WRDLY - Worldline: Strong Momentum Boosts Free Cash Flow Result

2023-07-29 10:40:00 ET

Summary

- Worldline SA is a large French payment services provider. It is still digesting the acquisition of Ingenico.

- This weighs on the results, as the transaction and integration expenses remain relatively high.

- On a normalized basis, the earnings and free cash flow results remain strong. Margins should increase further from here on.

- Worldline has announced a new joint venture with Crédit Agricole, a large French bank, but there will be no noticeable contribution before 2025.

Introduction

In a previous article , I mentioned it didn’t look like Worldline SA ( WRDLY , WWLNF ), a world leader in payment solutions headquartered in France, would be able to meet my free cash flow projections for 2024. I am keeping an eye on the company’s performance to make sure the timeline to reach the 3 EUR per share in free cash flow doesn’t slip by too much. Unfortunately Worldline only publishes detailed financial results every six months, and while the interim trading updates are always interesting, the half-year and full-year reports provide a more detailed look under the hood. This article is meant as an update to previous articles, and I’d recommend you to have a look at those older articles here to get up to speed on the business model.

{kind=link}

Worldline has its primary listing in Paris, where it's trading with WLN as its ticker symbol . The average daily volume in Paris is approximately 600,000 shares for in excess of 20M EUR per day (I will use the Euro as base currency throughout this article). The current market cap of the company is approximately 9.8B EUR, as there are just under 283M shares outstanding.

On track to meet my cash flow expectations

In my previous articles, I was focusing on the company’s near-term objectives rather than the "instant satisfaction" of the most recent results. As explained in the introduction, my investment thesis is centered around the free cash flow performance of the company, and I was (and still am) aiming for a sustaining free cash flow result of 3 EUR per share in 2024.

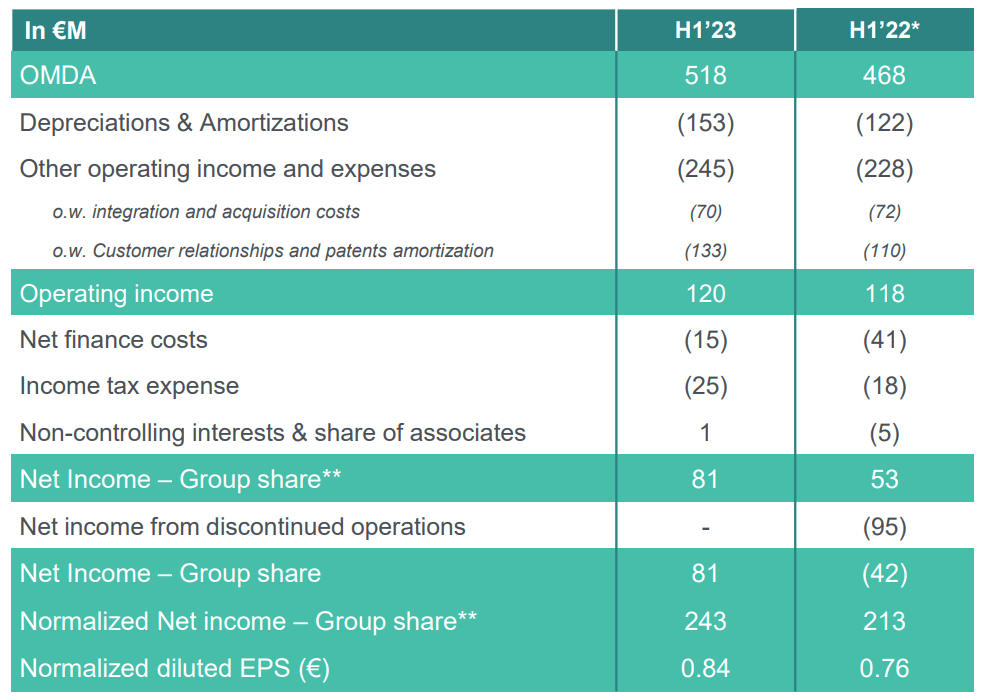

I was happy to see Worldline reported a 9.3% organic revenue increase thanks to a very strong performance in the merchant services division, which provided an impressive boost to the margins. And while the net income does not appear to be extremely impressive with a reported net income of just 81M EUR, the normalized net income of 243M EUR represents an increase of almost 15% compared to the first half of last year. The normalized diluted EPS increased by 11% to 0.84 EUR per share.

