revival over the past 18-24 months as store openings have considerably outpaced store closings over the past two years, driving occupancy rates to record highs and fueling impressive double-digit rent growth. Office REITs have posted the strongest stock performance this earnings season as results have been "less bad" than feared, and there are signs that the "return to the office" may be picking up steam.

{kind=link}

Among other notable positive themes this quarter, expense pressures abated a bit for some sub-sectors - notably in the labor-intensive senior housing, cold storage, and hospitality sectors - while tenant rent collection improved marginally for most healthcare and cannabis REITs, but lingered for debt-burdened tenants. As with the prior quarter, earnings "misses" and downward earnings revisions were driven predominately by elevated debt servicing expenses, underscoring the continued challenges facing more-highly-levered real estate portfolios from the higher rate environment. A bit more concerning were the handful of downward revisions driven by pockets of demand softness, notably from the hotel and billboard sectors, while results from storage REITs also showed a late-quarter slump in activity in most markets. While the Sunbelt vs. Coastal bifurcation hasn't completely dissipated, market-level performance is becoming more localized. New York City was a notable upside standout, while we observed clear West Coast weakness across most sectors.

{kind=link}

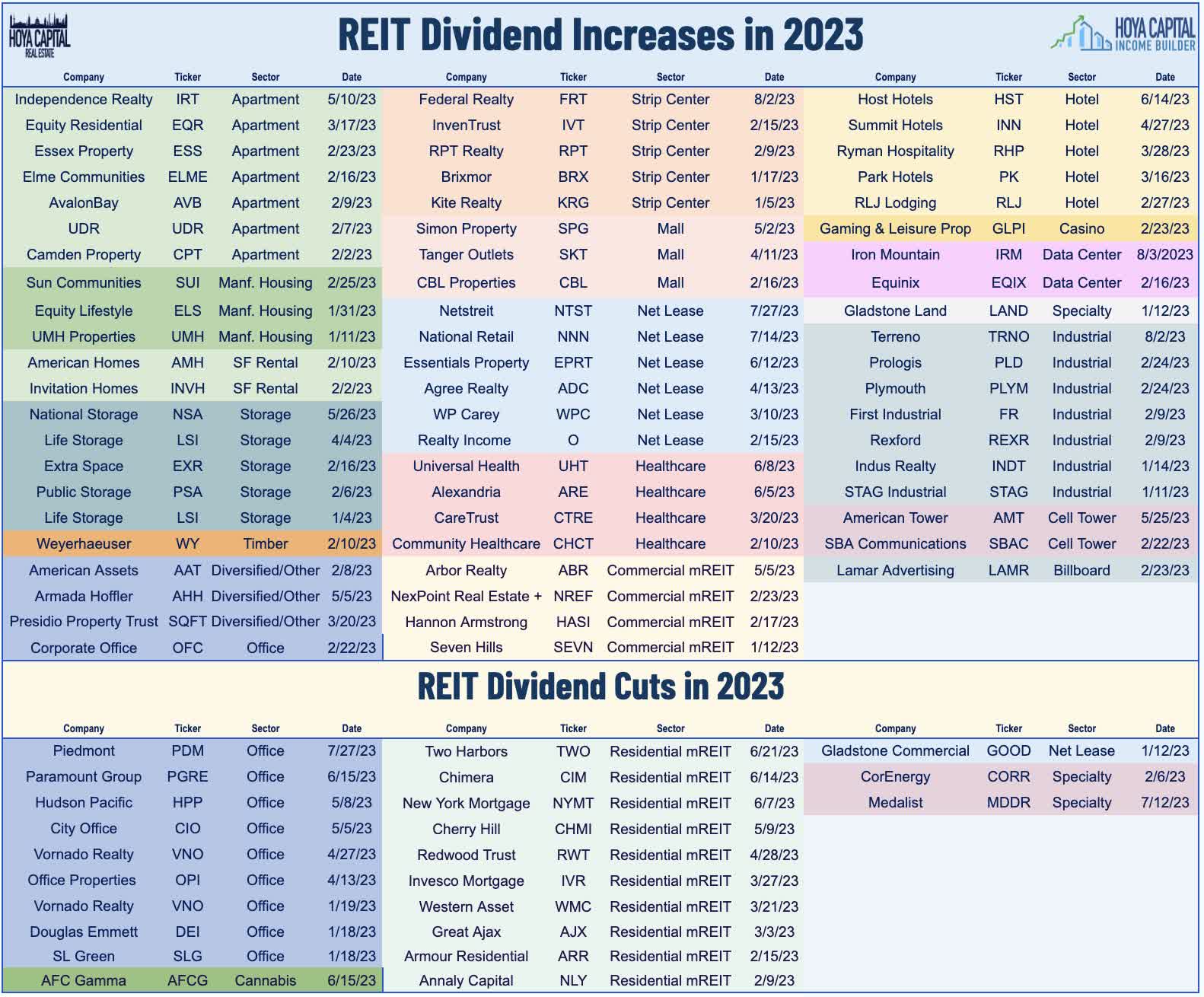

Dividend sustainability is always a focus during earnings season, and we've been scouring through earnings calls to glean insights into the outlook for dividend hikes - and in some cases, dividend cuts - this year. Six REITs hiked their dividends during earnings season, bringing the full-year total to 63: Mall REIT Simon Property raised its quarterly dividend by 3%, industrial REIT Terreno Realty raised its quarterly dividend by 12%, business storage REIT Iron Mountain raised its quarterly dividend by 5%, strip center REIT Federal Realty raised its quarterly dividend by 1%, and a pair of net lease REITs - National Retail and Netstreit - each raised their quarterly dividends by 3%. We've only seen one REIT reduce its dividend this earnings season - office REIT Piedmont - which slashed its dividend by 41%, becoming one of 23 REITs to reduce their dividend this year. A handful of other REITs - primarily in the mREIT space - also hinted at a dividend reduction in the near future.

{kind=link}

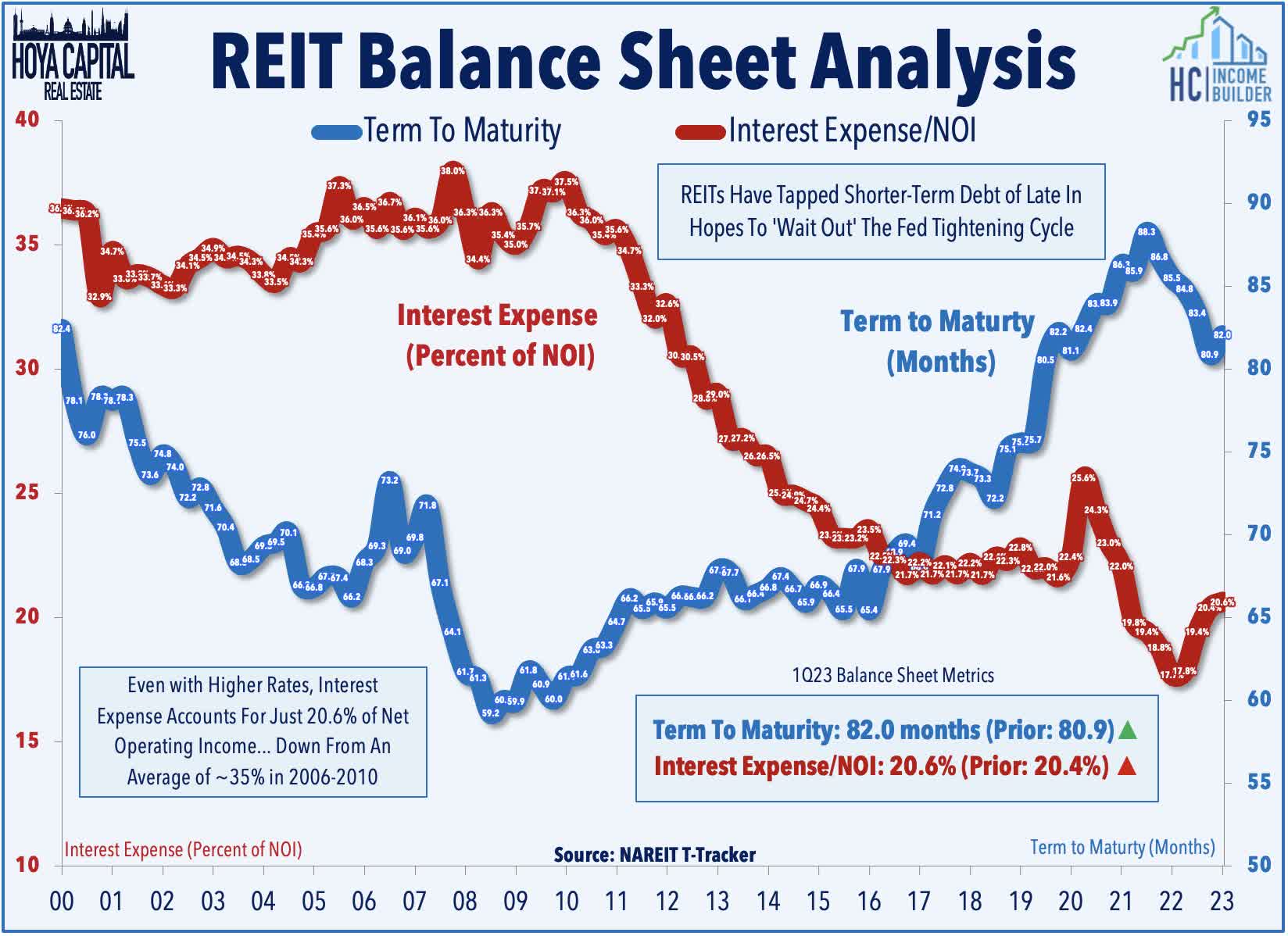

REIT balance sheets - and particularly variable rate debt exposure - remained in focus this earnings season and, relatedly, the degree of capitulation from highly-levered private market owners that had hoped to "wait out" the higher interest rate regime. As we've covered extensively in our State of the REIT Nation reports, most public REITs have been preparing for this exact kind of dislocated macro environment, perhaps to the frustration of some investors that turned to higher-leveraged and riskier alternatives in recent years across private markets - including the non-traded REIT platforms from Blackstone , KKR & Co and others that have been forced to sell some of their best-performing assets to public REITs in recent quarters to fulfill investor redemption requests. Bid-ask spreads in private markets remain wide, so transaction activity remains depressed, but there was a prevailing consensus in earnings call commentary that public REITs with some balance sheet firepower will have plentiful opportunities to flex their muscles in the near future as the "cheap" 3-5 year debt comes due for maturity.

