LDNXF - Wolters Kluwer: A Bullish Outlook For Growth And Value Creation

2023-07-14 12:16:32 ET

Summary

- Wolters Kluwer is a global provider of professional information, software solutions, and services.

- We expect revenue growth, as its quality business model and wide moat allow the business to exploit industry trends, such as AI.

- The company currently has an EBITDA-M of 30%, with scope for further improvement as the business benefits from scale and sticky revenue.

- Distributions to shareholders have been substantial, as Management shrewdly allocates capital.

- With a strong relative performance to its industry, we believe the business is well priced for long-term value.

Investment thesis

Our current investment thesis is:

- Wolters Kluwer (WTKWY) has a fantastic business model, with recurring software revenue, as well as a wide moat.

- Growth has been strong, with the outlook positive based on AI developments, ESG, and further demand for data services.

- Margins have consistently improved as scale and service development continue to drive value.

- Relative to peers, the business looks highly attractive. Despite this, it is only trading at a small premium.

Company description

Wolters Kluwer is a leading global provider of professional information, software solutions, and services for various industries, including legal, tax, healthcare, finance, and compliance.

Share price

WK's share price has performed well in the last decade, returning more than double that of the S&P 500. This is a reflection of its impressive financial improvement during this period, implying commercial and financial superiority.

Financial analysis

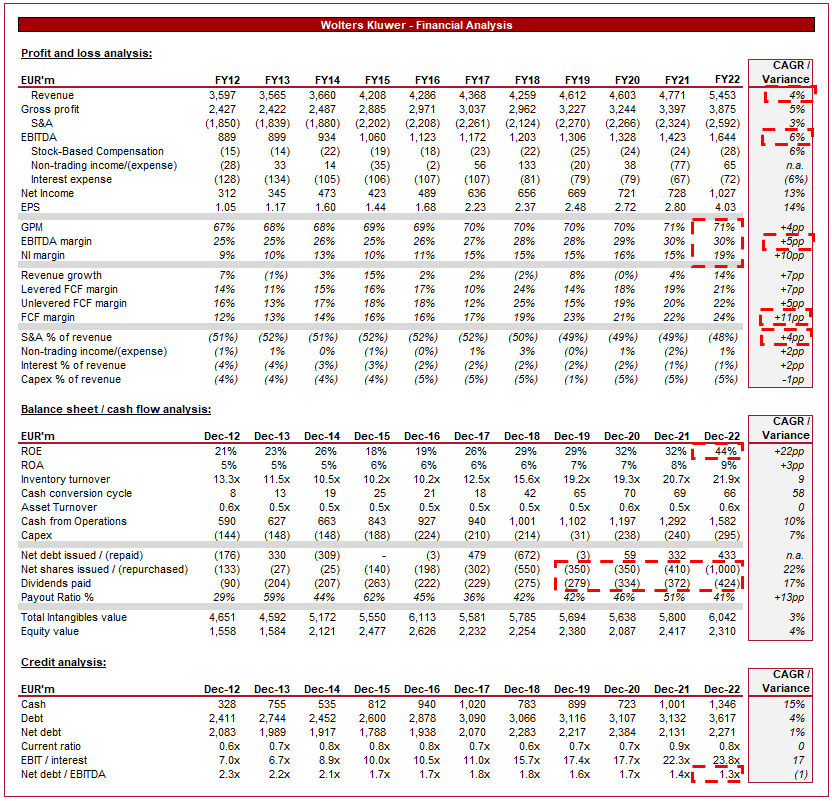

Wolters Kluwer financial analysis ( Wolters Kluwer)

{kind=link}

Presented above is WK's financial performance for the last decade.

Revenue & Commercial Factors

WK's revenue has grown at a mild CAGR of 4% in the last 10 years, with generally consistent growth YoY. As a global business, the company faces a degree of FX risk, partially contributing to volatility.

Business Model

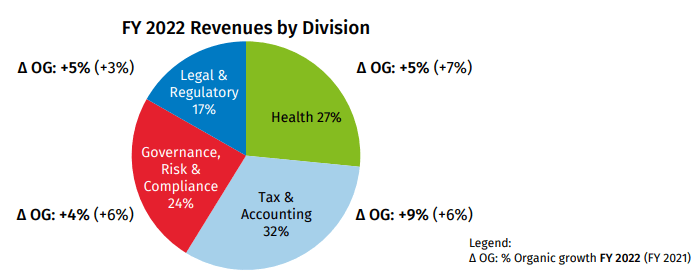

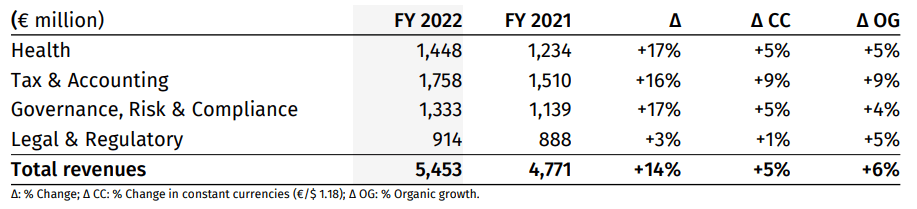

WK operates through four main divisions:

- Health: Provides evidence-based clinical decision support, clinical documentation, and patient engagement solutions for healthcare professionals.