{kind=link}

The large difference between the reported net income and the underlying net income is caused by a (traditionally) high amortization expense related to customer relationships and patents, while the company also included about 70M EUR in integration and acquisition expenses in its H1 income statement.

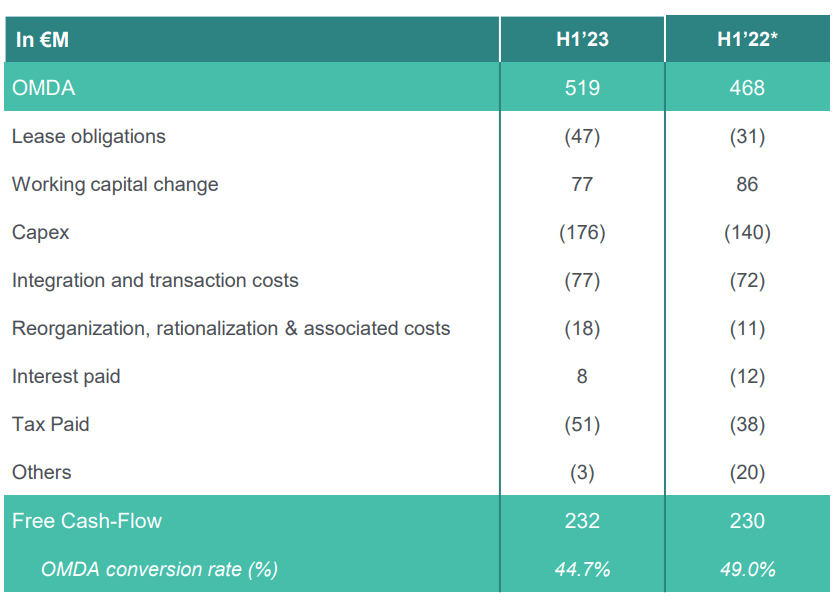

As explained before, I’m mainly interested in the cash flow performance of the company, and just like in the first half of last year, there are some adjustments to be made when looking at the cash flow summary. The starting point is the OMDA, the Operating Margin before Depreciation and Amortization. And as you can see below, the free cash flow result was 232M EUR.

{kind=link}

However, this included a 77M EUR contribution from changes in the working capital position but it also included a 77M EUR integration and transaction related cash outflow as well as a 18M EUR reorganization cash outflow. Additionally, the company paid 51M EUR in cash taxes although only 25M EUR is due based on the H1 income statement .

This means the underlying free cash flow result is approximately 44M EUR higher than the reported free cash flow result. Expressed in absolute numbers, the underlying free cash flow (excluding restructuring and integration expenses) was 276M EUR. This represents approximately 95 cents per share. Even on an annualized basis, that’s not even close to the 3 EUR per share I was anticipating for next year, but let’s not forget there are several factors that still have to come into play.

{kind=link}

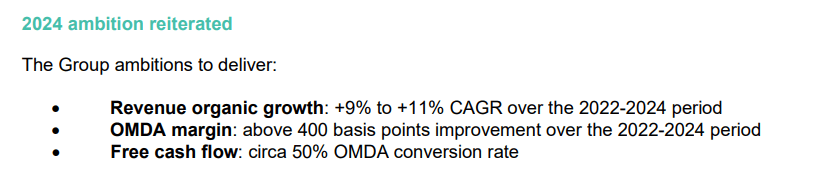

As you can see above, the company expects next year’s revenue to increase again by a similar percentage (the H1 2023 revenue growth rate was on the lower end of the 2022-2024 CAGR guidance), while more importantly, the OMDA margin should increase by 400 bps (while we only saw a 100 bps increase in the first half of this year). Additionally, the conversion rate of OMDA into free cash flow should increase to 50%.

The OMDA margin in H1 was just 23.1%, an increase of just 80bps compared to the 22.3% in H1 2022. This means that if I would assume a 5.1B EUR revenue in 2024 and a 26% OMDA margin (which would still be lower than the 26.3% margin that Worldline guidance is implying), the anticipated OMDA would be 1.33B EUR. That would be a 27% increase compared to the annualized OMDA result in the first semester of this year thanks to the combination of a higher revenue and a higher OMDA margin). And assuming a 50% conversion rate, the underlying free cash flow result would be around 660M EUR or 2.28 EUR per share.

That’s indeed lower than the 3 EUR per share I am aiming for, but on the one hand I am using the lower end of the guidance, and on the other hand the free cash flow conversion rate will likely still be impacted by transaction and integration expenses (albeit hopefully at a lower level than what we’ll see this year).