{kind=link}

With real estate earnings season now essentially complete - sans a handful of stragglers that report results over the coming weeks - we compiled the critical metrics across each real estate property sector. In Part 1 of our two-part REIT Earnings Recap, we focus on the "Winners of REIT Earnings Season."

Winners of REIT Earnings Season

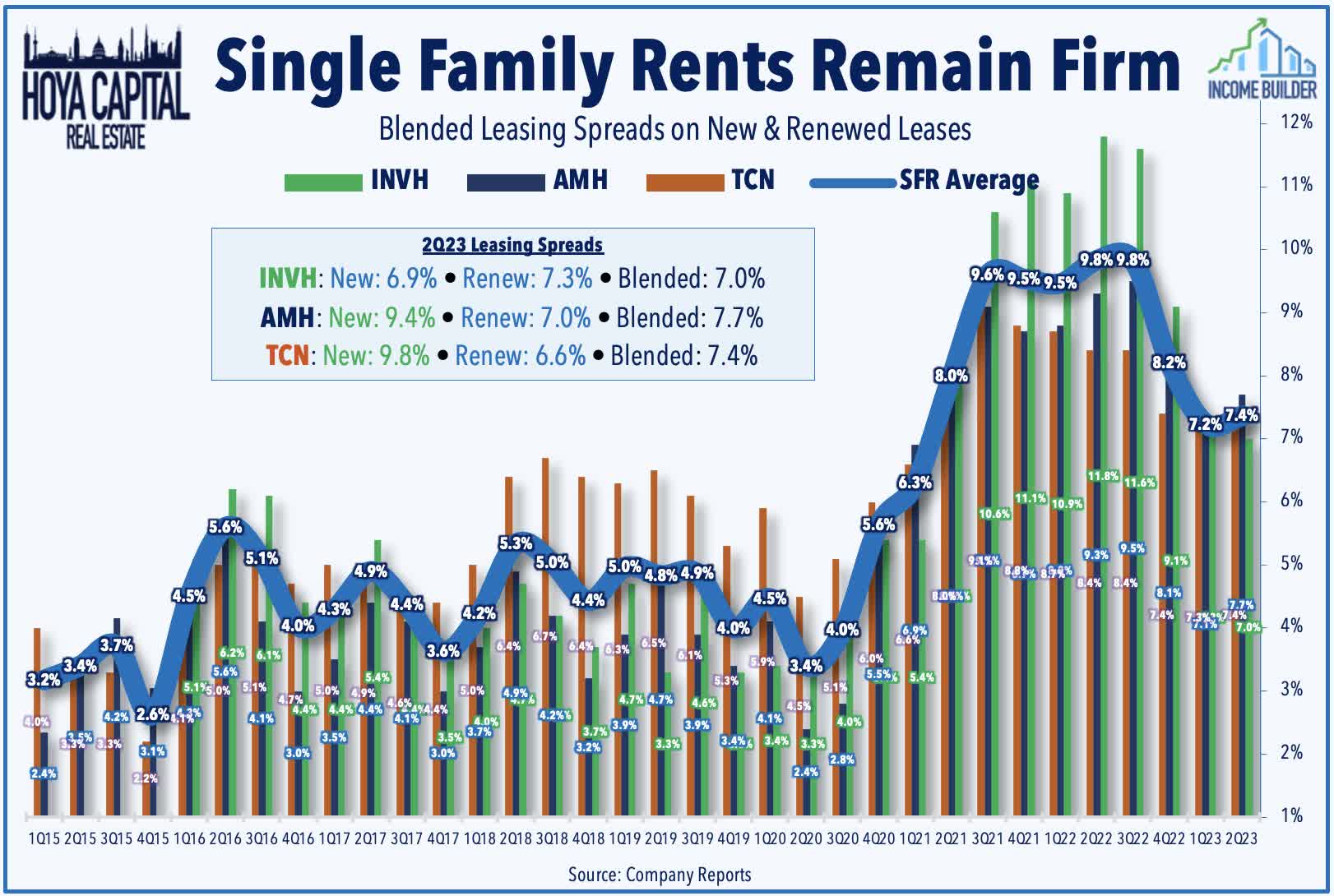

Single-Family Rental : (Final Grade: A-) Buoyant rent growth was the prevailing theme for residential REITs this earnings season, particularly these SFR REITs, which aren't facing the same supply headwinds as multifamily REITs. The two largest SFR REITs - American Homes and Invitation Homes - reported impressive "beat and raise" results, while small-cap Tricon reported decent results while maintaining its full-year FFO outlook. AMH recorded blended leasing spreads of 7.7% in Q2 - an acceleration from the 7.1% rate in Q1 - which drove a boost to its full-year FFO growth outlook to 6.5% - up 200 basis points from the prior quarter. INVH recorded blended leasing spreads of 7.0% in Q2 - which was down slightly from the 7.3% blended increase in Q1 - and drove a boost to its full-year FFO growth outlook to 5.0% - up 70 basis points from last quarter. TCN recorded blended spreads of 7.4% while maintaining its occupancy rate near record highs at 97.5%. While TCN scaled back some of its external growth plans, given its elevated leverage levels, the two larger REITs showed some renewed appetite for growth. AMH announced a $625M second strategic joint venture with JPMorgan Asset Management to construct "built to rent" homes, while AMH announced that it acquired 1,900 homes for $650 million from Starwood Capital's non-traded REIT platform.