- Tax & Accounting: Offers software solutions, research tools, and services to tax, accounting, and audit professionals.

- Governance, Risk & Compliance ('GRC'): Provides regulatory compliance and risk management solutions to financial institutions, legal professionals, and corporate compliance officers.

- Legal & Regulatory: Delivers expert legal information and software solutions to law firms, legal departments, and professionals.

WK's revenue profile is highly diversified, with no single segment representing more than 35% of total revenue. Given the wide range of industries targeted, this reduces dependency on any single industry for growth. Also, the business has significant exposure to non-cyclical industries, further reducing the risks to revenue.

Revenue by division (Wolters Kluwer)

{kind=link}

All segments are currently growing well, with healthy organic growth. Despite the 4% rate looking mild, we must remember the business operates within mature industries. Exceeding the long-term target growth rate is a commendable achievement.

{kind=link}

The company's objective is to empower professionals with information they can trust, and increasingly insights that can assist with making informed decisions, driving commercial improvement and productivity. Access to usable information is not readily available, especially when manipulated to enhance value, representing a key value proposition to Corporates. The value proposition continues to develop as we transition into a data-driven era.

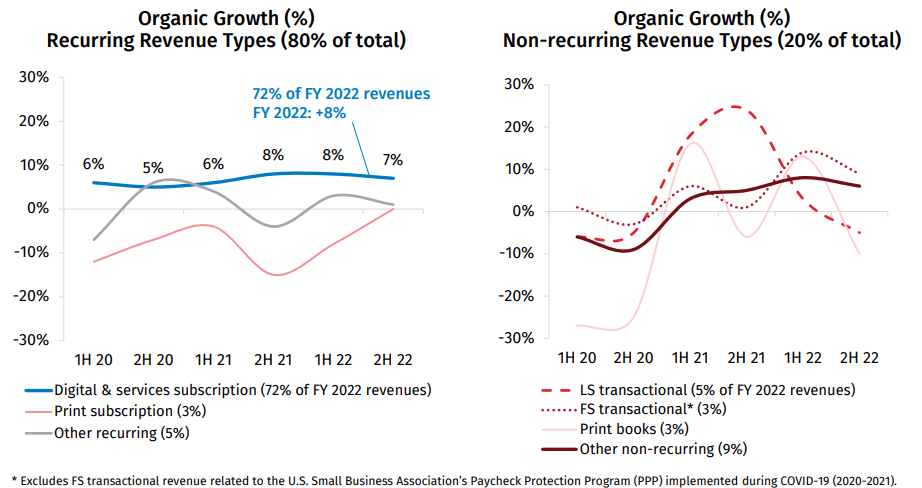

WK's revenue is also highly attractive due to its nature. 80% of its revenue is recurring in nature, with clients committed to regular payments in exchange for access to WK's services. Recurring revenue gives WK greater certainty over forward revenue, allowing the business to focus on new customer wins. Additionally, this reflects the quality of WK's services as customers are willing to maintain long-term contracts.

Recurring revenue (Wolters Kluwer)

This quality is illustrated below, as growth has been incredibly consistent and at above-average levels, compared to non-recurring, which generally fluctuates with market conditions and demand.

{kind=link}

Within this recurring segment is a key growth area for the business, namely cloud software services. WK has achieved impressive growth in recent years, as technological development and changing working conditions drive the implementation of cloud-based solutions. We expect this to be a key growth area in the coming years.

Software (Wolters Kluwer)

WK has recently launched a new division, bringing together existing assets to exploit the current growth in ESG. We consider this a lucrative segment, given the regulatory and social pressures continuing to propel this industry forward. By creating a department, a dedicated team can focus on the development of its offering.

Pro-forma revenue (Wolters Kluwer)

Competitive Positioning

WK's competitive advantage revolves around 3 key factors:

- WK's various services have a large brand awareness and market presence, allowing the business to compete for new work.

- The company's comprehensive databases, publications, and research materials (alongside deep expertise) are only rivaled by a few other businesses globally.

- WK consistently invests in technology advancements keeping the company's offering at the forefront of the industry.

Data Industry

Companies differentiate themselves through industry-specific focus, deep content libraries, a breadth of value-added support, and technology-driven solutions. In many cases, clients will hold subscriptions across several leading firms, reducing the degree of head-to-head competition among peers.

WK faces competition from companies such as Thomson Reuters ( TRI ), LexisNexis ( RELX ), Clarivate ( CLVT ), and Bloomberg in specific segments of its business. The wider data industry also includes Experian ( EXPGY ), Equifax ( EFX ), TransUnion ( TRU ), LSEG ( LDNXF ), and Verisk ( VRSK ).

As touched on previously, the shift towards digital platforms and cloud-based solutions is contributing to increased digital services (and reduced services, print, etc). This should contribute to continued margin improvement, although to a far less extent given the transition has broadly occurred.