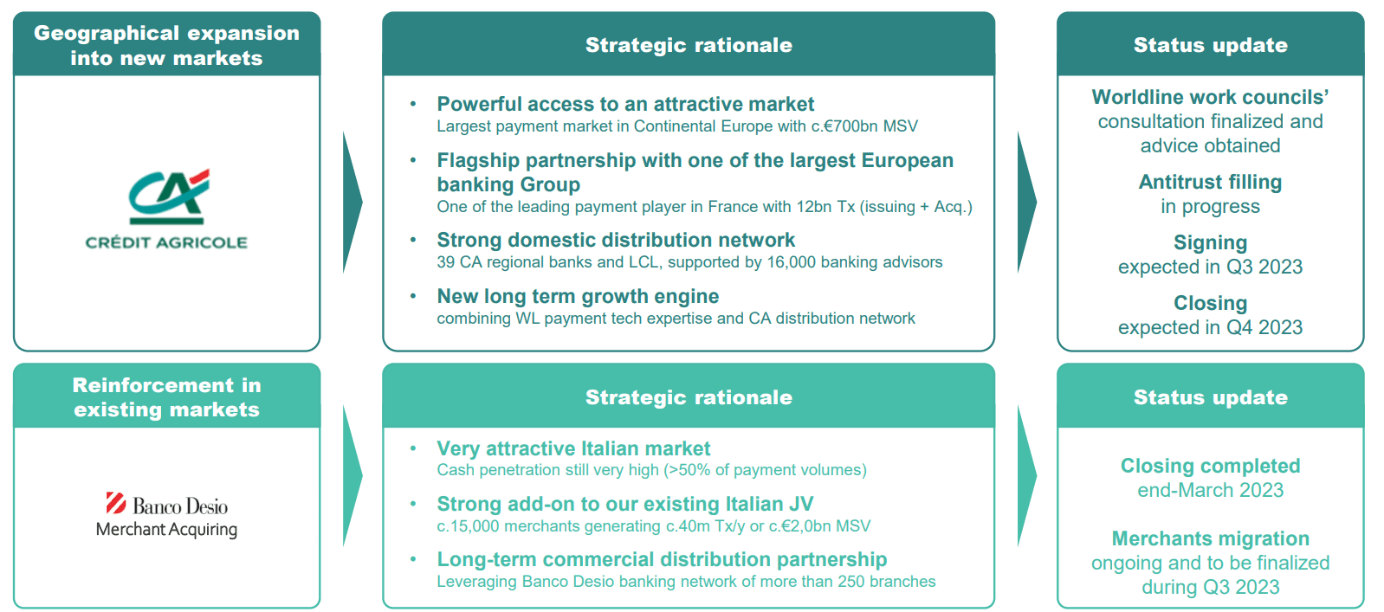

While the H1 results were good, let’s not forget Worldline continues to work on bolt-on M&A ideas which could immediately increase the profitability and free cash flow of the company. Worldline entered into an agreement with Credit Agricole ( CRARF , CRARY ), one of France’s largest banks, to work on a long-term partnership and the creation of a joint venture. This makes sense as this way, Worldline’s technology could be combined with Credit Agricole access to distribution. This joint venture will likely only start to contribute to Worldline’s bottom line from 2025 on as the roadmap envisages an initial investment of 80M EUR in 2023-2024 ahead of the official launch of the joint venture, which should become a dominant player in the payment services landscape.

{kind=link}

Investment thesis

While I am still hopeful to see a full-year free cash flow result of 3 EUR per share in 2024, it looks like I may have to throttle back my expectations a little bit. The momentum is clearly visible in the continuously improving results, but it may take an additional year for Worldline to reach the underlying free cash flow result of 3 EUR per share.

I’m definitely willing to wait for that, as the company’s growth trajectory likely won’t remain limited to just the 2022-2024 plans and I think it’s acceptable to expect another high single digit or low double digit revenue growth in 2025. The analyst consensus estimates are aiming for an EBITDA of 1.65B EUR on a 5.65B EUR revenue, which should result in a net free cash flow result of almost 850M EUR, but I think that’s a bit optimistic.

I currently have no position in Worldline stock, but I am continuously writing put options with a strike price in the low-30 EUR range.

For further details see:

Worldline: Strong Momentum Boosts Free Cash Flow Result