{kind=link}

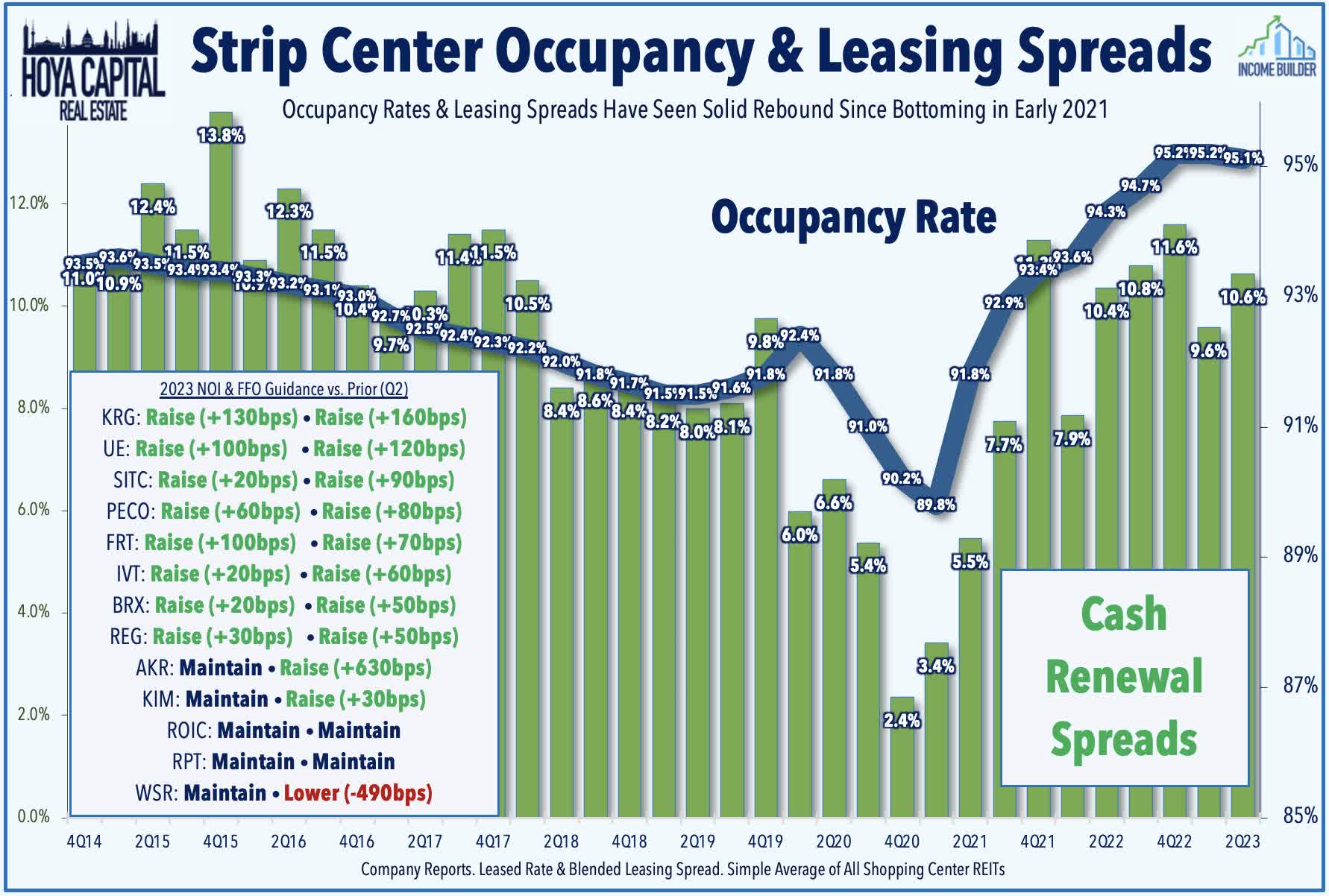

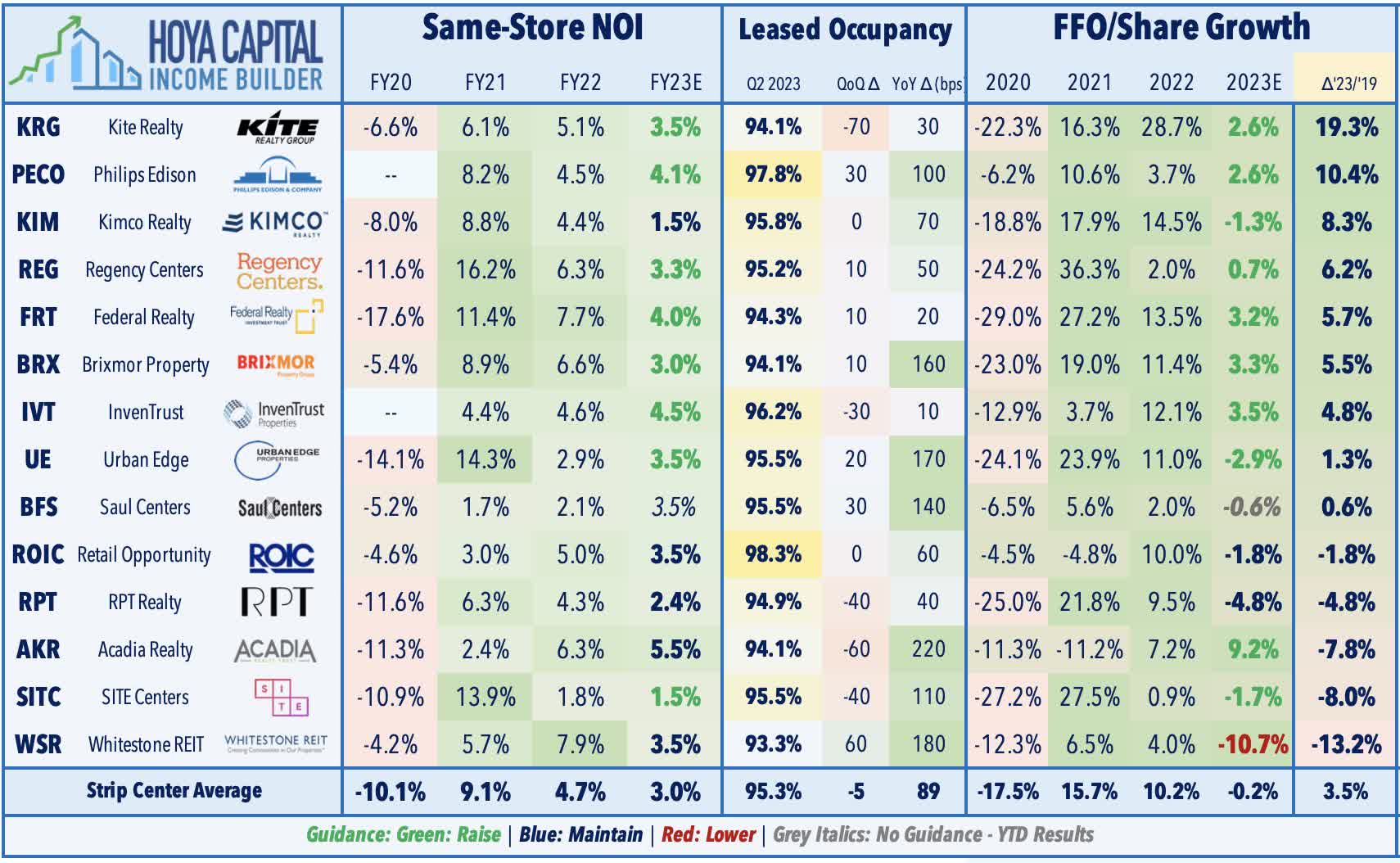

Strip Center : (Final Grade: A-) Strip center REITs were a notable upside standout with a near-perfect slate of upward guidance boosts as record-high occupancy rates resulting from a decade of limited new development fueled another quarter of double-digit rental rate spreads. Continuing a trend of better-than-expected results stretching back to late 2021, 10 strip center REITs raised their full-year FFO outlook while just one lowered their FFO target as demand for "big box" space has significantly exceeded the available supply despite the recent high-profile bankruptcies of Bed Bath & Beyond and Party City. Kite Realty was the upside standout, reporting cash leasing spreads of 14.8%, which drove a 130 basis point upward revision to its same-store NOI outlook and a 160 basis point boost to its FFO outlook, while results from Philips Edison was also among the more impressive with blended leasing spreads of 18.9%. Acadia Realty posted the strongest FFO guidance boost driven by "outperformance in leasing and better than anticipated collections," along with a one-time gain related to the early termination of its Bed Bath leases.

{kind=link}

REITs with exposure to Bed Bath and Party City expressed a high degree of confidence in their ability to release the space. Site Centers noted that roughly 60% of the vacated space has already been re-leased and that SITC is on target to achieve a "20% to 25% increase" to the existing in-place Bed Bath rents, an expectation that was echoed by several other REITs. The lone downward FFO revision came from Whitestone , which resulted from legal expenses related to the termination of its former CEO in early 2022. Overall, strip center REITs now expect their FFO to be only fractionally lower in 2023, on average, which would be 4% above the pre-pandemic 2019 level.

{kind=link}

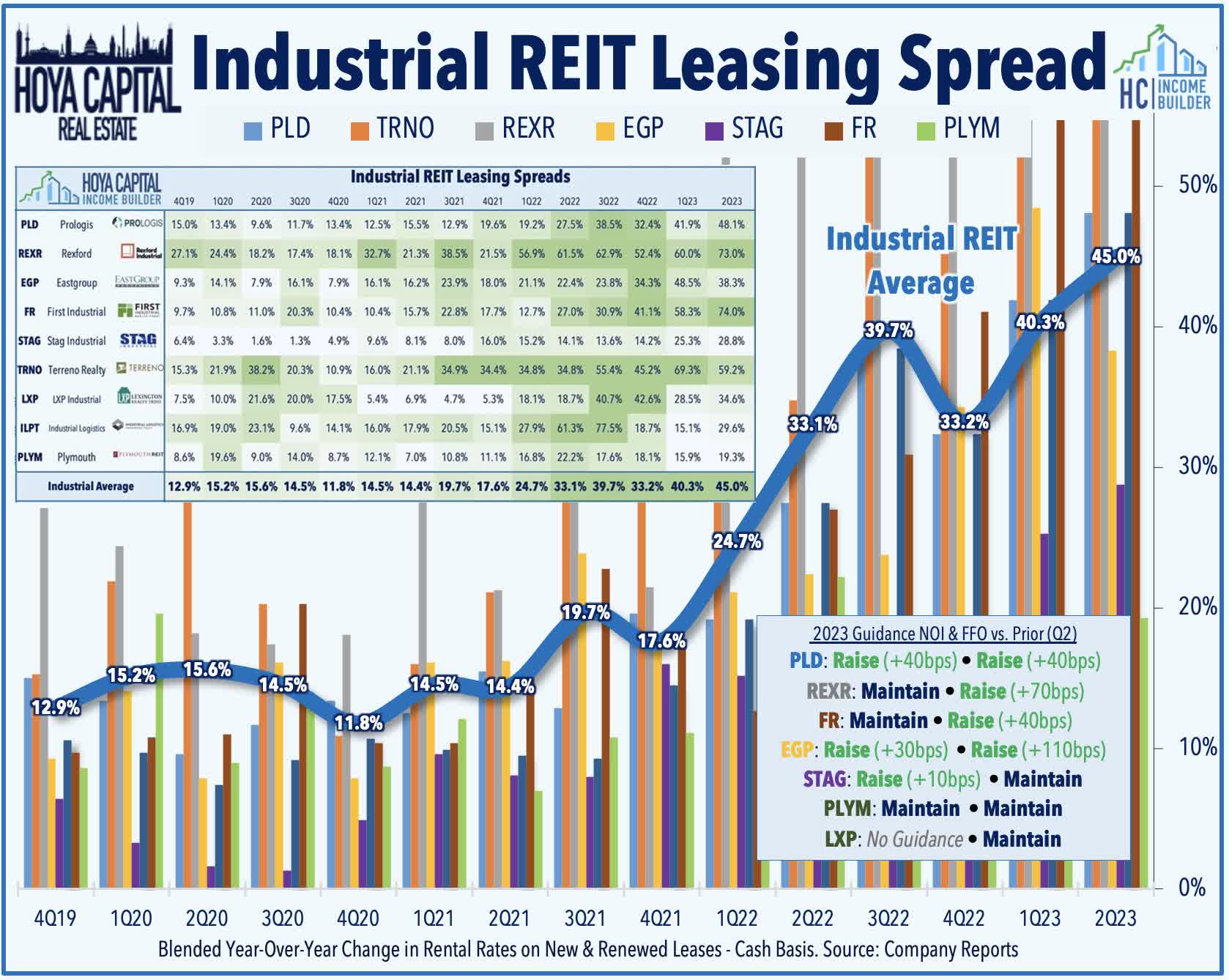

Industrial : (Final Grade: B+) Overshadowed by the bankruptcy of shipping giant Yellow - and the potential impact on the logistics industry - industrial REITs reported another very strong slate of earnings reports. After a rent growth moderating in late 2022 - which many expected to continue throughout this year - rent spreads have actually reaccelerated in early 2023, perhaps credited to a moderation in cost pressures for tenants in other areas of the supply chain, specifically freight costs, which are as now much as 90% lower than their peak in September 2021. Five of the seven REITs that provide full-year guidance raised their FFO outlook, led on the upside by EastGroup , which raised its FFO growth target by 110 basis points to 9.0% driven by rent increases of 52.8% on new and renewed leases. Echoing commentary from other industrial REITs, EGP did comment that it has seen "normalizing" demand in recent months and cautioned of a near-term supply overhang. Prologis' earnings call commentary also indicated expectations of near-term softness in the back half of 2023 before re-tightening in 2024 with new development starts in Q2 down 40% in the U.S. and 50% in Europe.