AI is a key development in the industry, as some have suggested it could replace the provision of data solutions. We see this as the biggest opportunity in the industry since the advent of the internet. The use of generative AI alongside a deep content library will allow WK (and others) to significantly increase their value-added proposition, as analytics and insight can be tailored in real-time to changing scenarios.

Increasing regulatory requirements across industries will continue to drive demand for compliance and risk management solutions. The complexity of business operations only look to be increasing, implying this should be a sustainable trajectory.

Continued growth in emerging markets represents a key opportunity for WK, as the need for greater support and data services will drive demand for Western solutions.

Margins

WK's margins are impressive, with an EBITDA-M of 30% and a NIM of 19%. Margin improvement has been driven by a transition toward software services, increased scale economies, and positive pricing action.

Margins across the division are relatively homogenized, with only L&R significantly underperforming. This said, it is the lowest segment in the business, thus not overly concerning.

{kind=link}

Q1

{kind=link}

In the most recent quarter, WK continues its strong growth trajectory, with revenue up 5% and Recurring revenue outperforming. This illustrates the company's resilience to any type of external factor, given the diversification and attractive nature of revenue.

The only concern is that margins have slightly slipped, with inflationary pressures impacting personnel costs. We expect there is a degree of mismatch here, as WK will look to increase subscription prices over the coming 12-18 months as they are renewed in order to pass these costs on.

For this reason, we expect margins to bounce back and eventually continue their improvement trajectory.

Balance sheet & cash flows

WK's balance sheet is fairly uneventful. The company is conservatively financed, owing to its impressive cash flows and moderate Capex requirements. Capital is allocated healthily to distributions, with both dividends and buybacks.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

As the business is providing a sticky service with a diversified revenue stream, we expect revenue to grow at a consistent level in the long term. Analysts have a similar view, forecasting a continuation of the recent growth rate.

Margins are expected to gradually improve, a reasonable estimate as scale grows.

Industry analysis

Research and Consulting Services (Seeking Alpha)

{kind=link}

Presented above is a comparison of WK's growth and profitability to the average of its industry, as defined by Seeking Alpha (30 companies).

WK performs extremely well relative to its peers. The business is slightly lagging in revenue growth, a characteristic of its scale that restricts its ability to generate substantial upside, but is made up for in profitability growth.

Profitability is substantially higher than the peer group, with ROE illustrating that this is efficiently generated. The business is not the largest in the industry yet is comparably impressive. RELX and Thomson Reuters, for example, have significantly higher revenue while being within 1ppt at an EBITDA level.

Based on this, we would suggest a premium valuation is warranted relative to its peer group.

Valuation

{kind=link}

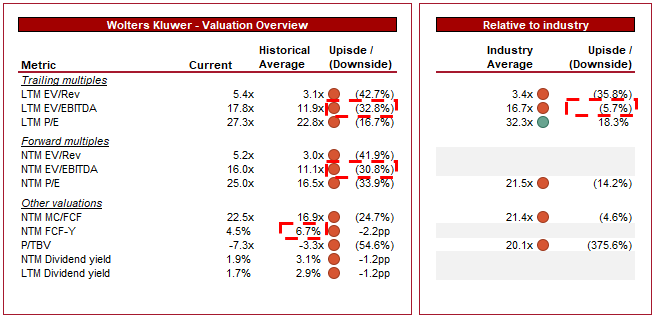

WK is currently trading at 18x LTM EBITDA and 16x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is undeniably warranted, given the scale and margin improvement. With a strong business model and industry tailwinds ahead, we believe a stable growth trajectory is ahead.

Interestingly, the business is only trading at a small premium to the wider industry. This suggests upside to us, given the significant margin superiority.

The two valuation methods imply differing conclusions. This historical average view implies no material upside, as the c.30% premium looks fairly rich, even if the business has noticeably improved. Relative to peers, however, the business looks cheap, although not materially so.

Relx is trading at 22x LTM EBITDA while Thomson Reuters is at 29x. This implies WK has further room for upside, although potentially not substantially so.

Key risks with our thesis

The risks to our current thesis are:

- AI. Although we see AI as a key opportunity, successful development (compared to WK) by its peers could quickly make this concerning for WK.

- FX. FX Fluctuations could erode underlying revenue growth as income is converted to Euros. Currently, the dollar is declining and so has the potential to be beneficial in the short term.

Final thoughts

WK is a fantastic business. The business model is highly resilient from a downside perspective while representing upside potential with industry tailwinds. The company has the potential to grow at a similar level for a substantial amount of time.

When partnered with high margins and a defensible market position, we consider the business extremely attractive. When compared to peers, WK holds its own, and in many cases, outperforms.

We are strong believers that great companies cost a premium. WK may not necessarily be glaringly cheap but it's not clear if this will ever be the case. We see value at the current share price given its relative valuation, which better reflects current market conditions vs. the historical view.

For further details see:

Wolters Kluwer: A Bullish Outlook For Growth And Value Creation