{kind=link}

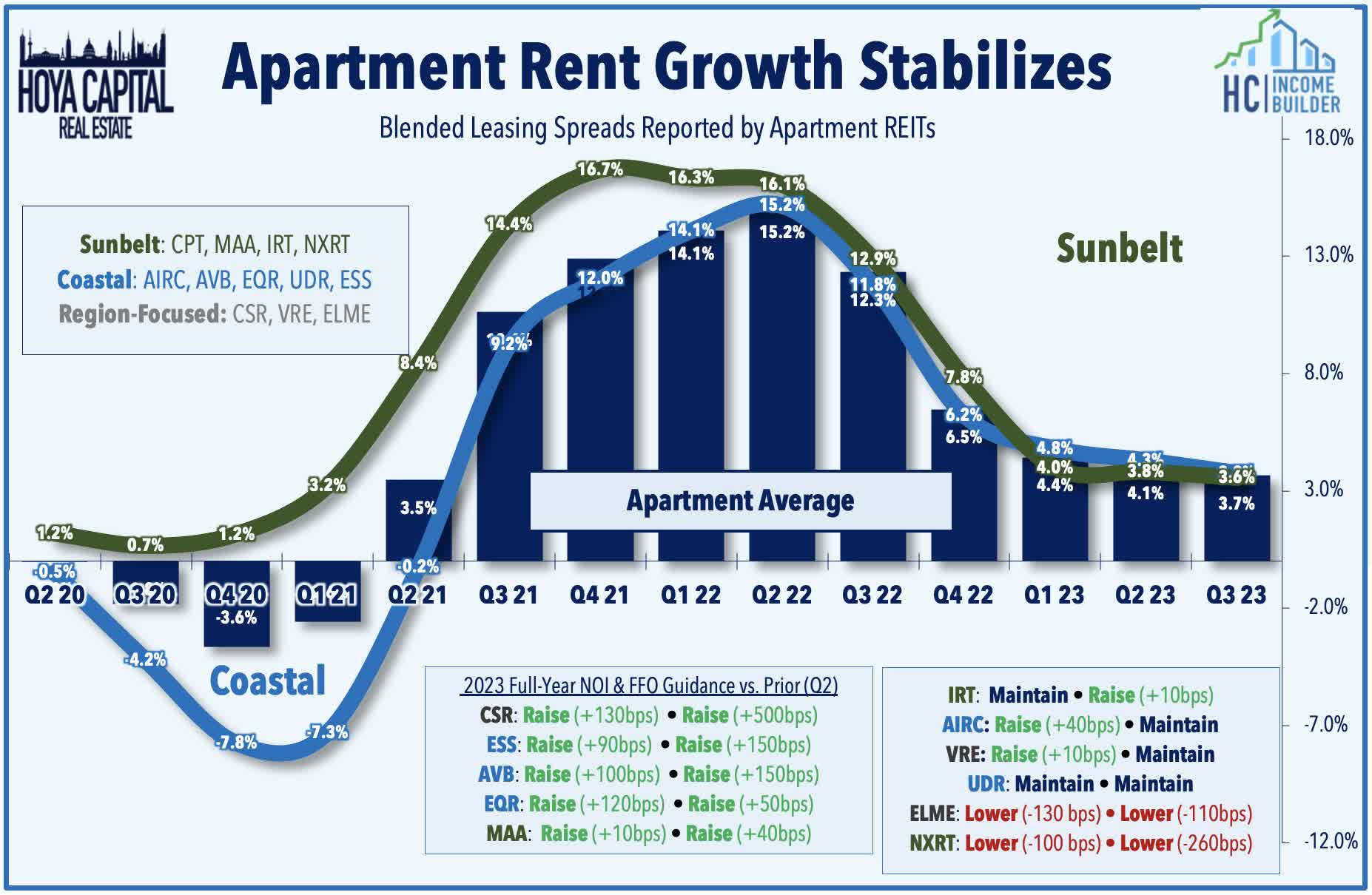

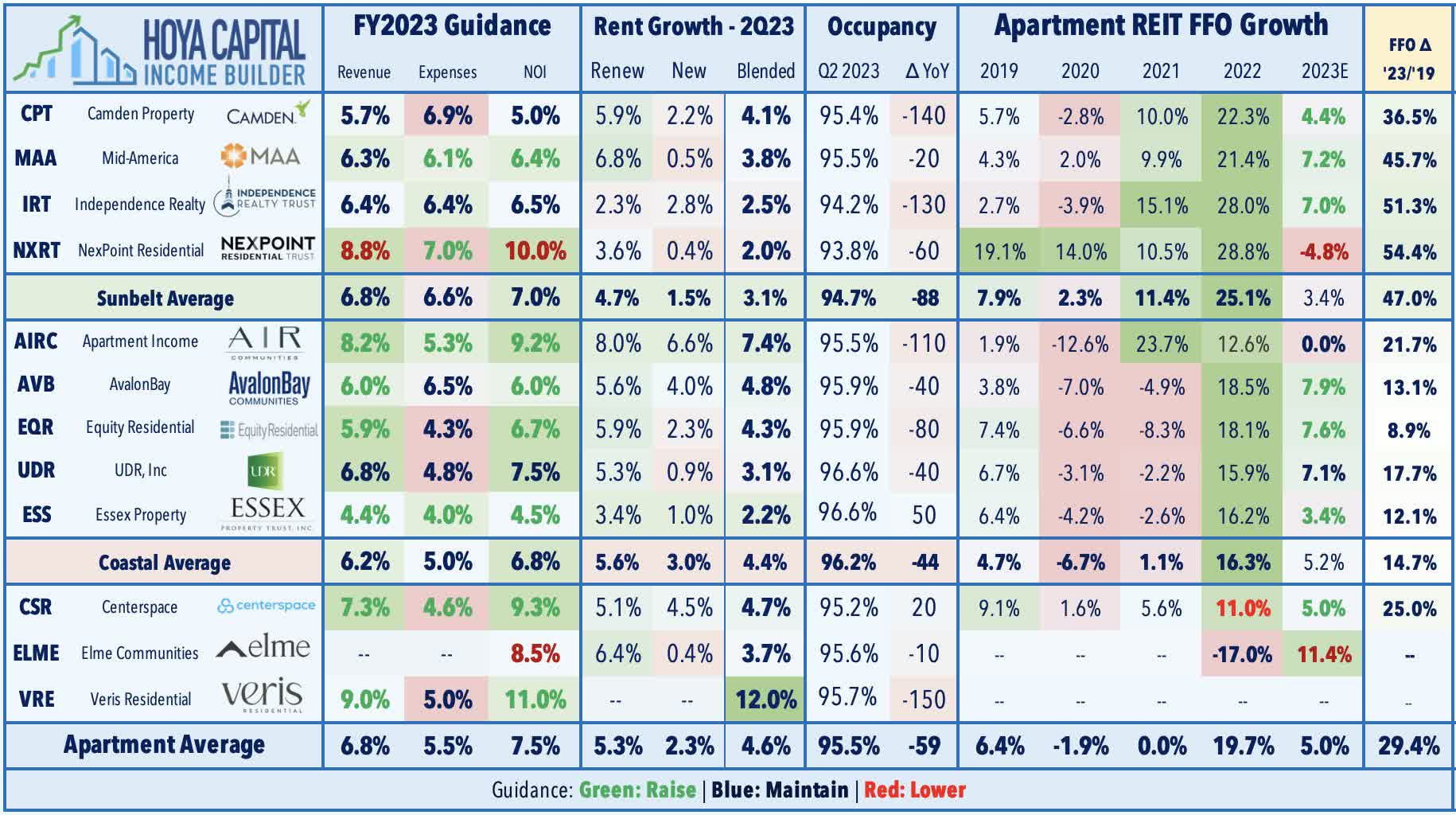

Apartment : (Final Grade: B+) Rent growth has indeed moderated from the historic pace seen from mid-2021 through mid-2022, but contrary to the bearish consensus late last year calling for a rent "correction" with negative growth, we've instead seen stabilization in the typical "inflation-plus" range between 4-5%. Of the REITs that provide full-year FFO guidance, six of the 11 REITs raised their full-year FFO outlook while eight of the eleven raised their same-store NOI outlook, upward revisions helped by moderating expense pressures. Impacts from a historically large multifamily development pipeline are beginning to become more visible as all but two REITs reported a year-over-year occupancy decline, but there was an overwhelming consensus on earnings calls that supply pressures will abate into 2024 given the extremely challenging financing environment for new ground-up development. Results from coastal-focused REITs were marginally stronger than their Sunbelt-focused peers, with particular strength on display in the NYC market.

{kind=link}

NYC-focused Veris Residential has been a top-performer this earnings season after raising its full-year outlook and announcing that it completed a $520M buyout from its joint-venture partner Rockpoint - a major step toward simplifying its business structure as a pure-play multifamily REIT. The biggest upside surprise came via West Coast-focused Essex , which reported surprisingly solid results and significantly raised its full-year growth outlook, citing strength in Southern California markets, which offset relative weakness in Northern California and Seattle. Downside surprises have come from REITs focused on the middle-tier market segment, where we've seen an uptick in bad debt expense and a more pronounced deceleration in rent growth. Small-cap NexPoint Residential has been the laggard after lowering its NOI outlook citing weakness in its Class B properties in Atlanta and Las Vegas, and lowering its FFO outlook as it works through disruptions in asset sale plans.

{kind=link}

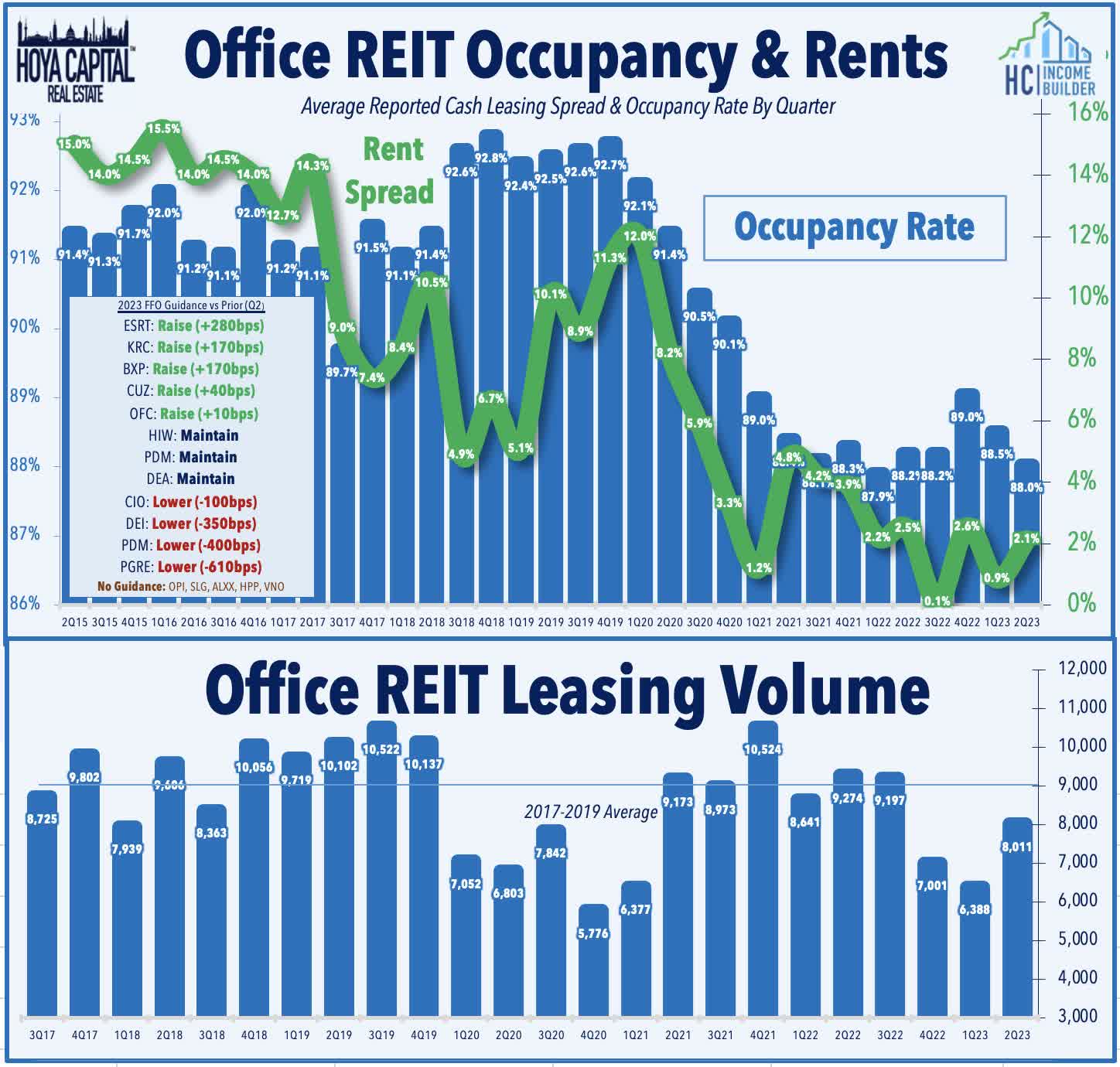

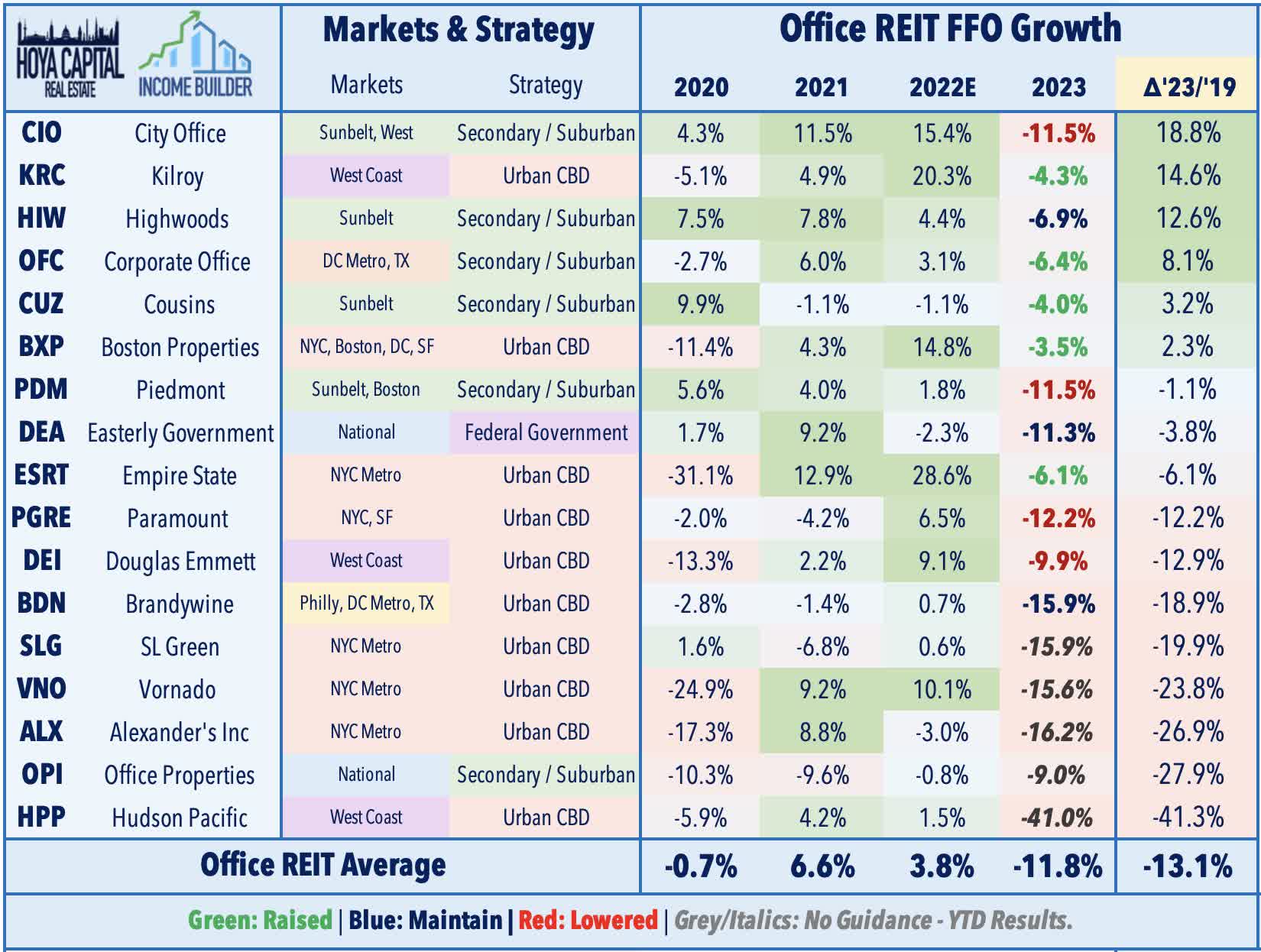

Office : (Final Grade: B+) The battered office REIT sector has led the gains this earnings season on the heels of a slate of surprisingly solid reports showing that leasing activity and pricing trends do indeed appear to have rebounded in recent months, with total volume trending toward levels that are only slightly below the pre-pandemic averages after two historically weak quarters. Five office REITs raised their full-year outlook this earnings season, including the largest office REIT - Boston Properties - which recorded leasing volume of 938k square feet - up from 660k in the prior quarter - and achieved renewal rent spreads of 6.3% - the strongest since Q2 of 2022. NYC-focused Empire State Realty also raised its guidance driven by strong leasing volume of 336k square feet - above its pre-pandemic average from 2017-2019 - and achieved effective rent increases of 10.1% on these leases. Sunbelt-focused Cousins also raised its full-year FFO growth outlook and recorded rent growth of 7.9% on leasing volume of 435k square feet - each an acceleration from last quarter. Corporate Office - another Sunbelt-focused REIT - also boosted its full-year FFO growth outlook and recorded its strongest quarter of leasing activity and occupancy since 2021. The third Sunbelt REIT - Highwoods - reported leasing activity of 918k square feet - 16% above its four-quarter average - and achieved cash rent growth of 0.5% on these leases.

{kind=link}

Office REITs received more good news this week after tech firm Zoom - a company that has been the "poster child" of the Work from Home Era - made a splash by calling its employees back to the office. A memo to employees detailed a new "hybrid" approach to WFH where by employees who live near a Zoom location must be on-site at least two days per week, a move that comes alongside a recently-announced workforce reduction, consistent with the theory that office utilization rates will actually improve as job growth cools and as workers yield some negotiating leverage. Results from West Coast-focused REITs have been notably weaker, however. Paramount reported very weak results and significantly lowered its full-year outlook driven by the bankruptcy of First Republic - its largest tenant - and deepening distress in the San Francisco office market. PGRE leased just 72k square feet of space in Q2 - 70% below its pre-pandemic average from 2017-2019. Piedmont also lagged after it announced the refinancing of $400M in debt at a sharply higher interest rate - 9.25% compared to its maturing 4.45% note - which prompted a downward revision to its FFO outlook.

{kind=link}

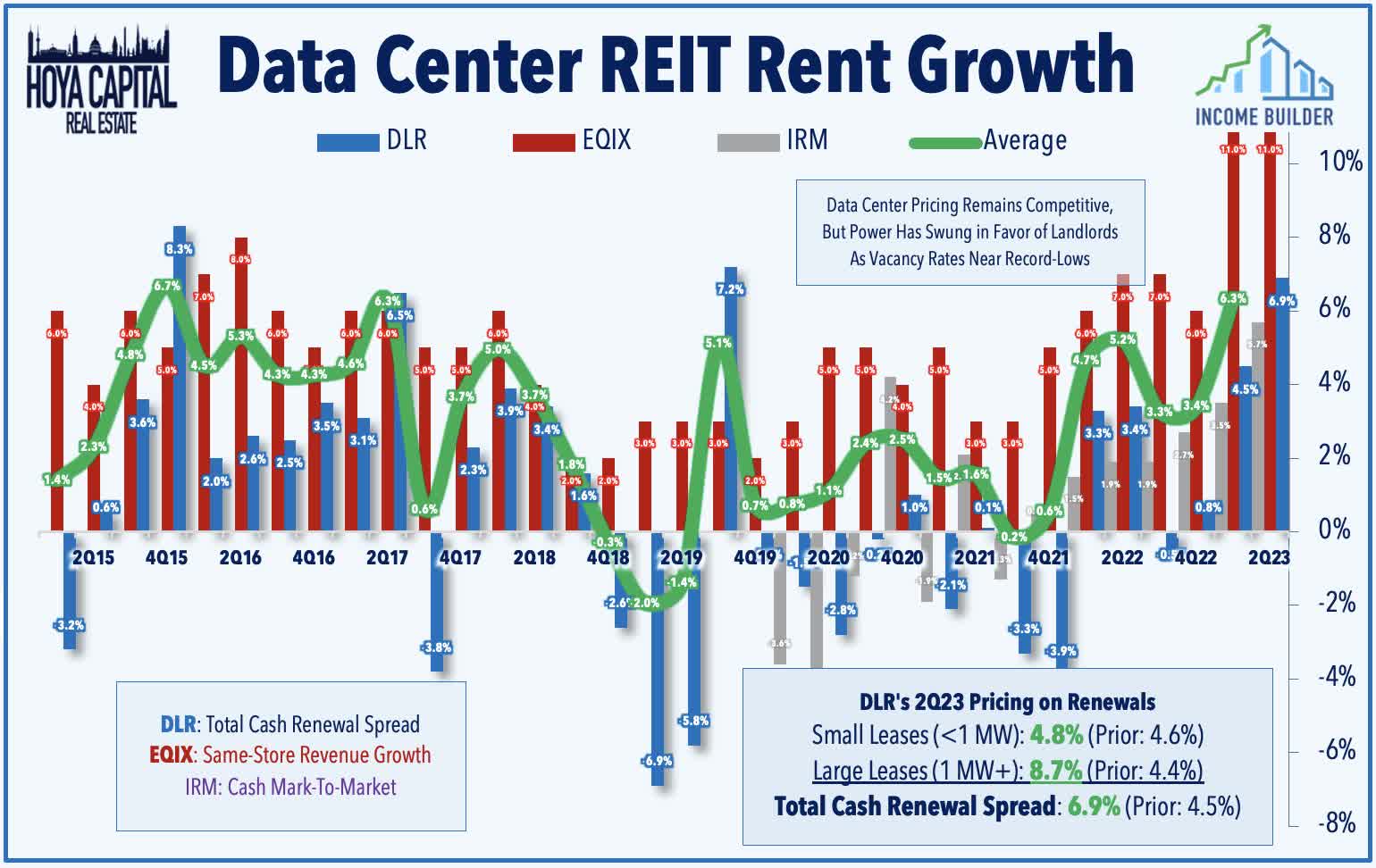

Data Center : (Final Grade: B+) Pricing power remained impressive for data center REITs as AI-driven demand has clashed with a confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - to create a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Digital Realty reported cash re-leasing spreads of 6.9% - the highest in three years - with notable strength from larger leases which posted rent spreads of nearly 9%, which had been an area of weakness in recent years. DLR trimmed the midpoint of its full-year FFO outlook due to unpaid rent from Cyxtera - which declared bankruptcy earlier this year - but raised its outlook for cash re-leasing spread and same-store NOI growth by 100 basis points each. Equinix reported solid results and boosted its full-year FFO outlook by 80 basis points to 7.7%. driven by "same-store" recurring revenue growth of 11%. Iron Mountain maintained its full-year outlook across both its business storage and data center segments.

{kind=link}

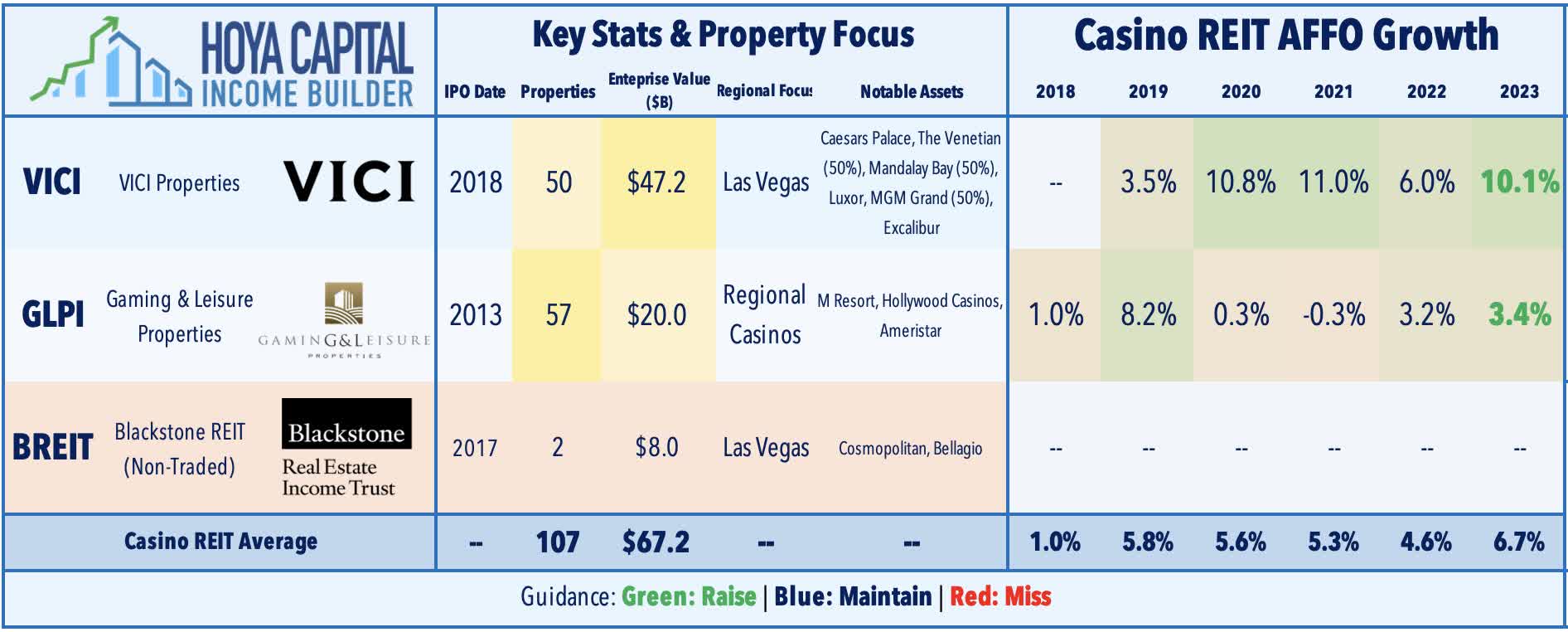

Casino : (Final Grade: B+) Heralded last year for their inflation-hedging characteristics, casino REITs have faced the other side of that trade this year as inflation normalizes from the four-decade highs seen last year, but have been among the better-performers this earnings season on the heels of a pair of solid reports. VICI Properties raised its full-year FFO growth target to 10.1% - up 50 basis points from last quarter - while Gaming & Leisure Properties hiked its FFO growth target to 3.4% - up 60 basis points from last quarter. M&A opportunities were again the focus of both REITs' earnings calls in light of recent reports that Blackstone may be looking to sell its stakes in the Bellagio and Cosmopolitan. VICI indicated that the current asking price on the Bellagio would be "dilutive." VICI did announce a $300M investment into resort owner Canyon Ranch, which would grant VICI the option to acquire the real estate assets of its two resorts in Arizona and Massachusetts. VICI noted that Las Vegas is continuing to see record traffic, and noted that regional casinos are performing well "as the high-value consumer segment remains healthy." GLPI - which has been quiet on the M&A-front since last June - noted that tighter credit conditions have made it difficult to source new deals.

{kind=link}

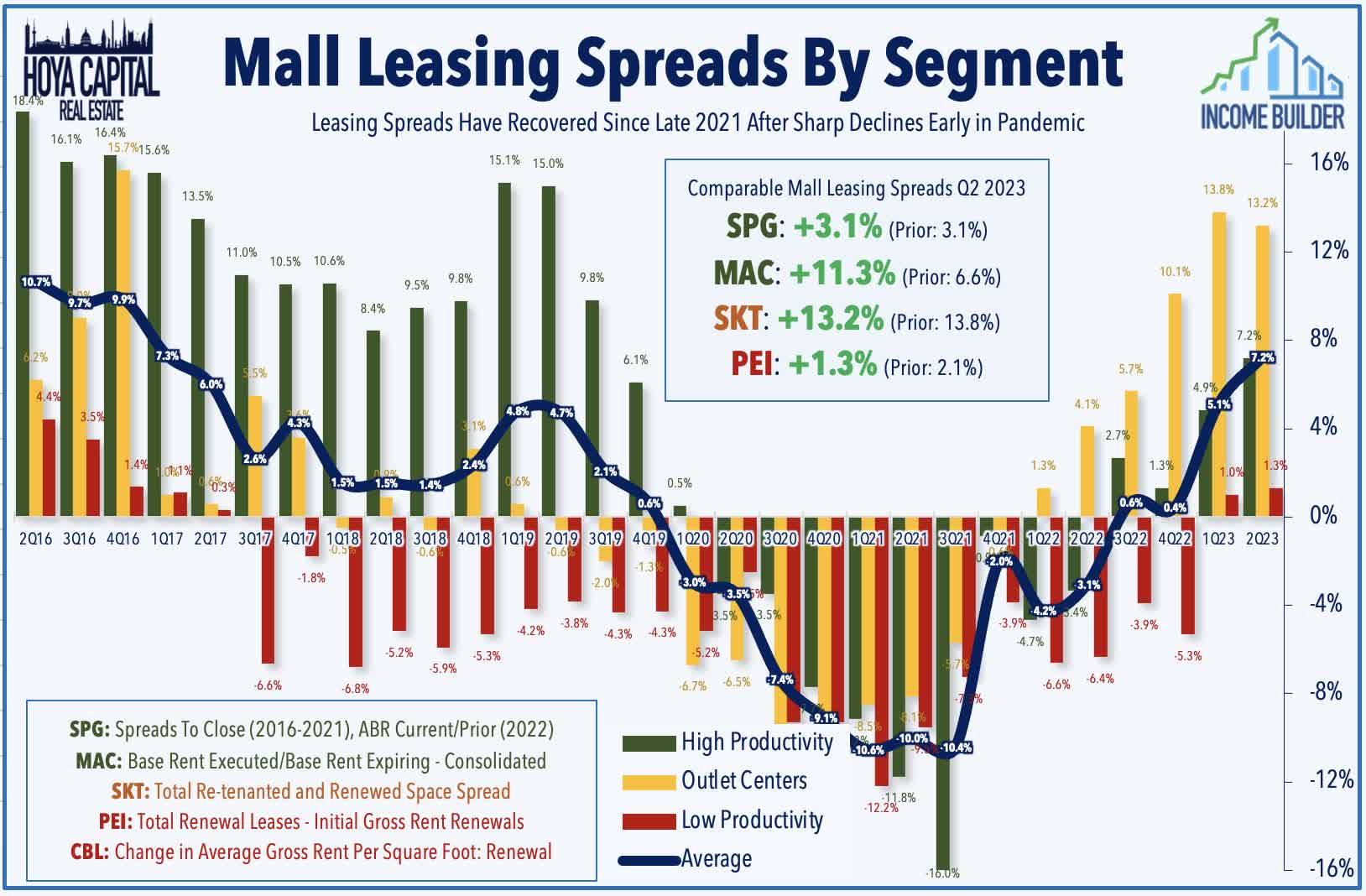

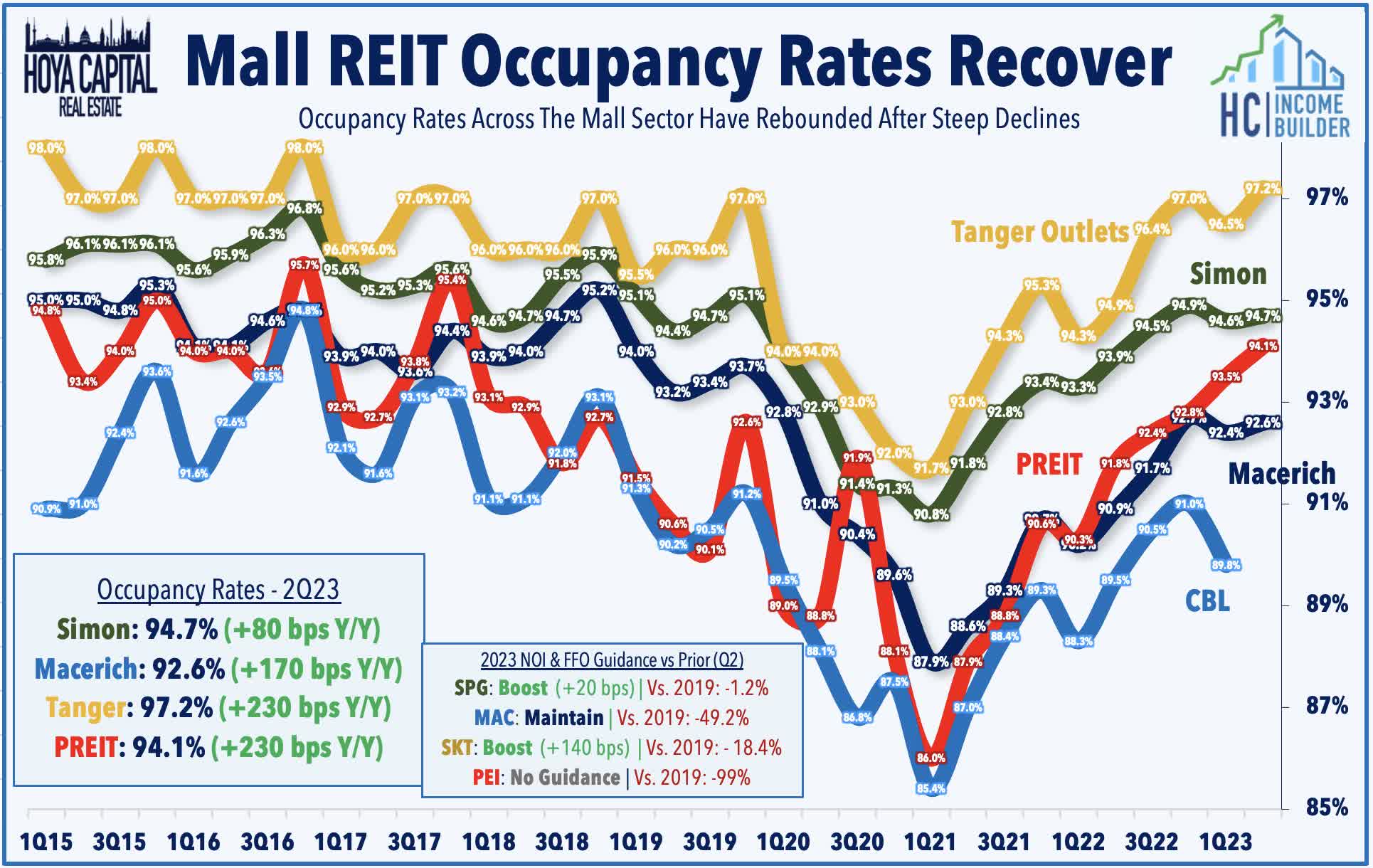

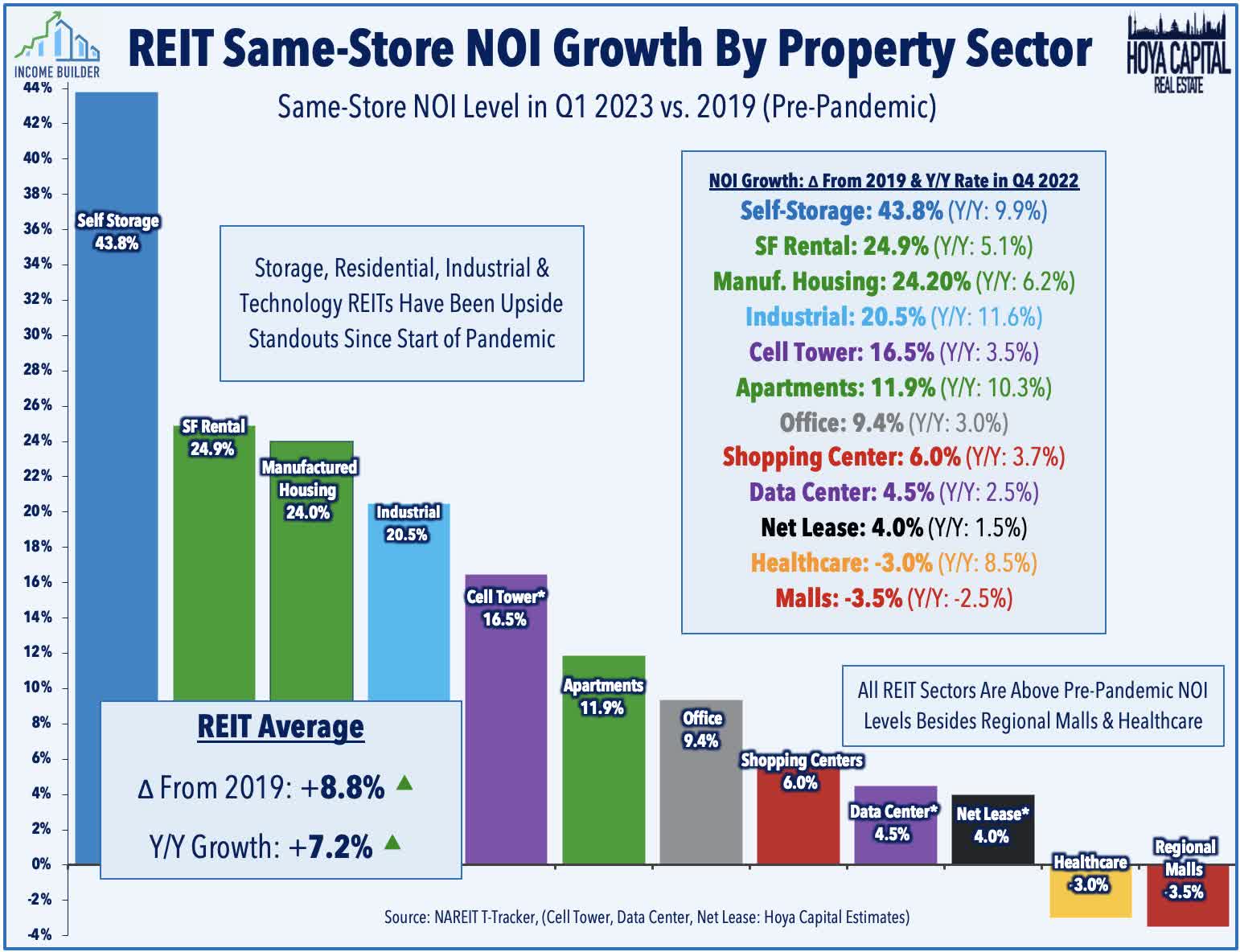

Malls : (Final Grade: B) While not displaying the outright strength seen in the strip center format, mall fundamentals have stabilized in recent quarters with occupancy rates rebounding to the cusp of pre-pandemic levels while rental rates have turned firmly positive following a dismal stretch of negative growth from late 2019 through mid-2022. Tanger Outlets reported strong results and raised its full-year outlook on robust leasing volume and improving pricing power. Driven by over 2 million square feet of leasing activity in Q2, portfolio occupancy improved to over 97% for the first time since late 2019, and Tanger achieved blended spread of 13.2% on these leases - its sixth-straight quarter of positive spreads following a stretch of 11 straight quarterly declines.

{kind=link}

Macerich also has been an upside standout after reporting that its consolidated portfolio occupancy increased to 92.6% - up 170 basis points from last year. Re-leasing spreads increased by 11.3% on a trailing twelve-month basis, up from 6.6% last quarter and marking its strongest quarter since 2019. Leasing volumes were up 34% through the first six months of this year compared to the same period last year. MAC reiterated its guidance calling for FFO decline of 8.2% this year as interest expense remains a significant drag on its earnings. Results from Simon Property were decent, driving a modest boost to its full-year FFO outlook, but underlying occupancy and rent growth improvements weren't as strong as its peers.

{kind=link}

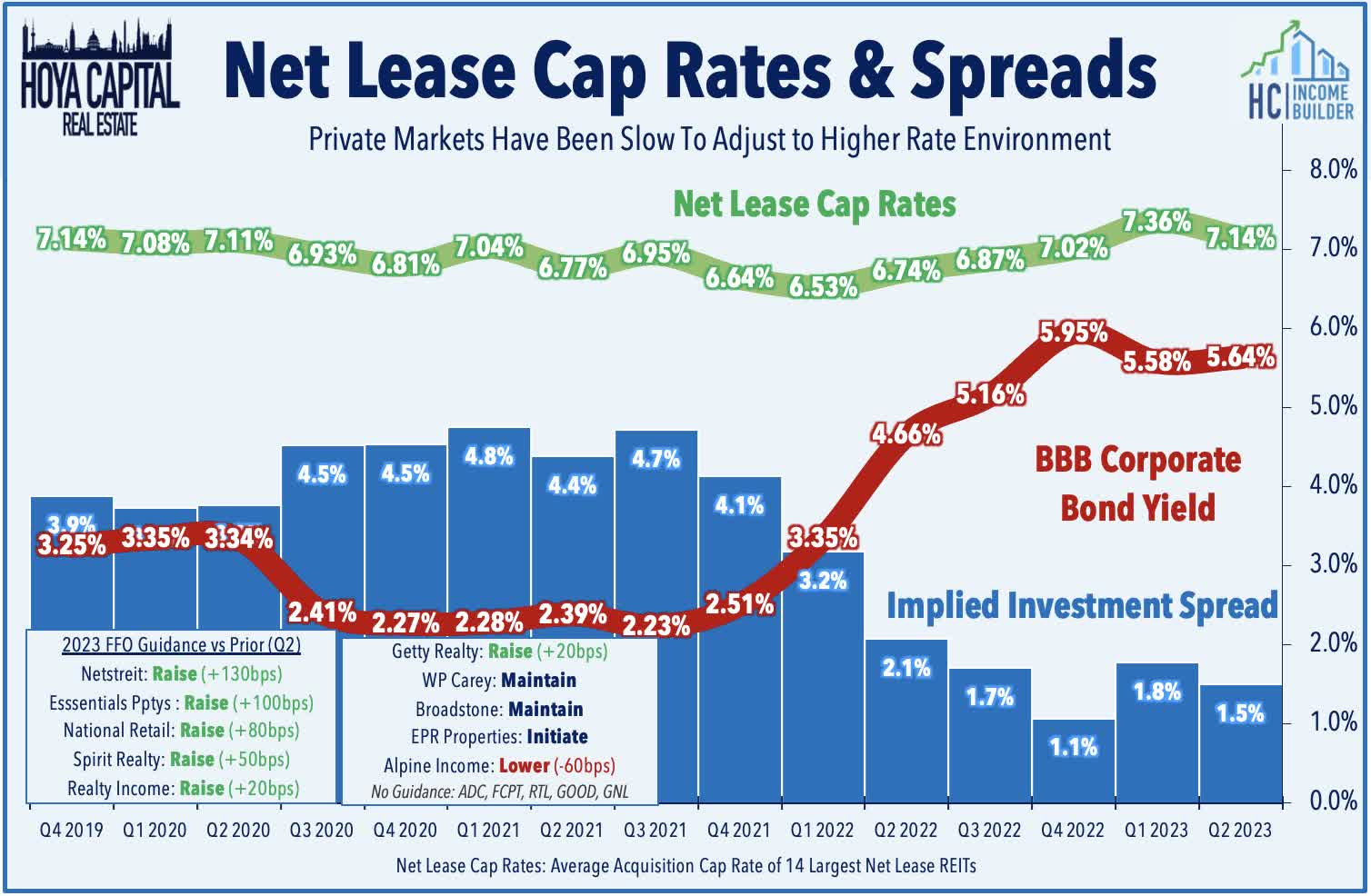

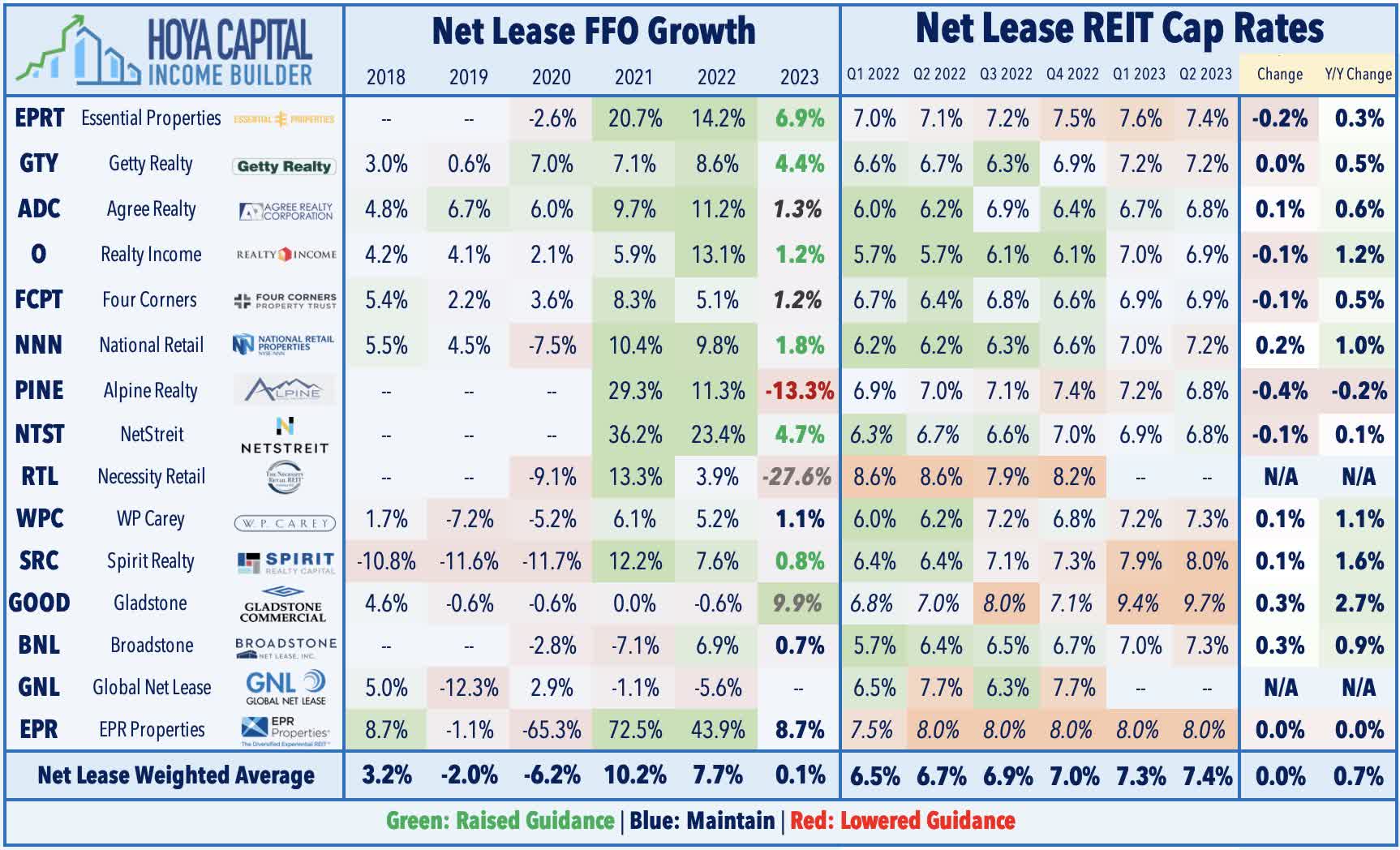

Net Lease : (Final Grade: B) Six of the 10 net lease REITs that provide guidance raised their full-year outlook, as strong underlying retail performance has helped to offset a more challenging acquisitions and financing environment. Cap rates remained sticky in the second quarter as private market property owners have generally been slow to adjust their valuation expectations to the higher interest rate environment, which has prompted most net lease REITs to scale-back acquisition plans until either market cap rates increase or financing costs decrease. On average, net lease REIT acquisition cap rates increased 60 basis points from last year to roughly 7.1%, during which time benchmark financing rates (as implied by the BBB Corporate Bond Yield) increased by over 100 bps.

{kind=link}

Spirit Realty was among the upside standouts after lifting its full-year FFO growth target to 0.8% - up 50 basis points from its prior outlook - and noting that its average acquisition cap rate climbed to 8.0% in Q2 - up 160 basis points from last year. Realty Income , meanwhile, boosted its outlook by 20 basis points to 1.2%, while four other REITs also lifted their guidance: Netstreit raised its full-year FFO outlook to 4.7%, Essential Properties raised its outlook to 6.9%, and Getty Realty increased its FFO growth outlook to 4.4%. On the downside, W. P. Carey maintained its full-year outlook and noted that it sees its rent growth "peaking" this year at around 4% as the tailwinds from the CPI linkage become modest headwinds into 2024 given the recent inflation trends.

{kind=link}

Takeaway: Strength From Unexpected Sources

While there were some of the usual suspects among the Winners of REIT Earnings Season - namely residential and industrial REITs - we also saw strength from unexpected sources: retail and office REITs. Retail REITs - particularly within the strip center format - have enjoyed an under-discussed revival over the past 18-24 months as store openings have considerably outpaced store closings over the past two years, driving occupancy rates to record highs and fueling impressive double-digit rent growth. Office REITs have posted the strongest stock performance this earnings season as results have been "less bad" than feared, and there are signs that the "return to the office" may be picking up steam. Meanwhile, buoyant residential rent growth fueled a strong set of reports from single-family rental REITs and mostly-solid results across the multifamily and senior housing sectors. While we were impressed by this strength from previously beaten-down sectors, we also saw some unexpected weakness from several previously outperforming sectors including storage, manufactured housing, and cell tower REITs, which we'll discuss in Losers of REIT Earnings Season later this week.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Winners Of REIT Earnings Season